FGPR - Ferrellgas Partners: Still A Long Shot For Huge Upside

Summary

- FGPR came a step closer to avoiding massive dilution for its publicly-traded units.

- Going forward, it will be challenged to generate enough cash flow to avoid dilution.

- However, if it succeeds, the units could offer 700% upside from current levels.

Since we last covered Ferrellgas Partners, L.P. ( FGPR ), the company has paid another $50 million toward repaying its Class B units. To date, it has paid $100 million of its $357 million original Class B balance. FGPR currently has to pay $257 million to Class B unitholders before March 30, 2026, to avoid significant dilution to its publicly-traded Class A units that would occur from the conversion of its Class B units to Class A units.

Fiscal First Quarter Results: Good Financially, Mediocre Operationally

The investment case for FGPR's Class A units revolves around the company's ability to maintain stable operations and generate enough cash flow to meet its Class B obligation while remaining in compliance with its financial covenants.

FGPR's first quarter financial results for the three months ending October 31, 2022 were an improvement over previous years' results. Most importantly, for the Class A units, the results were good enough to keep FGPR comfortably in compliance with all its debt and preferred unit covenants.

{kind=link}

Operating results during the quarter were not as strong. They reflect FGPR's pivot away from wholesale propane sales and toward retail in an overall market that has shrunk in the low-single-digit percent over the past few years.

{kind=link}

FGPR's Cash Flow Challenge

FGPR will be challenged to generate enough cash to satisfy its $257 million Class B obligation over the next few years. The table below shows that the primary source for its $50 million Class B payments in Q1 2022 and Q4 2022 was the cash it had on hand after it emerged from bankruptcy in April 2021. Notice the cash drawdowns that occurred in those quarters in the top row of the following table. The $50 million redemption payments are highlighted in the Total Distributions row.

{kind=link}

By the end of October, FGPR had only $55.3 million on hand, $15 million of which it generated from drawing on its revolving credit facility and from asset sales.

To put the magnitude of FGPR's cash flow challenge in perspective, consider that over the past twelve months, the company only generated $11 million of free cash flow before having to pay $63 million of preferred distributions. And that was in a good year, where adjusted EBITDA was 7% higher than fiscal 2021 and more than 20% higher than fiscal years 2018-2020.

FGPR must maintain significant liquidity to fund its $16 million of quarterly preferred distributions in its seasonally slower quarters during the summer. It also needs significant cash on hand to fund broker margin deposits, as was the case in the first quarter. We don't see its cash balance dropping much below $50 million, so it can maintain a sufficient buffer of liquidity.

FGPR's financial flexibility is further limited by the indentures governing its senior notes, credit facility, and preferred units. However, as things stand today, it should have little trouble meeting its 2.5 times EBITDA interest coverage ratio, as well as the 4.75 times maximum leverage ratio stipulated by its credit facility.

Looking several years out, an additional challenge comes from FGPR's $650 million debt maturity in 2026. However, as long as the company can keep its leverage ratio around today's 4.0 times EBITDA, it should have little trouble refinancing, though potentially at a higher rate than the current 5.375% interest rate it pays on its senior notes.

FGPR's cash flow challenges are the main reason why its Class A units trade at a low 6 times EV/EBITDA multiple. The units are pricing in the massive dilution that would occur if the company fails to generate $257 million by 2026 to meet its Class B obligation. The units are also trading low enough to make it prohibitively expensive to issue Class A units for the purpose of paying the Class B obligation.

Valuation

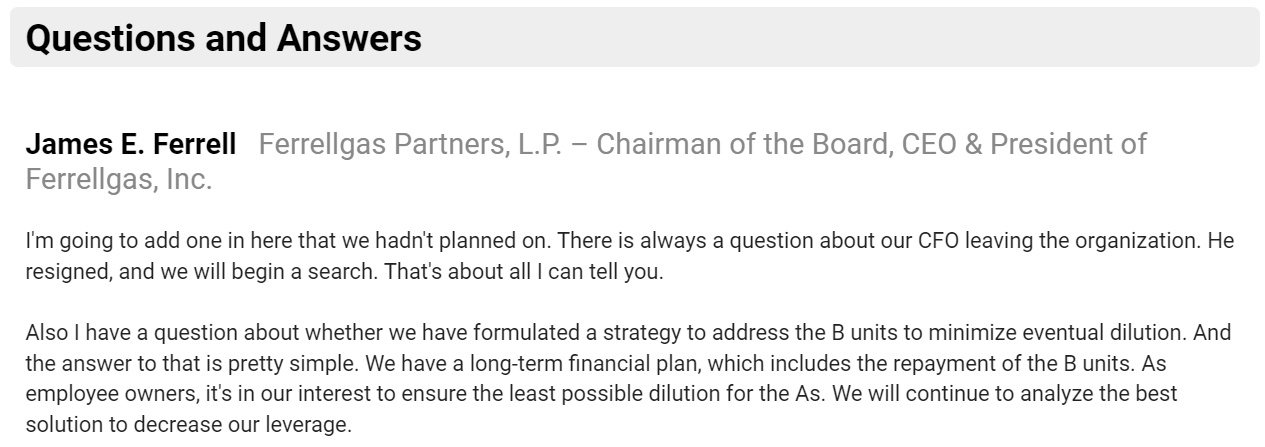

Clearly, everything has to go right for FGPR to pay its remaining Class B obligation. Unfortunately, management has failed to discuss the matter with public Class A unitholders on its quarterly earnings conference calls. Management's only public comments to date on the Class B unit situation were made on its December 2021 earnings conference call. The excerpt below demonstrates how opaque management is toward public unitholders.

