GSM - Ferroglobe: Buybacks Expected Amid Short Term Uncertainty

2024-01-08 19:37:53 ET

Summary

- Ferroglobe redeemed $150m in senior notes in the summer, lowering their Net Debt / LTM EBITDA to 0.45x.

- Based on the assumptions below, shares could trade 107% higher than the current market price a few years out.

- Management believes the silicon market has bottomed and expects demand to pick up in the second half of 2024.

Ferroglobe ( GSM ) is a leading global silicon manufacturer currently valued at $1.17bn with an EV of $1.33bn. While the silicon manufacturing sector is highly cyclical aligned with supply/demand dynamics and overall GDP growth, GSM is a deleveraged cost efficient silicon producer. Below I argue why GSM offers investors an interesting opportunity after 2 years of declining silicon prices.

Silicon Market Dynamics

Silicon metal and silicon based alloys are important metal additives for several sectors. The Silicon Metal Unit produces silicon for aluminium, chemical and polysilicon manufacturing. The smaller silicon alloy and manganese units supplies steel/aluminium manufacturers. Overall these serve a diverse range of end markets from semiconductors to construction.

Q3 volume and EBITDA:

Silicon Metal: Volume 57kt and $80m adj. EBITDA

Silicon Alloys: Volume 46kt and $25.3m adj EBITDA

Manganese: Volume 56k and $11m adj. EBITDA

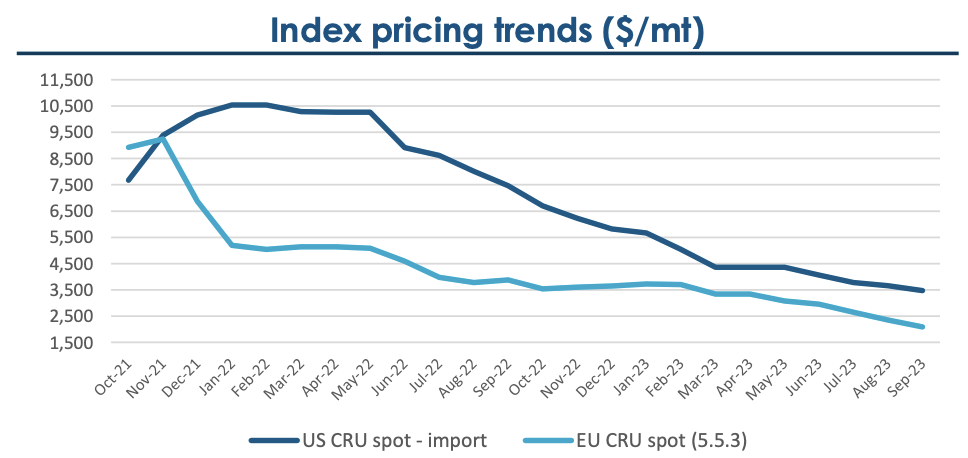

This volume is slightly lower than Q3 2022 however, because so much cost has been pulled out of the business the fall in silicon prices in 2023 hasn't led to negative EBIT or net income like the pre-covid days. Plus Q3 numbers were supported by lower coal prices (page 5).

{kind=link}

Silicon metal accounts for most of GSM's profitability and represents the biggest growth opportunity due to increased demand for US Solar build out in the coming years. Today solar end markets accounts for roughly 20% of the silicon metal unit volume. GSM estimate solar growth of 21% annually until 2032 . Furthermore the SEIA expects solar capacity in the United States to reach 377GW by 2028 vs the 160GW capacity today. More generally Straits Research estimate the global silicon market will reach $20bn by 2030.

In the EU and US, GSM is a market leader due to their integrated manufacturing capabilities, which includes quality quartz supply. Barriers to entry are high due to significant initial CapEx requirements (few hundred million for electric arc furnace) and personnel specialisation. Furthermore producing molten silicon is highly energy intensive making up the majority of process plant costs.

