REG - Federal Realty: Still Waiting To Buy The REIT Dividend King Yielding 4.37%

2023-04-04 09:00:00 ET

Summary

- I am willing to make an exception in yield for shares of FRT as its longevity is worth its weight in gold with 55 years of consecutive annual dividend increases.

- FRT's diversified approach has been a winning combination for decades, and I am intrigued by its tenant diversification as no tenant makes up more than 3% of its ABR.

- The valuation is the only aspect holding me back from adding FRT stock to my dividend portfolio as it trades above its peer group average in every category I look at.

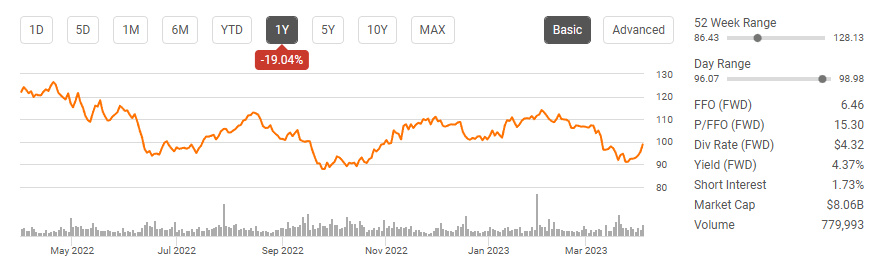

REITs have been under pressure as rates continue to rise, causing many to decline in value. The Vanguard Real Estate ETF ( VNQ ) has declined -23.37% over the previous year, and many individual names have followed its trajectory. I like going against the grain and taking a long-term position in companies on the way down when I feel a correction I overdone. I have been following Federal Realty Investment Trust ( FRT ) for some time, and this is a REIT I want to own, just not at the current valuation. FRT is the only REIT that is classified as a Dividend King , as it has more than 50 consecutive years of dividend increases under its belt. FRT is also the 4 th largest-yielding Dividend King in the market at 4.37%. The fact that FRT has been able to raise its dividend through every crisis in the past 55 years, including when inflation hit 14.8% in 1980, the Dotcom bust, the financial crisis of 2009, and the pandemic of 2020 is a testament to their business model, the strength of properties, and excellent management. As much as I want to invest in FRT, the valuation is just too expensive for me, and I will continue to sit on the sideline until a better entry point presents itself.

{kind=link}

FRT may not have the largest dividend yield in the REIT sector, but it's the only Dividend King with an incredible track record

