FDX - FedEx: When Size Doesn't Matter

Summary

- FedEx Corporation sees hammered revenues and margin contraction.

- Liquidity levels stay decent, but borrowings appear troublesome.

- Dividends are still well-covered, matched with better-than-market-average yields.

- Investment returns are increasing in general but measly relative to earnings.

- The stock price has increased in the last four months but has not rebounded to 2022 highs.

The small package carrier industry is an integral component of economic growth. It works hand-in-hand with many industries like e-commerce. With its massive size, there is an evident duopoly in the market. One of the two giants is FedEx Corporation (FDX). It holds a substantial market share along with United Parcel Service, Inc. ( UPS ). Over the years, they have capitalized on growth through acquisitions.

Today, FedEx is hammered as market volatility persists. Revenues and margins are still stable but contracting with a weak rebound potential. In addition, its financial positioning is not in good shape. It appears overleveraged since borrowings comprise 44% of the total assets.

Meanwhile, dividend payouts are still well-covered with enticing yields. However, actual investor returns have been meager in recent years. Also, the stock price may be overvalued.

Company Performance

In the past year, market volatility has intensified. It coincided with skyrocketing fuel prices and slow improvement in supply chains. Despite this, FedEx Corporation maximized its capacity while withstanding market blows. It exceeded its FY 2022 targets while delivering quality service to customers.

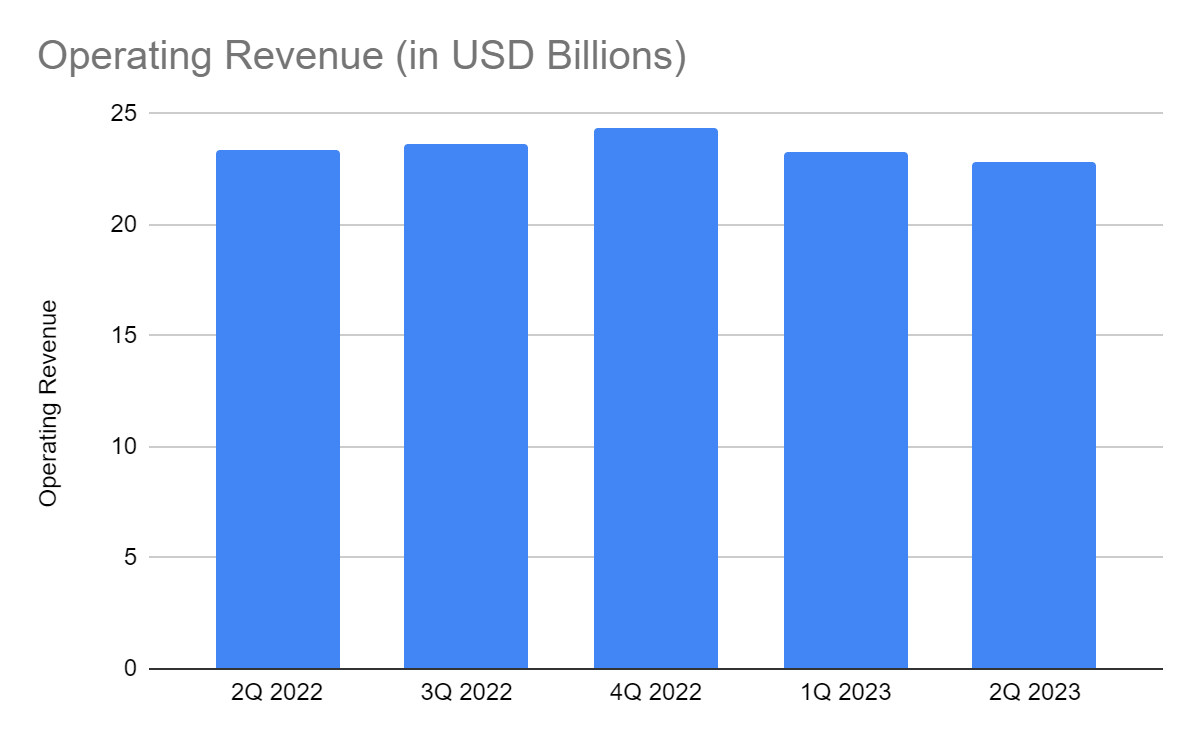

However, FY 2023 presents a different scenario for the company. Inflation peaked and led to skyrocketing fuel and equipment prices. Massive lockdowns in China further aggravated the situation. Note that FedEx has over 100 locations in Mainland China and Hong Kong. Limited movements mean limited operations and revenues. The operating revenue of $22.81 billion is a 3% year-over-year decrease. Indeed, it can hardly manage its business dynamics in a volatile market with low demand. Changing its pricing strategy cannot make up for the lost volumes. We can also notice mixed changes in the operating revenue segments. FedEx Express and Ground segments are its primary revenue components. Unfortunately, they cannot offset the decrease in other segments.

