RACE - Ferrari Is A Long-Term Holding Despite Incumbent Risks

2023-05-14 03:45:04 ET

Summary

- Ferrari has the highest operating margin in the auto industry, but this metric has plateaued.

- Revenue and net profit are analysed in Ferrari's official financial statements and reveal stable growth, although slowed, due to the stagnating operating margin metric.

- Ferrari will likely still be a long-term growth vehicle for investors due to its acclimation to emerging economies such as China and the Middle East, and electric vehicle demand.

- Investors have to be wary of an overvalued company that may see a reversion to the mean in the short-to-medium term, but should expect continued above-index returns over the long haul.

- Competition with Tesla and other EV manufacturers, a small market of niche consumers and no strategy for non-luxury products are other risks worth considering.

Editor's note: Seeking Alpha is proud to welcome Oliver Rodzianko as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Ferrari ( RACE ) has the highest operating margin metric in the auto industry, resting at around 24% from 2019 onwards. This thesis will outline the recent plateau of margin growth, but will also develop an argument as to why the stock is still favourable to purchase due to the already established exceptionally high rate in relation to continued revenue growth and expansion into emerging markets in the years to come.

The Highest Operating Margin in the Auto Industry

In comparison to LVMH Moët Hennessy Louis Vuitton (MC.PA) ( LVMHF , LVMUY ), which has a market cap of around EUR 440 billion, Ferrari is relatively small, which is to be expected when analysed against a conglomerate. However, its market cap of around EUR 49 billion is supported by a 24% operating margin, which almost matches LVMH’s 26% .

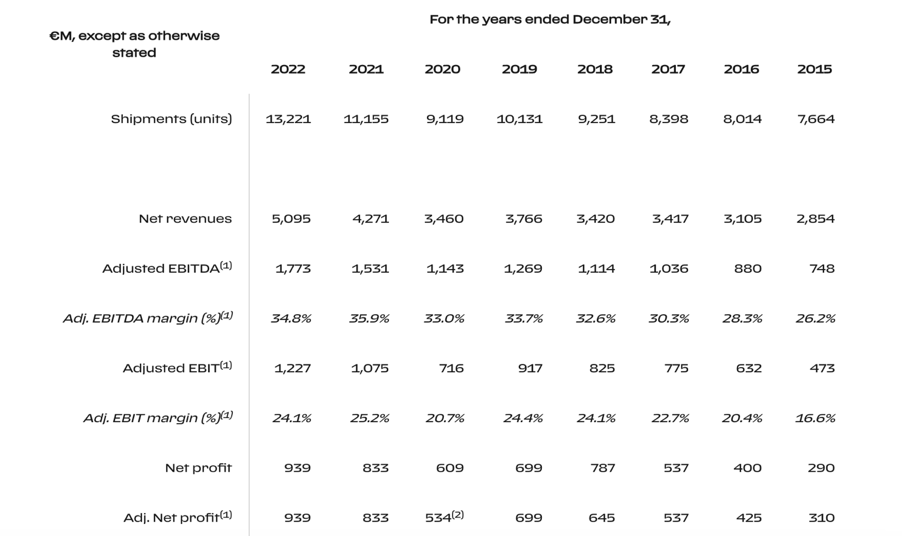

By analysing the 2021 table below, you can see that in the auto industry, Ferrari is far down the food chain in terms of total operating income. However, when you compare the leader in income Toyota ( TM ) with Ferrari on net profit margin, you notice an 11% difference. Toyota’s was registered around 7% in 2022 while Ferrari’s was 18%. Between 2015–2020, the average net profit margin for major automotive companies worldwide was only around 7.5%

