RIET - Fed Fights 'Ghost Of Inflation Past'

2023-03-19 09:00:00 ET

Summary

- U.S. equity markets oscillated forcefully while interest rates plunged this week as contagion from a pair of mid-sized bank collapses spread to other lenders while authorities scrambled to contain the fallout.

- On brand with the "March Madness" theme this week, the S&P 500 seesawed between gains and losses in each session but ultimately ended the week higher by 1.1%.

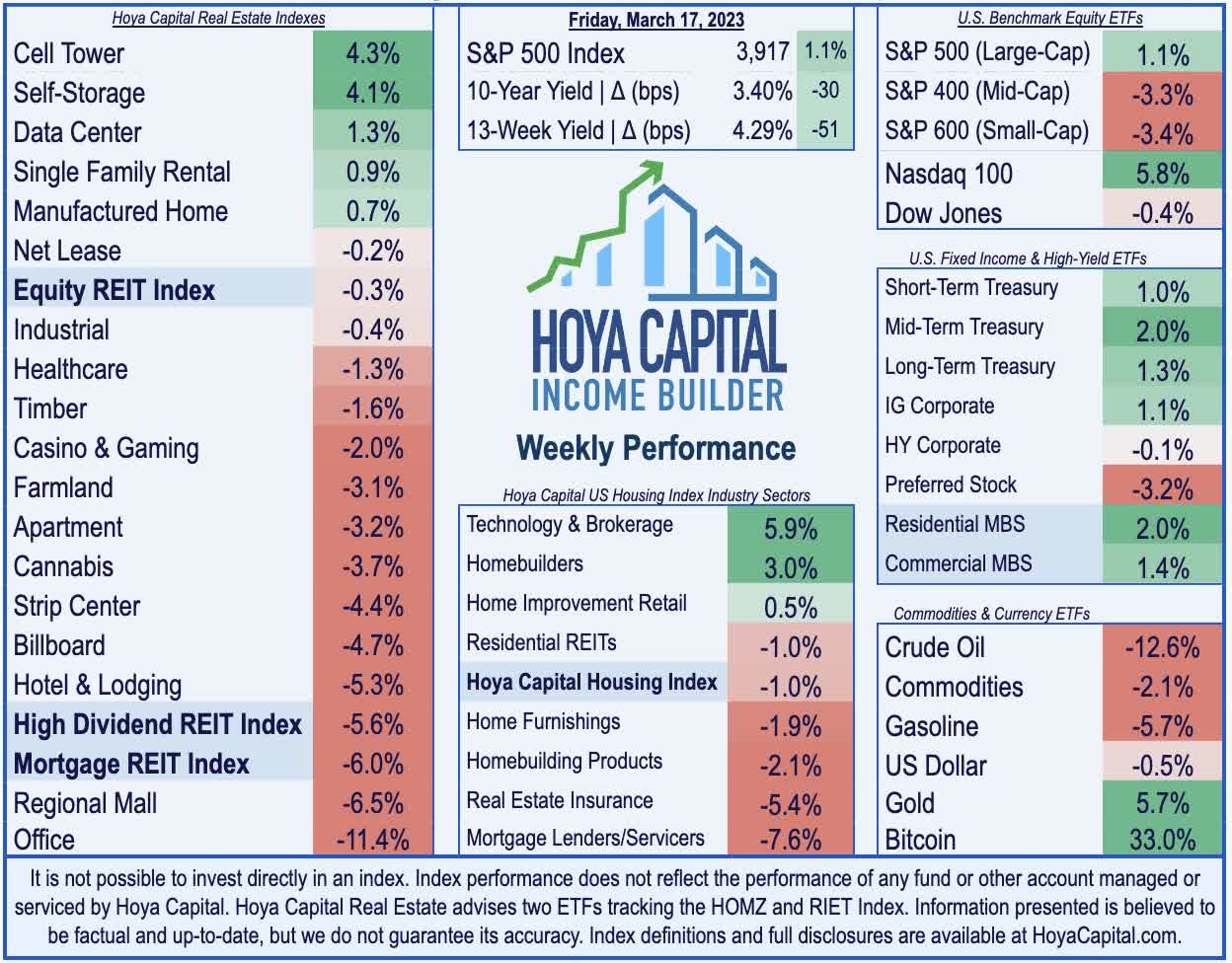

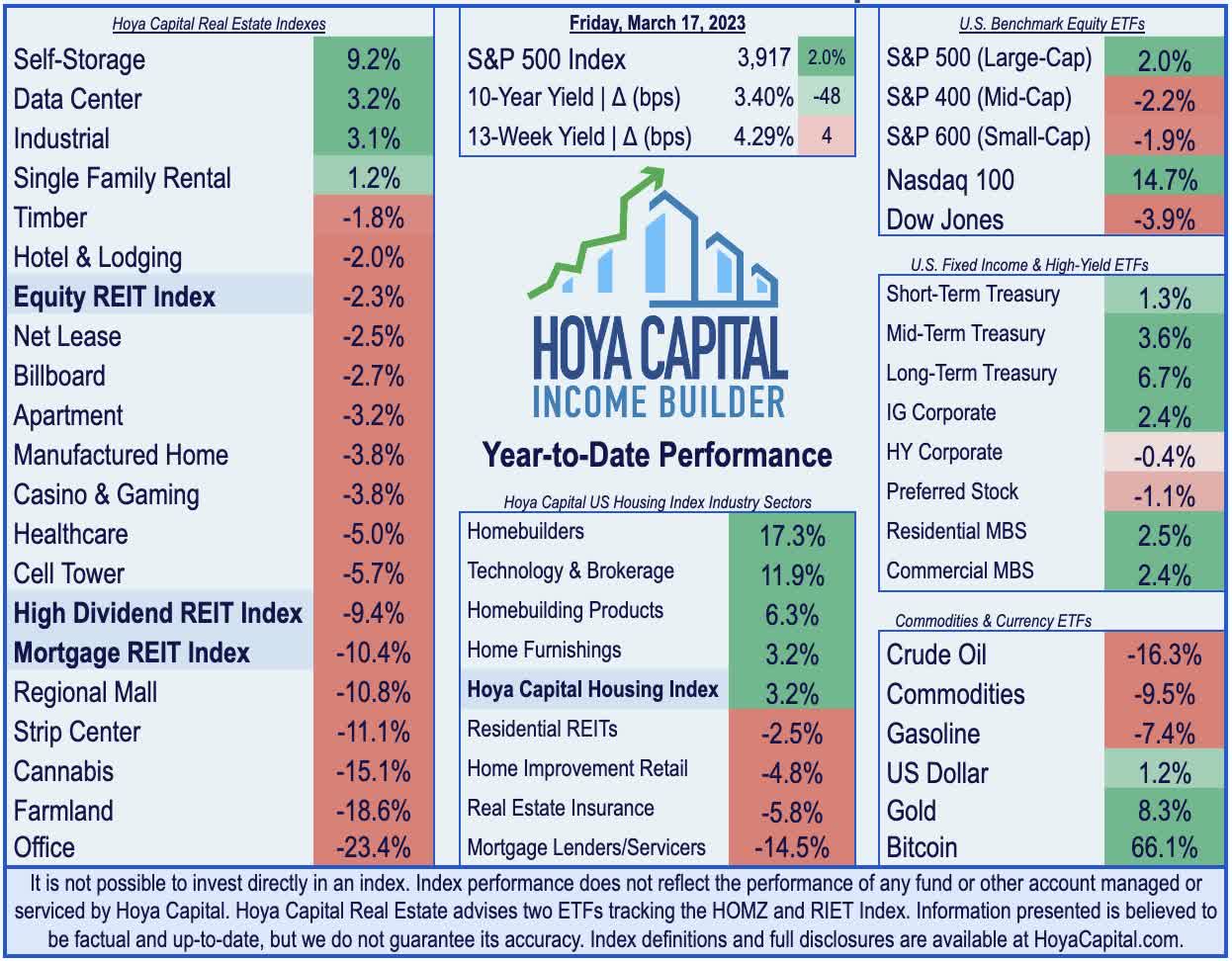

- Real estate markets experienced similarly-sharp deviations, with a nearly 15% spread between the top-performing and worst-performing major property sectors, masked by the modest 0.3% decline on the Equity REIT Index.

- Inflation data and market interest rate pricing indicate that the Federal Reserve is now woefully ahead of the curve - potentially fighting the "ghost of inflation past" - with consequences that threaten to be more painful than the central bank's policy errors in the opposite direction.

- Amid the market turmoil, we did see some positive dividend news this week with a half-dozen REITs raising their payouts, including net lease REIT Realty Income and apartment REIT Equity Residential.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on March 17th.

U.S. equity markets oscillated forcefully while interest rates plunged this week as contagion from a pair of mid-sized bank collapses spread to other lenders while authorities scrambled to contain the fallout. Contagion concerns from the collapse of Silicon Valley Bank were amplified by turmoil at First Republic Bank and Credit Suisse, which required a series of government backstops and rescue packages in a bid to stave off cascading distress. Inflation data and market interest rate pricing, meanwhile, indicate that the Federal Reserve is now woefully ahead of the curve - perhaps fighting the "ghost of inflation past" - with consequences that threaten to be more painful than the central bank's policy errors in the opposite direction.