{kind=link}

Operating Revenue (MarketWatch)

Aside from macroeconomic volatility, many other factors contributed to FDX's weaker performance. Lower global volumes remain hammered amidst the moderating demand. It is typical in industries that work directly with small package couriers. After the boom in e-commerce, projections show a potential slowdown this year. The softening of demand became more evident in the second half of 2022. It can prove that the e-commerce upsurge is less persistent than expected. Even worse, UPS is better positioned than FDX, given its 4% revenue growth.

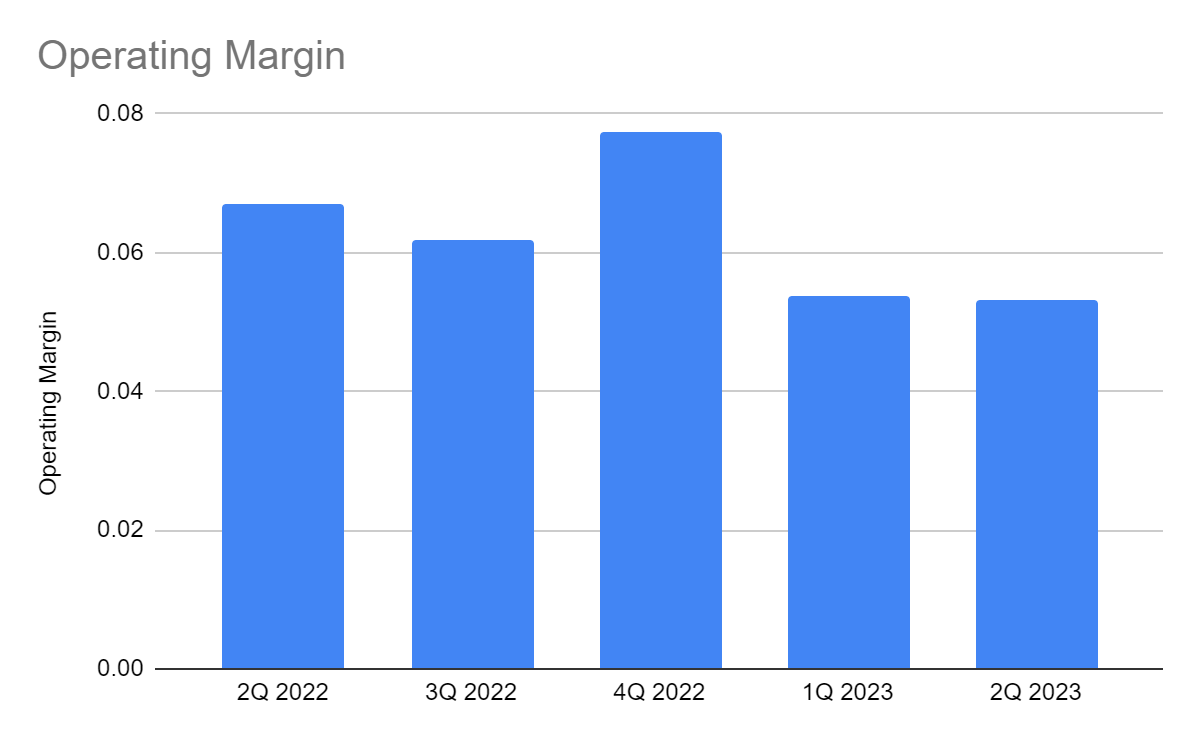

Meanwhile, FedEx remains successful at stabilizing operating costs and expenses. There were mixed changes. Fuel increased by 40%, labor decreased by 5%, and equipment decreased by 10%. Fortunately, its cost-reduction strategies worked against inflationary blows. However, lower expenses could not offset the impact of revenue decrease. The operating margin dropped to 5.3% versus 6.7% in 2Q 2022. What bothers me more is that despite its vast size, margins remain low. UPS's margin is more than twice the margin of FDX. And although the 1Q-2Q 2023 trend appears stable, the core operations remain hammered.

