FERG - Ferguson: Long-Term Compounder Facing Housing Market Downturn

2023-07-10 04:10:06 ET

Summary

- Ferguson is a high-quality business, owing to its sticky margins, high market share, and market-leading business model.

- We believe the company is facing near-term material headwinds, as Residential and Commercial market weakness will lead to reduced demand.

- The robust nature of the industry and M&A will act to offset the impact of this. Nevertheless, we expect FY24 will be difficult.

- Based on Ferguson's valuation, we do not see upside and believe the company is slightly overvalued.

Investment thesis

Our current investment thesis is:

- Ferguson plc ( FERG ) is a highly attractive business due to its high market share, deep expertise, scale, and business model.

- The industry is also attractive due to its resilience and increased infrastructure spending forecast in the coming decade.

- The near-term, however, is highly concerning. Economic conditions are dampening the Residential and Commercial property markets, contributing to reduced demand and home builds.

- We do not believe Ferguson's valuation is justified today.

Company description

Ferguson plc is a multinational distributor of plumbing and heating products, serving professional clients and consumers worldwide, in the residential, commercial, civil/infrastructure, and industrial end markets. Further, the company provides after-sales support.

Ferguson is a UK-based business that in 2022 switched its primary listing to the NYSE , coinciding with its sale of the UK business Wolseley to CD&R, becoming a wholly North American operation. It is estimated to be the largest plumbing manufacturing and retail business in the US.

Share price

Ferguson has outperformed the market in the last decade, as its strong financial profile in conjunction with its market positioning has allowed the business to generate sustained attractive returns.

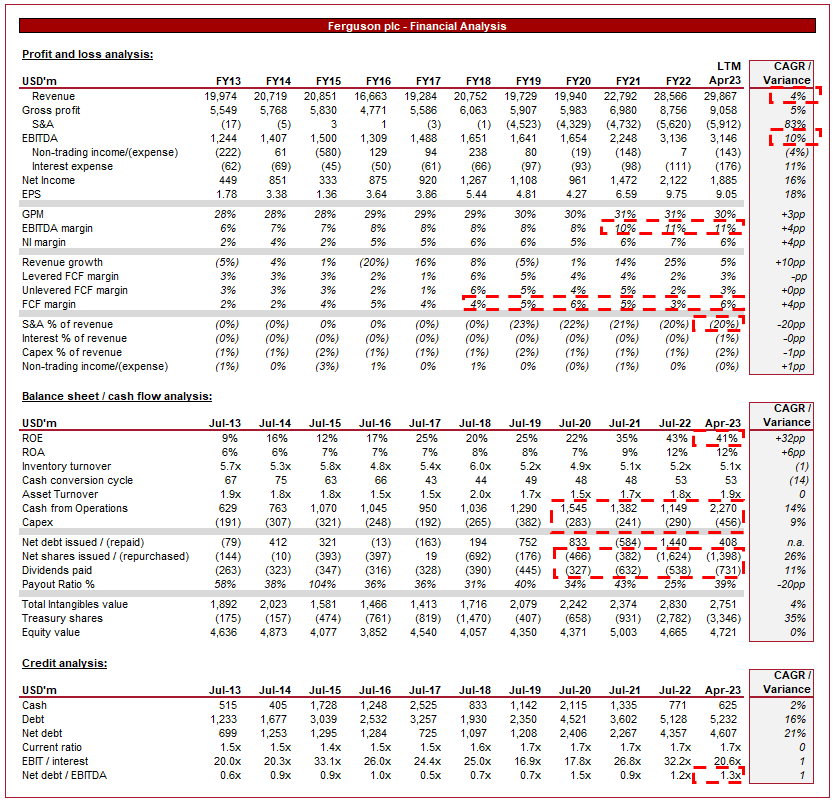

Financial analysis

{kind=link}

Presented above is Ferguson's financial performance for the last decade ( Note: due to the retrospective change from GBP to USD, historical figures before FY17 could be distorted ).

Revenue & Commercial Factors

Ferguson's revenue has grown at a CAGR of 4% during the last 10 years, with extremely consistent financial results. This is a reflection of the industry within which it operates.

Business Model

Ferguson's business model revolves around being a one-stop shop for plumbing and heating products, offering a comprehensive range of items needed for residential and commercial projects. This allows the business to benefit from scale economies while leveraging its brand and expertise to cross-sell to customers. The natural expansion of products has been highly successful for Ferguson and is one of the primary reasons for its attractiveness.

It sells its products through wholesale distributors, supply houses, retail enterprises, and e-commerce. This omnichannel approach allows the business to offer supreme convenience to its customers, improving its value proposition in the process. In many cases, the need for plumbing products is an emergency or more convenient to pick up and so Ferguson's wide reach in the US is a critical success factor.