{kind=link}

Hoya Capital

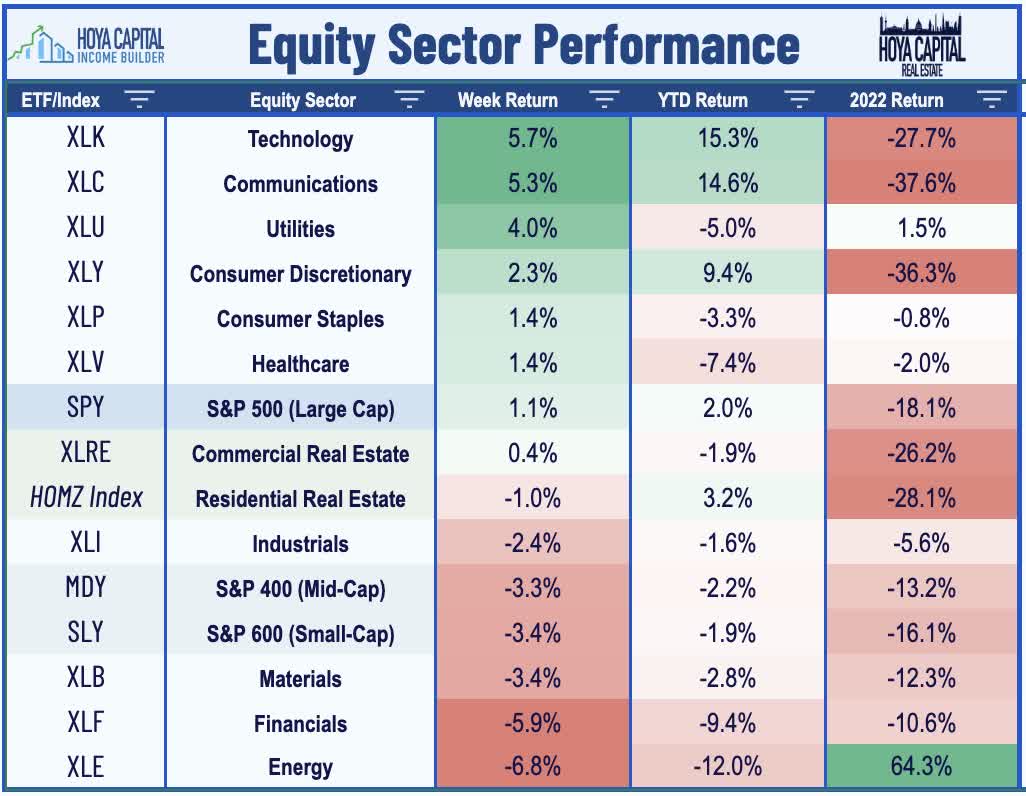

On brand with the "March Madness" theme this week, the S&P 500 seesawed between gains and losses in each session but ultimately ended the week higher by 1.1%. This week saw a remarkable divergence between the major benchmark indexes, with the tech-heavy Nasdaq 100 soaring nearly 6% on the week, while the Mid-Cap 400 and Small-Cap 600 each dipped by over 3%. Real estate markets experienced similarly sharp deviations this week, with a nearly 15% spread between the top-performing and worst-performing major property sectors. Masking this intra-sector volatility, the Equity REIT Index posted rather muted declines of 0.3%, but the Mortgage REIT Index dipped by another 6%. Homebuilders rallied on surprisingly solid earnings reports and housing data alongside the retreat in mortgage rates.

{kind=link}

Hoya Capital

Even more extraordinary volatility was seen in U.S. Treasury markets - the most liquid financial market in the world - as benchmark interest rates swung wildly ahead of next week's FOMC rate decision. The policy-sensitive 2-Year Treasury Yield posted a historic plunge to close at 3.85% - nearly 125 basis points lower than its highs of 5.07% in the prior week. The 10-Year Treasury Yield dipped 30 basis points on the week to close at 3.40%. The Crude Oil benchmark dipped below $70/barrel for the first time since late 2021 and is now nearly 50% below its 52-week highs last summer. Natural Gas futures - the other critical inflation-driving commodity - dipped another 3% on the week and is now 76% below its 52-week high. Energy ( XLE ) stocks dipped nearly 7% on the week, while Financials ( XLF ) stocks also posted steep declines.