{kind=link}

Operating Margin (MarketWatch)

Today, FDX must beware of the potential economic slowdown that may further drive the softening of freight demand . We already saw a decrease in consumer spending in 4Q 2022. It may persist as prices remain high. Seasonality is also an essential aspect of freight demand changes. So, it may return to pre-pandemic levels. China has started to ease its hard lockdown measures. But FDX may still take some time to adjust its operating capacity. Also, its latest cost-reduction strategy is not efficient and sustainable. It laid off 10% of directors and officers to cope with the cooling demand. Hence, rebound potential may remain limited even if the operating margin stabilizes.

FedEx Corporation This Year

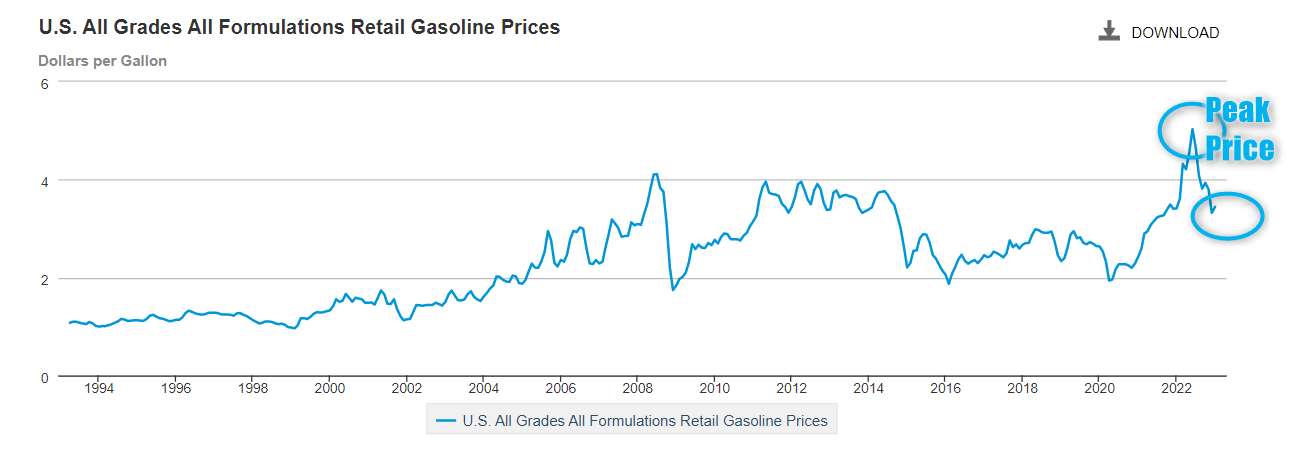

We must weigh the impact of macroeconomic changes on the small parcel industry. I will discuss the potential reasons one by one. Its consolation is that inflation keeps decreasing to 6.5%, about 30% lower than its peak. Fuel prices have become more stable and affordable. In fact, gasoline prices of $3.445 are now about 30% lower than last year's peak price. Border reopenings in China may increase its volumes since it is a primary FDX market. More importantly, it holds the majority of the e-commerce sales, with nearly $3 trillion. As such, FDX may increase its movements in East Asia and benefit from the e-commerce rebound. But these may not materialize quickly as demand and supply are still normalizing. We have to understand that inflation acts like a double-edged sword. Companies are starting to be more conservative with their inventory management. It is due to clearing supply chain bottlenecks in the second half of 2022. Rising prices are leading to the normalization of consumer spending. With that, market supply is about to catch up with market demand. We can see it in the decreasing Global Supply Chain Pressure Index . It is a combination of easing pandemic restrictions and lower consumer spending.

{kind=link}

Gasoline Prices (U.S. Energy Information Administration)

FedEx must watch out for more risks. For instance, the market may face overcapacity during slowdowns this year. I don't think there will be a deep recession since inflation is more demand-pull than cost-push. But there may be economic slowdowns. They may hurt FedEx if they further lower demand and volume flow. FedEx must also be careful with potential competitors that may set lower prices. The rebound across industries may mean more business openings. It may be evident in e-commerce, given the presence of small online retailers. Right now, near-term headwinds still outweigh opportunities in the long run. With that, FedEx must cope with lower volume flows amidst elevated prices.