{kind=link}

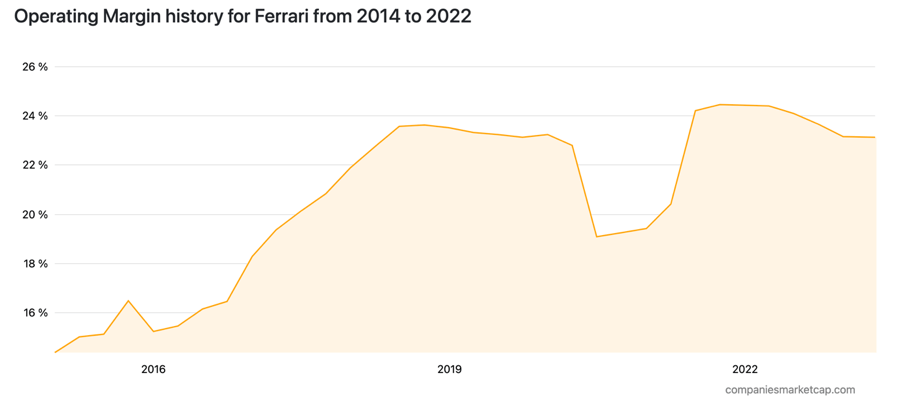

The main cause for concern here should be whether the stock can continue to grow its profit margin over the long term, or whether the figure will begin to plateau. However, with increasing revenues even if the profit margin is only maintained, it is still a very attractive business with growth potential in terms of bottom-line income. Look at the graph below, and you will notice the beginning of a potential long-term plateau in operating margin around 2019:

{kind=link}

Fundamental Components & Valuation of Ferrari

Ferrari's fundamental business has several appealing elements for investors, which are evident in the company's positive revenue growth. However, the revenue growth appears to be outpacing the operating margin, indicating a potential short-term decline in the stock price as the market adjusts to the new equilibrium of fundamentals. The reversion to the mean in terms of valuation could slow down the overall stock price appreciation.

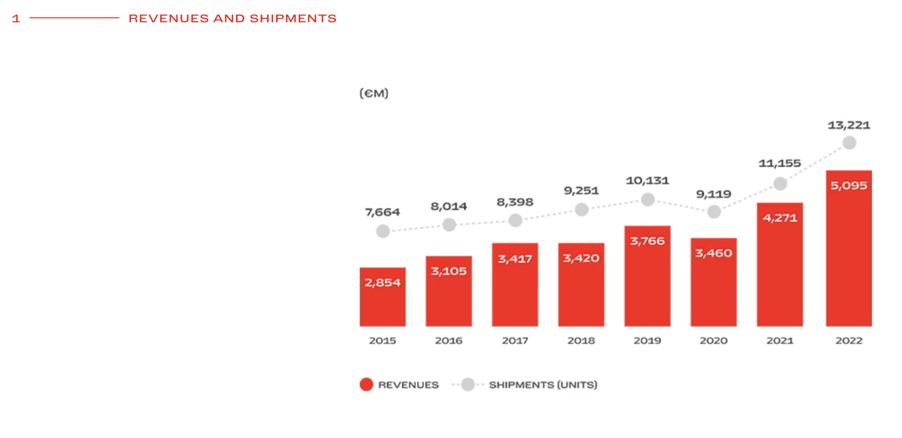

Ferrari’s revenue is steadily increasing, from EUR 2.9 billion in 2015 to EUR 5.1 billion in 2022:

{kind=link}

Ferrari’s growth is still ongoing:

{kind=link}

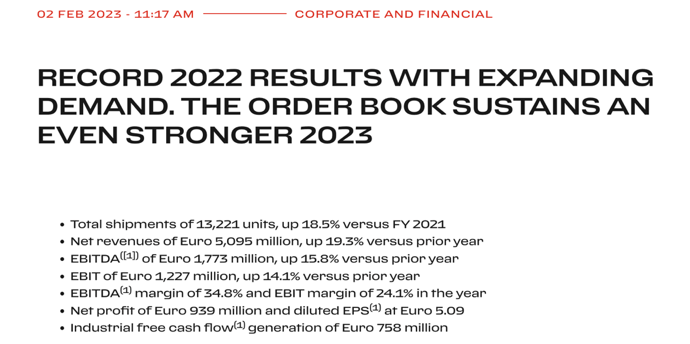

If we analyse the trajectory of the EBIT margin (%) in the following graph, we notice that since 2015 the company has seen a 7.5% increase in the metric, but since 2018, the metric has increased by 0%, or 1.1% if we take into consideration 2021 as the peak metric registered to date. This is cause for concern, but if we look at net revenues from 2018 onwards we have a EUR 1.675 billion increase. Net profit has increased by EUR 152 million since 2018, also favourable to the long-term appreciation of the stock price. However, this is not like 2015 to 2018, which saw a EUR 497 million rise, due in large part to the 7.5% increase in EBIT margin.