{kind=link}

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

Hoya Capital

Has the Fed been fighting the "ghost of inflation past?" The Consumer Price Index this week showed a modest month-over-month uptick in inflation in February but a continued moderation in the annual rate, providing fodder to both sides of the inflation debate. The delayed recognition of shelter inflation, however, continues to heavily distort the headline and core metrics. The metric that we watch most closely - CPI-ex-Shelter Index - showed an eighth straight month of cooling in the year-over-year rate. Since July, this CPI ex-Shelter Index has declined by about 1% on an absolute basis. Despite real-time rent and home prices metrics showing muted - or negative - increases since mid-2022, the CPI Shelter Index soared 8.1% - the highest in four decades - and accounted for 70% of the monthly CPI increase. When the BLS Rent Index is replaced with the Zillow ZRI Rent Index, we observe a sharp decline in the CPI Index since mid-2022, with this "Rent-Adjusted CPI" slowing to 3.16% in February and averaging just 1.2% over the past eight months.

{kind=link}

Hoya Capital

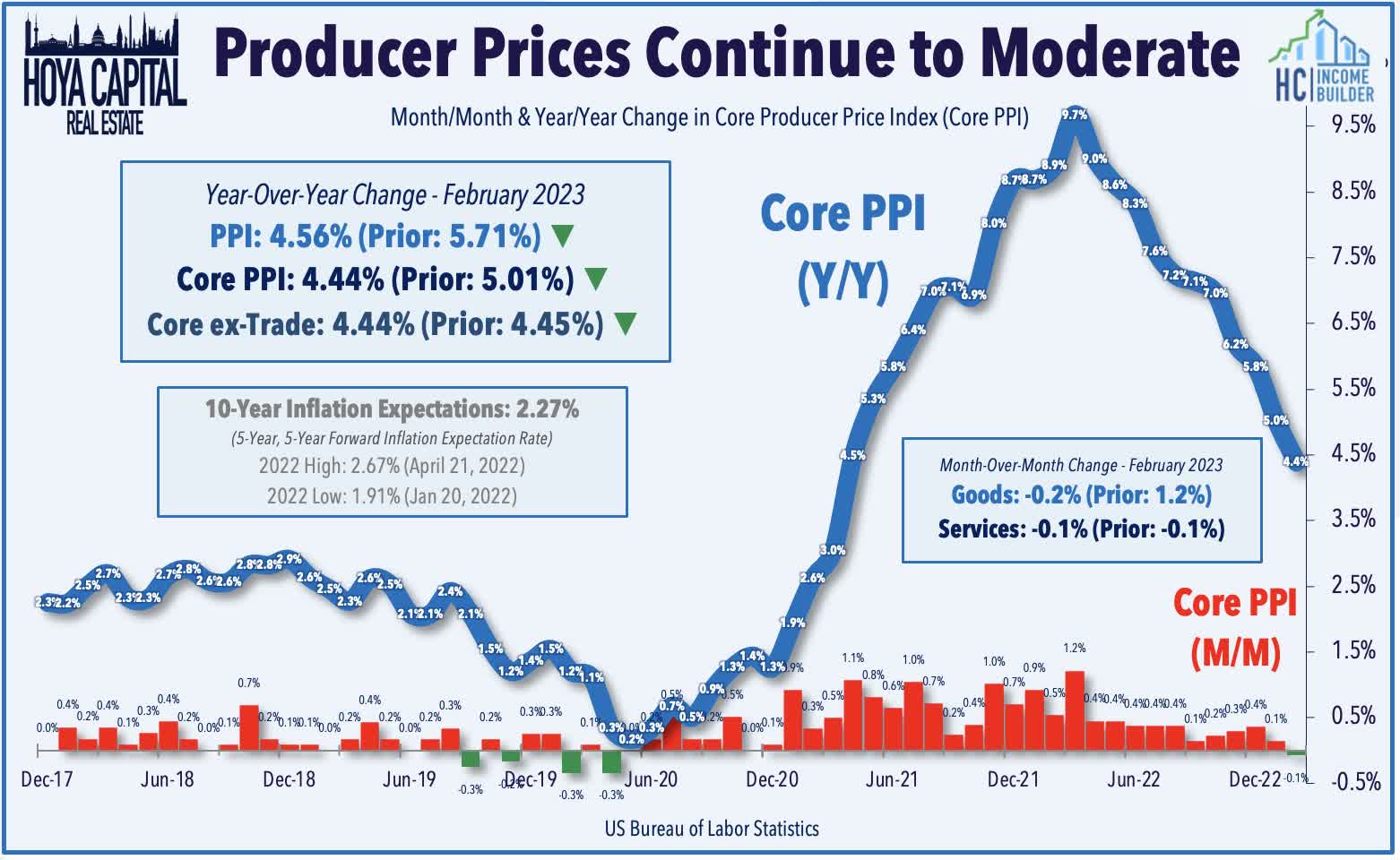

Producer Price Index data this week was also significantly cooler than expected, with the Core PPI Index posting a month-over-month decline for the first time since May 2020. Both services and goods prices declined in February, dragging the annual increase on the headline PPI index to 4.6%, well below the downwardly revised 5.7% level from the previous month. The theme of cooler-than-expected inflation data continued in the final reading before the FOMC's rate decision next Wednesday. The University of Michigan's Survey of Consumers showed that short-term inflation expectations fell in early March to the lowest level in nearly two years, while long-run inflation expectations also eased. Respondents said they expect inflation to rise 3.8% over the next year - the lowest reading since April 2021 - and expect inflation to average 2.8% over the next five to ten years, which was the lowest in six months.