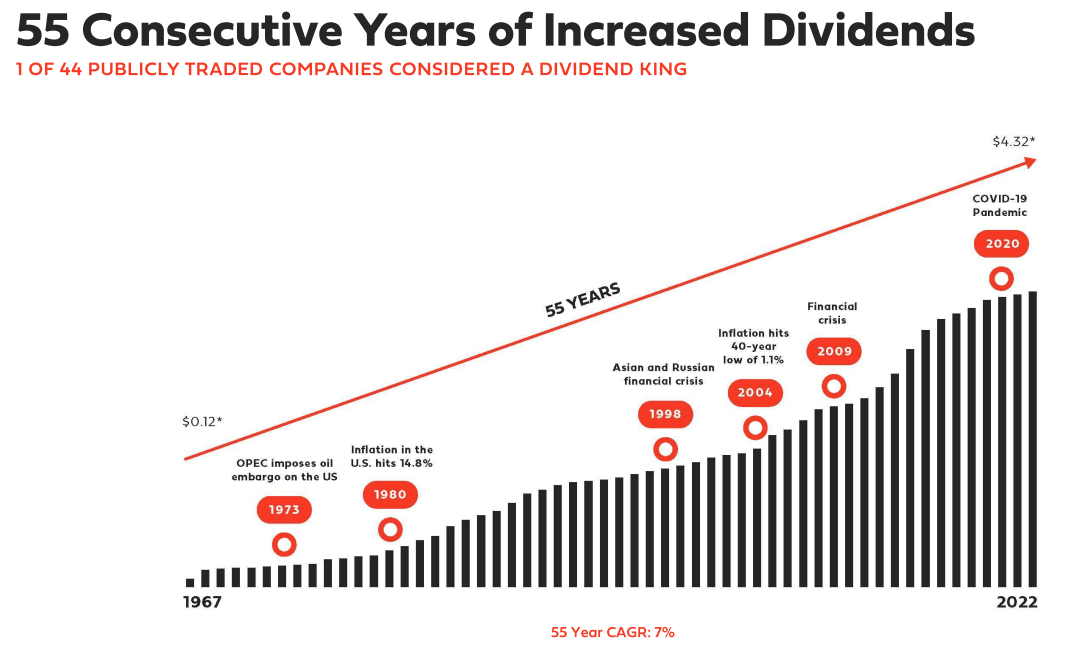

Only 44 companies can claim the title of Dividend King, and FRT is this illustrious club's only REIT. When I look to invest in REITs, I am doing so to generate a significantly larger yield than I can from non-risk assets such as CDs or T-bills. FRT is one of 2 REITs for which I have made an exception, the other being Realty Income (O). Regarding REITs, I usually like to get a 6% dividend or larger, especially in today's environment when CDs and T-bills are generating over 4% risk-free. Making an exception for FRT is a no-brainer for me due to the quality of its dividend.

Only 44 companies have increased their dividend on an annual basis for 50 consecutive years or more. FRT has increased its dividend on an annual basis throughout every economic environment and catastrophic event for more than half a century. Since its first year of paying a dividend in 1967, the annual dividend has increased by 3,500% ($4.20) from $0.12 to $4.32. Since 1967, FRT has provided investors with a dividend compound annual growth rate of 7%, and more than 5 decades later, the dividend continues to increase annually . FRT has a forward funds from operations ((FFO)) of $6.46, which provides a 1.5x dividend coverage ratio. FRT has more than enough room to continue raising its dividend annually based on the FFO it produces.

FRT may not have the largest yield, but it may have the most impressive REIT sector dividend, depending on how you look at things. I am willing to sacrifice yield for quality any day, and FRT is a symbol of quality regarding the dividend, not just in the REIT space but in the entire market. If the valuation was more attractive, I would be adding FRT to my dividend portfolio, but for now, it will remain on my dividend watchlist.

{kind=link}

In addition to the dividend, I like FRT's diversified REIT model

I like FRT's integrated real estate approach as their 103 properties include 3,300 commercial tenants and 3,000 residential units across 26 million sq feet of space. An aspect that sets FRT's properties apart from other REITs is that over 75% of its locations have a grocery component. I am a fan of this approach because grocery stores act as conductors for commerce. Everyone needs to buy groceries, and a large percentage of the population still buys groceries at brick-and-mortar locations rather than through delivery services. This increases the number of people who visit retail centers with a grocery component, which increases the probability of potential customers visiting a neighboring location.

FRT has a diversified income stream and portfolio composition. Diversification is critical, and FRT doesn't have a single tenant that makes up more than 2.8% of its average base rent ((ABR)). FRT's 10 largest tenants make up 14.5% of its ABR, with Home Depot ( HD ) in the 10 th spot representing 0.9% of RT's ABR. At the end of 2022, FRT owned or had a majority stake in community and neighborhood shopping centers and mixed-use properties which are operated as 103 predominantly retail real estate projects. These locations were 94.5% leased and 92.8% occupied

