GSM - Ferroglobe Secular Tailwinds For A Cyclical Miner

2023-08-24 17:29:37 ET

Summary

- Ferroglobe is a global leader in advanced metallurgical products used in various industries.

- The company experienced a 10x growth in its stock price after a 90% crash in 2018.

- Q2 earnings showed a considerable rebound, indicating potential future growth, but concerns remain about production shutdowns and environmental regulations.

The London-based Ferroglobe ( GSM ) is a "global leader in advanced metallurgical products" necessary in a wide variety of industries including automobiles, suspension bridges, and healthcare products. With an industrial footprint that spans across the globe, Ferroglobe both digs up raw materials at mine sites and fashions them into useful metals at many of their metallurgy plants.

Following a 90% crash at the end of 2018, GSM was a mere penny stock, trading under a dollar from 2019-2021 until it eventually shot up to its current price of around $5. Perhaps this 10x growth is a sign that investors have already missed the boat on Ferroglobe, especially as GSM stock has been fairly stagnant for the past year. Despite having a consistently high FCF yield and low P/E ratio, we would have labeled GSM as a value trap a few weeks ago due to consistently underwhelming earnings and rising production costs and issues.

However, on August 15th, Ferroglobe reported its Q2 earnings, which included a considerable rebound in nearly every aspect of the company for the first time since early 2022. This bounce back in earnings, in addition to the stock price rising by around 18%, makes us wonder whether Ferroglobe still has room to grow into a higher multiple. After providing an overview of Ferroglobe's general business and the clients it serves, we will dive into why the company was on such a downward streak and whether this past quarter is a one-time event or a sign of future growth.

Business Overview

Ferroglobe specializes in three main products that account for over 90% of its revenue: Silicon Metal, Silicon-Based Alloys, and Manganese-Based Alloys. Silicon metal makes up the most significant percent of Ferroglobe's revenue, which they are the biggest producer of in the Western World. The largest purchaser of silicon metal is the chemical industry, using Ferroglobe's silicon to produce solar cells and electronic semiconductors. With the shortage of semiconductors delaying automobile manufacturing over the past years, it becomes clear why GSM stock suddenly skyrocketed, as manufacturers were in dire need of silicon metal to rapidly produce these chips. Although this boom in production caused by the shortage is already flattening out, as seen in Ferroglobe's financials, that doesn't mean silicon metal won't remain a necessary product.

There may be potential for another boom in silicon demand. According to analysts , silicon is in the early phases of replacing graphite in electric car batteries as it "enables significantly higher energy density and faster charging". This is a trend adopted by car manufacturers GM, Porsche, and Mercedes Benz, plus these silicon batteries are theorized to be necessary for any sort of electric plane that may be developed in the future. Finally, with the number of solar panels growing at a greater rate every single year, nearly doubling in 2022, silicon is constantly needed to produce these solar cells. Overall Ferroglobe is in a great position as the leading supplier of silicon metals and should be able to capitalize on a long term secular demand.

Ferroglobe's other main products are used to "improve strength and quality of iron steel products" according to the company website. More specifically, this alloy-treated steel is a massive part of the support materials used in suspension bridges and automobiles, in addition to other basic construction projects. Since bridges and automobiles are both necessary parts of global infrastructure that need constant repair and renovation, there doesn't seem to be any worry that demand will disappear for these products.

These metals are all mined and treated at Ferroglobe's 25 global operating sites spanning 5 different continents. Historically, the company has added a new site every year, and they are planning to continue with the purchase of a new quartz mine and the expansion of an existing one in Spain. Consistent and controlled growth is something we like to see in stocks, something Ferroglobe continues to stay on track of achieving. Obviously, mining isn't the most eco-friendly business, which is a slight concern as governments continue to enforce strict environmental regulations. However, Ferroglobe appears committed to keeping its production clean, mainly through the launch of its 2022-2026 ESG strategy. This includes more efficient use of energy, reducing the carbon footprint, and working on their relationships with local governments.