{kind=link}

Hoya Capital

Equity REIT Week In Review

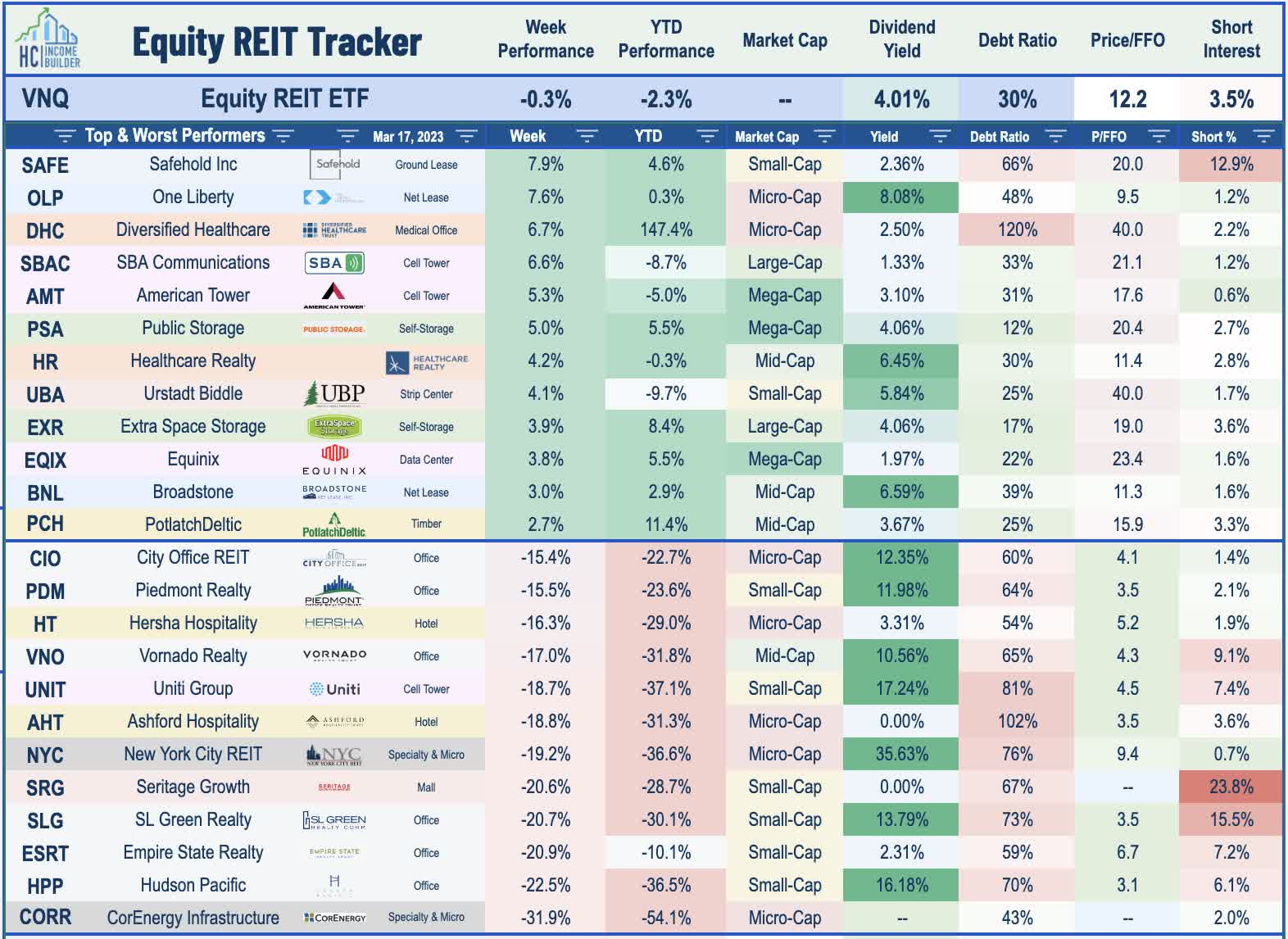

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Hoya Capital

Beginning with the good news: Amid the market turmoil, we did see some positive dividend news this week. Net Lease REIT Realty Income ( O ) hiked its monthly dividend for the second time this year. Apartment REIT Equity Residential ( EQR ) hiked its dividend by 6% to $0.6625/share. Park Hotels ( PK ) boosted its quarterly dividend to $0.15/share, a 25% boost from its prior rate. Several other REITs officially declared the hikes that were indicated in their earnings reports last month, including RLJ Lodging ( RLJ ), which boosted its quarterly payout by 60%; shopping center REIT InvenTrust ( IVT ), which hiked its quarterly dividend by 5%; and apartment REIT UDR ( UDR ), which raised its quarterly payout by 10.5%. We've now seen 39 REITs hike their dividends this year, while eight REITs have lowered their payouts, including mortgage REIT Annaly Capital ( NLY ) which trimmed its payout by about 25% this week, as indicated in its recent earnings report last month.

{kind=link}

Hoya Capital

This week, we published our State of the REIT Nation report, which examined high-level REIT fundamentals to chart the likely path forward for the real estate industry amid the recent turmoil. Owing to the harsh lessons from the Great Financial Crisis, most REITs have been exceedingly conservative with their balance sheet and strategic decisions, ceding ground to higher-levered private-market players. Critically, publicly-traded REITs have had far greater access to longer-term, fixed-rate unsecured debt that has allowed REITs to lock in fixed rates on nearly 90% of their debt while simultaneously pushing their average debt maturity to nearly 7 years, on average, thus avoiding the need to refinance during these highly unfavorable market conditions. Meanwhile, REITs reported in Q4 that their Funds From Operations ("FFO") were 10% above pre-pandemic-levels, on average, while dividend coverage remains historically strong with an average FFO payout ratio of below 70%.

{kind=link}

Hoya Capital

