FERG - Ferguson: Still A Buy After Its 30% Rally

2023-03-09 10:00:00 ET

Summary

- Ferguson ran up 30% since I started to cover the company.

- Earnings came in nicely and the company is printing cash again.

- Besides New residential construction, the company is growing nicely in a tough environment.

- Ferguson fundamentally remains a buy.

Ferguson (FERG), a leading value-added distributor in the construction space, has been on a tear lately. The stock has returned 32% since my initial coverage last October. Let's see what happened since then and if shares are still attractively priced.

Why are distributors a great business?

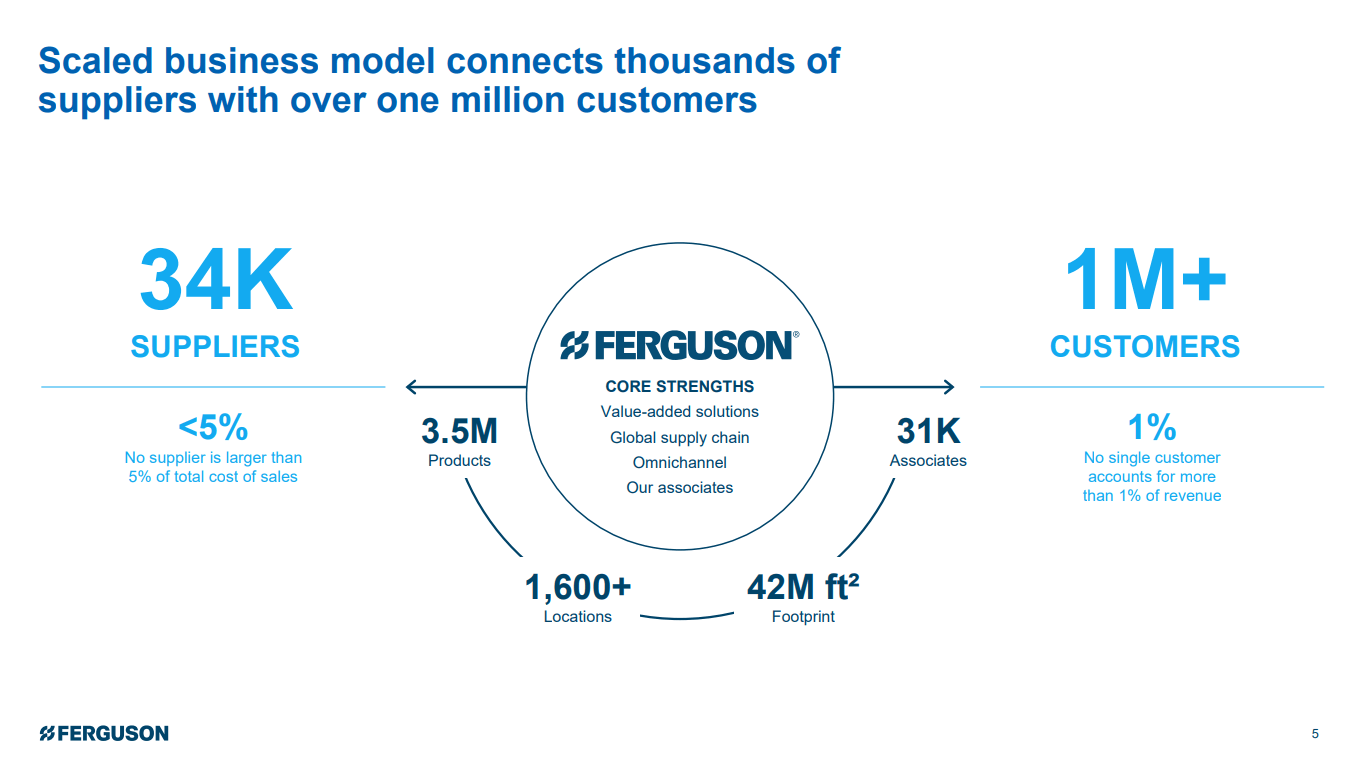

First, let's quickly reiterate why distribution businesses are typically great with large moats. Leading Distributors can enjoy large moats due to network effects. Below we see a graphic from Ferguson that nicely illustrates the point. The company is the middleman between a large number of suppliers (>34,000) and customers (>1 million) with millions of products across vast geographic distances. A well-connected distributor can be an invaluable part of the supply chain by matching buyer and seller and offering value-added services and supply chain solutions. Other great examples are Watsco (WSO), a company I own that offers its customers proprietary marketing software to help them sell more effectively and W.W. Grainger (GWW), which provides inventory management solutions and consulting to its customers .

{kind=link}

Latest earnings beat expectations

Ferguson reported earnings yesterday and beat the bottom line by $150 million while missing EPS estimates by $0.04. While they beat the bottom line, we can still observe a material deceleration in the business; after a 31.8% sales increase in 2022, growth slowed to 4.9%. As a business in the construction sector, the looming recession has kept expectations down for a while. This quarter's expectations were flat, so 4.9% revenue growth is positive. Operating profits saw a similar story. With a dramatic rise (68% in 2022), we are now down to a slight decrease of 1%. The slowdown is most notable in residential (54% of revenue), which decelerated from 15% to 1% growth sequentially. Non-residential held up better while still decelerating meaningfully from 20% to 11% sequentially. Below I highlighted a comment from the CEO: Most of the slowdown is in new construction, while repair and maintenance remained relatively strong (21% to 12% deceleration).

From an end market perspective, clearly we are seeing pressure on the new residential construction side, especially on the single family side, a little bit less so on multifamily. Did it happen a bit faster than expected? Maybe a touch, but if you look at the repair and maintenance side of the world, especially as we discussed in our first quarter call, and we were very pleased to see that that high-end remodel residential demand picture remains fairly solid.

