FEMY - Femasys: A Women's Health Medical Devices Company Ready To Turn The Corner

2023-11-28 08:40:23 ET

Summary

- Femasys is a medical device company that offers a suite of minimally invasive reproductive health products for women.

- The company recently received clearance for its FemaSeed product and plans to launch it in early 2024.

- Femasys is also developing a device called FemBloc for permanent birth control and a device called FemCerv for cervical tissue biopsy.

- The Company recently raised $18M in an ATM draw, and through a convertible note - potentially funding to cash flow positive in 2026.

Femasys - Overview

Femasys (FEMY) (the "Company") is a commercial-stage medical device company that has a suite of products minimally invasive reproductive health products for women, all of which are designed to be used in the gynecologist's office. The commercial stage devices include FemaSeed, a device for insemination, FemCath and FemVue, a device and diagnostic approach for selective fallopian tube blockage evaluation, and FemCerv, a device for cervical tissue biopsy. In development, the Company is currently running a registration-enabling study on FemBloc, a device to provide permanent birth control. Ultimately, the Company's portfolio is designed to provide gynecologists with a broad set of in-clinic women's health tools spanning from general health, to fertilization, to pregnancy prevention.

Femasys was founded in 2004 and went public in June 2021 at $13 per share, rising approximately $32M after fees and expenses. The Company then followed the general market downward for the next two years. Operationally, the Company continued to execute its plan. The Company recently received 510(k) clearance for its FemaSeed product, which created a flurry in the market. Its stock ran from $0.33 to an intraday high of $4.75 a few days later, only to fall back to the $1 range.

During that flurry of activity, the Company used its ATM to raise $11.3M. Subsequently, the company raised an additional $6.8M in a convertible note and issued warrants that could raise an additional $15M in the coming years if the stock price cooperates. The primary risk factor preventing me (and others I assume) from holding a full position has been the risk of financing. The market has severely punished any company that was not fully funded. Based on my model, it appears that the Company has dramatically reduced that risk with the two recent funding events, which will allow investors to focus on the execution, instead of being caught under the financing overhang.