{kind=link}

Source: BamSEC, Ferrellgas Partners, L.P. Earnings Conference Call Transcript, Dec. 17, 2021 .

Still, management is no doubt motivated to repay the Class B units. FGPR's Chairman and CEO, James Ferrell, and the entities he controls own 28.1% of Class A units, while public unitholders own 71.7% of Class A units.

Another glimmer of light comes from insider purchases of Class A units. Carney Hawks, the FGPR board member who was elected by the Class B unitholders during bankruptcy proceedings, purchased 16,011 units at $9.92 per unit on October 4, 2022 for $158,829. Before this purchase, he had purchased 28,989 units at $16.32 per unit in June 2021 for $473,204. These purchases appear to be a vote of confidence in management's ability to disastrous dilution.

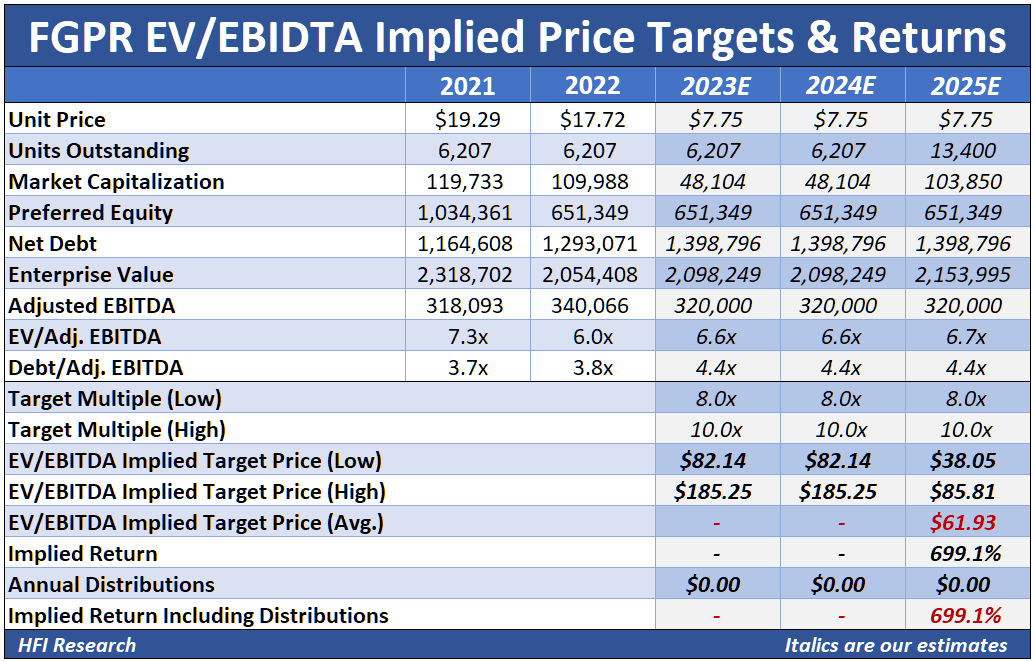

Our valuation assumes that FGPR's adjusted EBITDA runs at $320 million through 2026 while its debt balance remains unchanged. It assumes a conversion ratio of 5-to-1 for the Class B units and also assumes FGPR issues an additional 2 million Class A units in order to facilitate Class B payments. Using these assumptions, our valuation implies FGPR units have nearly 700% upside if the company can resolve its Class B obligation before 2026.

{kind=link}

FGPR would have an easier time meeting its Class B obligation if it could sustain the $340 million of adjusted EBITDA generated in fiscal year 2022. Doing so would allow it to draw $200 million on its credit facility to fund Class B payments, assuming its debt balance stays flat at current levels. However, such a historically high adjusted EBITDA and flat debt balance are two assumptions we're not comfortable making given the volatility inherent in FGPR's business.

Conclusion

While the situation remains precarious for FGPR's Class A units, we continue to see a low probability of a high return several years out. Until the company makes significant progress ensuring the safety of its Class A units, FGPR's unit price is likely to languish. After all, its units have attributes that will all but ensure they remain neglected. For one, the company is an MLP, so its equity is out of favor out of the gate. But consider further that FGPR emerged from bankruptcy in early 2021, its units have a small market cap of $270 million, and they trade on the OTC Pink Market with virtually no analyst coverage. If FGPR's fortunes turned for the better, it could take a while for the market to appreciate the upside potential of its Class A units.

For the time being, we maintain our "Sell" rating on FGPR equity because the prospects for restating the Class A distribution are virtually nil, while the units continue to possess high risk of permanent capital loss. But we'll continue to monitor developments. If the huge upside becomes a more likely prospect, we would flip bullish and change our rating accordingly.

For further details see:

Ferrellgas Partners: Still A Long Shot For Huge Upside