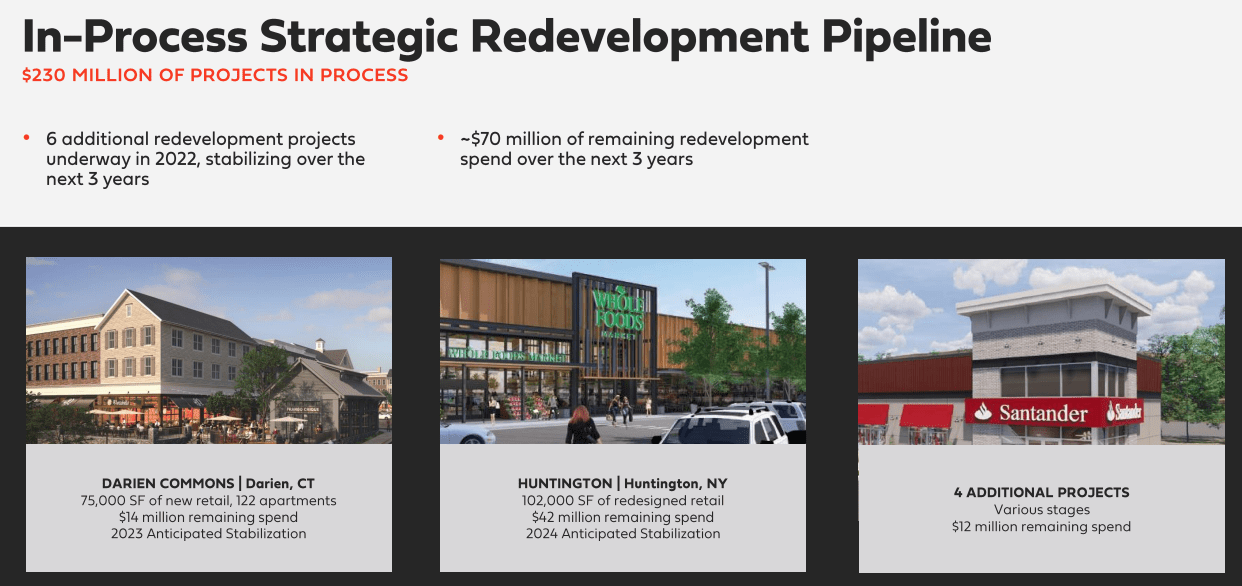

FRT has a strong pipeline of projects to help drive future revenue. There are 6 additional redevelopment projects underway in addition to 5 redevelopment projects that became stabilized in 2021. FRT also acquired Kingstowne Towne Center located in Virginia's Fairfax Country. This location provided FRT with 410,000 sq feet of leasable space on 45 acres. The surrounding 3-mile radius has 47,266 households with a population of 124,052 and an average household income of $159,576.

{kind=link}

I can't move FRT from the watchlist to my Dividend Portfolio because of the valuation

As much as I respect FRT, and want to be a shareholder, I am not willing to pay more than I feel is an appropriate price for its shares. FRT has all the characteristics I want to see, but the share price is still expensive compared to its peers. The peer group I am comparing FRT against is:

- National Retail Properties ( NNN )

- Agree Realty Corporation ( ADC )

- Spirit Realty Capital ( SRC )

- Regency Centers Corporation ( REG )

- Phillips Edison & Company (PECO)

- Realty Income ( O )

- Kimco Realty ( KIM )