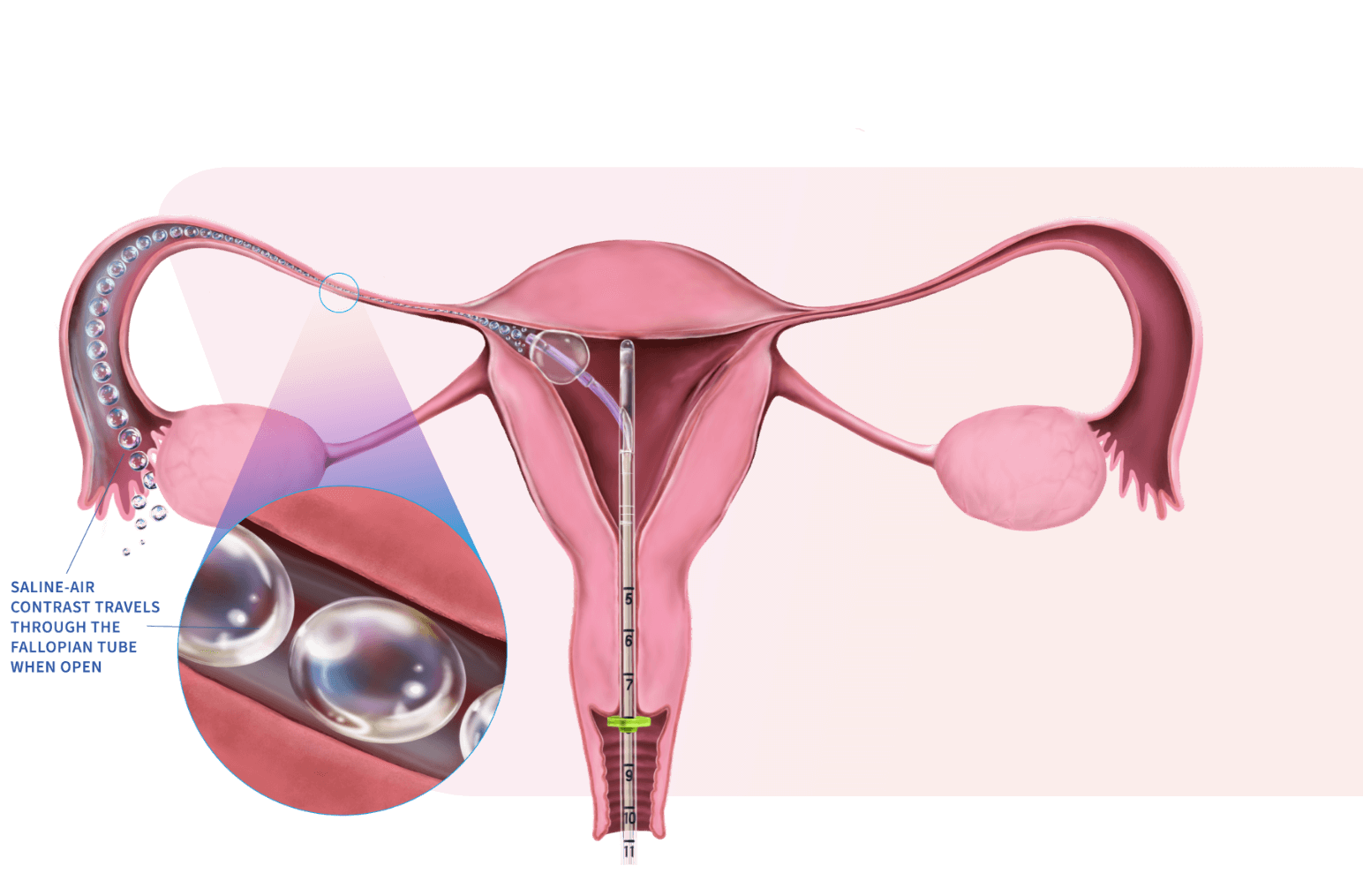

FemVue and FemCath- Fallopian Tube Assessments

FemVue is a device that injects saline and air into the fallopian tube through a catheter. FemVue was first 510(k) cleared as a medical device in 2009 . The Company improved the product and submitted additional 510(k)'s over the subsequent years. FemVue injects bubbles composed of saline and air into the fallopian tubes and allows an ultrasound technician to assess any blockage in the fallopian tubes. For instances where precision is needed to target a specific tube, the FemCath device provides a directional, inflatable balloon to open up the chosen fallopian tube.

{kind=link}

Figure 1: FemVue and FemCath. Source - Femasys .

According to the CDC, in 2015 approximately 7.3M women sought fertility services . While it is not specifically cited in the data, one can assume that a fallopian tube check is a routine part of that service. Prior to FemVue, it was standard to send a woman to radiology to have her fallopian tubes checked for blockage. The test is called a hysterosalpingography, or HSG. FemVue allows gynecologists to perform the fallopian blockage check in the office with an ultrasound device.

In 2019, Exem® Foam was approved by the drug division of the FDA as an ultrasound contrast agent for a sonoHSG. Exem® contains hydroxyethyl cellulose, glycerin, and purified water . Hydroxyethyl cellulose is a commonly used thickening agent found in cleaning solutions, cosmetics, and other household products. Exem Foam Inc. is a private company with revenues less than $5M , according to ZoomInfo , and is the only direct competitor to the FemVue product.

To date, Femasys has not had an active sales force promoting FemVue. The price point is less than $100 a procedure. Without the full suite of products, it did not make sense for the Company to invest in a sales force. Now that FemaSeed is cleared for marketing, the Company will be creating a small sales force to support its growing suite of products.

Given the Company's expected 2023 sales of $1.2M, and the price point, the Company will likely sell ~12,000 FemVue's this year. There are approximately 450 fertility clinics in the US. According to the Company, there are fewer than 20 large chains of clinics, which should allow them to hire a very small sales force to target a large percentage of the market. To better address the cadre of independent clinics scattered across the country, the Company has been building a portfolio of training modules to allow them to provide virtual support.

Despite having no sales force, the Company has been in the market for a number of years and believes it has solid brand recognition for the FemVue product. They believe they can use the FemVue product awareness to quickly introduce additional products as they build a sales force.

FemaSeed - Intratubular Insemination

FemaSeed is a medical device designed to deliver sperm directly into a fallopian tube. Femasys received 510(k) clearance for FemaSeed in September this year and expects to launch the product in early 2024. Importantly, the Company expects to complete an open label, single arm clinical trial for FemaSeed in women whose male partners have low motile sperm count. The study addresses one of the major factors in infertility - the male part of the equation.

