FERG - Ferguson: Undervalued But Not The Right Time To Buy

2023-10-13 06:11:06 ET

Summary

- Ferguson posted Q4 FY23 and FY23 results, with a decline in sales but increased profitability.

- The company performed well in adverse market conditions, but macroeconomic headwinds make it a risky investment.

- Technical analysis suggests the stock is nearing important resistance levels, making it an unfavorable time to buy.

Ferguson (FERG) distributes heating products in North America. The company was expecting slow revenue growth in FY23, and that was the case. However, the acquisitions proved beneficial, and I mentioned in the previous report that the price action indicated a trend reversal. Thus, the thesis was carried out effectively. I am writing this follow-up because I think the current market conditions aren't favorable. The stock price is nearing the important resistance, and I believe the stock has mostly run its course. It recently posted Q4 FY23 and FY23 results. I will analyze its FY23 results in this report. I think it is a great company performing well in adverse market conditions. But I don't think it is a great time to buy it due to macroeconomic headwinds. Hence, I assign a hold rating.

Financial Analysis

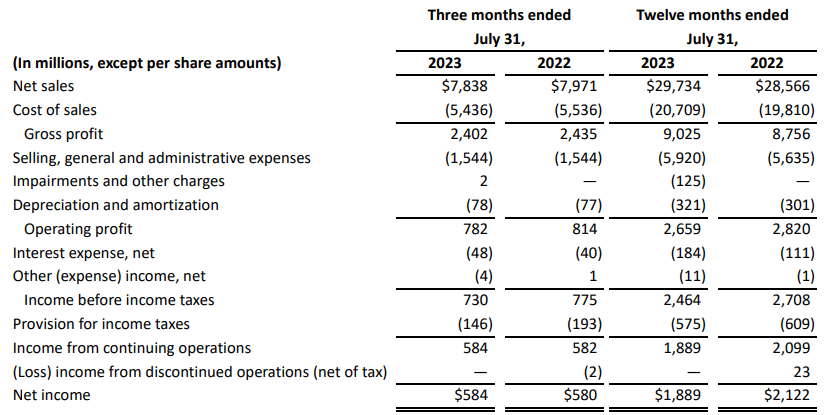

It recently posted its Q4 FY23 and FY23 results . The net sales for Q4 FY23 were $7.8 billion, a decline of 1.6% compared to Q4 FY22. Weakness in the residential market was the major reason behind the sales decline. Both Canada and the U.S. saw a weakness in the residential market, due to which sales in Canada and the U.S. declined by 5.1% and 1.5% in Q4 FY23 compared to Q4 FY22. Despite the slight decline in sales, its net income increased slightly. Pricing discipline helped them to achieve better profitability.

{kind=link}

The net sales for FY23 were $29.7 billion, a rise of 4% compared to FY22. A strong demand in the non-residential market in the U.S. and contribution from the acquisitions were the major reasons behind the sales growth. The net income declined 11% in FY23 compared to FY22. Higher interest expenses affected its profitability. Despite a decline in quarterly sales and low sales growth in FY23, I believe they performed extremely well. I am saying this because the performance of its residential and non-residential markets is dependent upon certain macroeconomic trends and can be affected by certain macroeconomic factors like rising interest and mortgage rates, and there is no need to say about the rising rate. The mortgage rates were quite high in FY23, which affected the construction market. But despite the adverse market conditions, the company was able to post positive revenue growth, which is appreciable. Talking about FY24, I expect their revenue growth to be stagnant, and the management has also provided revenue guidance for FY24. They expect FY24 revenue to be flat. I expect stagnant revenue growth because of the adverse market conditions. The current mortgage rate is sky-high, and the interest rate is also rising. So, there are headwinds that will hamper the company's revenue growth in FY24. Now, talking about the free cash flow, it increased significantly this year. The free cash flow increased by $1.4 billion to $2.3 billion in FY23 compared to FY22, and they have used most of the cash in acquisitions, share repurchases, and dividends. Expanding the business through acquiring business is one of their major strategies, and they acquired eight businesses in FY23 and purchased shares worth $908 million in FY23. They also increased their dividend payment by 9% in FY23 compared to FY22. I think they should also focus on reducing the debt as the increased interest expense affects the profitability to some extent. Although its long-term debt by the end of July 2023 was $3.7 billion, it was $3.6 billion in July 2022. So, the debt hasn't increased much, and looking at the cash flow, I think they are in a comfortable position.

