GSM - Ferroglobe: Excellent Business At A Cheap Price

2023-12-12 02:26:49 ET

Summary

- GSM is one of the leading companies in silicon metals and silicon alloys globally. The primary buyers are steel, cast iron, and aluminum producers.

- The company has improved its balance sheet significantly over the last three years. Last quarter, GSM redeemed $150 million in senior notes, reducing the company's total debt to $316 million.

- GSM is more profitable than similar-sized “diversified metals and mining” companies, generating 43.7% Gross Margin, 14.1% ROTC, and 14.7% ROE.

- The company is undervalued compared to its past multiples and percentile ranks, and price action is favorable for entry.

- Given company fundamentals, cheap valuation, and supportive price action, I give GSM a buy rating.

Introduction

Ferroglobe ( GSM ) is a leading producer of silicon metals, silicon alloys, and ferroalloys. They're crucial for steel, cast iron, and aluminum production. Besides that silicon is an integral part of solar panels and battery manufacturing. The demand for both is expected to grow with a double-digit CAGR in the coming years.

The company has solid financials with $161 million cash and $316 million total debt. GSM`s profitability is excellent, too. The company realized 43.7% Gross Margin, 14.1% ROTC, and 14.7% ROE. Last quarter was disappointing due to declining revenue and EBITDA. However, lower energy and materials costs improved the EBITDA margins.

The company is cheaper than its past multiples and is valued in lower percentiles than Global Materials and Global Equity. The price action supports entry with a confirmed breakout above the narrow range and 36 monthly moving average. Only one factor is missing to give a strong buy rating: the company does not pay dividends or repurchase its shares. My verdict is a buy rating.