Company Website

Figure 2: FemaSeed insemination device. Source-Femasys .

It is estimated that approximately 500,000 artificial inseminations occur per year in the US . The procedure is currently performed with a catheter designed to deposit sperm into the uterus. The sperm is placed in the back of the uterus, near the openings to the fallopian tubes. FemaSeed was designed to inject sperm directly into the fallopian tube, directed toward the ovulating side.

According to the literature, intrauterine insemination ("IUI") is the most common form of artificial insemination done by doctors, versus intratubular ("ITI") and intracervical ("ICI"). One study that aggregated data from multiple studies amalgamates the success rate of becoming pregnant with ICI is 14%, and 51% with IUI when using the woman's natural menstrual cycles. The odds increase to 38% and 63% for ICI and IUI, respectively, when the woman is on gonadotropin stimulating therapy.

In one study performing a direct comparison of IUI with ITI, the clinical pregnancy rate (defined by the presence of fetal cardiac activity) was 12% for IUI, versus 22% for ITI . In another study , it was 47% for ITI and 18% for IUI .

If ITI > IUI > ICI, then why wouldn't every doctor use the ITI procedure for insemination? I believe that the broad literature is inconclusive. There were a few meta-analyses in 2004 and 2013 that point toward not seeing a benefit in ITI versus IUI. The 2013 meta-analysis claimed a 19% chance of pregnancy for ITI and between 10%-20% chance of for IUI. Additionally, on fertility websites, there are statements that suggest that ITI has a safety risk. "Unfortunately, intratubal insemination has been associated with greater risk for infection and trauma, and there's a debate on whether it's more effective than regular IUI." Source - Very Well Family website . Of course, there is no data source cited.

When looking at some of the single site studies, where the procedures and patient characteristics would have been most controlled, there is clear evidence that ITI is better than IUI. In general, I believe meta-analyses are great for huge indications, like hypertension. In smaller indications with smaller numbers, and potentially different inclusion/exclusion criteria, those types of studies are noisy at best, and worthless science at worst. As an example, a 1997 study of 100 patients compared the standard IUI procedure with an ITI procedure using a Foley catheter designed for pediatric use. The study showed an 8% pregnancy rate for ITI, and a 20% rate for IUI. The study only collected data on 1 cycle, noted the potential for issues relating to the use of a pediatric Foley catheter not designed for insertion into the fallopian tubes, and cited another paper that reported a 40% rate for ITI and a 20% rate for IUI . Additionally, the 2004 and 2013 meta-analyses were written by the same group.

Ultimately, Femasys needs to create its own data, using its own device, to report pregnancy success rates and probabilities of complications. When doctors rely on data from the 90's, they risk not doing the right thing for patients, or not realizing that they are comparing apples to pineapples. It is, however, incumbent on the Company, to educate the field about the latest data, which will take time and effort. By mid-2024, the Company should have data on their male low sperm motility trial. That study will be very useful in opening doors, and reframing the ITI discussion with a new device that was actually made to safely inject sperm into the fallopian tube, not a repurposed pediatric catheter.

In the US, there were approximately 330,000 inseminations in 2020 , performed at 450 clinics. The total addressable market ("TAM") for FemaSeed is approximately $330M in the US, assuming a $500 price point and an average of 2 cycles of treatment per successful insemination. There is likely a similar market size available in Europe and Asia.