Past Earnings and Potential Concerns

The main reason we chose to mention Ferroglobe's efforts to be more environmental is that the company's earnings have been shaken up due to shaky agreements with governments in the past. Despite the Q2 earnings moving in a strong direction, Ferroglobe was on a multi-quarter trend downward, something we want to explain in case of a future recurrence. The worst of this slip in earnings was earlier this year when the company's adjusted EBITDA fell 66% in Q1 2023 earnings. However, this wasn't some catastrophe with a product or some rare one-off event, but a consistent downward spiral of production volume and costs on all ends of the business. To begin, the cost of producing all three products had been trending upward, particularly due to a lack of energy and C02 compensation. With how much management claims to be focused on improving the cleanliness of their product, it is suspect that their compensation decreased. Additionally, the price of all three products fell in markets across the world, due to the cyclical nature of the industry.

Finally, the volume of production fell for both silicon metal and manganese alloys. This was mainly due to a shutdown in France due to an agreement failure with the French government. A new agreement has been reached, as seen by the bounce back in Q2, though that doesn't mean a similar issue couldn't arise in a different nation or in the future.

Shutdowns due to poor government relations or new regulations are our greatest concern with Ferroglobe. This includes an American shutdown in 2018 at Niagara Falls , that saw disappointing earnings lead the stock price to fall over 90%. More recently, extremely high power prices and strict natural gas laws led to a Spanish shutdown in 2021. We do believe Ferroglobe is better equipped to handle these shutdowns now, particularly as they continue to expand/diversify their global footprint each year and reach new agreements with national governments. Unplanned shutdowns need to be avoided in the future.