Single-Family Rental : Consistent with that note, Invitation Homes ( INVH ) - which we own in the Dividend Growth Portfolio - advanced about 1% on the week after it announced that it received an S&P credit rating upgrade to ' BBB ' from ' BBB -' with a stable outlook. S&P cited INVH's "improved capital structure over the past two years along with expectations that positive operating performance will be sustained." After relying on shorter-term mortgage-based debt early in its existence, it has leveraged its solid operational track record - and status as the largest single-family rental owner in the country - to access longer-term unsecured financing channels over the past several years. INVH has refinanced over $3 billion of secured debt in 2021 and 2022 and has been able to push its nearest-term debt maturity to 2026.

{kind=link}

Hoya Capital

Net Lease : Small-cap One Liberty Properties ( OLP ) was also among the upside standouts this week, rallying more than 7% on the week after reporting better-than-expected fourth-quarter results, noting that its AFFO for full-year 2022 rose about 2% to $1.98/share driven by an improvement in its occupancy rate to 99.8%. OLP owns a portfolio of 125 net lease properties - split roughly 60/40 between industrial and retail assets - with a concentration along the US East Coast. In our State of the REIT Nation report, we noted that net lease REITs have been far-and-away the most active acquirers in recent quarters - accounting for more than a third of total net purchases across the REIT industry - taking a surprising "business as usual" approach to external growth despite the shifting interest rate environment.

{kind=link}

Hoya Capital

Office : Now, onto the bad news: More than a dozen REITs dipped by more than 15% on the week, with the office sector once again the center of the painful price action amid a wave of corporate announcements of space reductions and concern over a potential surge in loan defaults. Over the past month, 10 office REITs have declined by at least 30%, while another 9 have posted declines in excess of 20%. A handful of office REITs, including Hudson Pacific ( HPP ), Alexandria Real Estate ( ARE ), and Cousins ( CUZ ), provided updates on their exposure to Silicon Valley Bank (SIVB) and Signature Bank (SBNY), which range from direct landlord relationships to indirect exposure through letters of credit that SVB and SBNY issued to tenants of several REITs which effectively served as security deposits. There remains uncertainty over whether the FDIC will void these letters of credit, which would leave landlords with no recourse to withdraw payments if a tenant does not pay rent.

