FEN - FEI: Underperforms The Index But Still A Good Fund

2023-09-14 18:04:01 ET

Summary

- First Trust MLP and Energy Income Fund Common has delivered a solid performance among energy infrastructure funds with a 10.88% total return year-to-date.

- The FEI closed-end fund could continue to deliver respectable returns due to the potential undersupply of crude oil and rising energy prices.

- The fund invests in the common equity of midstream partnerships and corporations, providing access to a larger investment universe than the MLP index.

- The fund's distribution appears to be sustainable, although its yield is only 7.43%.

- The fund is currently trading at a very attractive discount on net asset value.

A few days ago, we discussed the popular First Trust Energy Income & Growth Fund ( FEN ), which has long been heralded as one of the better midstream partnership funds in the market. Unfortunately, that fund was shown to chronically underperform other energy infrastructure funds from the same fund sponsor.

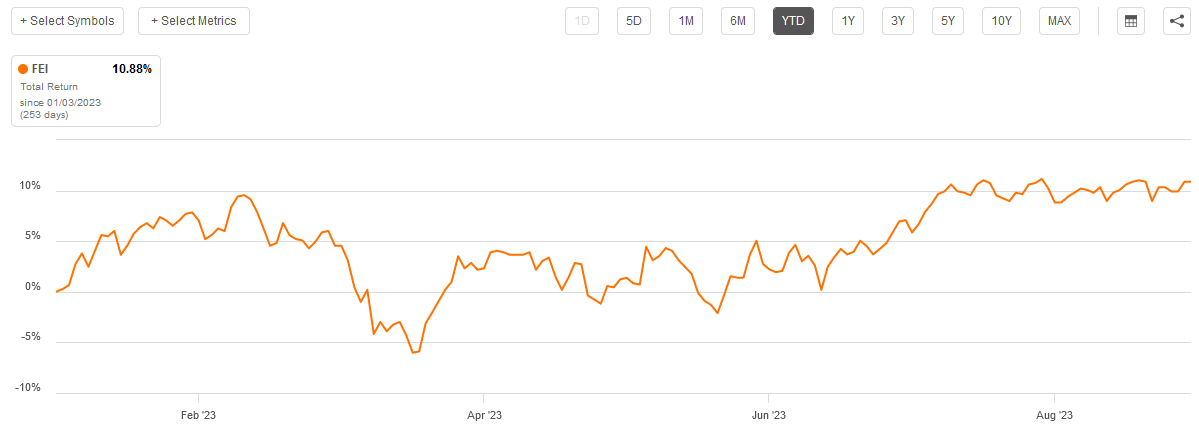

In this article, we will discuss the First Trust MLP and Energy Income Fund Common ( FEI ), which was shown to perform much better in terms of total return. In fact, this fund has delivered an impressive 10.88% total return year-to-date:

{kind=link}

There are some reasons to expect that this fund could continue to deliver respectable returns going forward. As I discussed in a recent article , the world could be significantly undersupplied with crude oil relative to demand during the final quarter of this year. That could cause energy prices to continue the upward momentum that we have seen over the past two months. If this were to happen, most things connected to the energy industry would see buying pressure. While the cash flows of the companies that the First Trust MLP and Energy Income Fund invest in are for the most part not affected much by energy prices, the price of their shares and partnership units in the market most certainly is. As such, this fund could be a reasonable way to play rising crude oil prices and earn an attractive 7.43% yield today.

It has been a little while since we last discussed this fund, as the most recent focus article dates back to February. As such, it is a good idea to revisit it and see what changes have been made to the fund’s portfolio as well as the overall business environment since that time. In addition, the fund has released a more recent financial report than what was available the last time that we discussed this fund, so we will naturally want to review this as well. Therefore, let us discuss this fund and see if it makes sense to purchase its shares today.

About The Fund

According to the fund’s website , the First Trust MLP and Energy Income Fund has the stated objective of providing its investors with a high level of total return. As is usually the case, the website provides a much more detailed description of the fund’s objectives and strategy:

First Trust MLP and Energy Income Fund is a non-diversified, closed-end management investment company. The Fund’s investment objective is to seek a high level of total return with an emphasis on current distributions paid to common shareholders. Under normal market conditions, the Fund invests at least 85% of its managed assets in equity and debt securities of publicly-traded MLPs, MLP-related entities and other energy sector and energy utility companies that the Fund’s Sub-Advisor believes offer opportunities for growth and income.

Despite the fact that the fund’s description of its strategy states that it invests in both equity and debt securities of energy infrastructure companies, the portfolio currently consists entirely of common equity and cash:

CEF Connect

It is perhaps not surprising that the fund would opt to focus its attention on common equity right now considering that the objective is to maximize total return. After all, pretty much all bonds and other fixed-income securities have been getting punished over the past eighteen months or so as the Federal Reserve’s monetary tightening policy has been raising interest rates and pushing down bond prices. However, there may be another reason for focusing on common equity as opposed to bonds considering that this fund specifically states that this fund invests in master limited partnerships.

