VTI - Fed Update: Jay Powell Is Trying To Walk And Chew Gum At The Same Time

2023-05-05 14:54:49 ET

Summary

- Fed Chairman Powell has been fighting battles on two seemingly incongruent fronts.

- His first goal is to meet his primary mandate of conducting monetary policy to promote stable prices.

- His second goal is to uphold his responsibility to promote the safety and soundness of individual financial institutions.

- The disconnect between these two objectives is that the tool to battle the first, namely raising interest rates, is the main reason why there are problems with the second.

Fed Chairman Jay Powell has been fighting battles on two seemingly incongruent fronts.

The first is his attempt to meet one of his primary mandates of conducting monetary policy to promote stable prices.

The second is to uphold his responsibility to promote the safety and soundness of individual financial institutions.

The disconnect between these two objectives is that the tool used to battle the first, namely raising interest rates, is the main reason why there are problems with the second.

Inflation

The Fed has set a target inflation rate of 2%.

When the 2% level was breached in spring of 2021, Chairman Powell was slow to react. His first inclination was that the increase in inflation was “transitory” due to supply chain bottlenecks appearing during the COVID pandemic.

PCE Core Inflation

{kind=link}

It took him a full year before he apparently realized his initial assumptions were wrong and that inflation was here to stay.

He then moved aggressively to bring inflation down. Over the past 14 months, the Fed has used its most effective tool and increased the Fed Funds rate 10 times by a total of 500 basis points. The current range of 5.00-5.25%, with this past Wednesday’s most recent hike, is the highest level in 16 years.

{kind=link}

Quantitative Tightening

Raising interest rates, however, is only one part of the Fed’s monetary policy. The second part is what is referred to as Quantitative Tightening ("QT").

QT is the opposite of the policy used since 2008 called Quantitative Easing ("QE"). QE was an unconventional policy tool implemented during a period of extreme economic stress, when the Fed began purchasing large quantities of U.S. Treasury securities and MBS. This policy, carried out over a period of 14 years, caused the Fed’s balance sheet to balloon from $900 billion to almost $9 trillion, a tenfold increase.

{kind=link}

QT is integral to the Fed’s policy normalization program and aims to withdraw liquidity, which in large part contributed to the spike in inflation, by reducing the size of the Fed’s Balance Sheet.

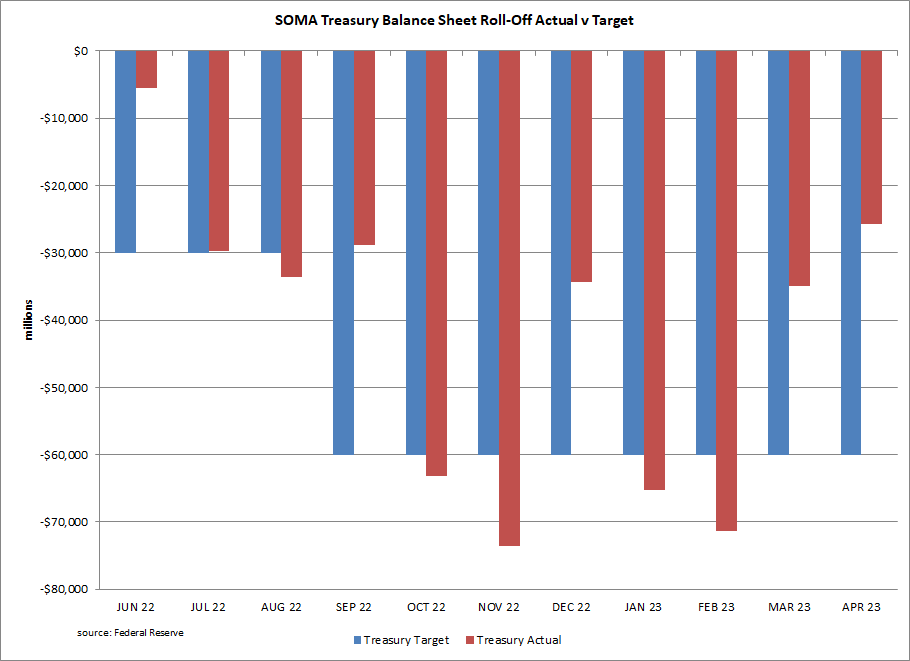

Exactly a year ago, the Fed announced their intention of beginning QT in June 2022 through a balance sheet roll-off. The target was to let Treasuries and MBS mature at the rate of $95 billion a month, phased in over three months. Initially $30 billion of Treasuries and $17.5 billion of MBS would be allowed to mature each month, increasing to $60 billion of Treasuries and $35 billion of MBS.

Balance Sheet Roll-Off Results

The Fed now has eleven months of QT under its belt, and the results have been less than initially projected.

The Fed has hit their target reduction in 6 of the 11 months for the Treasuries in their SOMA portfolio. In aggregate, the Fed has reduced their Treasury securities by $466 billion of the projected $570 billion, or 82% of target.

{kind=link}

The SOMA MBS portfolio roll-off has been more problematic. The Fed has only met or exceeded projections in 2 of the 11 months. In total, the Fed has reduced their MBS holdings by only $170 billion of the projected $333 billion, or 51% of target.

The main reason for this is that the monthly principal and interest payments on MBS are not predictable. When interest rates were lower, a significant portion of the monthly cash flow on the MBS holdings was from extra principal payments due to refinancings or full payoffs from home sales. As mortgage rates have risen, however, both refinancings and home sales have ground to a halt, thereby hampering the Fed’s ability to reduce their MBS position through roll-offs.