Company Overview

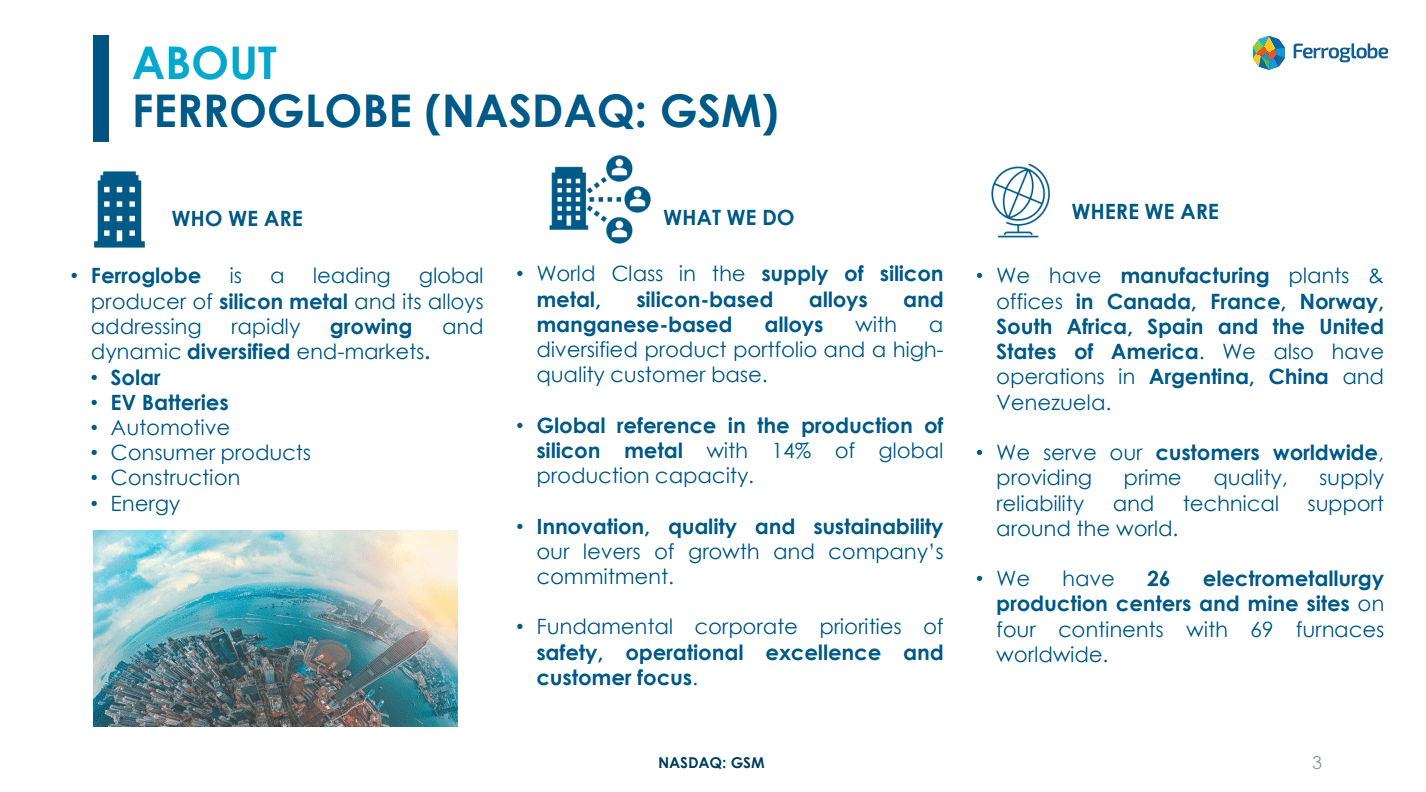

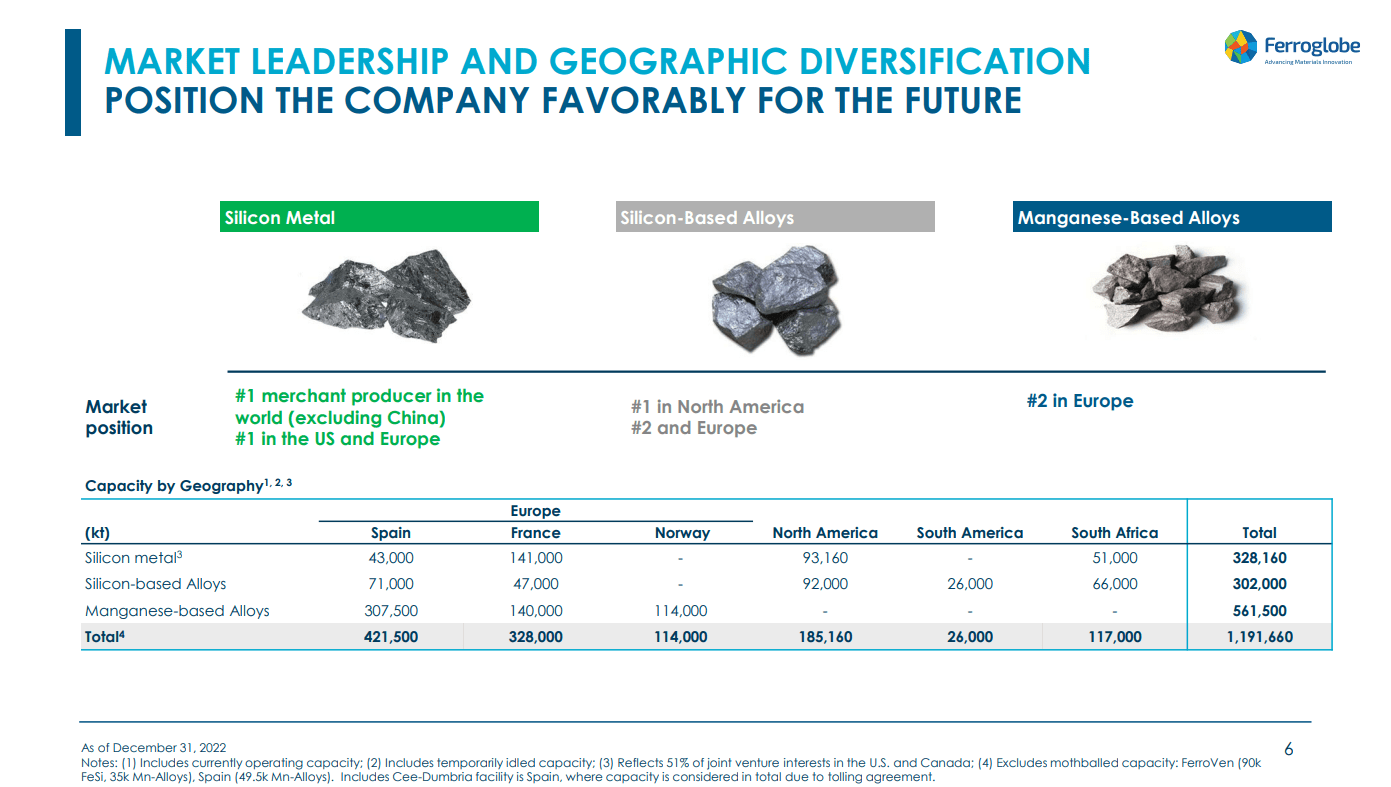

GSM is one of the leading global silicon metals companies, producing 14% of the world supply. GSM has 26 electrometallurgical production centers and mine sites on four continents. The chart below from the last company presentation shows GSM at a glance.

{kind=link}

The company has manufacturing facilities in Canada, France, South America, and South Africa. Besides that, it has operational facilities in Argentina and Chile. GSM has 69 furnaces globally.

The company`s operations are spread across several countries, as shown in the table below:

{kind=link}

27% of the total production comes from silicon metals, 25% from silicon alloys, and 47% from manganese alloys. Geographically, the most significant % of company output derives from Spain, 35%. GSM has even assets in Spain involved in various stages of the production process.

Boo facility is designed to manufacture Calcium Carbide. The plant primarily produces ferro alloys such as ferromanganese, silicon manganese, and refined ferromanganese alloys. The plant has four submerged electric arc furnaces. Monzon is another Spanish facility located in Spain producing ferroalloys. It has two silicon manganese furnaces and two ferromanganese furnaces.

France is GSM's second most crucial country, delivering 27% of the total output. The company has six operation sites there. Aglefort produces silicon metals. The plant has two 33MW furnaces with compound electrodes. Dunkirk plant is dedicated to making manganese sinter alloys and ferromanganese. It has one 102MVA closed electric arc furnace to produce ferromanganese. Montricher plant has three furnaces with compound electrodes for silicon metal production.

Outside Europe, the GSM operates in Canada, the US, China, Argentina, Chile, and South Africa.

GSM`s US segment accounts for 15% of the company`s output. The company in the US has a low ash met coal mine in Kentucky, run by Alden Resources LLC. Another US subsidiary is Alabama Sand and Gravel ((AGS)). It produces metallurgical-grade gravel. ASG currently runs two wash plants and two mines. The alloy plant has five large furnaces (1x32MW, 4x22MW) for ferroalloy production. However, since 1990, the main output of the alloy plant has been silicon metal.

The company has a plant in Mendoza, Argentina, in South America, for calcium silicon and ferrosilicon production. Curiosity is a GSM`s Venezuelan plant, Puerto Ordaz, for ferroalloys production. The plant is still operational despite the political turmoil persistent in Venezuela. South American facilities generate 2% of the company`s output.

GSM has two plants in South Africa: Polokwane and Emalahleni. The former produces metallurgical and chemical silicate. The latter makes ferrosilicon and inoculants. Both plants are located near Johannesburg. South African output is 10% of the company`s total.