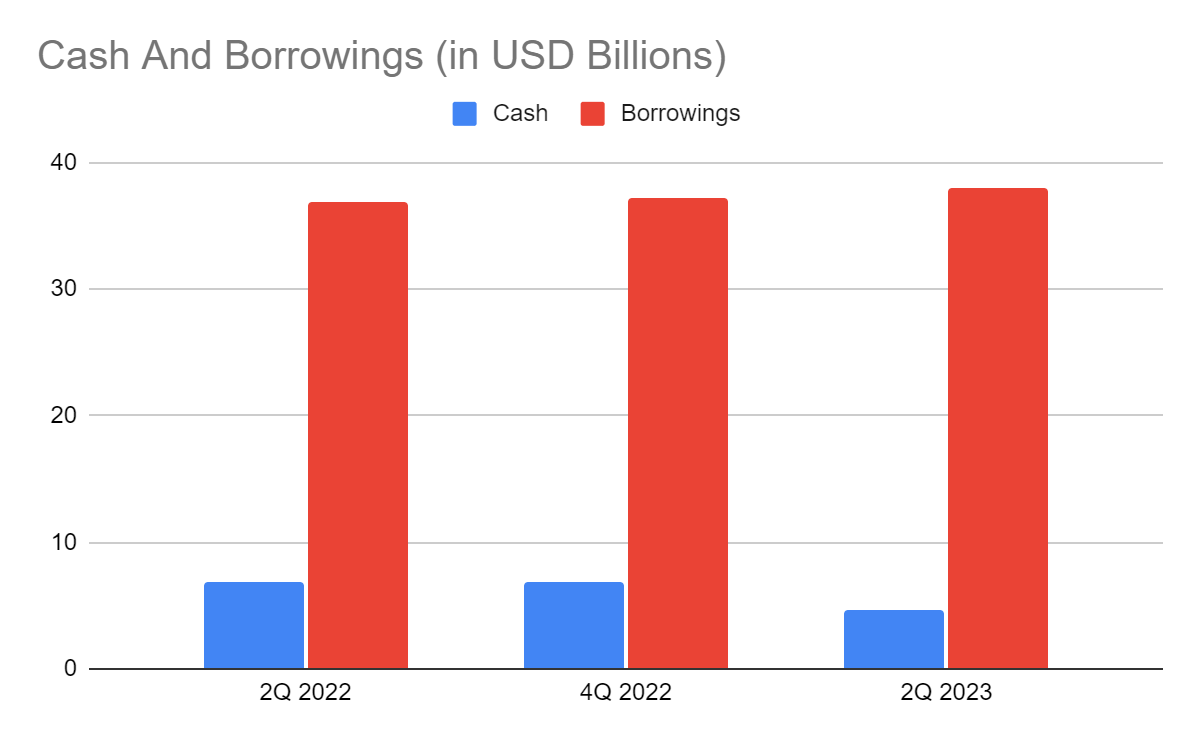

Moreover, FedEx must improve liquidity to withstand volatility. Cash remains relatively stable but low at $4.7 billion. Meanwhile, borrowings are about eight times as large as cash. Also, borrowings comprise nearly half of the total assets. As such, FedEx may be overleveraged. It is a crucial factor to consider since it is a capital-intensive company. It needs adequate cash reserves, given the massive capital for its business operations. Given these figures, FDX relies heavily on borrowings to sustain its current capacity. It is even riskier for a company as large as FedEx. It may lead to more cash burns or higher financial leverage. Also, it must beware of interest rate hikes that may intensify this year. The cost of borrowing may become more expensive. It may struggle to keep up with maturities despite its rebound potential.

{kind=link}

Cash And Equivalents And Borrowings (MarketWatch)