Given the company works primarily with builders, be it in the commercial or consumer segment, it focuses on maintaining and developing deep relationships with suppliers. This revolves around ensuring a broad product offering, competitive pricing, and reliable inventory availability. The latter of this is an underrated characteristic that Ferguson supports through its omnichannel approach.

In an industry where "commoditized" products are sold, Ferguson has done a fantastic job of building a competitive position and generating consistent revenue. It has substantial scale, an unrivaled distribution network, and a brand synonymous with high quality and reliability, in an industry where this is critical.

Plumbing Industry

The plumbing industry is an example of a highly lucrative mature industry, in our view. The reason for this is that demand, in theory, should remain strong forever. With economic and technological development, the existence and strength of this industry should endure.

Despite near-term concerns (which we will discuss later), we are long-term bullish on construction. Government investments in infrastructure projects are expected to increase, spearheaded by the Infrastructure Investment and Jobs Act. Further, the demand for homes in key economic hubs will remain due to the increased concentration of high paying jobs and quality amenities such as schools, contributing to the need for new build properties. Finally, we are seeing an increased need for "megaprojects", as new technologies demand production facilities. Examples of this include semiconductor manufacturing and battery plants. These factors should drive demand for plumbing and heating products and represent an opportunity to expand its product range.

Ferguson has consistently grown through M&A, which it will continue to invest in via the utilization of excess capital. 5 transactions are expected to close in Aug23, with the pipeline healthy. These businesses are expected to contribute ~$330m in annualized revenue, which is 1.2% of FY22 revenue.

Given the large commercial base, house building is critical to the growth trajectory of the business. Greater construction will contribute to increased demand for plumbing products, a positive for Ferguson. For this reason, the company does have a degree of cyclicality.

With elevated interest rates and high inflation in the US, consumers are suffering from rising costs and a decline in discretionary income. Wage inflation has been unable to keep up, with consumers losing out in response. This has contributed to weakness in the residential housing market, as consumers are not in a position to be buying properties, as well as the risk of defaults rising. This is compounded by the factor renovations and maintenance spending on plumbing equipment is likely to be reduced where non-critical. This residential weakness is illustrated below, with concerning price movements beginning in 2022.

Alongside this, the commercial real estate industry is also faltering, as Covid-19 has transformed the way people work. With increased working from home, the demand for offices is softening rapidly, with many businesses downsizing.

As home prices decline / economic conditions deteriorate, those who can, sit tight and do not make large purchases. This is illustrated below, with pending home sales rapidly declining in 2022.

These two factors contribute to a significant reduction in the demand for homes. Those forced to sell are unlikely to buy an expensive new home, and those who can financially afford it are unlikely to do so.

With such bearish residential conditions, home builders are disincentivized to build new properties. This is not expected to last forever, however, home builders cannot be sure and must protect their liquidity as average purchase prices decline. Compounding this is that the cost of capital has increased, making financing production more expensive.

As the following illustrates, this has contributed to a decline in US housing starts and a decline in the forecast starts. This is extremely problematic for Ferguson and will inevitably have a material impact on the company's financials in the coming years (54% of revenue from Residential, 32% from Commercial). Ferguson is unlikely to be immediately impacted, as ongoing builds are unlikely to halt. However, as the company runs through the current projects, we expect a slowdown. In the most recent quarter, sales declined (2)% ((6)% decline in Residential), potentially signaling the beginning of a slowdown.

Further, the construction industry is experiencing a shortage of skilled labor in the industry, impacting project timelines and the demand for products. We consider this a lesser issue but nevertheless has impacted the industry at an inopportune time.

Margins

Ferguson has one of the cleanest margin evolutions we have ever seen. Across the historical period, it has seen slow but consistent margin improvement, reaching an EBITDA-M of 11% and a NIM of 6%.

The improvement is driven by scale economies and pricing competitiveness, offset partially in recent years by inflationary pressure. We suspect further improvement is possible but only once Residential conditions improve, which could be 2-3 years from now.

Balance sheet & Cash Flows

Ferguson is conservatively financed, with a ND/EBITDA ratio of 1.3x. This implies a healthy use of leverage, leaving sufficient flexibility for further raises in the future if required.

Cash flows have been incredibly consistent, driven by a strong P&L performance in conjunction with operational excellence, as its CCC has gradually declined.

Distributions to shareholders have been through both buybacks and dividends. Given the recent uptick in payments relative to FCF, we suspect a reduction in buybacks will occur. Nevertheless, distributions are attractive in our view.