{kind=link}

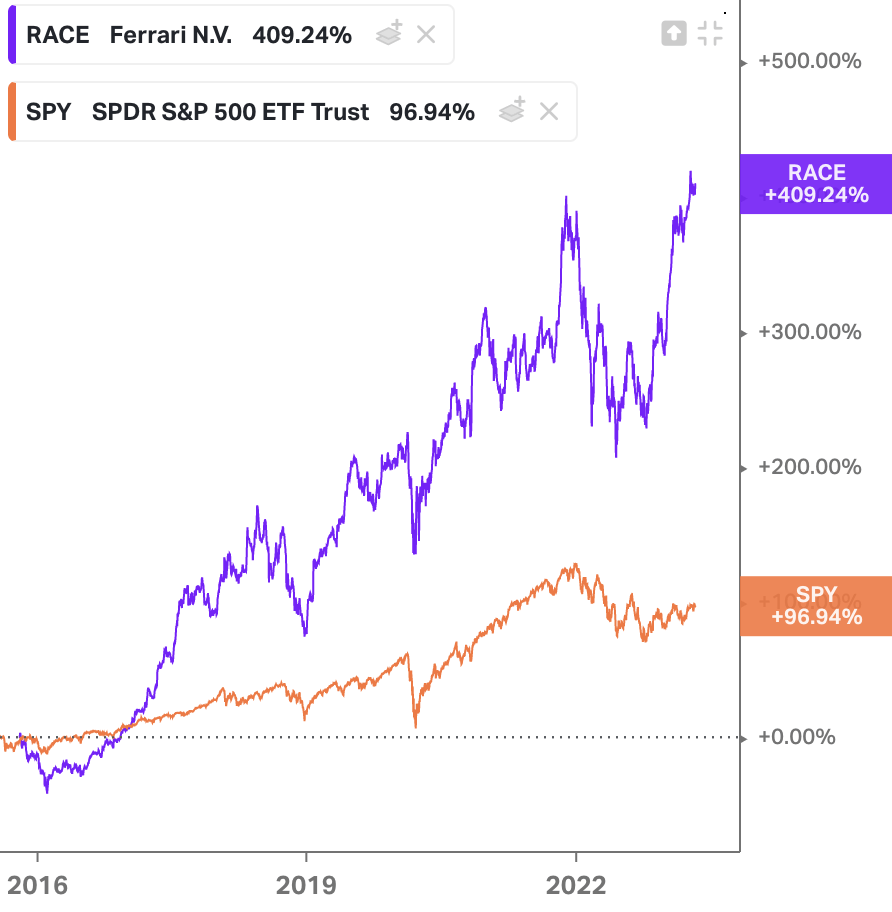

Ferrari has shown remarkable stock price appreciation since its separation from its former parent company, Fiat Chrysler (now Stellantis) (STLA). From January 2016, the company's stock price has increased by an impressive 409.24% at the time of this writing, surpassing the S&P 500's growth rate significantly. The company's P/E ratio is currently at 49.25, reflecting the market's high expectations for future growth and earnings. The premium valuation suggests that investors believe in the company's long-term potential and its ability to maintain its competitive edge in the luxury car market, but investors have to be wary of an overvalued company that has not yet registered the effects of a plateauing operating margin which will inevitably affect net income growth. However, as the company transitions into electric and hybrid vehicles and taps emerging markets, we may see an opportunity for increased revenue growth that will balance a stagnating margin metric.