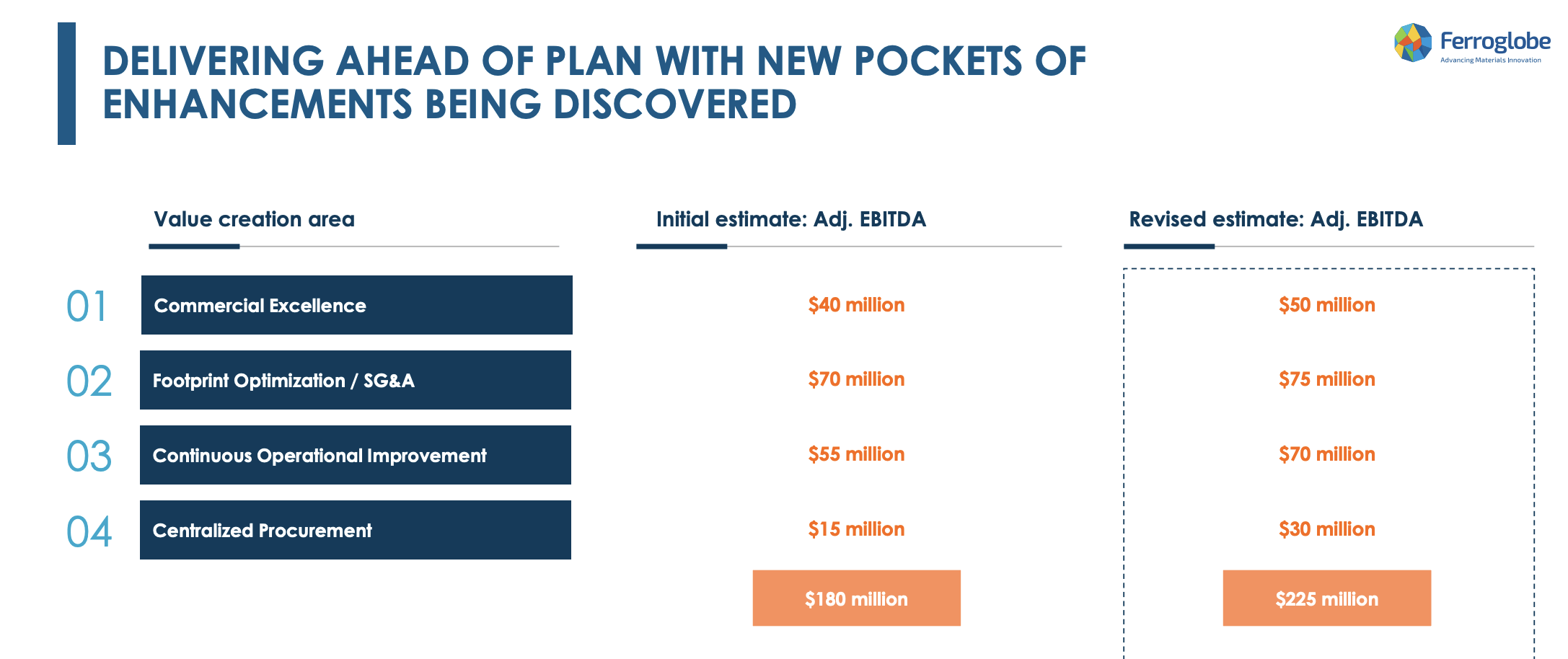

GSM was formed in 2015 via a merger between FerroAtlàntica and Globe Specialty Metal in which synergies never materialised. A new CEO was appointed in 2020 which has worked out well looking at results. Last year management revised several cost efficiency estimates for 2023 ($200m+ in cost savings), these are now being delivered.