Kevin Murphy, CEO Ferguson PLC Q2 2023

The cash is flowing again

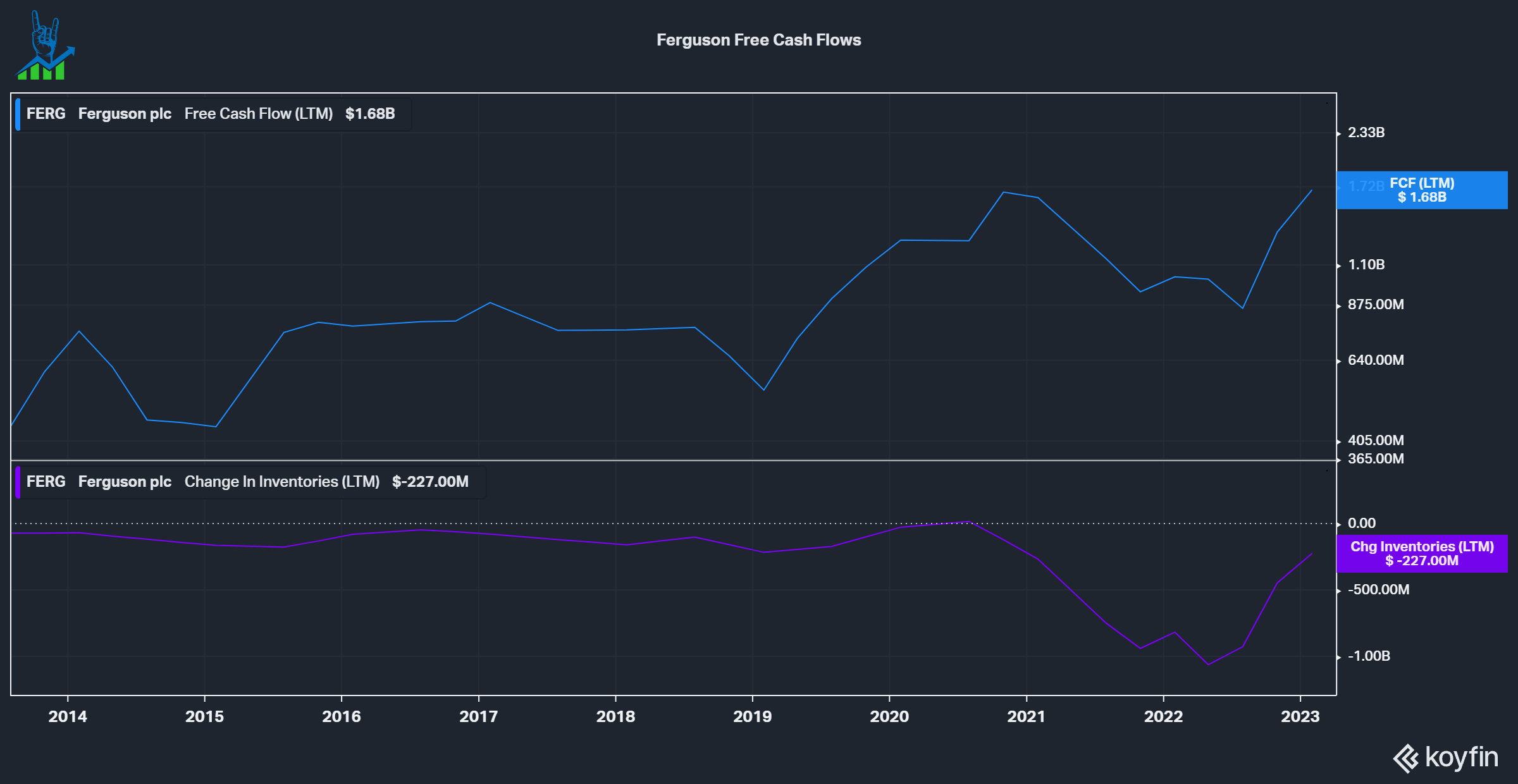

After Ferguson struggled with Free Cash Flows due to inventory build-up and working capital impacts, the company is finally reporting strong free cash flows again. In the first half of the year, the company produced $936 million in free cash flow, up from $109 million in H1 2022. This is great to see; after all, Ferguson is a business that returns a lot of money to shareholders and invests in CapEx and acquisitions.

{kind=link}

Capital allocation

Ferguson closed four acquisitions in the HVAC, Waterworks and industrial customer groups in the last quarter. These acquisitions bring in annualized revenues of around $300 million or 1% of annual revenues. The company has historically (5 years) grown by 2.4% a year through acquisitions, so this was a solid above-average quarter on that front.

Ferguson also increased its dividend by 9% to a quarterly dividend of $0.75 or a 2.2% yield and repurchased $0.6 billion of shares in the first half of 2023.

Lastly, on capital allocation, the company increased its guidance for Capital Expenditures by $50 million from $350-400 to $400-450 million for FY 2023, driven by the timing of real estate purchases for their market distribution center strategy. This means this is not additional CapEx but a timing issue.

Guidance is mostly unchanged

The FY 2023 guidance remains primarily unchanged. Besides the abovementioned CapEx increase, the company also expects an additional $15 million in interest expenses due to slightly increased debt levels. Besides that, Ferguson continues to expect to outgrow the market (low-single-digit decline expected) by growing low-single-digits due to market share gains and acquisitions.

Valuation

Like in my first article , I'll value Ferguson based on an inverse DCF model. Since then, the cash flows have improved significantly due to the significant headwinds from inventory build-up leveling off. Based on the last decade, I assumed a 1.7% annual reduction in outstanding shares. We reach a 5% Free Cash Flow growth expectation with these inputs. Ferguson expects to grow with low-single-digits this year compared to a declining end market and a 10% growth rate throughout the cycle. Ferguson remains attractive at these levels unless we see a deep recession. I presently do not own shares in Ferguson because I prefer the focused approach of Watsco on the HVAC end market.

Ferguson Inverse DCF (Authors Model)

For further details see:

Ferguson: Still A Buy After Its 30% Rally