{kind=link}

Ferrari is a strong investment opportunity, but using discounted cash flow ('DCF') analysis to value the company may not be the best approach. As a forecasting method, DCF requires making assumptions about future cash flows, discount rates, and other variables that can be challenging to predict accurately. Investors such as Warren Buffett and Charlie Munger also share this view , highlighting the subjectivity and limitations of DCF. Instead, it is essential to approach any valuation with caution and recognise that it is just one of many factors to consider when evaluating a company's worth. Evaluating Ferrari's long-term prospects and growth potential, including its business positioning in the market, product lineup, distribution network, brand strength, and competitive landscape, is more valuable in my opinion than relying on DCF. By using predictive measures, investors can evaluate whether a high valuation in terms of stock price can be maintained over the long term based on the company's underlying fundamentals. Despite the challenges of valuing Ferrari quantitatively, the company's strong brand, reputation, history of generating strong cash flows, and ability to adapt to the changing market landscape make it an attractive long-term investment opportunity.

Ferrari’s Supply Strategy & Electric Vehicle Transition

Although Ferrari is producing more cars as demand increases, they are still retaining a waiting period, often over 12 months. The reason for this is quality control and also a luxury supply model which purposely limits production to increase product price with demand. What the company have to be careful of now is that their supply chain can handle increased production that does not negatively impact the quality of the vehicles. Each car is personally crafted for the customer and in emerging countries like China and the Middle East customers are demanding a lesser waiting time than the 12-month standard for Western buyers.

Understanding the risk of operating margin plateau alongside the positive factors of emerging market demand and continually increasing revenues is about setting realistic expectations for the stock moving forward. There is a risk that the stock will not see exponential growth at the level seen previously if margins are only maintained, especially considering the investment into electric and hybrid models currently adopted by the company.

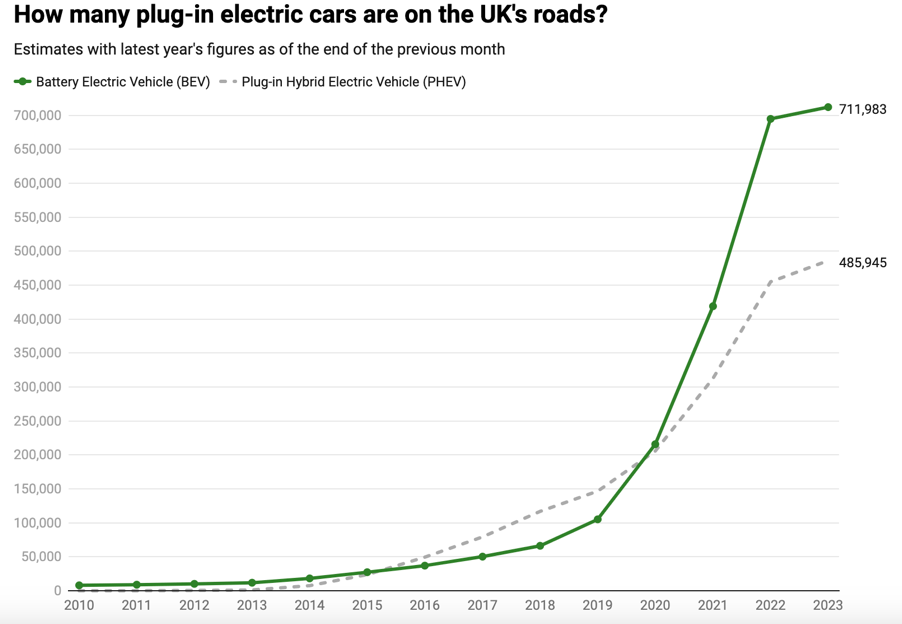

Ferrari is positioning itself to become a 40% electric vehicle company by 2040, with 40% of the rest of the car portfolio being hybrid and only 20% running pure combustion engines. Investors can expect a heightened risk profile for the stock as it transitions, but also expect growing revenue from a market previously untapped. The idea that consumers will not be favourable to the electric and hybrid models is unsupported by RAC’s representation of the staggering increase in electric and hybrid vehicles on UK roads since 2010:

{kind=link}

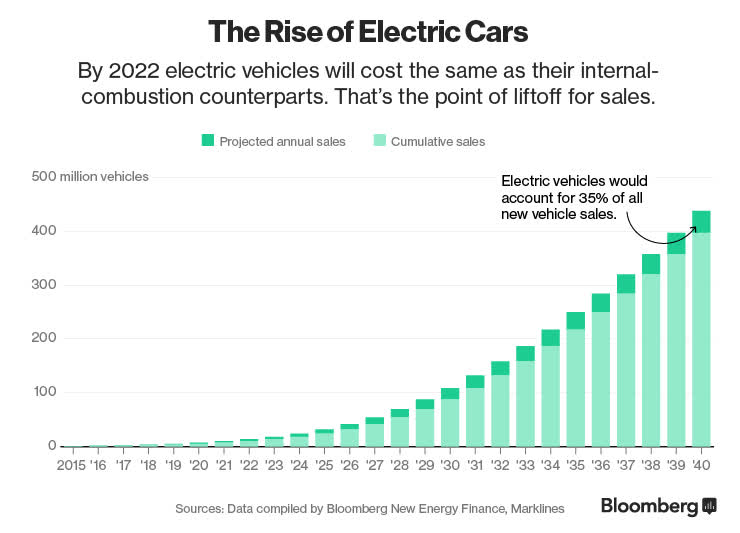

Also, note the rise in electric vehicle sales presented by Bloomberg:

{kind=link}

Further Notable Risks

We've outlined a risk here of potential overvaluation, which may limit growth or stagnate stock appreciation in the short term, but there are other factors to be concerned with that are likely to affect revenue growth that Ferrari needs to be careful of.

According to Cox Automotive , investors should be aware that Tesla ( TSLA ) has maintained its dominance in the EV market, with a first-quarter market share of 62.4% in the U.S. out of a total of 258,885 battery electric vehicles sold. The electric vehicle market is already full of established names ; while the luxury electric vehicle market is less saturated, there is still fierce competition from the likes of Porsche (PAH3.DE) (POAHY), Jaguar (TTM), and of course, Tesla. It remains to be seen whether Ferrari can effectively compete in this space.

Based on the information available, Ferrari does not appear to be actively seeking to appeal to less wealthy customers. Ferrari is known for its high-end luxury sports cars and has a long-standing reputation for exclusivity and high price points. While the company is now developing electric vehicles, it is still expected that they will be aimed at the luxury market rather than a mass-market audience. Ferrari has stated that their goal is to maintain the exclusivity and prestige of their brand while also transitioning to electric vehicles. The Wall Street Journal article on Ferrari's plan to enter the EV market is an excellent exposition of Ferrari's strategy moving forward, which does not include a non-luxury product. This could concern the investor looking for an increased market cap, but it would be a mistake to rebrand an already established and successful business for the sake of misguided and unrealistic growth ambitions. Moving into the EV market as a luxury player seems to be the forward-focused and competitive move needed to keep Ferrari flourishing and dominant in the high-end auto industry in the next generation of vehicles.

Conclusion

Ferrari is a highly profitable automotive stock that has demonstrated strong fundamental growth. The company has a reputation for producing high-end luxury sports cars, which positions it well in a niche market of luxury consumers who are willing to pay a premium for its products. Moreover, the company is expanding its market reach to emerging economies like China and the Middle East, which presents significant opportunities. Additionally, the increasing demand for electric vehicles provides the potential for further growth, and Ferrari is well-positioned to take advantage of this trend. Despite the challenges presented by the shift towards electric vehicles, potential risks of overvaluation and stagnating metrics, Ferrari's already exceptional operating margin and strong fundamentals make it an excellent buy-or-hold investment vehicle for long-term capital gains.

For further details see:

Ferrari Is A Long-Term Holding, Despite Incumbent Risks