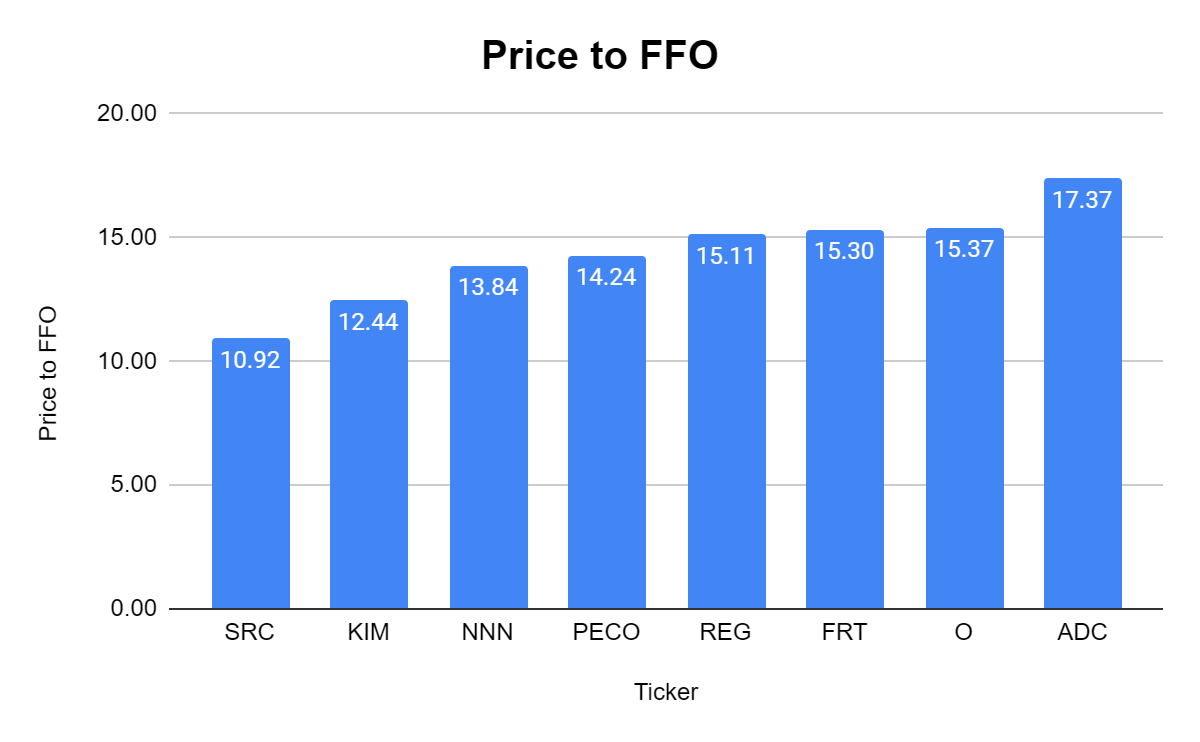

I don't like overpaying for a REIT's FFO. FFO is the equivalent of a traditional equity's EPS as this is the pool of capital dividends are paid from, and the metric used to evaluate REITs. The Peer group has an average price-to-FFO ratio of 14.32x, with 4 REITs falling under the peer group average. FRT doesn't have a horrible metric as its slightly over the peer group average at a price to FFO of 15.3x.

{kind=link}

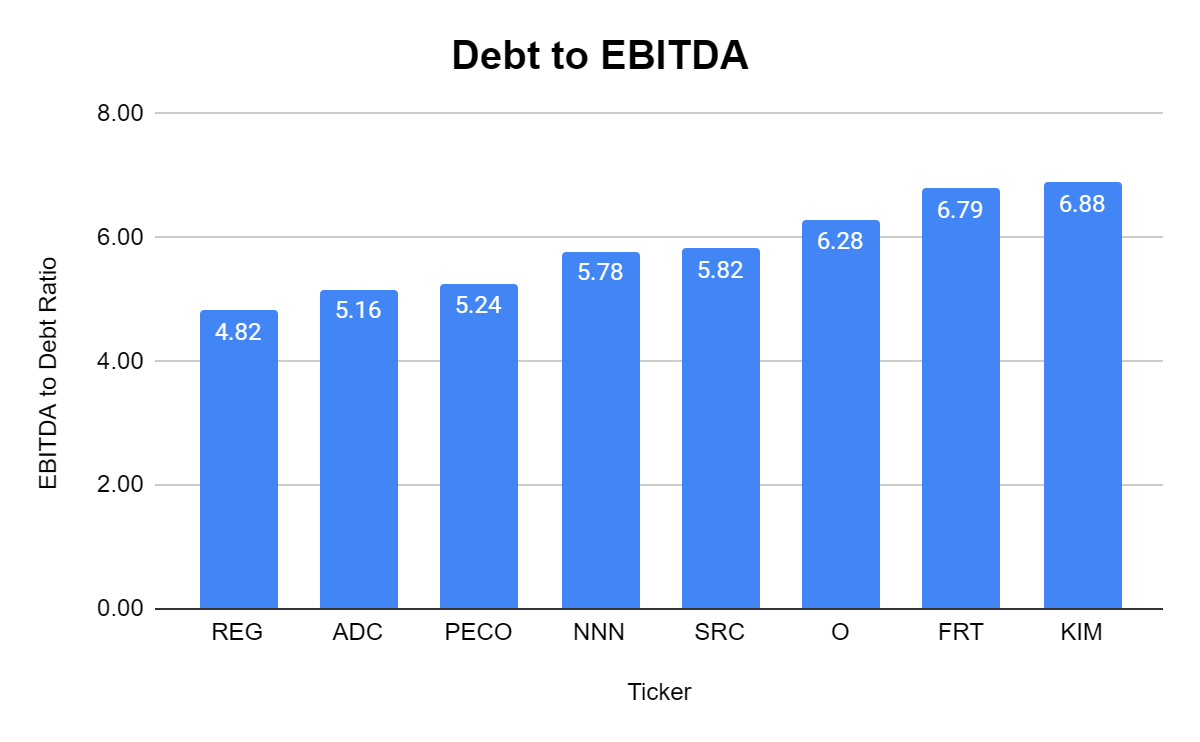

FRT's total debt to EBITDA ratio is on the high end of the spectrum at 6.79x. The peer group average is 5.85x, and FRT has the 2 nd largest debt to EBITDA ratio in its peer group.

