BNDW - FCO And BWG: A Swap Opportunity Presents Itself

2023-07-10 17:31:37 ET

Summary

- The abrdn Global Income Fund is showing signs of an unsustainable high distribution rate and a high premium, which could lead to poor results.

- The BrandywineGLOBAL - Global Income Opportunities Fund offers a more sustainable alternative for global fixed-income investments, despite an elevated distribution, due to its deep discount.

- The biggest risk to this swap is FCO remaining at its current high valuation or pushing even higher into premium territory, producing an opportunity cost if BWG stays at a deep discount and FCO rises.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on June 26th, 2023.

Investors in abrdn Global Income Fund ( FCO ) have seemingly been pushing their luck as the fund displays the exact opposite of what you want to see for a closed-end fund. An incredibly high premium and an unsustainably high distribution rate. This sort of combination often leads to dismal long-term results as the inevitable distribution cut comes. When such a distribution cut actually comes is really anyone's guess. However, every day and month that goes by, investors in FCO are pushing their luck.

However, FCO does have an alternative for investors looking to invest in global income investments. The distribution rate is lower but a bit more sustainable and realistic at this time. That can come from BrandywineGLOBAL - Global Income Opportunities Fund ( BWG ). While that fund has an elevated and unsustainable distribution, the valuation differences between the two are what really sets the funds apart.

BWG is at a deep discount, and any distribution cut is going to be met with a fairly muted reaction. In fact, they cut earlier this year, and the discount widened, but not anything like the extreme reaction we see when funds at premiums cut their distributions. Duff & Phelps Utility and Infrastructure Fund ( DPG ) is the latest example of this when the fund cut its latest distribution by 40%.

YCharts

FCO Basics

- 1-Year Z-score: 2.16

- Premium: 37.75%

- Distribution Yield: 14.95%

- Expense Ratio: 2.25%

- Leverage: 25.32%

- Managed Assets: $68.517 million

- Structure: Perpetual

FCO's investment objective is to "provide high current income by investing primarily in fixed income securities. The Fund also seeks capital appreciation, but only when consistent with its principal investment objective." To achieve this, the fund will "under normal market conditions, invests at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in debt securities."

BWG Basics

- 1-Year Z-score: -1.34

- Discount: -15.12%

- Distribution Yield: 12.05%

- Expense Ratio: 2.62%

- Leverage: 41.22%

- Managed Assets: $268.263 million

- Structure: Perpetual

BWG's investment objective is to "seek current income with a secondary investment objective of capital appreciation." To achieve this, the fund offers a "flexible portfolio that targets sovereign debt of developed and emerging market countries, U.S. and non-U.S. corporate debt, mortgage-backed securities and currency exposure."

Basic Comparison

Both of these funds are quite small, but FCO is incredibly small. They also both utilize leverage, with BWG being much more aggressive on that front. As is the case with most global funds, the fund's expense ratio is also pretty high. When including leverage expenses, it goes even higher. For BWG, it climbs to 3.47%, and FCO has a total expense ratio of 3.11% when including leverage.

They are both having to deal with higher interest rates driving up their borrowing costs. However, part of BWG's leverage is in fixed-rate preferred , Series D and E issuance. These serve to limit the interest rate risk of their borrowing costs. So that's part of weighing BWG over FCO as well; higher leverage means potentially higher risk and greater volatility.

{kind=link}

BWG Fixed-Rate MRPS Leverage (Franklin Templeton)

FCO had been utilizing interest rate swaps to limit the interest rate risk for the fund as well. These were listed in the semi-annual report for the period ended April 30th, 2022. By their annual report for the period ended October 31st, 2022, interest rate swaps were not listed. However, they did provide realized gains to the portfolio during the reporting period.

Valuation Divergence Creates Swap Opportunity

When looking at FCO, they've tended to trade at a premium for a while, but this premium is becoming even more stretched again recently. The fund peaked at premium levels through 2021. This coincided with the broader CEF space reaching historically high valuations in the same year. FCO is trading well above its decade-long average premium.

YCharts

Conversely, BWG is trading below its decade-long average, and the distribution cut earlier in the year likely pushed it there, but the reaction was fairly muted because the fund had already been trading near a 10% discount level. Even if FCO simply reverts to its longer-term average and BWG doesn't move, this would be a winning swap.

In looking back at the last decade of performance between these two, BWG has even been able to top FCO's performance on a total NAV return basis. That is to say, the underlying portfolio of BWG has performed better than FCO. Shareholders on a total price return basis wouldn't have noticed due to FCO's expanding premium.

YCharts

More recent results on a YTD basis show that they've been more correlated on a total NAV return basis. Once again, on a total share price basis, we can see that FCO really has led the way, but the underlying portfolio performance isn't supporting it.

YCharts

Thanks to the large divergence in valuation between these two, the distribution rates aren't all that different in terms of what investors would be "giving up."

Due to FCO's extreme premium, the distribution rate comes to 14.95%. At the same time, BWG's distribution rate comes to 12.05%. On a NAV basis, FCO's distribution rate comes to a stratospheric 20.59%. The large discount for BWG means that the NAV rate comes to a more realistic 10.22%.