{kind=link}

The overall results of the Fed’s balance sheet roll-off have been disappointing. The Fed has not met their projected roll-off goal in any of the 11 months to date. Cumulatively, the Fed has only reduced their SOMA bond holdings by $636 billion of the projected $903 billion, or 70% of target. This represents only a 7% reduction in their SOMA bond portfolio.

{kind=link}

Regional Banking Turmoil

While the Fed has been raising rates to fight inflation, their aggressive action has wreaked havoc on regional banks.

The rapid rate hikes have revealed the basic asset/liability mistakes made by many banks. Simply put, over the past few years under the zero-interest rate policy of QE, many bank managements invested the short-term low-cost deposits they gathered into fixed rate assets. This created an asset/liability mismatch.

This is the same management error that brought down the S&L industry forty years ago. For a detailed analysis see our Seeking Alpha article , "The Largest S&L In The World - Lessons Not Learned."

As interest rates have risen, the value of the bank’s fixed rate assets have fallen. At the same time, depositors have withdrawn their cash for higher earning alternatives. This has squeezed banks' earnings and impaired their capital, causing panic in the market.

In the past six weeks we have had three bank closures, including two of the three largest bank failures ever, as the Fed stepped in to take over Silicon Valley Bank of SVB Financial Group (SIVBQ), Signature Bank (SBNY), and just this week First Republic Bank (FRCB).

Regional banks, as measured by the KBW Regional Banking Index below (see the Invesco KBW Regional Banking ETF (KBWR)), have dramatically underperformed the overall market. The KBW Index is down 32.7% YTD, while the S&P 500 (SP500) is up 5.7% during the same period.

{kind=link}

The Fed has fulfilled their responsibility by being the lender of last resort for these troubled institutions.

Problem banks have borrowed from the Fed under three lending facilities. The first is the discount window. This is the primary place banks go for short-term borrowing from the Fed. Loans here peaked at $117 billion during the second week of turmoil in late March, and have since declined to $50 billion. Instead, these borrowers switched to the second facility, the Bank Term Funding Program ((BTFP)), which opened with $2 billion in mid-March when it was introduced, and has since grown to $78 billion.

BTFP offers very favorable terms to borrowers. Collateral is valued at par, instead of the lower market value, which allows borrowers access to larger funds and eliminates the need for forced asset sales. In addition, the term for borrowing is longer than under the Discount Window. BTFP loans are up to one year while Discount Window borrowings are only for 90 days.

The third credit facility is loans for banks that were acquired under the FDIC receivership. This category is for the bank takeovers like Silicon Valley and First Republic. It started at $52 billion and is now at its largest at $192 billion.

{kind=link}

Looked at in total though, the problem bank loans peaked at $352 billion on March 23 rd , and have since come down to $318 billion, despite this week’s failure of First Republic. The banks are not clamoring for new loans, and as the FOMC said in their policy statement on Wednesday “The US banking system is sound and resilient.”

{kind=link}

In spite of the gyrations in stock prices, watching the weekly problem bank loans will be an indicator of how the sector is faring.

Walking And Chewing Gum At The Same Time

The initial increase in problem bank lending was a setback for the Fed in their policy normalization. Total Fed assets climbed in March 2023 back to their level of November 2022, reversing four months of QT. Since then, though, the Fed is back on track with their balance sheet reduction. Chairman Powell is managing his QT monetary policy and the regional banking crisis.

{kind=link}

Fed’s Earnings Problem

The irony of the Fed assisting troubled banks is that the Fed has exactly the same asset/liability mismatch as the regional banks. The Fed’s balance sheet is comprised mostly of fixed rate bonds in their SOMA portfolio, and they are funded with variable rate short term liabilities, mainly bank reserves and reverse repurchase agreements.

Last July the Fed warned that they may start losing money, and sure enough, with the rate hike they implemented in September 2022, they did.

The Fed now has a negative interest rate margin, meaning that their interest expense on their liabilities is greater than the income they earn on their assets. Currently they are losing more than $2 billion a week. The Fed’s losses will continue until the cost of their liabilities drops below their breakeven point, which is 2.75%. With a cost of liabilities at 5.25%, it doesn’t look like they will get to break even anytime soon.

{kind=link}

Cumulatively, the Fed has lost $54.5 billion since September. Their capital account is only $42 billion. However, due to the unique accounting procedures determined by the Fed Board of Governors, the losses will not impair the Fed’s capital at all. Instead, the losses are carried as a negative liability called “Earnings Remittances Due To The Treasury.”

{kind=link}

In addition, like many banks, the Fed is sitting with a huge $1.1 trillion unrealized loss in their SOMA bond portfolio. This is why they are reducing their balance sheet through maturity roll-offs. They can’t sell securities, because to do so would require them to recognize losses.

Conclusion

Chairman Powell has been insistent that the Fed will fight the inflation battle until we are back at the 2% level. This means that rates will likely stay elevated for quite some time. Based on the FOMC dot plot projections, rates aren't expected to decline to below the Fed's break-even rate until 2026.

FOMC

Bond traders seem to disagree with the Fed and have priced in a 40-basis point cut in the funds rate in 2023 and another 100-basis point cut in 2024. Traders, however, have been talking about the Fed pivot for at least six months, but are still waiting.

Today’s surprise non-farm payroll increase of 253,000 suggests we will not see rate cuts any time soon. The unemployment rate also dropped to 3.4%, the lowest level since 1969.

The Fed likely will not cut rates while we are at record levels of employment and inflation still is significantly above their 2% target.

Chairman Powell will be walking and chewing gum for quite some time.

For further details see:

Fed Update: Jay Powell Is Trying To Walk And Chew Gum At The Same Time