FCO - FCO: 50% Downside Is Possible In A Conservative Scenario

2023-07-05 02:54:49 ET

Summary

- Distributions at over 20% of NAV? No Problem.

- At least that is the current mantra, offset by more and more issuance of units to gullible shareholders.

- FCO has returned less than 0.5% on NAV over the last decade and the current setup looks worse than when we first covered the fund.

The objective of abrdn Global Income Fund Inc. ( FCO ) is to provide high current income to its unitholders and it holds a portfolio comprising of primarily fixed income securities to accomplish that. Its secondary objective is capital appreciation, but only to the extent to which it is consistent with the primary objective. The portfolio held around 344 securities at May 31, 2023, with about a third being rated investment grade. Majority of the investment grade holdings fell in the last rung of that rating.

{kind=link}

As we have seen above, FCO takes a fair amount of credit risk with over 55% of its securities rated below investment grade and most of the balance flirting with the cusp of junk rating (rated BBB). Well, interest rate risk also joins the party with most of the holdings maturing over the medium to long term.

CEF Connect

In terms of geographic reach, the fund does not hold back as evident below.

CEF Connect

We could not capture the last country in the above graphic. For the curious minds with calculators on hand, the last 0.13% allocation was to Estonia.

We started our coverage on FCO back in March 2021 with a strong sell rating and we did not find a reason to change that rating in any of the four subsequent revisits. Few factors remain unchanged for this closed end fund, along with our outlook.

1) Depletion of its Net Asset Value or NAV.

This fund started with a NAV close to $14. When we first laid eyes on the numbers in March 2021, the NAV was a little less than $7 and has now whittled down to a little over $4. FCO has doggedly maintained its 84 cents in annual distributions come rain or sunshine.

{kind=link}

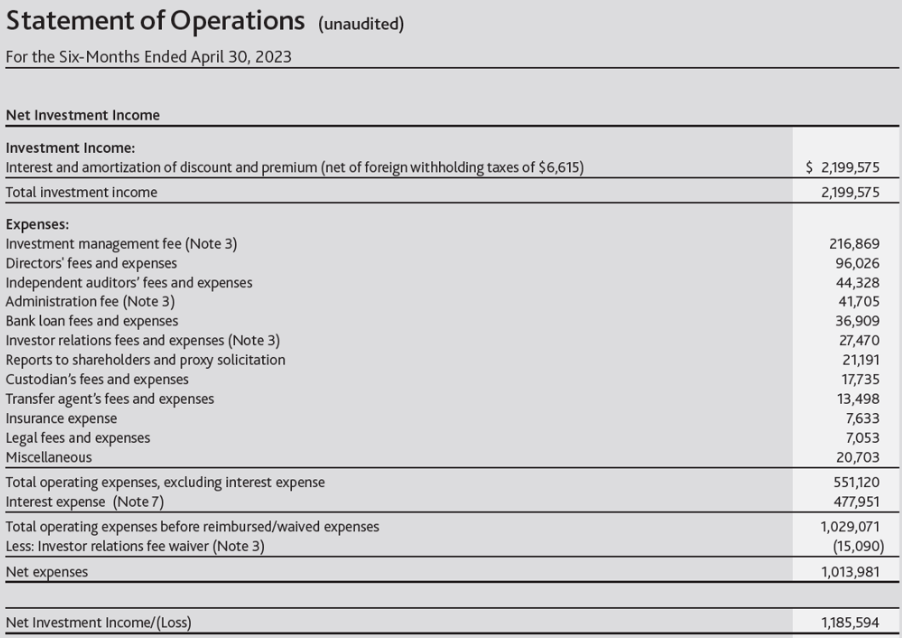

Its net income has fallen woefully short of what it distributes, resulting in return of capital being constant as a portion of each monthly distribution. To illustrate, below we have the numbers from the latest semi-annual financial report showing net income of a little over a million.