In some industries, bonds will have higher yields than common equity issued by the same company. After all, the S&P 500 Index ( SPY ) yields 1.46% today. Nobody in their right mind would buy a corporate bond yielding 1.46%, although Treasuries have traded for such yields in the past. The Bloomberg U.S. Aggregate Bond Index ( AGG ) yields 3.02% as of the time of writing, so we can make the general statement that bonds tend to have higher yields than equities. This makes sense considering that bonds deliver all of their net investment returns in the form of the interest that they pay. It is certainly not the case that a stock’s dividend is the only return that investors will earn from it, despite what the dividend discount model claims. The effective yield of master limited partnerships is considerably higher.

As of right now, the Alerian MLP Index ( AMLP ) yields 7.99%, but it has had higher yields in the past. That is much better than bonds, as even the Markit iBoxx USD Liquid High Yield Index ( HYG ) that tracks junk bonds yields 5.74% today. When we combine the higher yield of master limited partnership common equity versus bond and the potential for capital gains that we get with the equity, it makes sense for any fund focused on total return to be fully invested in the common equity of midstream partnerships or corporations.

As long-time readers are no doubt well aware, I have devoted a considerable amount of time and effort over the years to discussing various midstream partnerships and corporations here at Energy Profits in Dividends as well as at Seeking Alpha. As such, the largest positions in the fund will certainly be familiar to just about any reader. Here they are:

First Trust

I have discussed every company on this list except for Cheniere Energy Partners ( CQP ) multiple times over the years. Cheniere Energy Partners should still be reasonably familiar though, as it is simply a master limited partnership that owns a stake in one of Cheniere Energy’s ( LNG ) liquefaction plants. As such, its fundamentals are quite similar to those of the parent, which I have discussed multiple times in the past. In fact, the primary difference between the two entities is that Cheniere Energy Partners sacrifices some growth and upside potential for yield. Thus, overall, these companies should all be pretty familiar.

Despite the fact that more than six months have passed since we last discussed this fund, the portfolio has changed only slightly. The only change to the largest positions list is that Kinder Morgan ( KMI ) was removed and replaced with Plains All American Pipeline ( PAA ). Otherwise, the only change is that the weighting of several of the positions is very different than it was the last time that we discussed this fund. However, that can easily be explained by one company outperforming another in the market. It is not necessarily a sign that the fund is actively trading positions in order to change its weightings. As such, we might assume that this fund has a fairly low annual turnover. I explained why this is important in my last article on the fund:

The reason that this is important is that it costs money to trade equities or other assets, which is billed to the shareholders of the fund. This creates a drag on the fund’s performance and makes management’s job more difficult. After all, the higher the fund’s trading expenses, the higher a return management needs to generate in order to cover these costs and still give shareholders an acceptable return relative to the index. This is a task that very few management teams manage to accomplish on a consistent basis, which is one of the reasons why actively managed funds tend to underperform their benchmark index.

The First Trust MLP and Energy Income Fund had a 51.00% annual turnover during the full-year period that ended on October 31, 2022. This is, unfortunately, the most recent date for which that information is available. This is right about the median for an equity closed-end fund, especially one that invests in the energy infrastructure sector. However, it is still considerably more than the 26.00% annual turnover of the Alerian MLP ETF during the full-year period that ended on November 30, 2022.