{kind=link}

Hoya Capital

Apartment : Also among the laggards this week, Midwest-focused Centerspace ( CSR ) slumped about 8% after it announced a $144.3M deal to sell nine communities totaling 1,567 homes located in Minnesota and Nebraska, representing about 10% of its portfolio. Centerspace - which has a Debt Ratio of around 45% which is well above the apartment REIT average of 28% - plans to use the proceeds to pay down outstanding debt and extend maturities. CEO Mark Decker commented, "This is another step in our strategy to boost the quality of our homes, earnings power of the company, and flexibility of our balance sheet." CSR has underperformed its peers this year after reporting downbeat Q4 results and providing guidance calling for a 1% decline in FFO in 2023, which came amid an otherwise impressive earnings season across the apartment sector.

{kind=link}

Hoya Capital

Mortgage REIT Week In Review

This week, we published Mortgage REITs: High-Yield Opportunities & Risk , which discussed our updated outlook on the sector and recent allocations in our Focused Income Portfolio . Mortgage REITs have been slammed by the fallout of the ongoing regional banking crisis amid a resurgence of interest rate volatility and credit concerns, erasing their once-robust gains for 2023. Commercial mREIT exposure to the troubled office sector has come into focus following a wave of mega-sized loan defaults from over-levered private owners. For Residential mREITs, Book Values remain in decent-shape as MBS spread-widening has been more-than-offset by a decline in benchmark rates, but sharp changes in rates heighten the hedge-related risk. Despite paying average dividend yields in the low-teens, the majority of mortgage REITs are still able to cover their dividends, but we identified several mREITs that are most at-risk of dividend reductions and broader risk factors.

{kind=link}

Hoya Capital

On cue, we heard dividend declarations from 16 mortgage REITs this week, and with the exception of the aforementioned Annaly , each of these REITs held their payouts steady. That didn't stop the selling pressure this week, however, as mortgage REITs finished lower by 3.7% on the week while commercial mREITs plunged by 8.0%. Notably, the selling pressure came despite one of the strongest weeks on record for the underlying Residential MBS ETF ( MBB ) and Commercial MBS ETF ( CMBS ). which gained 2.0% and 1.4%, respectively, as tailwinds from lower benchmark interest rates more-than-offset the widening of MBS spreads. On the upside, New York Mortgage ( NYMT ) gained about 1% after announcing an upside stock buyback program to repurchase up to $250M in common stock and $100M in preferred stock.

{kind=link}

Hoya Capital

Elsewhere, Arbor Realty ( ABR ) was under-pressure this week following a published report by short-seller NINGI Research, which accused Arbor and its auditor, Ernst & Young, of various "misstatements and misconduct." ABR - which has been among the strongest performing mREITs over the past five years - commented that the report "lacks merit and contains numerous inaccuracies, misstatements, and otherwise misleading allegations." We see several glaring inaccuracies in the report, including its commentary on Arbor's Current Expected Credit Losses ("CECL") and an inaccurately identified "peer group" of other mortgage REITs for Arbor, which included mREITs with significant office and retail collateral exposure. As a whole, office assets represent less than 20% of commercial mREITs' property-level exposure, but a handful of names have outsized weight in the office sector, including Ares Commercial ( ACRE ), Ladder Capital ( LADR ), BrightSpire ( BRSP ) and Granite Point ( GPMT ) at more than 40% of their loan books.

{kind=link}

Hoya Capital

2023 Performance Recap & 2022 Review

Through the first eleven weeks of 2023, the Equity REIT Index is now lower by 2.3% on a price return basis for the year, while the Mortgage REIT Index is lower by 10.4%. This compares with the 2.0% gain on the S&P 500 and the 2.2% decline for the S&P Mid-Cap 400 . Within the real estate sector, 4-of-18 property sectors are in positive territory on the year led by Self-Storage, Data Center, Industrial, and SFR REITs. At 3.40%, the 10-Year Treasury Yield has declined 48 basis points since the start of the year - barely above its closing low of 3.39% in early February - and well below its 2022 highs of 4.30%. The US bond market has stabilized following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 2.9% this year.