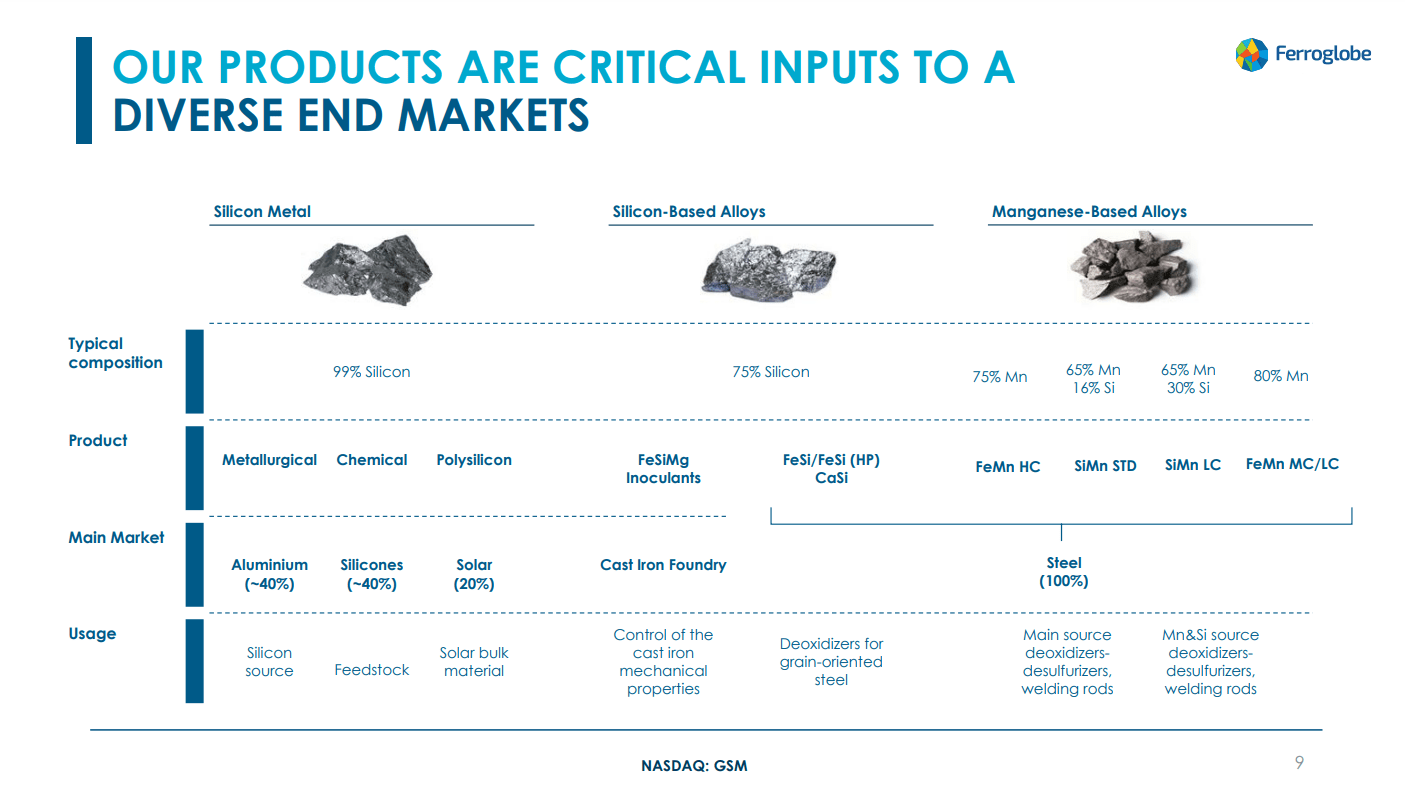

Silicon metals, silicon-based alloys, and manganese-based alloys are crucial for heavy industries such as steel, cast iron, and aluminum production. The table below shows the purpose of using GSM`s output.

{kind=link}

The silicon metal is used as a feedstock in metallurgy and solar panel production. The primary GSM customers of silicon metal are Alcoa ( AA ) and Rio Tinto ( RIO ). Silicon alloys are used in cast iron production to enhance the mechanical properties of materials and as deoxidizers for grain steel. Arcelor Mital ( MT ) and Tata Steel ( TATLY ) are the primary customers. Manganese-based alloys are used for welding rods, deoxidizers, and desulfurizers. thyssenkrupp ( TYEKF ), Tata, and Arcelor are among the top buyers.

GSM has an advantage over its peers as an established player in the industry. It is a high barrier to entry due to CAPEX-intensive business. Besides that, the operation requires highly qualified personnel. Heavy industry and mining have lost their attractiveness for the young generations. The consequences are long-term and profound. The limited supply of skilled employees creates a bottleneck in the industry. If the company has the best plant, its efficiency is limited to the number and the ability of the staff to run it safely and efficiently. In other words, you need tons of money and a large pool of qualified personnel to enter the silicon metal/silicon alloys industry.

In the long term, the demand for GSM production is expected to rise. Steel, aluminum, and cast iron are building blocks of the material world, resulting in a constant demand for GSM production. Besides that, the company has two long-term catalysts: solar panels and batteries.

Both need silicon and silicon-based alloys. Globally, solar power is expected to grow over 300% in the coming ten years, with a 21% CAGR. Battery demand is expected to grow with 56% CAGR till 2030.