Ferroglobe Investor Presentation

{kind=link}

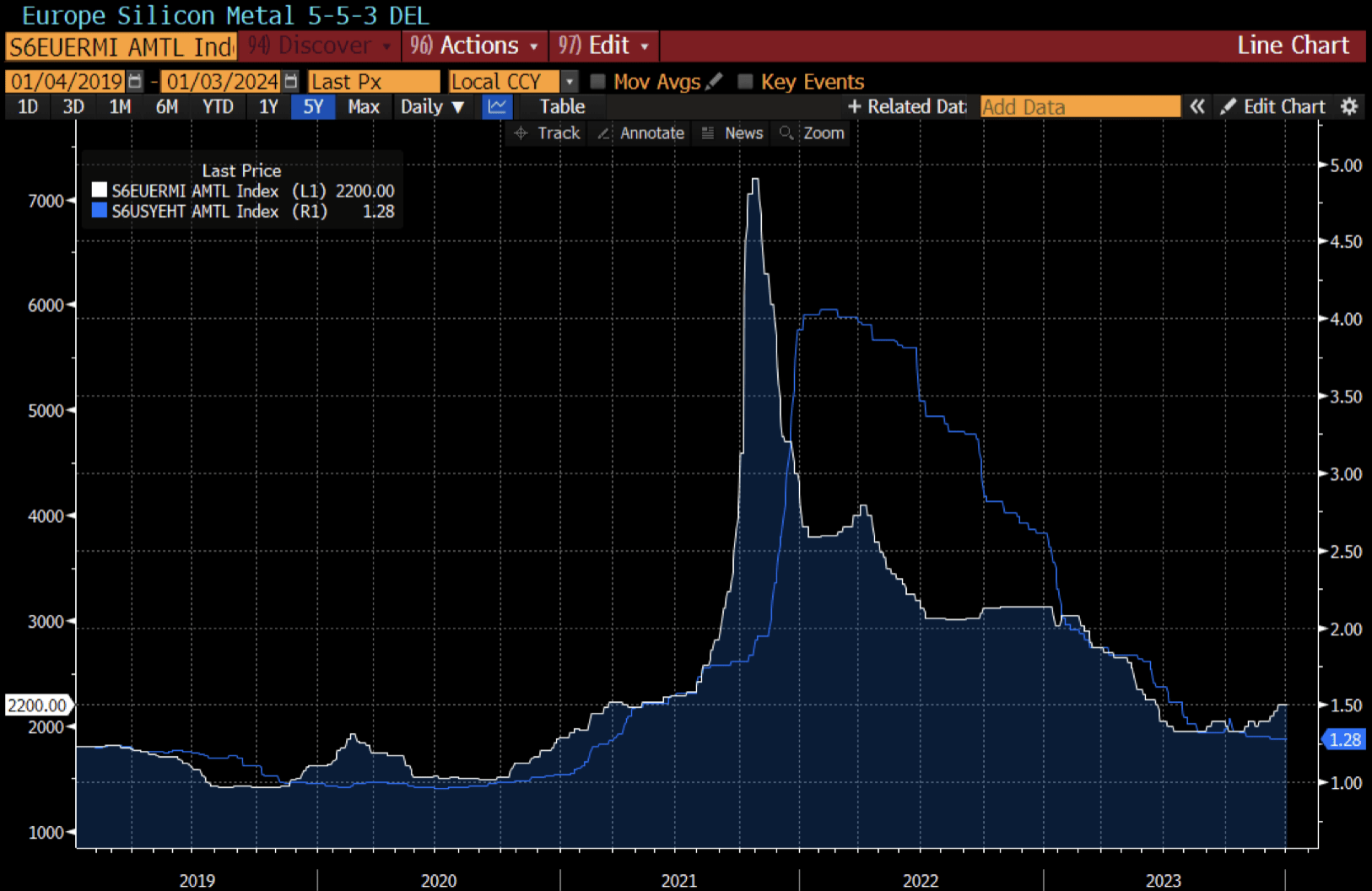

Silicon Metal Prices Likely Bottomed

Management believes the market has bottomed and demand will pick up through the second half of 2024. Price is forecasted to stabilise through 2024, therefore the hope is that volumes grow in second half and into 2025. Management is not adding speculative capacity without contract commitments from customers.

{kind=link}

The key derailment to this thesis is a macroeconomic slow down which will impact volumes in 2024. However considering the increase in volume from solar and supportive US legislation for increasing domestic silicon production over imports from Russia and Belarus, prices may be close to bottoming.

Sentiment is weak due to short term uncertainty despite impressive long term fundamentals. While the sector is highly cyclical, minimum leverage also protects the downside here. Furthermore minimum leverage allows for opportunistic buybacks when shares are undervalued.

Valuation Snapshot

Based on Wall St FCF estimates for FY24 ($273m) and FY25 ($267m), the valuation offers a 20%+ FCF yield. This seems interesting considering volume is expected to expand looking at current industry forecasts.

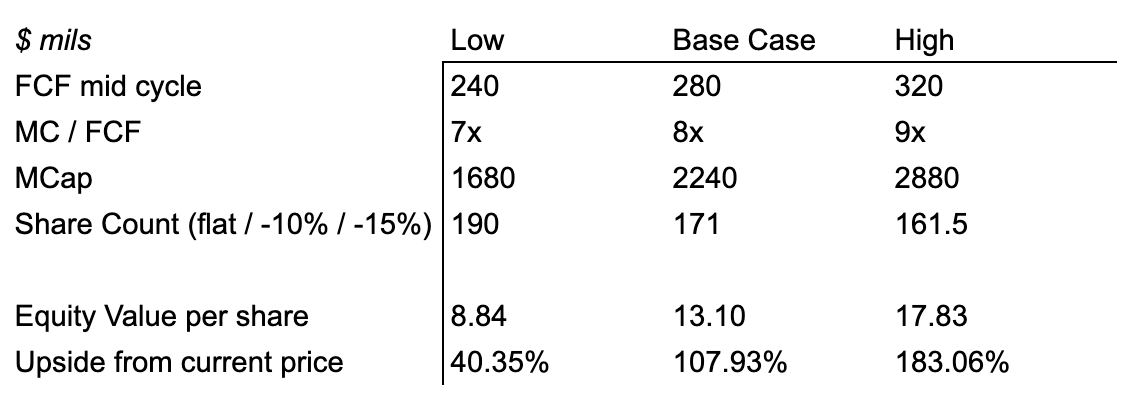

If we assume a 10% reduction in share count, $280m FCF mid cycle and 8x MC/FCF then upside could be 107% ($13.10) in few years' time. An 8x MC/FCF is reasonable in my opinion for a cyclical producer with a leading market position in silicon production. In fact 8x MC/FCF might be a bit conservative considering future volume growth.