{kind=link}

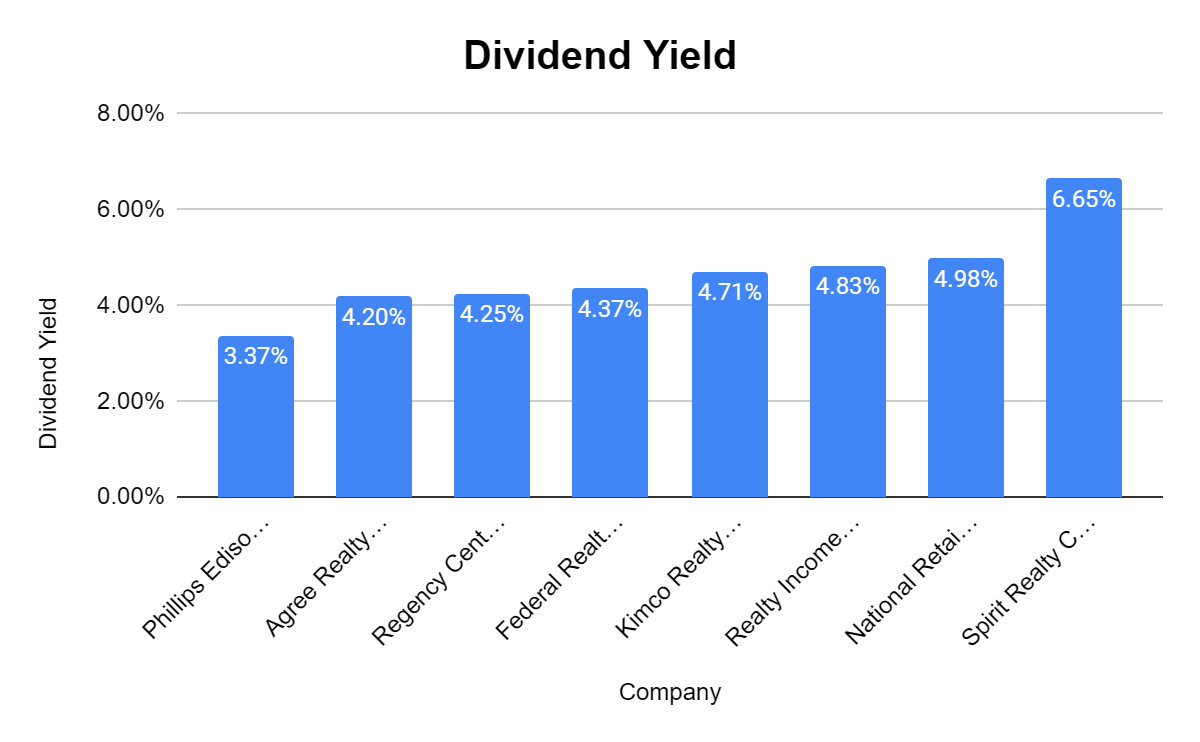

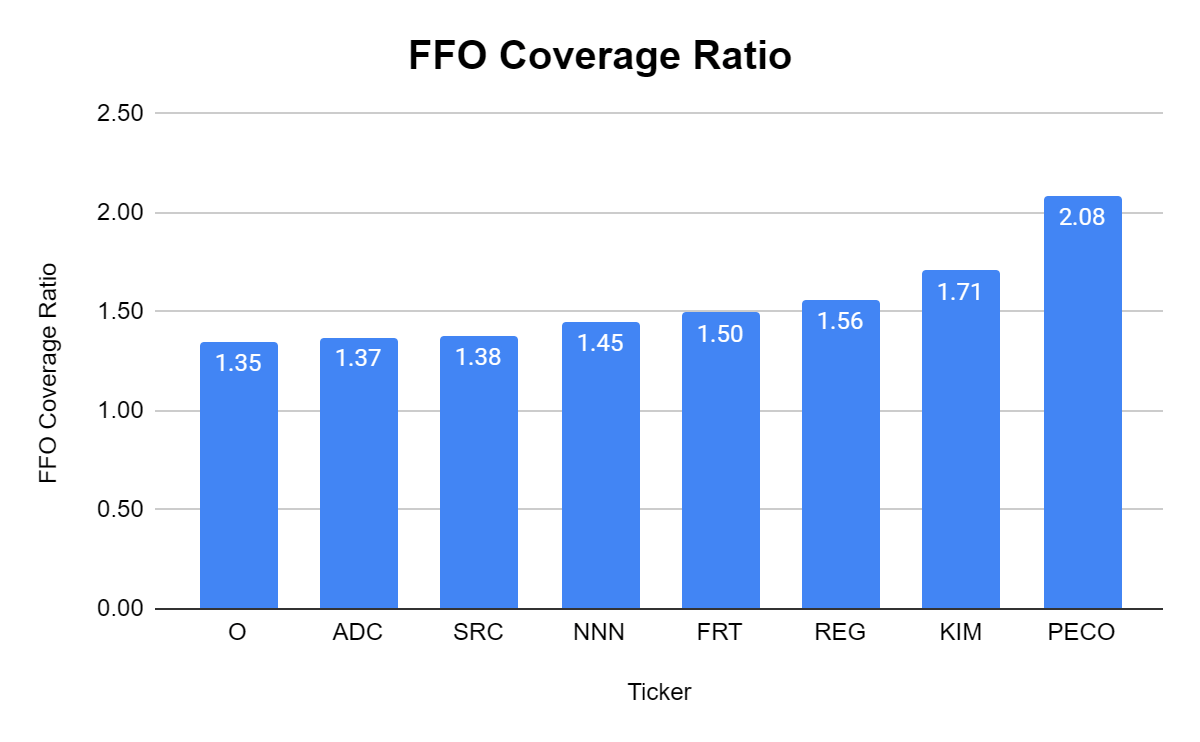

From a dividend perspective, FRT is right on the bubble as its yield is 4.37% compared to a peer group average of 4.67x. FRT also has an FFO coverage ratio of 1.5x compared to a peer group average of 1.55x. While the yield is slightly lower than its peers, FRT makes up for it with the longevity of 55 consecutive dividend increases.