{kind=link}

Hoya Capital

Economic Calendar In The Week Ahead

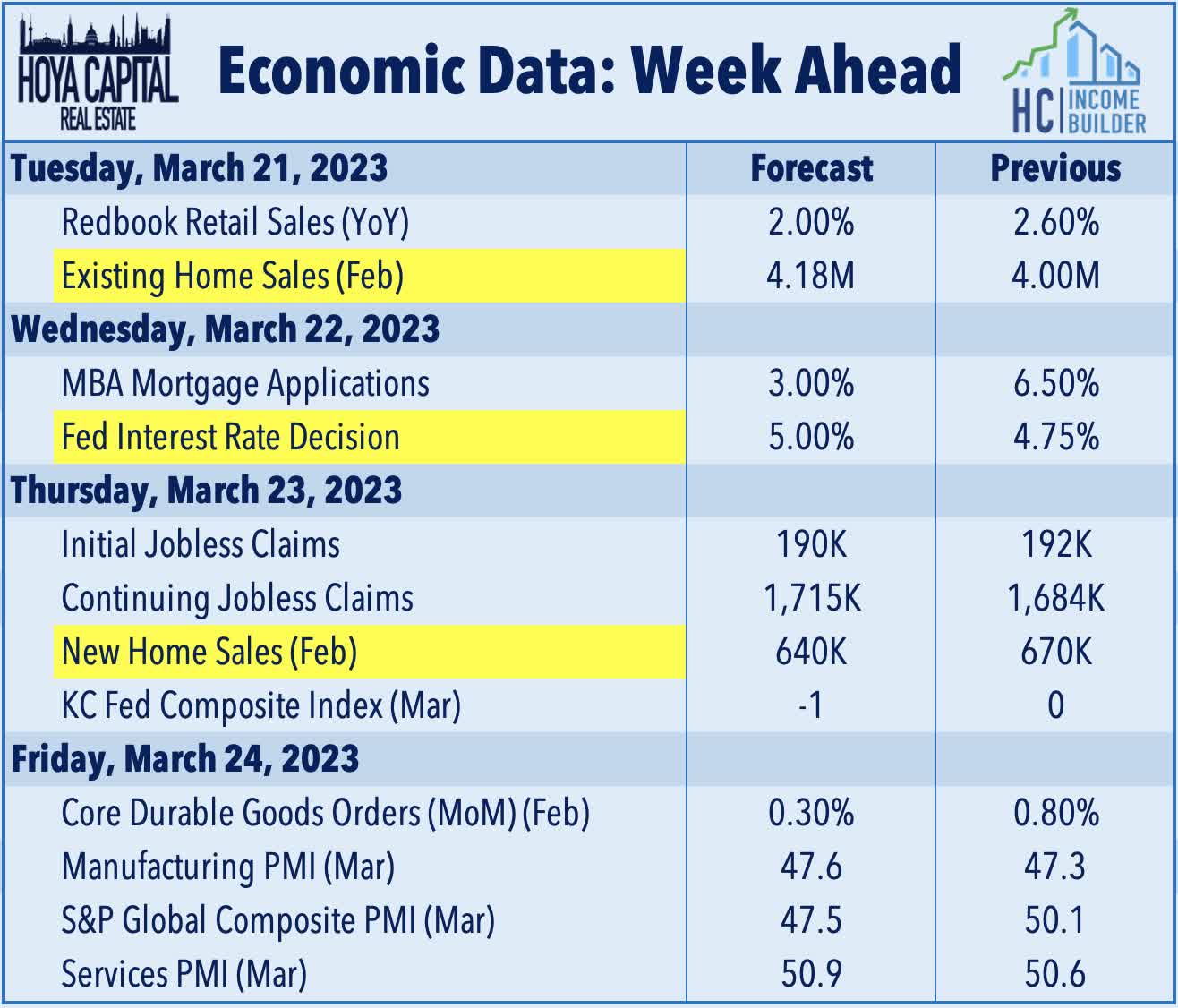

All eyes will be on the Federal Reserve in the week ahead. The Federal Open Market Committee ("FOMC") begins its two-day policy meeting on Tuesday which concludes with the Fed's Interest Rate Decision on Wednesday afternoon. As of Friday evening, swaps markets imply a roughly 60% probability of a 25 basis point rate hike to an upper bound of 5.0% with 40% odds of a pause. Notably, markets now expect this to be the final rate hike of this rate hike cycle and currently reflect expectations of four rate cuts by the end of the year which would bring the upper bound to 4.0%. It'll be another busy week of housing market data as well, with Existing Home Sales data on Tuesday and New Home Sales data on Thursday. Home Sales metrics have closely correlated with changes in mortgage rates, which averaged 6.66% in February, up from 6.26% in January. We'll also be watching weekly Jobless Claims data on Thursday and a busy slate of PMI data throughout the week.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

Fed Fights 'Ghost Of Inflation Past'