Q2 Rebound in Earnings

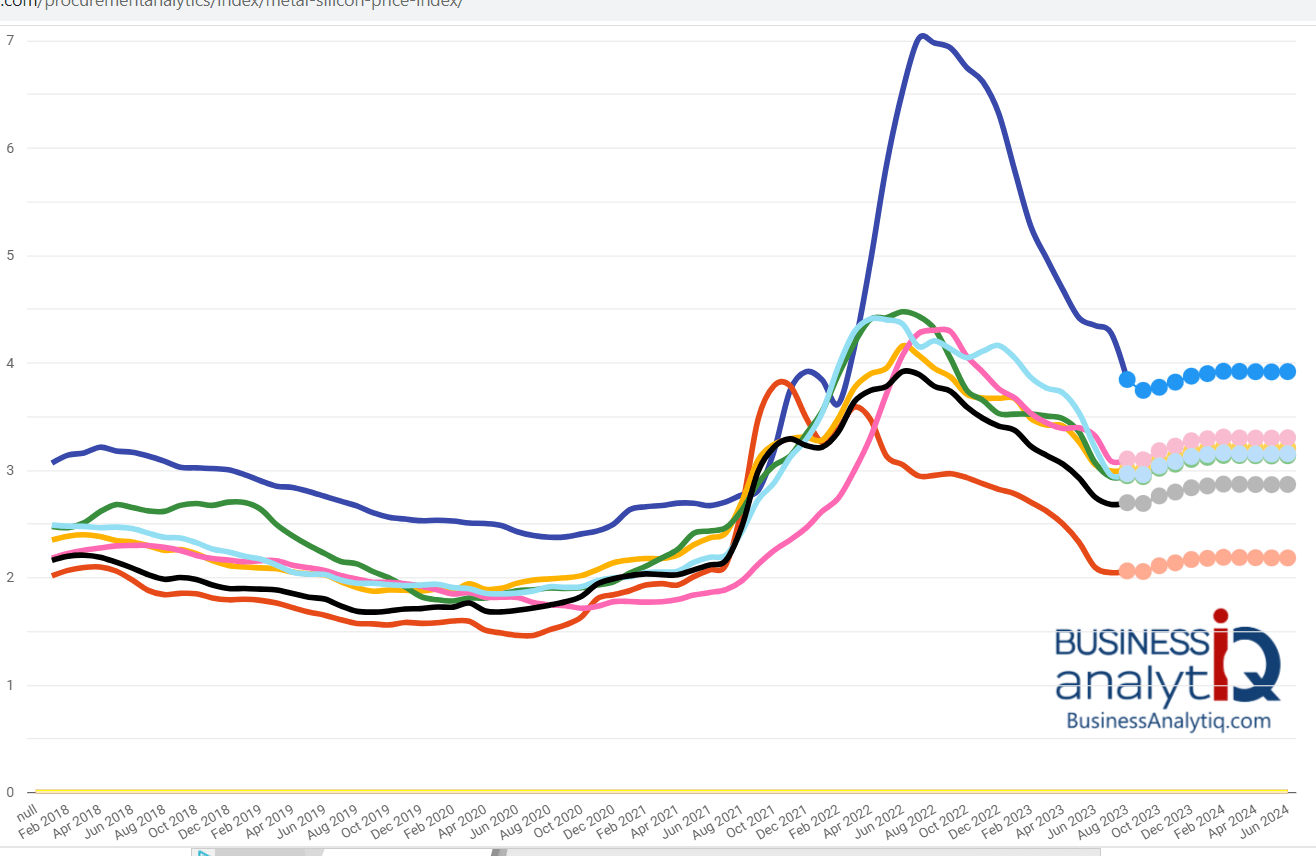

Metals: Silicon Pricing Major Markets of the World

{kind=link}

source: Business Analytiq

As the above chart shows, prices may be stabilizing for silicon metals. The dots are projected forward pricing.

For the first time since early 2022, Ferroglobe had a strong quarter, with pre-tax profit rising from Q1 to $56m. Despite commodity prices continuing to decrease (normalize) for all three products, management was able to create a 2.4x sequential rise in Adjusted EBITDA and a 52% jump sequentially. This was mainly facilitated by a boom in the production of Silicon Metal and Silicon-Based Alloys. Silicon Metal, Ferroglobe's largest product, increased revenue by 165% QoQ, in addition to cutting its manufacturing costs by $36.5. The same goes for other products, which all saw a rise in volume and decrease in costs, though not quite on the same level.

Steel demand has recently been low in Europe, driving the price down dramatically for alloy products and preventing a massive increase in earnings despite lower costs and higher production levels (GSM Q2 report ). As mentioned before, management's ability to negotiate positive agreements with the national governments they operate in could be the biggest factor in determining Ferroglobe's success. This past quarter, Ferroglobe finally has a positive outlook for future negotiations. Firstly, the shutdowns in France, which continued to drive down earnings, ended, as management has come to a long-term energy agreement there. The same goes for Spain, where the company recently finalized its first long-term power agreement, which allows for the resumption of operations that use only renewable energy. Finally, the US Department of Energy just announced that they are classifying silicon as a critical material, "encouraging onshoring and further development of the US supply chain for solar and batteries," an extremely positive outlook for production in the United States (USDE , GSM Report).

Cleaning up the Balance Sheet

As a commodities company, the price Ferroglobe receives for its products is out of its control. The business is hyper-cyclical. To deal with this, famed investor Peter Lynch advises that "the most important question to ask about a cyclical is whether the company's balance sheet is strong enough to survive the next downturn," something we believe Ferroglobe can handle. Despite some very shaky quarters with lower earnings, one mission has remained consistent for management: reaching net cash positive status over the next few quarters. This was further solidified this past quarter with an increase in cash and a continued decrease in net debt to $37m.

A large part of this debt-reduction plan has been the redemption of Senior Notes, something management continues to follow through with seen by the redemption of $150 million worth in July. Additionally, Ferroglobe continues to improve its cash flow, generating $131 million of working capital in Q1 and another $79 million in the past quarter. However, one thing the investor report fails to point out is that Ferroglobe's Free cash flow completely plummeted by 99%. This is particularly due to an 83% drop in operating cash flow, likely from releasing working capital and lower commodity prices, but is still quite odd with the increase in earnings and continued reduction of debt.

Management Strength

Management is a bit of a mixed bag when it comes to Ferroglobe. On the one hand they are extremely experienced. CEO Marco Levi has over thirty years of management experience in the industry and is known for turning around companies' earnings. From 2014-2016 he served as CEO of Ahlstrom, a global fiber materials company, where he increased company earnings for twelve consecutive quarters and managed to cut debt from 80% to 40%. Since becoming CEO of Ferroglobe in 2020, he has already generated 10x on the stock and has the company on track to further reduce debt. The same goes for the other management, who at least all have 20+ years in some niche of the metals industry. However, management owns less than 1% of the company's stock as a concern. A lot of management is fairly new to the company, as Ferroglobe began to clean house following the stock crash in late 2018.