Ferroglobe financials

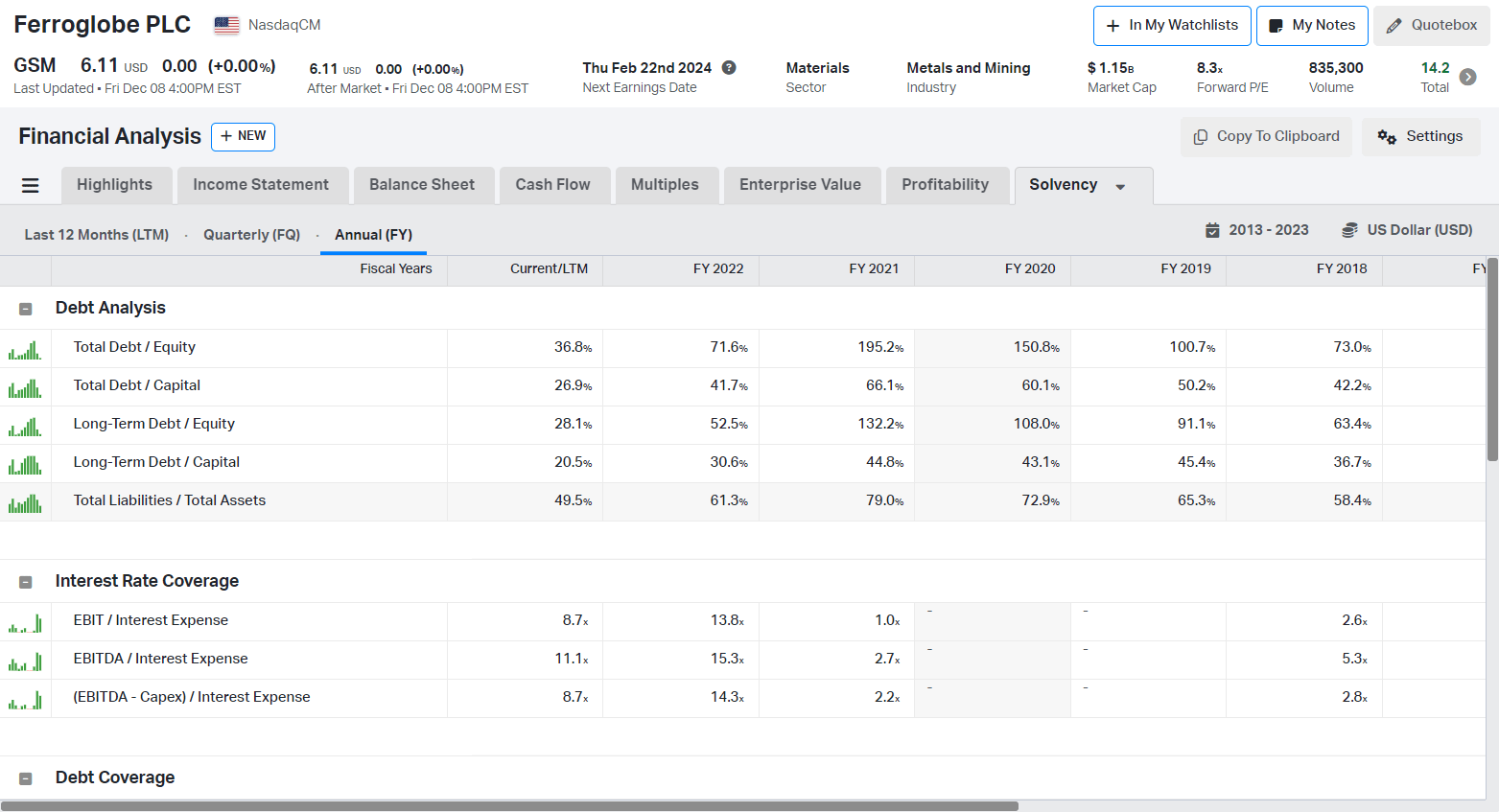

GSM maintains a neat and clean balance sheet. The company has managed to reduce its debts significantly in recent years. The table below shows the company`s capital structure and interest coverage.

{kind=link}

The successful deleverage is impressive. Over three-year GSM total debt/equity, you dropped from 192% in 2021 to 36.8% in 3Q23, an 81% decline. Similarly, long-term debt/capital declined from 44.8% in 2021 to 20.5% in 3Q23.

In 3Q23, the company redeemed $150 million of its senior security notes. GSM has $161 million cash and $316 million total debt, resulting in a total debt-to-cash ratio 0.5. GSM performs well compared to similar-sized “diversified metals and mining” companies. It is not the most liquid company, although it is far from the worst. Ivanhoe Electric ( IE ) has $249 million cash and $114 million total debt, but Nexa Resources ( NEXA ) has $422 million and $1.62 billion.