The median target price from 2 sell side analysts indicates 82% upside ($11.50). A 10% reduction in share count is roughly $119m if acquired at an average price of $6.30. Theoretically this can easily be facilitated based on annual FCF numbers.

I'm also assuming net debt of $0 due to low debt and some excess cash. Of course this depends on volume growth materialisation, moderate energy/raw material costs and silicon price stabilisation.

{kind=link}

GSM redeemed $150m in senior notes in the summer lowering their net debt / LTM EBITDA to 0.45x. Therefore if we get a hard landing, the risk of bankruptcy through the trough is far lower than typical CapEx intensive commodity producers.

Conclusion

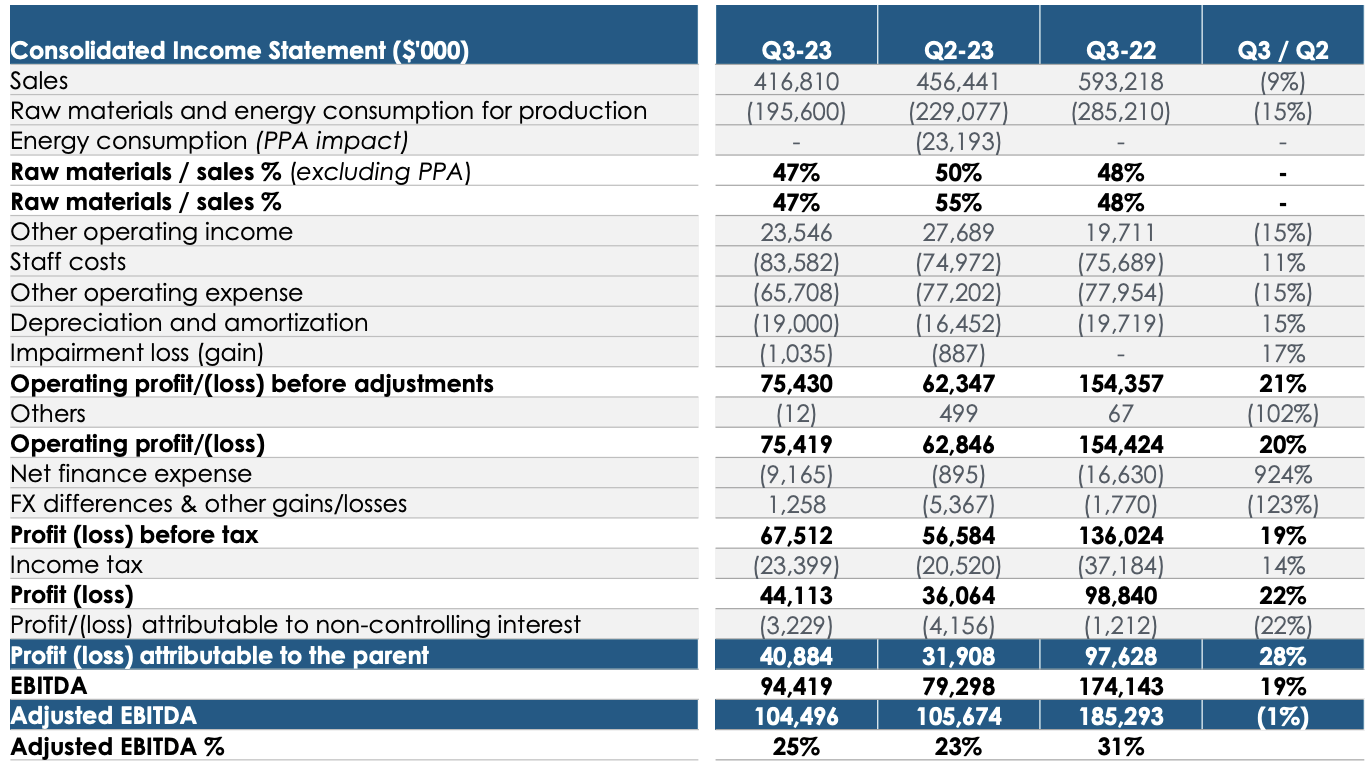

Looking below management continue to deliver impressive results in what is a difficult silicon market. In Q3 energy and raw material costs came in at 47% of sales, profit to GSM was $40.8m. This highlights how well cost and efficiencies across the business has been improved vs the pre-covid days.

{kind=link}

In February the company will announce their shareholder returns policy, I expect further debt reduction plus a dividends policy or buyback authorisation. If management is positive about volume in 2024 it would make sense to utilise buybacks over dividends. Management communicated in November they prefer buybacks if shares remain undervalued. However a risk is that as the market now expects this, a disappointing or weak capital returns plan will send shares falling by a larger degree.

For further details see:

Ferroglobe: Buybacks Expected Amid Short Term Uncertainty