{kind=link}

{kind=link}

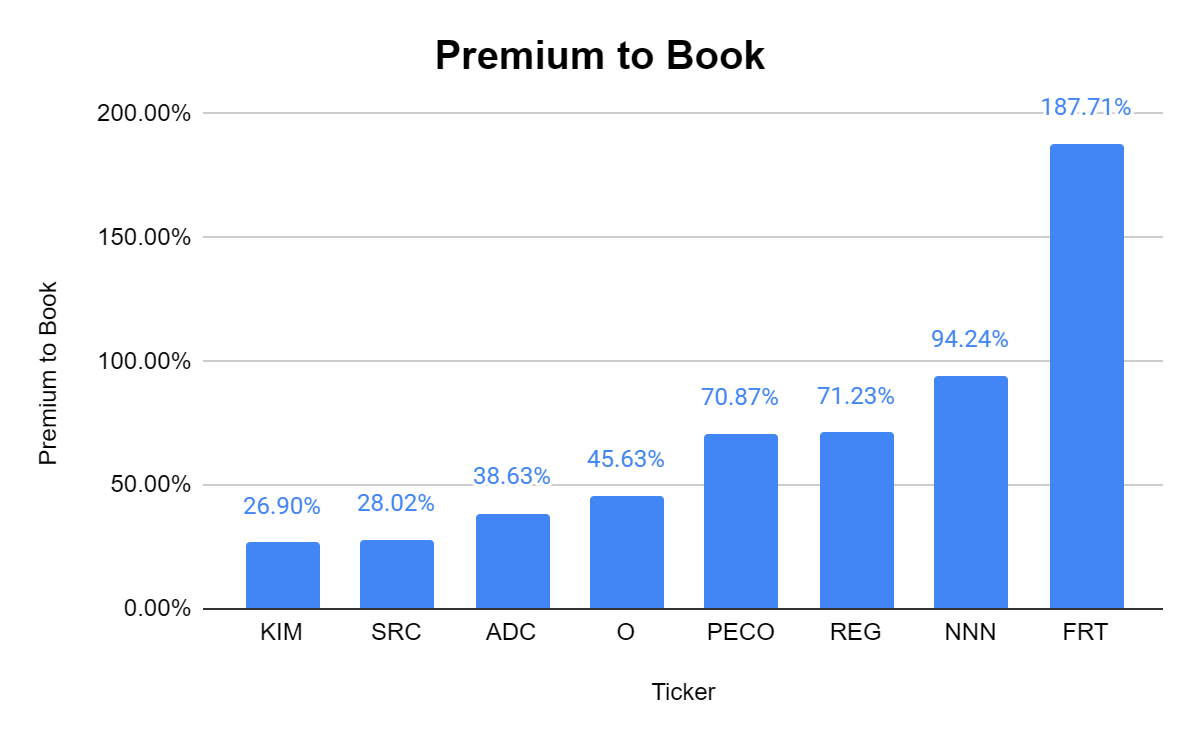

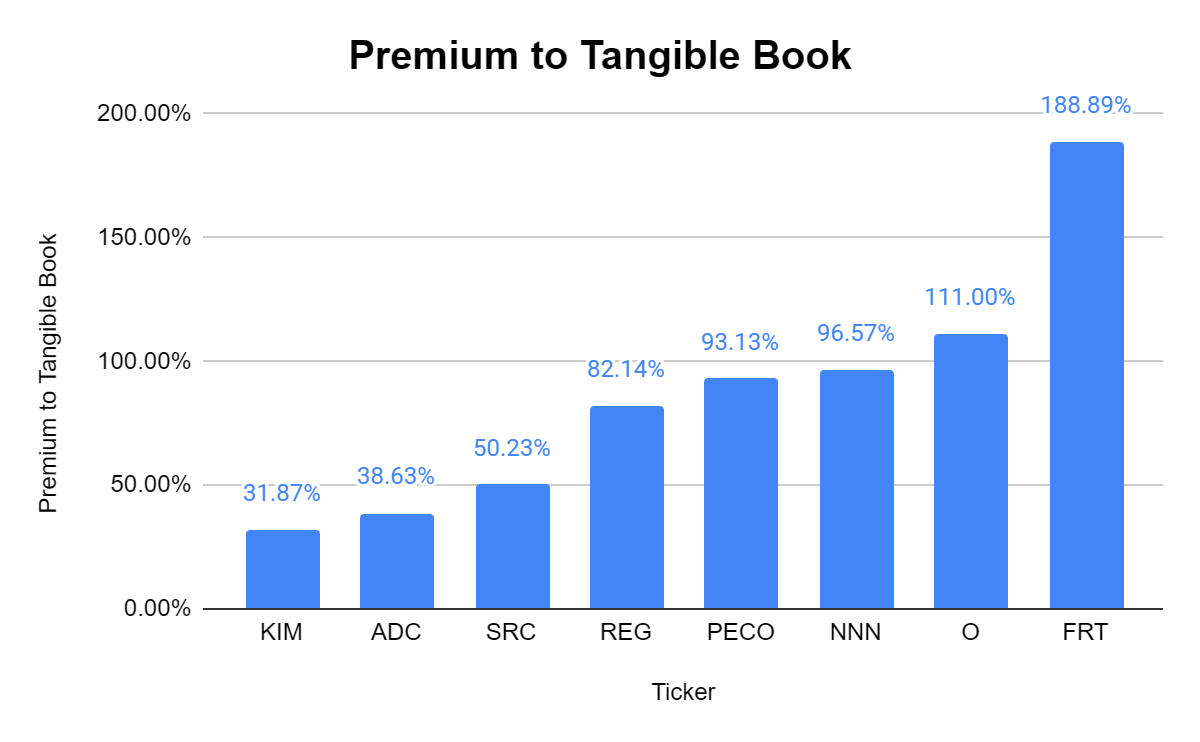

The metrics that are most alarming is the premium Mr. Market has placed on FRT's book and tangible book value. FRT has a book value of $34.35 and a tangible book value of $34.21, while its share price is $98.83. When I look at the peer group in both categories, FRT has a crazy premium tied to shares. Excluding FRT, the range for premium to book is 26.9% - 94.24%, and the range for premium to tangible book is 31.87% to 111%. FRT trades at a 187.71% premium to its book value compared to a peer group average of 70.41%. Tangible book is more strict as it strips away intangible assets, and FRT trades at a 188.89% premium to its tangible book value compared to a peer group average of 86.56%.

{kind=link}

{kind=link}

FRT is an impressive REIT, but there is nothing inexpensive regarding its share price. FRT trades above the peer group average for price to FFO, debt to EBITDA, premium to book, and premium to tangible book. FRT also has a dividend yield and a FFO coverage ratio that is lower than the peer group average.

Conclusion

I will continue to wait for shares of FRT to decline in value before making my initial purchase. FRT is the gold standard as it stood the test of time, and increased its dividend annually for the previous 55 years, regardless of external events. Outside of the valuation, FRT checks off all of the boxes I want to see, as its diversified REIT model has generated decades of success. I don't know if the premium to book or tangible book will ever be in line with its peers, so I will be watching the price to FFO closely. If FRT falls enough where its price to FFO is under 14x, I would highly consider starting a position as its current price to FFO is 15.3x, and the peer group average is 14.32x.

For further details see:

Federal Realty: Still Waiting To Buy The REIT Dividend King Yielding 4.37%