Technical Analysis

{kind=link}

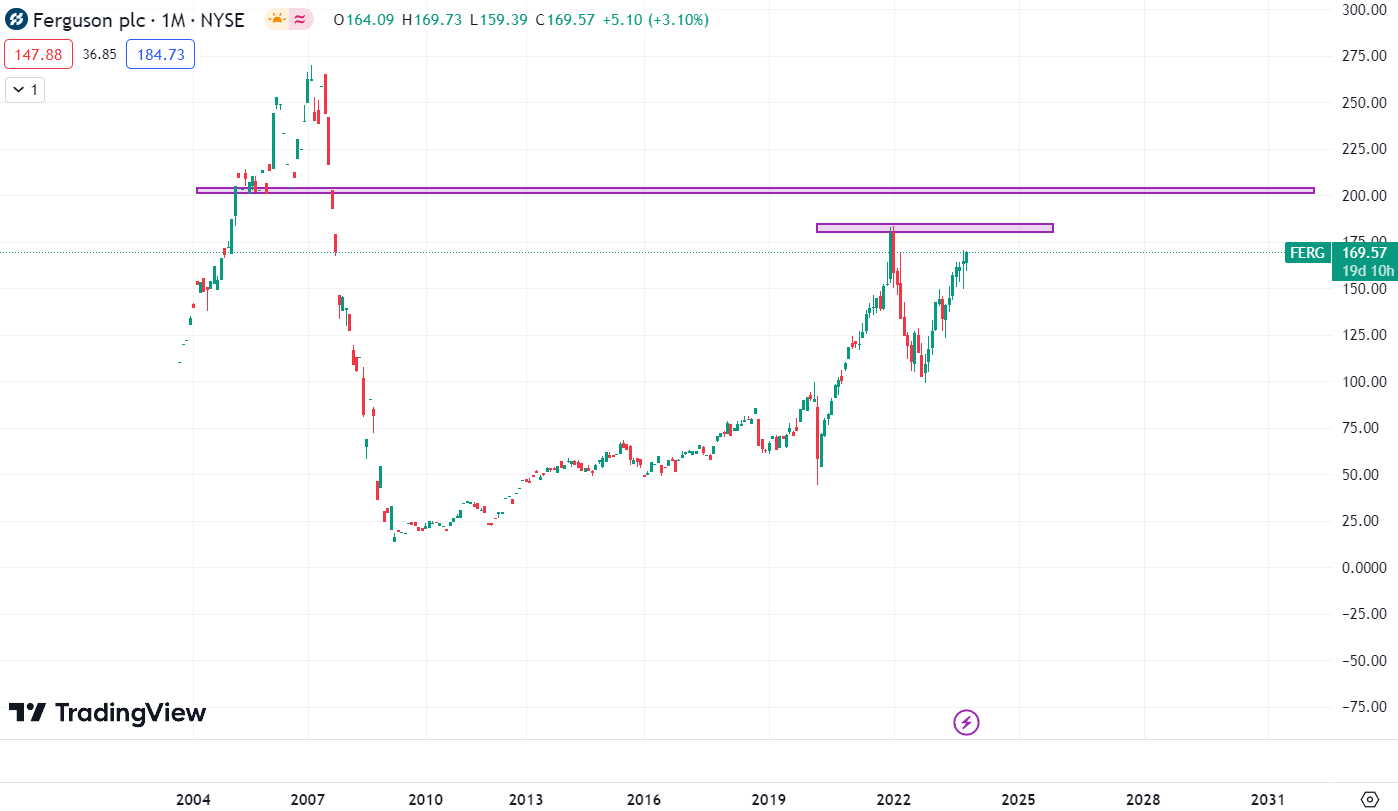

It is trading at the $169.5 level. The stock has given a strong upward rally in the last five months. It has risen more than 30%, and the stock refuses to stop. But generally, whenever there is a one-sided momentum in a stock, it is most likely that the stock will see a correction soon, and in this case, the stock price is nearing an important resistance of $180. The last time the stock touched the $180 level, it corrected more than 40%, so there is a high chance that the stock might correct after touching the $180 level. Suppose even if the stock breaks out of the $180 level, there is another resistance zone at $200. So, there are a couple of resistance zones ahead of the stock. Hence, creating a new position might not be a wise decision because, in my view, I don't see a strong upside from the current level. Hence, I assign a hold rating.

Should One Invest In FERG?

Now, talking about FERG's valuation . FERG has a P/E [TTM] ratio of 18.59x, which is lower than the sector median of 19.44x, and has a Price / Sales [ TTM] ratio of 1.18x compared to the sector median of 1.35x. Their ability to perform well in adverse market conditions makes them undervalued, and they have shown that in FY23, the market conditions weren't favorable. However, they still managed to grow the revenues, which might be why, despite posting low revenue growth, its stock price has increased in the past few months. But despite being undervalued, I don't think this is the right time to get into the stock as their future outlook is not so great, the market conditions aren't favorable, and technically, the stock is nearing a crucial level. Hence, I think one should wait for the market conditions to get normal and wait for the correction in the stock price as it has been continuously moving up in the last few months; hence, after looking at all the factors, I assign a hold rating.

Risk

They owed $3.8 billion in total debt as of July 31, 2023. They might take on a significant amount of additional debt in the future, especially about acquisitions that are still a key component of their plan, some of which might be backed by all or most of their assets. Their overall level of debt may occasionally have a negative impact on their strategy. For example, it may force them to allocate a portion of their cash flow to debt repayment, which would reduce the amount of money they have available for reinvesting in the company; it may prevent them from obtaining the financing needed to pursue acquisition opportunities; it may limit their flexibility in anticipating or responding to changes in their industry and business; it may restrict their ability to buy, redeem, or retire their common shares; and it may put them at a competitive disadvantage in comparison to their less indebted competitors. Furthermore, because some of their borrowings have variable interest rates, their debt exposes them to the danger of rising interest rates.

Bottom Line

FERG posted strong annual results. Although the sales growth wasn't significant, looking at the market conditions, it was impressive. But the future outlook isn't great, and the market conditions aren't favorable. In addition, I think the stock is due for a correction. Hence, I assign a hold rating.

For further details see:

Ferguson: Undervalued But Not The Right Time To Buy