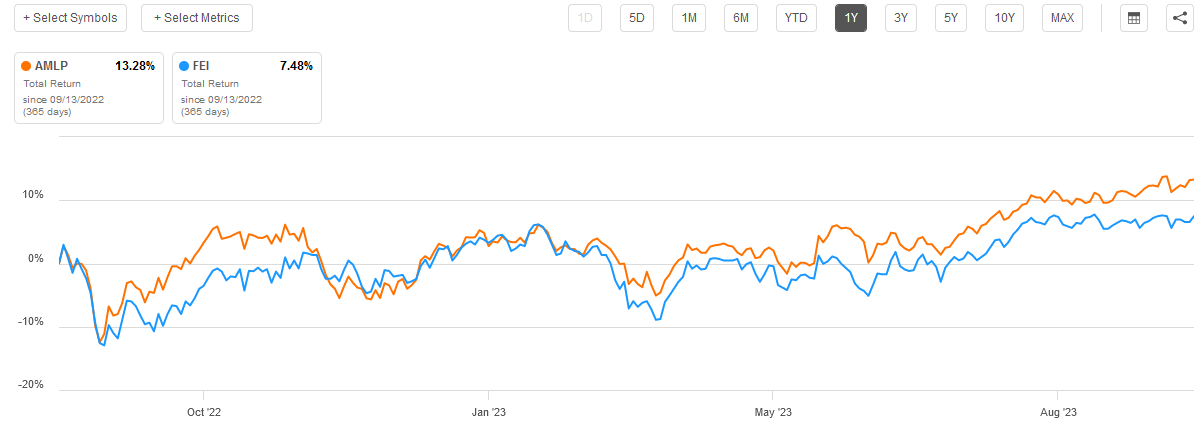

Unfortunately, the First Trust MLP and Energy Income Fund’s total return has lagged that of the Alerian MLP ETF over just about any relevant period. For example, over the past year, the First Trust Fund delivered a 7.48% total return, which is admittedly not horrible considering the poor returns of many other things in the market over the same period. However, it was still much worse than what the index fund managed to deliver:

{kind=link}

The same applies to the trailing three-year period, the trailing five-year period, and the trailing ten-year period. During all three time periods, the First Trust Fund underperforms the index. Interestingly though, its movements tend to be very much in lockstep. We can see that in the chart above, as the light blue chart looks very similar to the orange line with the exception of a small handful of periods in which the index delivers a bit stronger return. Nearly all of the performance differences between the two funds can be explained by such events. Regardless though, the index fund does deliver better total returns over time and has a higher distribution yield.

The only real advantage that the First Trust MLP and Energy Income Fund has over the index is access to a larger investment universe. The Alerian MLP ETF only invests in companies that are structured as master-limited partnerships. That is, to put it mildly, a dying business model. Over the years, various activist investors and others have pushed partnerships to convert to corporations in order to improve their capital gains. There are some problems with including partnerships in retirement accounts as well as most mutual funds, so converting to a corporate structure does increase the amount of capital that can purchase these companies. At the same time though, conversion to a corporate structure causes the company to lose certain tax benefits.

The point, though, is that because of this, the Alerian MLP ETF is limited to holding only sixteen companies. The First Trust Fund can hold many more firms than that, and if corporations really do give better returns than partnerships, the First Trust MLP and Energy Income Fund should be in a much better position to take advantage of that than the index fund. As of right now, though, this does not seem to be much of an advantage.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the First Trust MLP and Energy Income Fund is to provide its investors with a high level of total return. However, the fund seeks to achieve this objective by investing in master limited partnerships and companies that function very much like master limited partnerships. These companies deliver the majority of their returns in the form of direct payments to their unitholders or shareholders. The fund collects the money paid out by these companies, as well as any net realized capital gains, and pays it out to its shareholders net of what is required to cover the fund’s own expenses.

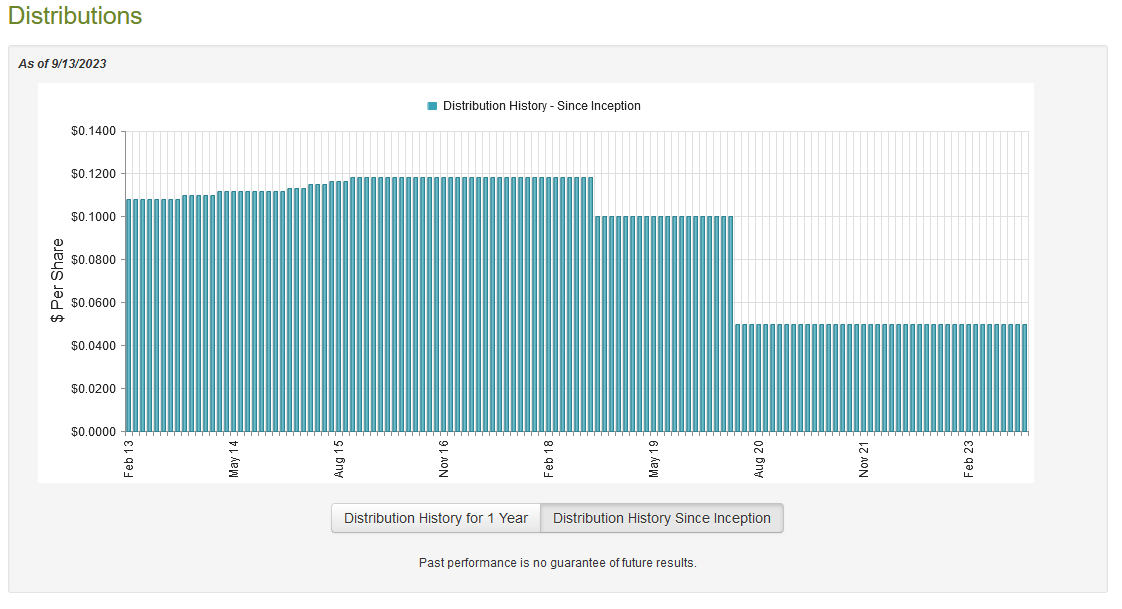

As master limited partnerships and midstream corporations tend to have fairly high yields, we can probably assume that this fund does as well. That is certainly the case, as the fund pays a monthly distribution of $0.05 per share ($0.60 per share annually), which gives it a 7.43% yield at the current share price. This is a reasonable yield, but unfortunately, this fund has not been very consistent with its distribution over the years. In fact, as we can see here, it has cut the payout multiple times:

{kind=link}

While the fund generally did pretty well in the first few years of its existence, its shine started to wear off around 2015. This is somewhat understandable as 2015 and to a lesser extent, 2016 brought a great many changes to the industry. That was the time period in which Saudi Arabia and the other major oil-producing nations were deliberately producing more crude oil than was needed to meet global demand in an attempt to bankrupt the American shale industry. While midstream companies tend to be relatively stable in terms of cash flow, this still caused shakeups across the industry due to the market’s belief that anything related to the fossil fuel industry was toxic. As a result, numerous companies cut their distributions and redirected their capital to improve their balance sheet strength. We saw the same thing happen in 2020 when the COVID-19 pandemic caused the global demand for crude oil to crash, and energy prices once again collapsed. In both cases, the temporary drop in midstream market prices and distributions forced the fund to cut its payout in order to ensure that its capital remains intact.

The most disappointing thing here is that the fund’s distribution has not been increased over the past year or two, as many other energy infrastructure funds have boosted the distributions that they give to shareholders now that the industry has generally recovered.

With that said, anyone buying the fund today will receive the current distribution at the current yield so events that occurred in the past are not necessarily the most important thing for current investors. The most important thing is how well the fund can sustain its current distribution going forward. Let us investigate that.

Fortunately, we do have a fairly recent document that we can consult for the purpose of our analysis. The fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is a much more recent report than we had available the last time that we discussed this fund, which is nice because it should give us a good idea of how well it performed in much of the first half of this year, which was not nearly as strong of an environment for energy companies as we saw in the first half of 2022. The relative recency of this report is also nice because it will give us much better insight into how sustainable the fund’s distribution is than an older report would.

During the six-month period, the First Trust MLP and Energy Income Fund received $5,089,887 in dividends and $226,341 in interest from the investments in its portfolio. This gives the fund a total investment income of $5,316,228 during the period. The fund paid its expenses out of this amount, which left it with a net investment loss of $137,707 over the six-month period. In this case, the fund’s expenses exceeded its total investment income. Obviously, it did not have nearly enough net investment income to cover the $13,568,671 that it paid out to its shareholders as distributions during the period. At first glance, this is almost certainly going to be very concerning.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. For example, this fund invests heavily in master limited partnerships that will pay distributions. These distributions are not considered to be investment income for tax purposes though, so they would not be considered in the figures given above. In addition to this, the fund might have been able to earn some capital gains that could be paid out to the shareholders. Fortunately, the fund did have some success at this as it reported net realized gains of $6,601,591 and another $4,601,384 in net unrealized gains during the period. These were more than enough to offset the net investment loss but still not enough to cover the distribution. In all, the fund’s net assets declined by $2,503,403 after accounting for all inflows and outflows during the period.

This is disappointing, but at the moment it is nothing that we need to worry about. During the full-year period that ended on October 31, 2022, the fund’s net assets increased by $39,426,830 after accounting for all inflows and outflows. That was more than enough to cover the shortfall in the first half of the fund’s fiscal year. Overall, this distribution should be fine, especially now that the energy sector is strengthening again.

Valuation

As of September 13, 2023, the First Trust MLP and Energy Income Fund has a net asset value of $9.36 per share but the shares currently trade for $8.10 each. This gives the fund’s shares a 13.46% discount on the net asset value at the current price. That is a very reasonable discount to pay for any fund, but it is only in line with the 13.10% discount that the shares have averaged over the past month. However, the current price for this fund is still very reasonable so anyone that is interested in it may want to consider a purchase today.

Conclusion

In conclusion, the First Trust MLP and Energy Income Fund is a reasonable way to play the midstream sector right now considering that it has begun to strengthen on the heels of improving energy prices. Unfortunately, this fund does fail to match the performance of the Alerian MLP ETF over time and it has a lower yield, so it may not be the most attractive way to play the sector. The fund’s ability to invest in corporations could give it a bit of an advantage though, if you truly believe that the corporate structure is a better business model. The fund’s huge discount on its intrinsic value is also a nice bonus. Overall, there could certainly be some reasons to consider this fund today.

For further details see:

FEI: Underperforms The Index, But Still A Good Fund