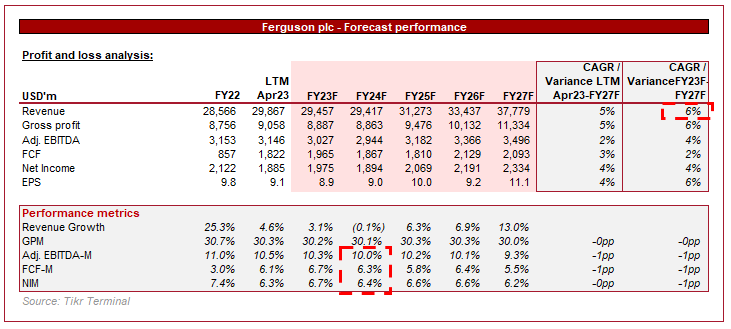

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a marginal decline in FY24F, which implies a difficult year when factoring in the inorganic impact of acquisitions. We believe the impact on the business will be slightly more than this (although analysts are potentially pricing in more acquisitions, which we are not) given the house-building statistics but this looks reasonable, especially given inflation is approaching a sustainable level (albeit slowly).

Margins are expected to deteriorate, an interesting assessment given margins are not materially down. This implies analysts are confident the business has not bottomed, with further downside possible.

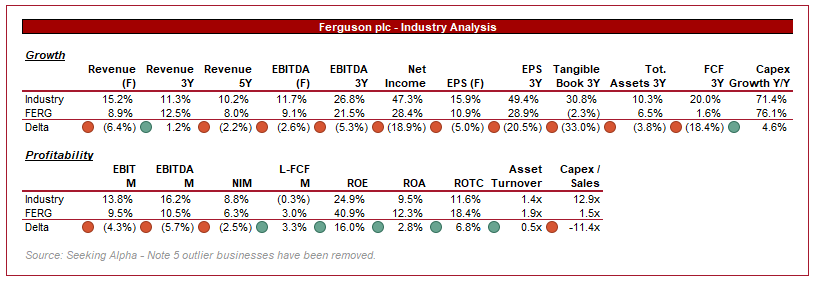

Industry analysis

{kind=link}

Trading Companies and Distributors Stocks (Seeking Alpha)

Presented above is a comparison of Ferguson's growth and profitability to the average of its industry, as defined by Seeking Alpha ( 42 companies).

Ferguson noticeably underperforms on growth metrics, reflecting the slow-moving nature of its specific segment, namely plumbing. We are not overly concerned by the delta given Ferguson is within range.

Profitability is slightly more problematic. Although the company is efficient, its EBITDA-M and NIM lag behind by a large amount. Based on this, we believe Ferguson should trade at a discount to these peers.

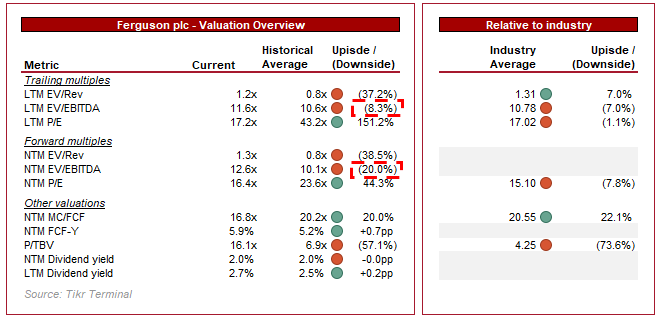

Valuation

{kind=link}

Ferguson is currently trading at 11.6x LTM EBITDA and 12.6x NTM EBITDA. This is a premium to its historical average.

The premium valuation looks incredibly difficult to justify. The company is facing industry headwinds to a degree unseen since the GFC. Further, it has experienced a recent quarterly decline, implying weakness is beginning to set in. Offsetting this against the "average position" is the margin improvement, increased scale, and NYSE listing. These factors would justify the premium in a good year but with what is ahead, we disagree.

Further, Ferguson is trading at a small premium to the industry average chosen. This once again could look reasonable, if a strong argument was made for industry tailwinds specifically impacting Ferguson in an outsized fashion, as well as brand superiority and a resilient business model. Now, however, this premium is unwarranted.

Final thoughts

Ferguson is an attractive business in an attractive industry. We like the brand and its approach to doing business. We are bullish on Ferguson long-term and believe a company of its financial and commercial nature is needed in most portfolios.

As of now, however, we believe the timing is incorrect. The company is facing headwinds that will last well into FY24 in our view and mean price action is unlikely. The margin contraction forecast is a further downside risk we do not have in our thesis either. We suggest caution.

For further details see:

Ferguson: Long-Term Compounder Facing Housing Market Downturn