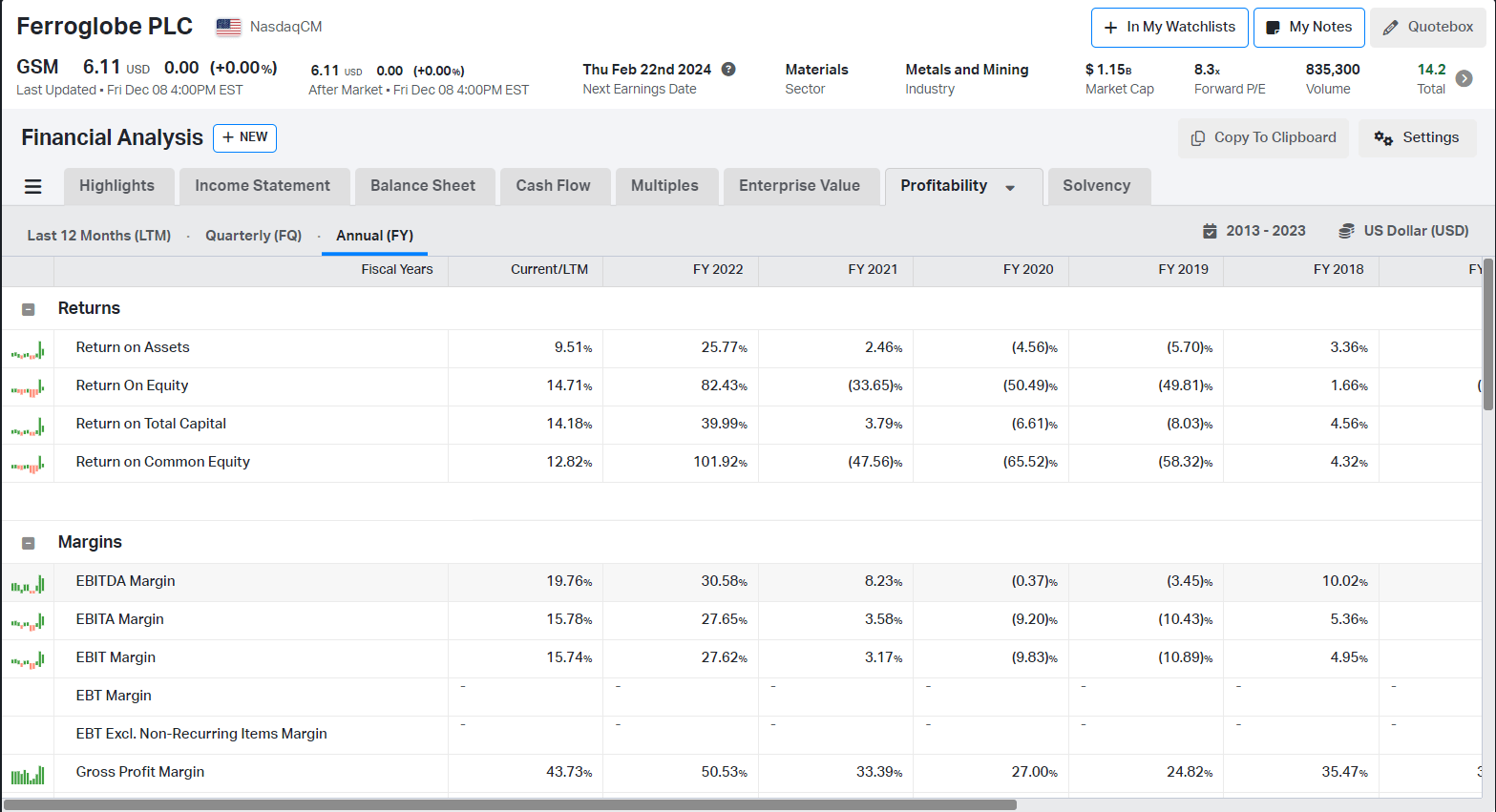

Profitability

GSM is a profitable business with adequate margins and returns.

{kind=link}

Since 2019/2020, the company has improved its results. For the last three years, it maintained a gross margin of over 30% and a positive EBITDA margin despite the ups and downs in the commodity markets. Compared with its peers, such as Compass Minerals (CMP), IE, and NEXA, the company fairs much better.

GSM has 14.1% ROTC, 14.7% ROE, and 19.7% EBITDA Margin. For reference, NEXA has (15)% ROTC, (1)% ROE, and 19.7% EBITDA Margin; CMP has 3.7% ROTC, 4.0% ROE, and 14.7% EBITDA Margin.