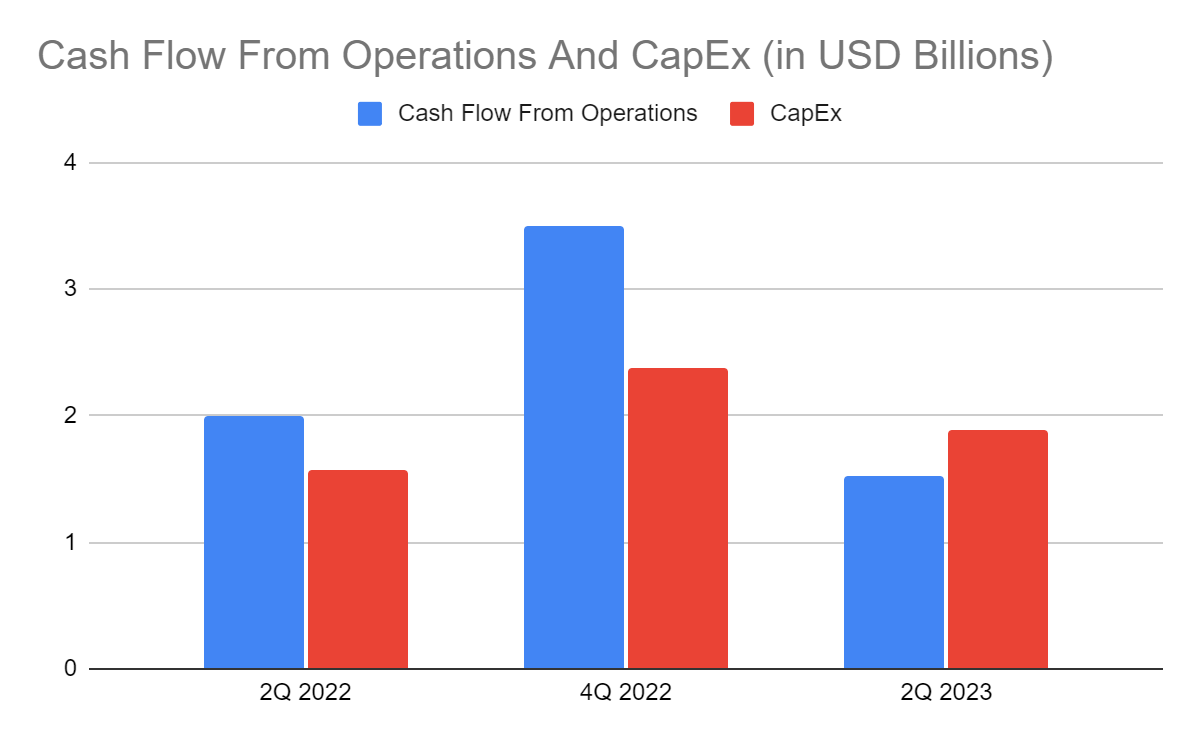

We can confirm it with the negative value of FCF. Cash inflows from operations cannot cover CapEx, leading to increased borrowings. Meanwhile, its Net Debt/EBITDA ratio remains acceptable at 3.88x, but it is near the maximum of 4-4.5x. The company must find ways to improve fundamental stability. For instance, it may repay borrowings to avoid higher interest expenses. Since cash levels are far lower, it may issue more shares. It may also lower its operating capacity to prevent more cash burns.

{kind=link}

Cash Flow From Operations And CapEx (MarketWatch)

Stock Price Assessment

The stock price of FedEx Corporation has been increasing sharply in the last four months. But it did not rebound to its 2022 average highs. At $207.98, the stock price remained 13% lower than its value last year. It may be a good discount, as shown by the PB ratio. Its current BVPS is 95.54, while its PB multiple is 2.18x. Also, it is better than the 2019-2022 average of 2.26x. Using the average PB multiple and current BVPS, the target price will be $215.93. But the EV Model gives a target price of ($81.38 B EV - $33.43 B Net Debt) / 252,397,000 shares = $189.98. It shows that the stock price is already excessive.

Meanwhile, dividends continue to increase, with enticing yields of 2.17%. It is better than the S&P 500 average of 1.68% but lower than UPS with 3.5%. If we use the PB Ratio target price, the dividend yield will still be attractive at 2.13%. Dividend payments are also well-covered, given the dividend payout ratio of 37%. However, investor returns in 2019-2022 were low. The change in the stock price was only 81% of retained earnings. So for every $1 increment in retained earnings, the stock price only increased by $0.81. In the last two years, returns have skyrocketed as FDX expanded and enjoyed a demand influx. The stock price also increased substantially in response. Despite this, their respective increases were not proportionate. The stock price increase was meager relative to earnings. The stock price has risen by 52%, but earnings were nearly thrice its value. As such, there has been a noticeable growth disparity. Their gap remains wide today even if both are increasing. To assess the stock price better, we will use the DCF Model.

FCFF $3,050,000,000

Cash $4,640,000,000

Borrowings $38,000,000,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 252,397,000

Stock Price $207.98

Derived Value $112.35

The derived value also shows potential overvaluation. The current stock price does not reflect the intrinsic value of the company. Despite this, we can see why the stock price increase cannot catch up with earnings. It may be because the stock has long been overvalued. As such, there may be a 54% downside in the next 12-18 months. Dividend investors may appreciate it. But we like it better since it can become an ideal point to sell shares and derive gains.

Bottom Line

FedEx Corporation is still stable despite the hammered growth. However, it must improve its fundamentals to navigate a rugged market. Cash levels and borrowings are troublesome, which affects its sustainability. It may be riskier as market headwinds may affect its performance this year.

Moreover, the stock price does not seem cheap despite the target price using the PB Ratio. It does not match company returns and intrinsic value, making it an expensive stock. Dividends may be a consolation, but they are not worth the risk. The recommendation is that FedEx Corporation is a sell.

For further details see:

FedEx: When Size Doesn't Matter