Neither fund has provided enough strong results to consider these distributions 'covered.' Net investment income coverage for FCO came to 30% based on their last report. BWG's coverage was much better in their last report, but it only came to ~74%. With the distribution cut and if they manage to produce similar NII, this coverage would be even higher now.

A distribution cut due to FCO's high NAV distribution rate is the biggest potential catalyst for seeing FCO's valuation collapse and investor losses mount. As we saw with DPG recently, that could very well happen to FCO. The premium is even higher in this case, so the fallout could be potentially worse.

Risks To Swap

The biggest risk to this playing out would be FCO remaining at its current high valuation or pushing even higher into premium territory. Therefore, this swap would potentially produce an opportunity cost if BWG stays at a deep discount and FCO rises.

While these funds have shown to correlate pretty closely as both global income funds, it's important also to factor in that they aren't identical funds. The overall credit quality is actually quite close. They both straddle the investment-grade and non-investment-grade credit ratings. Each fund favors below-investment grades but carries a fair bit of investment grade as well.

{kind=link}

Credit Quality Exposure (Fund Websites)

FCO had reported a modified duration of 3.08 years in their last fact sheet . However, it was 6.4 years back in their annual report. That suggests a fairly meaningful change in the fund. BWG's duration was last reported at 8.99 years. That would mean that BWG is more sensitive to interest rate changes, but that is both good and bad.

If the Fed is close to done raising rates and we get a cut next year, that could be a catalyst to see BWG's portfolio perform better. However, if inflation remains sticky and the Fed needs to boost more than anticipated, the reverse could be true. Interestingly, as we saw above, the total NAV return on a YTD basis was exactly the same. So interest rate sensitivity isn't playing a role in the performance, at least during this specific period.

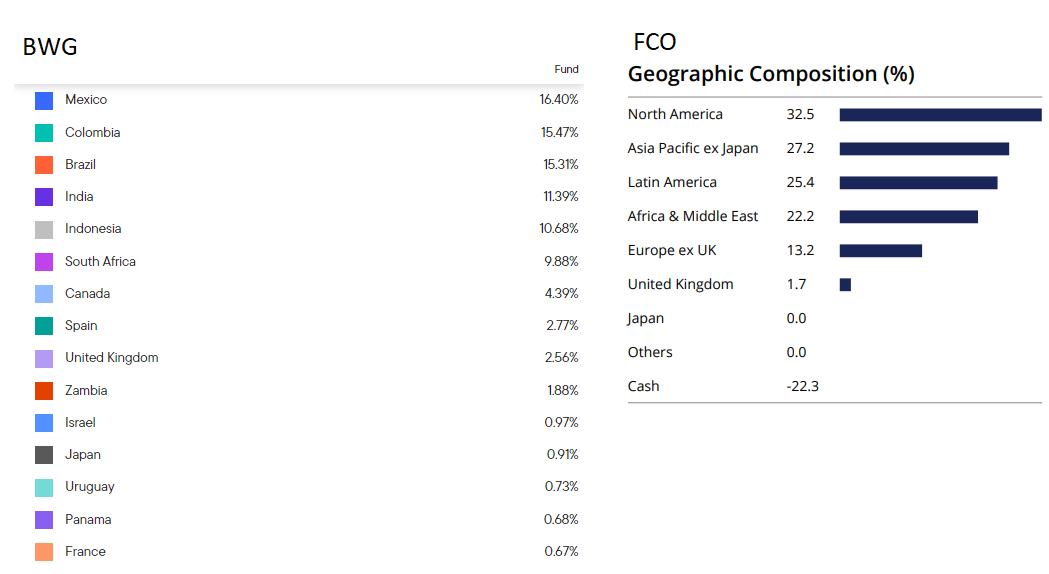

The geographic composition of the funds is also showing differences. For BWG, you are getting more exposure to Latin America. FCO seemingly favors North America, where BWG has very limited exposure to Canada and the U.S. at under 5% with the two combined.

{kind=link}

Geographic Exposure (Fund Websites)

Conclusion

FCO is trading at an extreme premium, not an all-time high, but it's definitely pushing toward that level. That could leave BWG a much better alternative in the global income space for investors who are still looking for a higher distribution rate.

Conversely, an investor could consider some combination of Vanguard Total World Bond ETF ( BNDW ) and VanEck Emerging Markets High Yield Bond ETF ( HYEM ) for non-leveraged ETF exposure. We are pretty limited in comparing historical track records as BNDW was incepted in 2018.

YCharts

However, the idea of mixing BNDW and HYEM would be because BNDW is invested most heavily in the U.S. by around 50%. The overwhelming majority of the portfolio is invested in investment-grade debt, with nearly 35% in U.S. Government debt. That's where HYEM would come in to provide a tilt towards below-investment grade exposure to emerging market economies. Almost the entire portfolio is positioned below investment-grade quality, and the fund offers limited exposure to the U.S. That would make it mirror closer to how FCO and BWG are positioned.

The downside to considering ETFs is being unable to buy at substantial discounts. However, that also means relatively limited volatility as CEFs have to regularly deal with discounts/premiums that don't cooperate for extended periods - case in point, FCO.

For further details see:

FCO And BWG: A Swap Opportunity Presents Itself