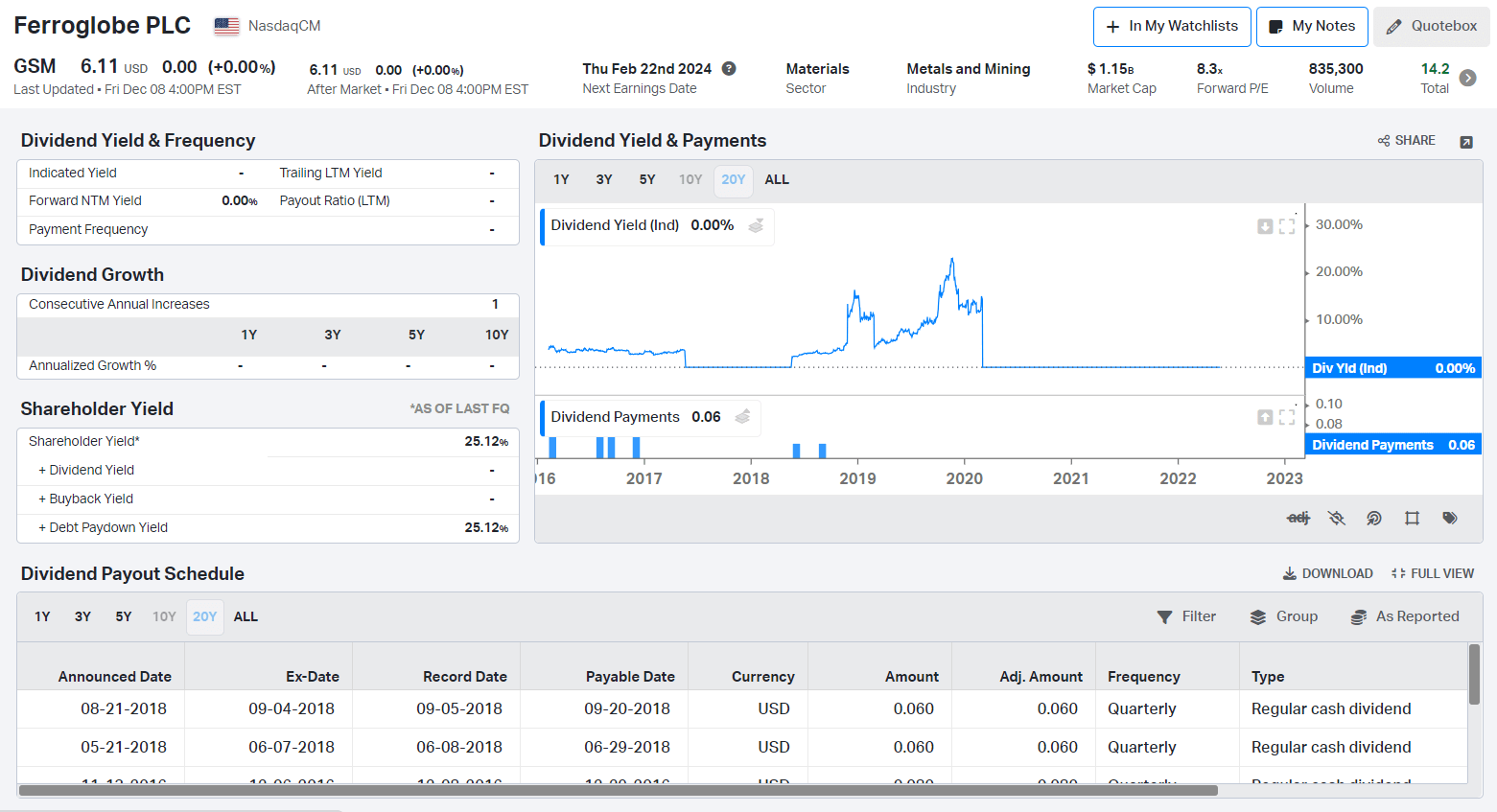

The last time the company paid dividends was in 2018. GSM does not have a shares buyback policy, either. However, improving the company`s debt profile generates yield for shareholders.

{kind=link}

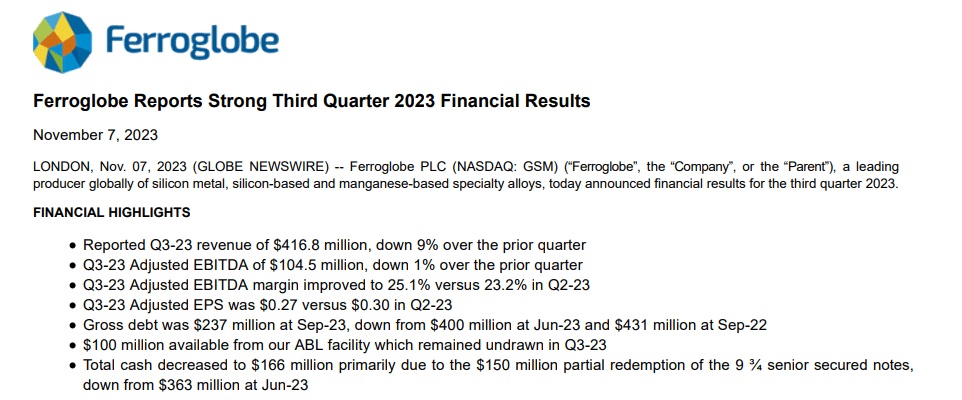

3Q23 results

Let`s look at the results from last quarter .

{kind=link}

Revenue declined 9% QoQ and 30% YoY. Adjusted EBITDA is down 1% QoQ. However, the adjusted EBITDA margin has improved to 25.1% from 23.2% QoQ. The company has significantly reduced its debt in the last quarters.

The lower costs are the reason for the improved margin despite declining sales and EBITDA. In 3Q23, production's raw material and energy costs dropped to $196 million, down 22% from $253 million 2Q23. Raw material and energy consumption for production as a proportion of sales declined to 47% in the third quarter of 2023 from 55% in the previous quarter.

The company bought a quartz mine in South Carolina with 300kt annual output. GSM plans to pay $11 million in cash and invest an additional $ 4$ million in CAPEX. The latter is a crucial ingredient in silicon metal production.