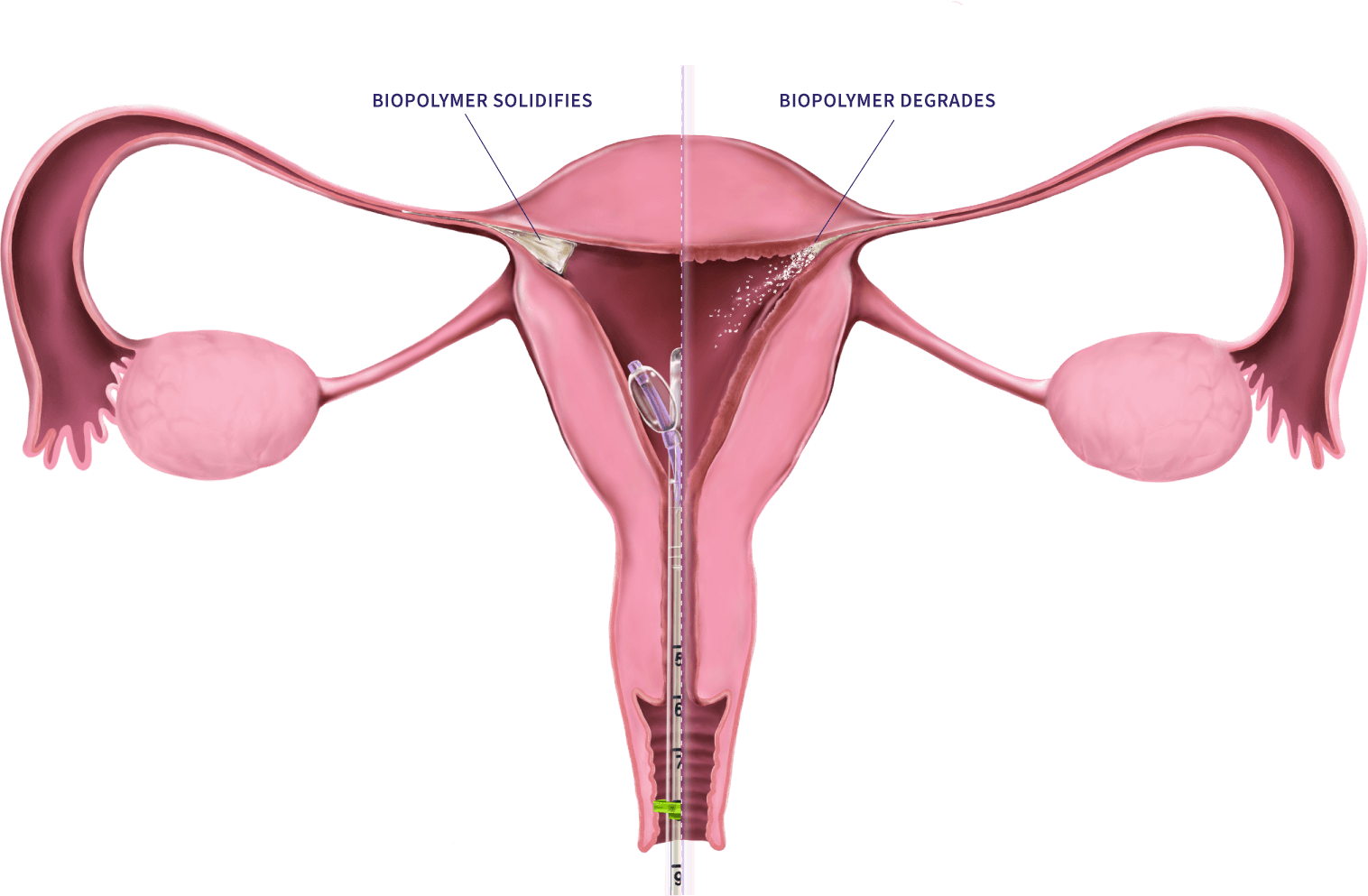

FemBloc - Permanent Birth Control

FemBloc uses the same device as FemaSeed, but instead of injecting sperm, a biopolymer is injected into the fallopian tube. The biopolymer then causes the fallopian tube to occlude, creating permanent blockage. After 90 days, the gynecologist can then use FemVue to confirm successful occlusion. The device can be used in the office and does not require a surgical procedure.

The current standard of care is to perform a tubal ligation (getting the "tubes tied"), a surgical procedure where the fallopian tubes are cauterized, or burned, to sever and seal the fallopian tubes. The tubal ligation procedure as a stand-alone, can cost $6,000 or more. Women have the option of getting the procedure done during a cesarean section, but they would need to make that decision on that option prior to giving birth, if the birth heads that direction.

{kind=link}

Figure 3: FemBloc birth control device. Source - Femasys .

FemBloc could be done in the office and is expected to cost less than $3K, including the office visits and the cost of the device. There are approximately 600,000 tubal ligations per year in the US. Assuming half of the tubal ligations are done during the c-section for their final child, then the TAM is approximately $600M, assuming $2,000 per procedure. There are also approximately 200,000 vasectomies per year - some portion of those procedures could be offset by FemBloc as well. If FemBloc is proven to be safe and easy, then it could take market share from women who are on pills, IUDs or implants for life, but do not wish to have a surgical procedure. That market is north of 10M women.

