GSM - Ferroglobe: Nice Rebound Quarter And Almost Net Debt Free

2023-08-15 17:17:19 ET

Summary

- Ferroglobe reported better-than-expected results with adjusted EPS of $0.30 and EBITDA of close to $106 million.

- The company redeemed $150 million of bonds and signed a new power purchase agreement with the Spanish government.

- The stock is still cheap and management is optimistic about a turnaround in the next few quarters.

Ferroglobe Second Quarter Update:

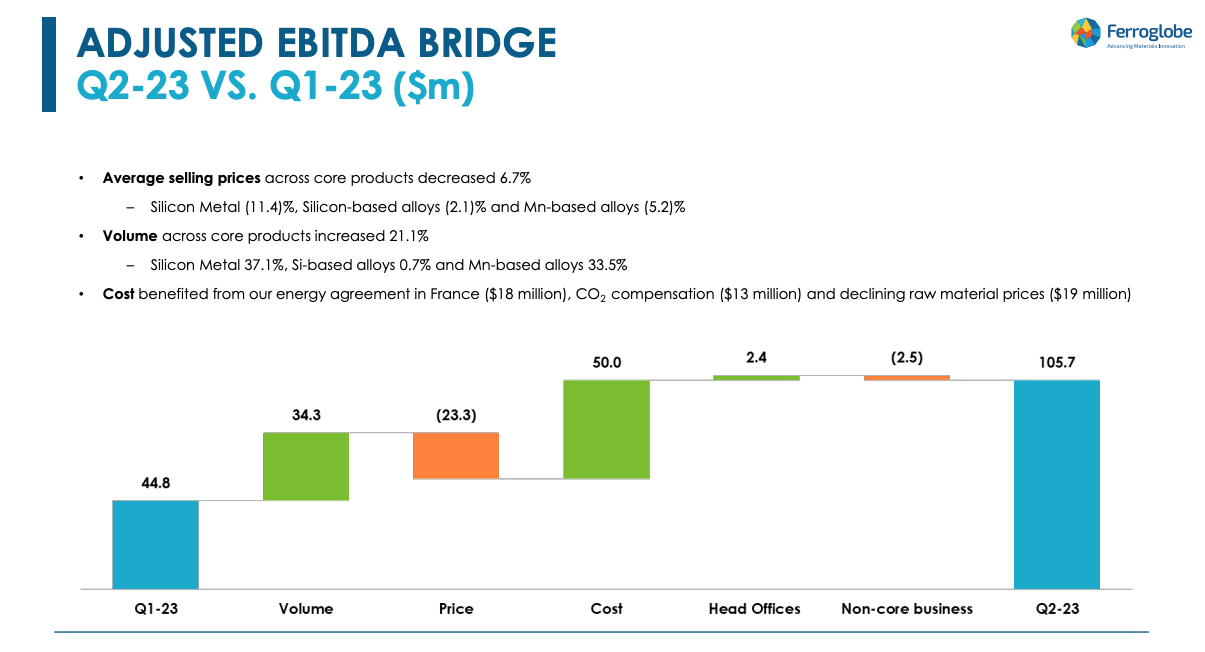

Ferroglobe ( GSM ) reported results that were better than most people expected on the buy-side and the sell-side. There are not many sell-side analysts, who cover the name, so speaking with other buy-side holders of the stock can matter more on how the stock trades. Regardless of who was looking, the numbers are solid. Adjusted EPS of $0.30 and EBITDA of close to $106 million were both a big rebound over Q1's $0.05/share and ~$45 million respectively.

{kind=link}

I continue to find it frustrating that cash generation lags, but whereas I have been critical of management not managing current assets aggressively enough, this quarter is not their fault. There was a pretty big buildup of "other current assets" that was tied to the PPA's (power purchase agreements) in Spain and France. Cash taxes also came in at $79 million versus income statement tax expense of $20 million. As a result, of these cash uses, cash generation was only about $1 million when including working capital.

Good News Going Forward

The company redeemed $150 million of the 2025 bonds which, restrict cash going to shareholders. They have less than $200 million to go on those bonds. It is painfully slow waiting for these bonds to be called as cash almost equals debt, but clearly the company wants to keep several hundred million of cash on hand. Other good news is the newly signed PPA with the Spanish government that gives the company access to renewable power at prices where the company can produce profitably. That doesn't guarantee the company's customers can run mills if power prices spike again, but it's a step in the right direction.

Lastly, silicon was added to the US critical materials list. That should reinforce protections against dumping by players like Russia, Kazakhstan and Malaysia, although the industry in the US is pretty protected already.

Conservative Guidance

The company is sticking with conservative guidance for the year citing weak volume and pricing environment. I'll highlight that the company just did about $150 million of EBITDA in the first half, with over $100 million in Q2. Yet, they're keeping the Q1 guide of $270-$300 million of EBITDA in place. Management calls the environment extremely challenging, mostly because of an anticipated slowdown of silicon metal production in France. On a cash basis, this will actually hurt as the company will build silicon metal inventory in Q3 to be able to supply customers when they slow down production in France. I expect Q3 to be close to Q2 and Q4 to be a down quarter. The good news is that they see an improvement in the silicon metal inventory at customers, while they expect alloys to remain weak through the end of the year.

Valuation

Either because skepticism of silicon alloy and silicon metal pricing holding up, fear of sluggish Chinese demand, conservative guidance, but this company trades at a low multiple of what looks like trough numbers and only $37 million of net debt on the balance sheet.

| Market Cap ($4.83/share) |

| $905 million |

| Debt |

| $400 million |

| Cash |

| $363 million |

| Enterprise Value |

| $942 million |

| EV/2023 Midpoint EBITDA ($285 million) |

| 3.3x |

Risks

Anything attached to metals trades cheap, full stop. GSM trades cheap for a metals company, even if its biggest segment, silicon metal is an input into solar panel production. I think once the company takes out the restrictive and high coupon bonds and starts returning cash to shareholders, it might start trading at a more reasonable valuation. But a drop in market prices of any of its products could keep it in the doldrums

Conclusion

The stock is reacting well to these numbers, but I think it's still cheap. Management was reasonably upbeat on the conference call that the cycle should be turning higher over the next few quarters, particularly in the US. The bonds are likely gone by year-end (either redeemed with cash or refinanced), which will allow the company to finally return cash to shareholders. Given that they can do this type of EBITDA even in a soft environment, a rebound in demand could be another catalyst to move it higher. In a market where a lot of garbage has rallied hard, this stock offers compelling valuation and a good risk/reward set up.

For further details see:

Ferroglobe: Nice Rebound Quarter And Almost Net Debt Free