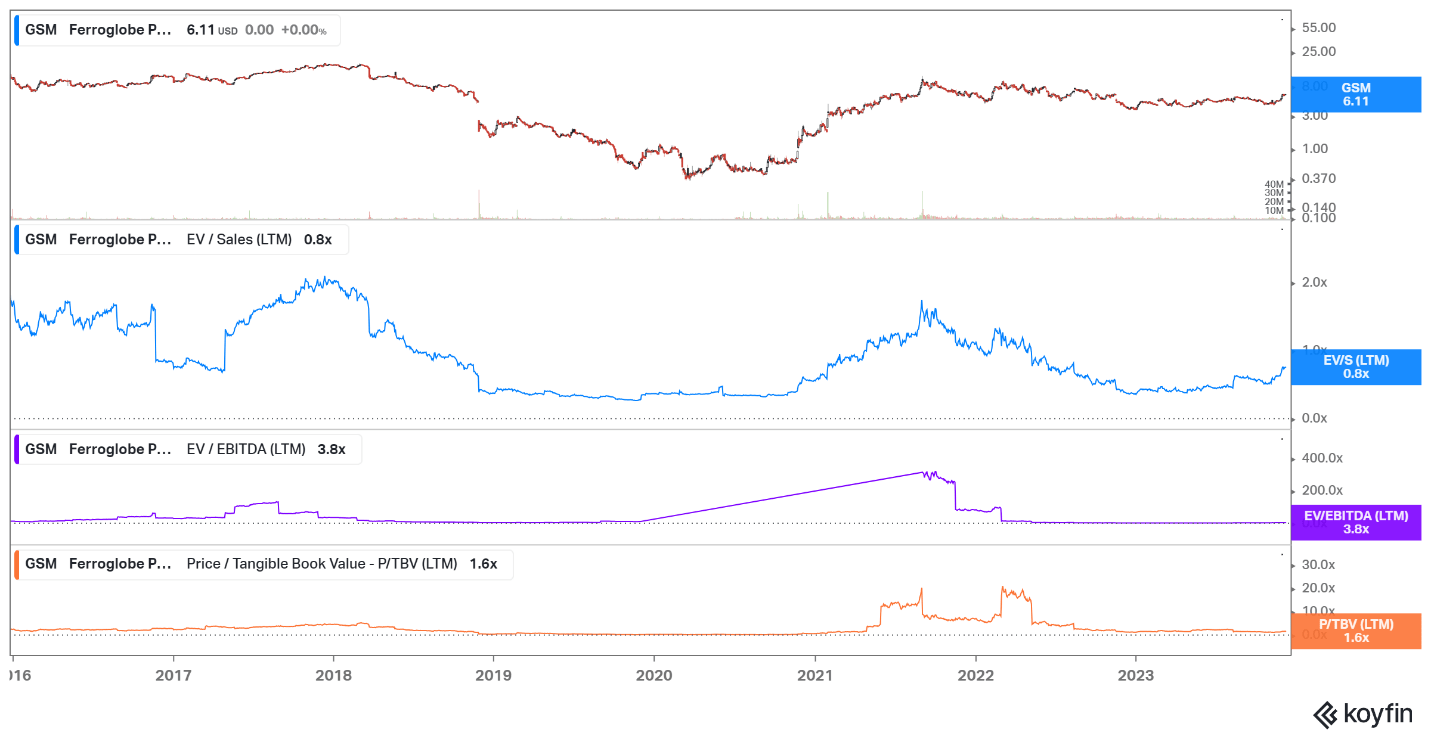

Valuation

GSM is cheaper compared to its historic multiples. The chart below shows the company`s EV/Sales, EV/EBITDA, and P/TBV for the past ten years.

{kind=link}

The current multiples are 0.8 EV/Sales, 3.8 EV/EBITDA, and 1.6 P/TBV. These figures are well below the company 10Y average (1.5 EV/Sales, 14.2 EV/EBITDA, 1.87 P/TBV) and past 10Y peaks (2.0 EV/Sales, 140 EV/EBITDA, 5.5 P/TBV).

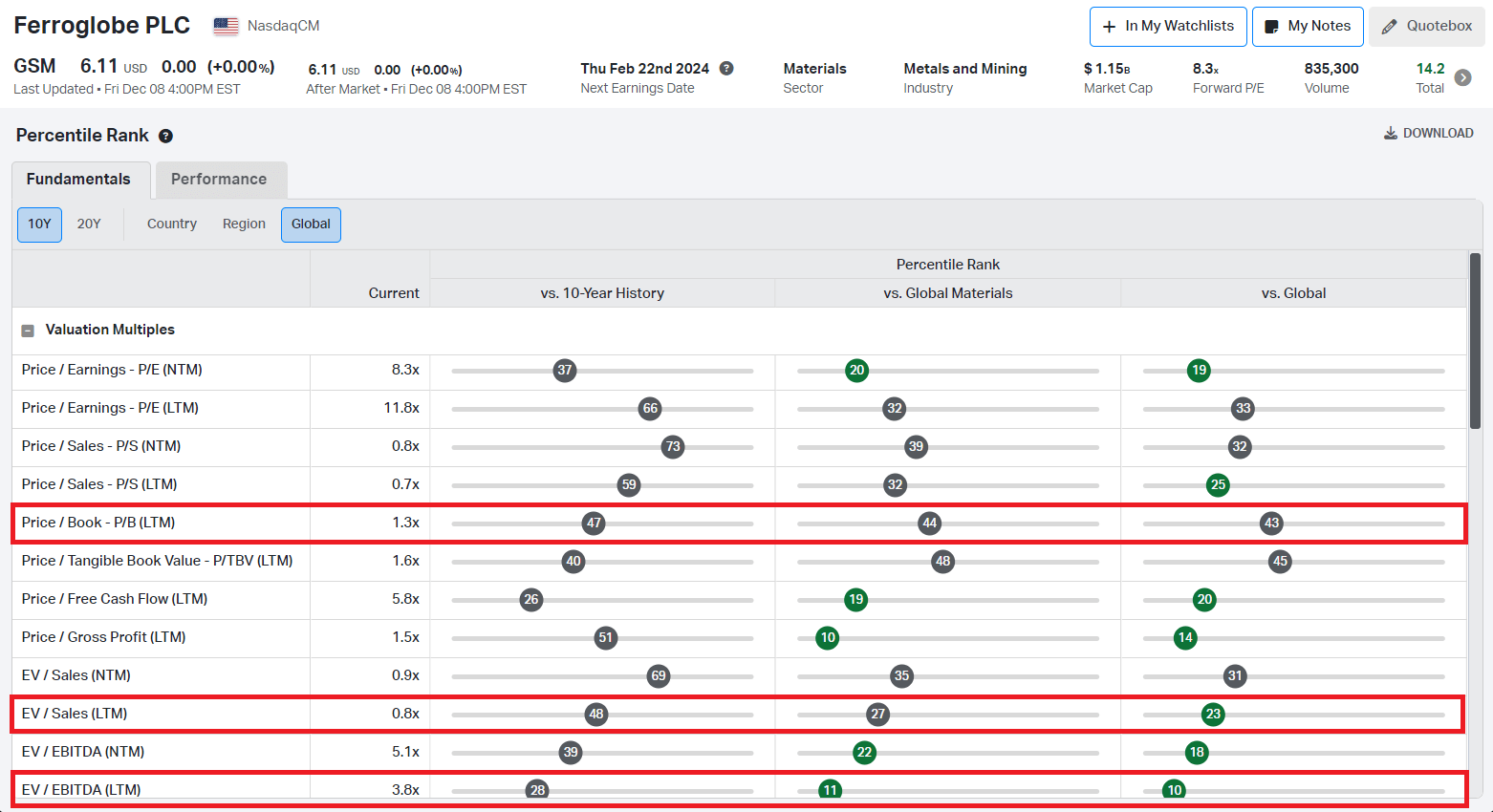

Compared to Global Materials and Global Equity, GSM trades in the lower percentiles, as shown in the chart below:

{kind=link}

Using EV/Sales, GSM is in the 27 th percentile in Global Materials and 23rd in Global Equity. Looking at EV/Sales, the stock is cheaper, falling into the 11 th percentile in Global Materials and 10ts in Global Equity. In conclusion, GSM is undervalued compared to its past multiples, Global Materials, and Global equity.