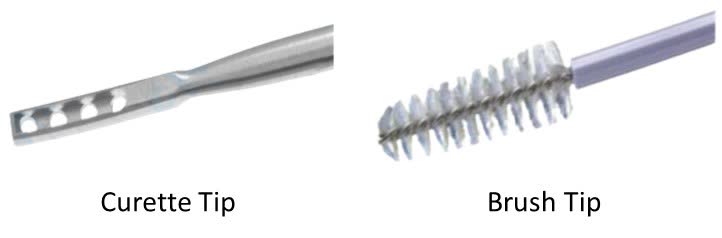

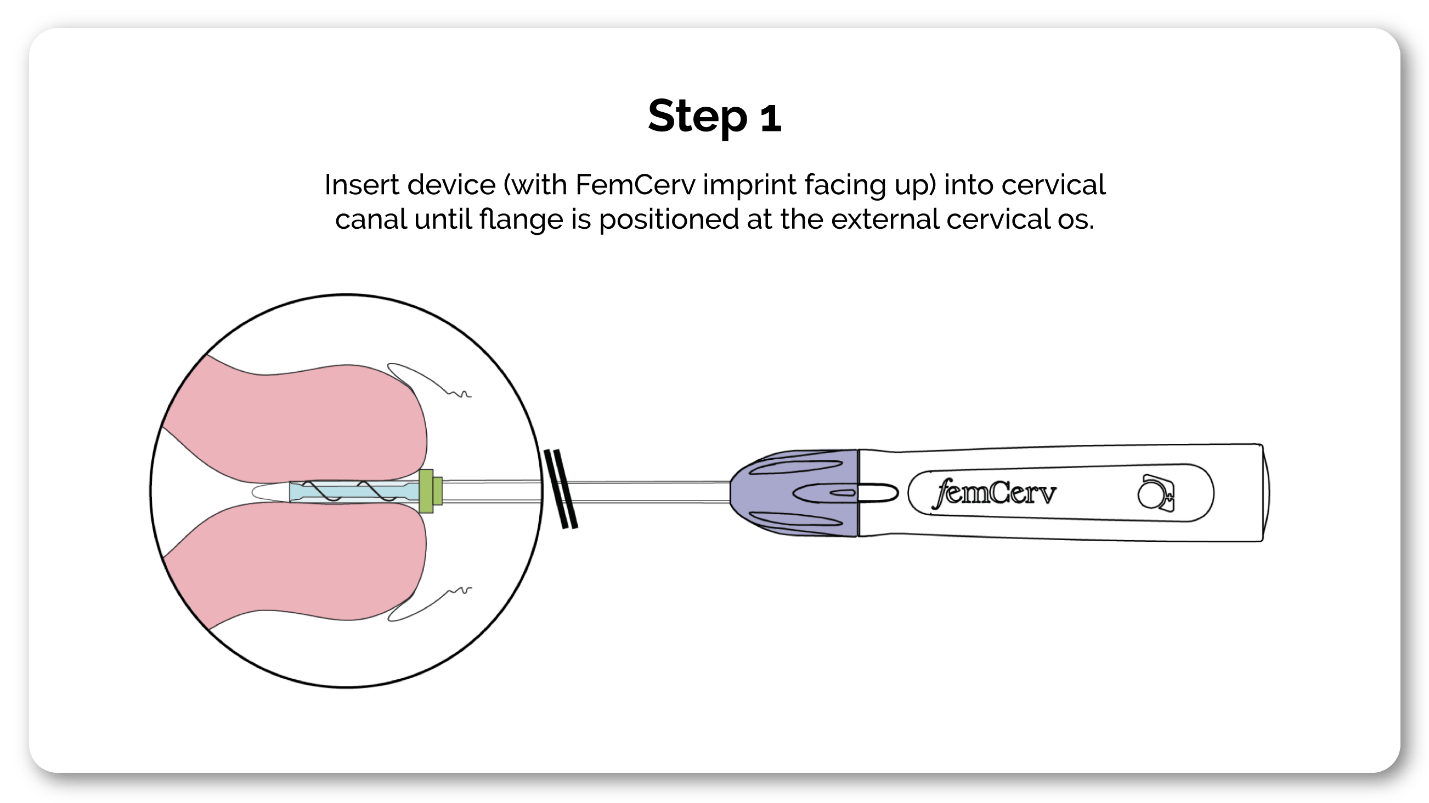

FemCerv - Cervical Biopsy

FemCerv was 510(k) cleared in December 2012 . FemCerv was designed to gently insert into the cervix, extract a tissue sample with as little pain as possible, and protect the sample from contamination during retraction of the tool. When compared to the standard tools, curettes and brushes, it seems ripe for disruption, aside from the cost advantage of the standard tools.

{kind=link}

Figure 4: Biopsy tools. Source - Femasys .

FemCerv was designed with the patient in mind, to minimize the pain of insertion into the cervix and of sample collection. From its clinical study, 92% of doctors found the device easy to insert, 95% of patients reported no or mild discomfort, and an adequate sample was collected in 94% of the procedures. The Company has yet to market FemCerv but may do so as part of a broader suite of products.