{kind=link}

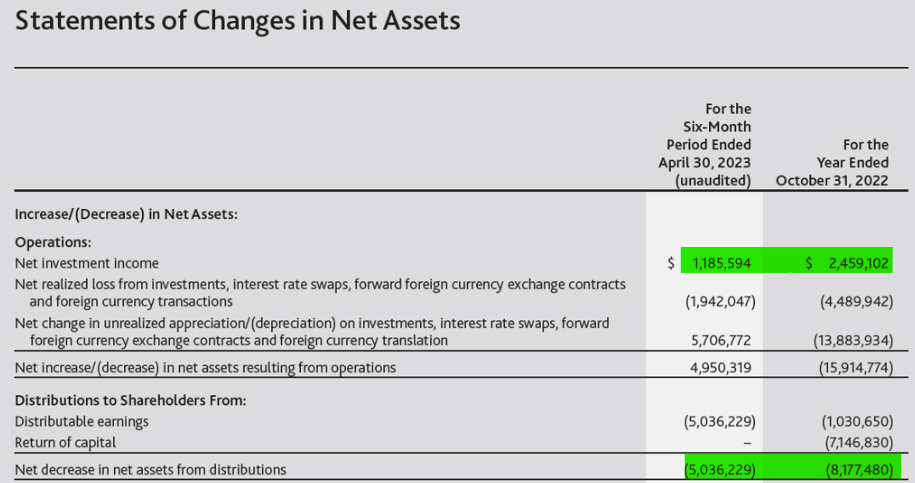

The comparative statement of changes in net assets gives a glimpse of the extent to which distributions exceed the net income.

{kind=link}

Note: While this only shows the recent data, the net income/distribution paid picture has only become worse over our coverage period.

We have ignored the realized gains from the illustration as these generally are offset by losses in other years. Take a look at the returns on NAV for the fund over the last decade.

{kind=link}

At the beginning of our journey with FCO, the 10 year return on NAV was a respectable 2.63%. We are using "respectable" in comparison to the current sub half percent in 10 year returns. There is virtually no fat in this milk. The fund has been steadily returning their investors money in the form of distributions, akin to periodic withdrawals we assume the unitholders are capable of making from their bank themselves.

2) It is capturing the purse strings of the blind income investor. Investors are choosing to pay exorbitant premiums to get in on this NAV depleting exercise.

FCO has won the hearts and minds of investors by holding their distribution steady. As more investors flock into this fund, the unitholders see the capital appreciation funded by the latest investor paying higher premiums than the last and this goes on till there is no greater fool left. We did see some cracks in this foundation over the last two years and that is why, since we started writing on this fund, it has gone nowhere in terms of returns.

Seeking Alpha

However, over the shorter time frame, since our last piece back in August 2022, it has regained the adulation of the income crowd.

Seeking Alpha

Do note the difference in price action between the two articles. Most of the party is funded by the crowd paying increasing premiums for FCO. This also delays the inevitable for the fund and enables issuance of units at premium prices. If not for that, the fund would have had no further capital remaining to return.

Verdict

Fundamentally, things have only got worse, not better for FCO. The party will continue until it does not. Investors willing to pay close to a $1.50 for each dollar of this fund's dwindling net assets are just prolonging the party for the current investors. The last time we downgraded from a strong sell to a "get out of dodge" rating for this fund and concluded with:

This fund continues to remain a strong sell in our opinion . Even based on just the 10-year total return on NAV, which comes in at a painful negative 1.4% per annum, it would be hard to even argue a "hold" rating.

There is no free lunch" would be our message to the investors choosing to buy this at a premium to get in on the "high yield". If this fund traded at a discount like it has done for most of its existence, the management would have cut the distributions by now. As we stand, the fund continues this policy of winding down assets in a most unique manner.

Source: FCO: Losses Proceed On Schedule

We certainly would have thought in an era where you are getting actual risk-free 5.25% returns, this fund would have sunk to at least a discount. Well, it will happen, even if it has not happened yet. With leverage costs up through the roof, we think the fund is going to have a hard time generating even 4% on NAV. It continues to distribute an increasing amount relative to NAV.

The funny thing about those two lines is that fund traded at a discount to NAV for the bulk of the last 10 years. That is until the NAV and price got so badly crushed that the distribution yield jumped and a bunch of yield chasers entered the equation. The saving grace so far has been new unit issuance, which has increased total units outstanding by more than 25% over the last 16 months. Considering the premiums at which this has been done, it has been a modest offset to the NAV depletion. We think the next bear market will break this source of funding and when that happens, the price returns will be truly brutal. Sprint, don't just run.

For further details see:

FCO: 50% Downside Is Possible In A Conservative Scenario