Price Action

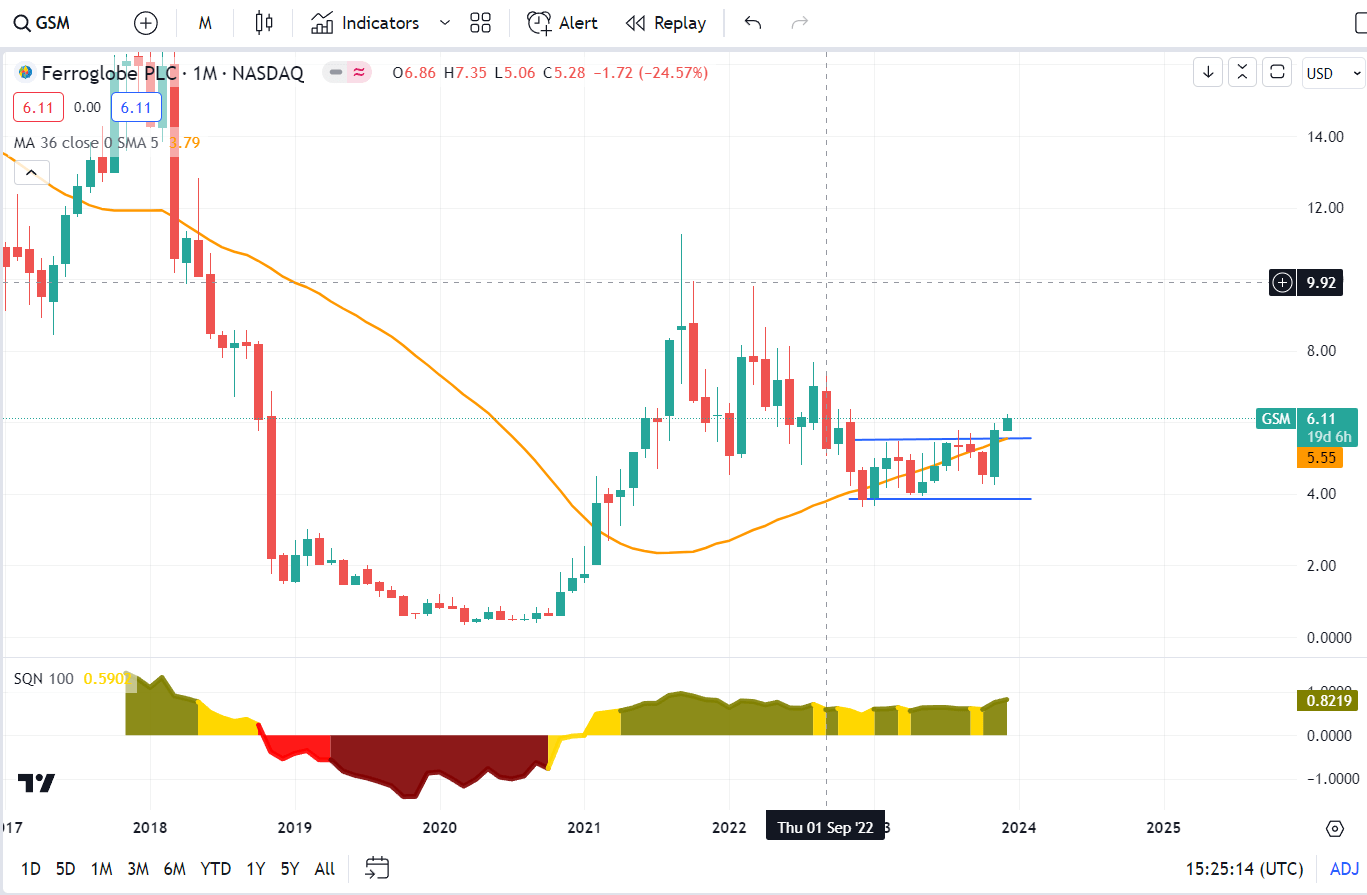

The price action is favorable for entry—the price breakout is from a narrow range and above 36 months' simple moving average.

{kind=link}

SQN indicator supports the thesis, too, being in a bull-quiet regime. The next significant resistance is around $7.5-$8.0 zone. Given the alignment of SQN, MMA, and the confirmed breakout, I consider the current setup an excellent entry point.

Risks

The demand for GSM`s production heavily depends on the economic cycles. If we enter a recession, the company`s performance will suffer. However, in the long term, the demand for steel, aluminum, and cast iron will continue to grow following the developments in the Global South. India, Nigeria, and Indonesia are among the countries with the largest populations. A growing fraction of them is entering the lower middle class, resulting in a higher demand for goods and services. This also means increased demand for material and energy.

The market risk is always present. The last several weeks were great for tech stocks and emerging markets. However, in the previous week, another cycle of asset rotation, from large caps (AAPL, META, TSLA, etc) into small caps started. This week has an FOMC meeting and a $120 billion auction of US bonds. The latter might set the tone for the coming week’s market price action.

Investors Takeaway

GSM is one of the leading companies in silicon metals and silicon alloys globally. The company supplies steel, cast iron, and aluminum producers with critical components for their production process. However, the two leading catalysts for GSM are batteries and solar demand growth in the coming years. The company has improved its balance sheet significantly over the last three years. Last quarter, GSM redeemed $150 million in senior notes, reducing the company`s total debt to $316 million. GSM is more profitable than similar-sized “diversified metals and mining” companies, generating 43.7$ Gross Margin, 14.1% ROTC, and 14.7% ROE.

GSM does not pay dividends and does not have a share buyback policy. If both were presented, I would give it a strong buy rating. However, the company is deeply undervalued compared to its past multiples and percentile ranks, and price action is favorable for entry. Given company fundamentals, cheap valuation, and supportive price action, I give GSM a buy rating.

For further details see:

Ferroglobe: Excellent Business At A Cheap Price