{kind=link}

Figure 5: FemCerv biopsy device. Source - Femasys .

Management Team

The Company has a very experienced management team.

| CEO & Founder |

| Kathy Lee-Sepsick

|

| CFO |

| Dov Elefant

|

| CMO |

| Edward Evantash, MD

|

The Company has a complete team of experienced executives, as one would expect from a development-stage medical device company. To date, the Company has not ramped up its sales and marketing efforts beyond a skeleton crew. They were wisely waiting to have enough commercial products to be worth the investment. Now that FemaSeed is 510(k) cleared, the Company has declared its intent to start investing in those capabilities. Given their last few years of living on a shoestring budget, I would not expect them to ramp up spending quickly.

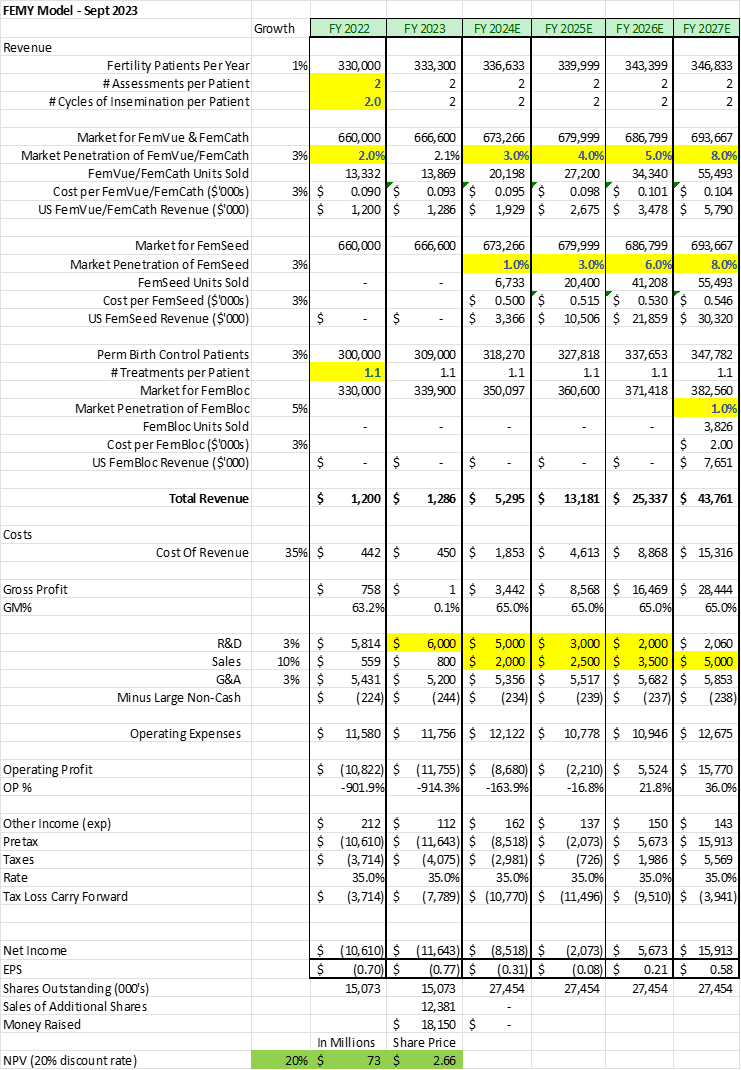

Proforma Model

When modeling the Company, I have made the following assumptions:

- 330,000 annual fertility patients per year, going through 2 cycles of insemination

- 300,000 annual sterilization patients per year, doing tubal ligation, not during c-section

- The Company will finish 2023 with $19.5M in cash

- The Company will increase its sales and marketing expenses slowly over the next 4 years

- FemVue market share will jump each time a new product is launched and promoted

- Pricing: FemVue ($95 in 2024), FemaSeed ($500 in 2024), FemBloc ($2k in 2027), growing 3% per year

- 35% COGS, 20% Discount Rate, Modeled to 2035, No Terminal Value

{kind=link}

With a very conservative assumption of the Company being able to achieve 8% market share in each product's respective markets, I estimate the NPV to be ~$70M. If they are able to achieve a higher share or become a standard of care, then obviously the valuation would become much higher.

On a recent stock price run, the Company raised $11.3M, and subsequently sold a convertible note for $6.8M. With these cash injections, I model that the Company has the ability to achieve cash flow positive without raising additional capital - assuming they are able to start increasing the revenue with the launch of FemaSeed, and by pro-actively marketing FemVue. The stock has fully shifted to an EBIT play, so each quarter will need to start showing revenue growth.

Analyst Coverage

The Company is covered by HC Wainwright ($10 target), Chardan ($12 target), Maxim ($5 target) and Jones Trading ($7 target). The price targets all suggest a 5x or greater return from today's stock price. The analysts have a wide range of 2024 revenue estimates (from $3M to 19M).

Insider Buying Activity

It does not appear that management has purchased shares in the recent past. They have likely been in possession of non-public, material information for a large portion of time during the last few years because of their development stage pipeline. After this quarterly earnings call, they may have a window to show investors that they believe in themselves.

Major Holders

FEMY does not have any institutional holders over 5%. Insiders own around 15%. If the Company can build institutional ownership, then I believe they have a chance at achieving a valuation that starts to align with an NPV model.

Potential Risks and Potential Surprises

1) Sales Force Effectiveness: The biggest risk to this Company, as with many others in the life science space, is future dilution. FEMY will have 4 major products approved that could help the Company exceed $100M within 5-7 years, depending on the pace of sales force activity and effectiveness. The Company has stated that its wants to take a measured approach to growing its sales force because they do not want to create a large burn without the sales to support it. This creates a chicken and egg issue. At some point, they will need to hit stride on sales force growth. The result of not becoming an effective sales and marketing company in the near term will be more dilution.

2) Financing: The Company had $8.7M in cash as of Sept 30, 2023, and raised over $18M through the ATM and recent convertible note. My model suggests that the Company does not need to raise money again if the sales grow. Therefore, the financing risk is linked to the risk of a slow launch of FemaSeed.

3) Valuation: Since the start of the pandemic, classical NPV valuation methodologies have been disconnected from public company market caps. This is especially true in the small-cap space. In June 2022, 20% of biotech companies were trading for less than the cash on their balance sheet. This disconnect may persist for a long time. Therefore, the models used to generate the stock price estimates in this report should be seen as directional. Financing risk outweighs biology risk right now.

Conclusion

FEMY is down approximately 90% since its public debut in 2021. The XBI, a biotech market index, is down 60% over that same period. This has been a brutal time in the life science market. Over the next 6-9 months, I believe that there will be further capitulation of companies that should probably dissolve. FEMY is not in that group. I believe that the Company is poised for a rebound as its shifts from the development stage, to the commercial stage. To be cash flow positive, the Company should need approximately $4.5M of revenue per quarter. The probability of success can be updated after every earning call.

Femasys has a good portfolio of products. When they turn the card on the FemBloc clinical study, I believe they have the opportunity to round out their portfolio of women's health products. They will be able to invest in sales and marketing with the faith that they can provide a suite of solutions that shift some of the current treatments into the doctor's office, changing the revenue potential of the office. My conservative growth model suggests a fair value above $2.50 right now and should exceed $5 once the company is CFP (modeled for 2026).

For further details see:

Femasys: A Women's Health Medical Devices Company Ready To Turn The Corner