Valuation

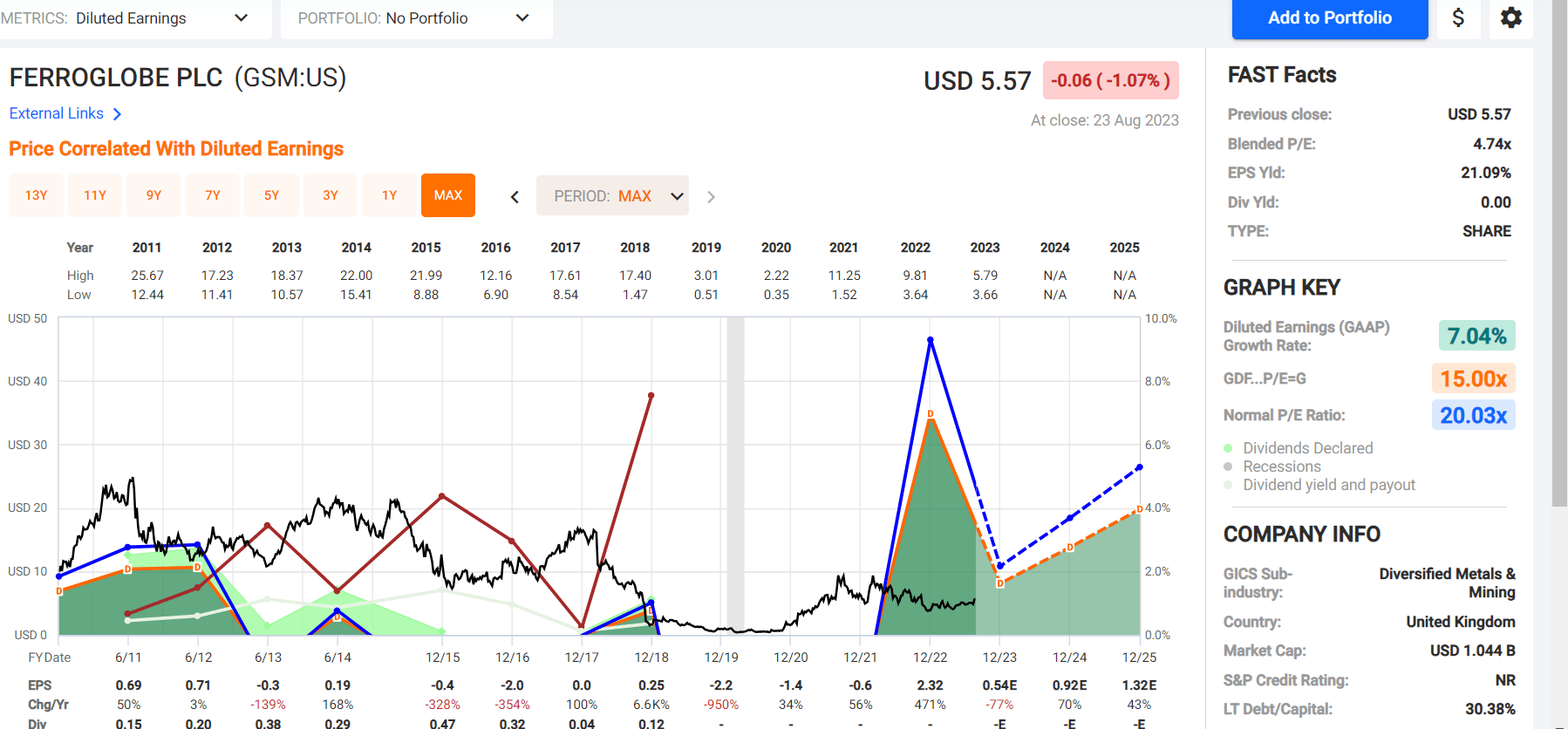

{kind=link}

Source: Fast Graphs

As the chart above shows, earnings (green shaded area) are uneven and spotty, as is usual for most mining concerns. Peter Lynch warns that "buying a cyclical… when the P/E ratio has hit a low point is a proven method for losing half of your money in a short period of time." For Ferroglobe, the low current P/E ratio of 4.7X would fit Lynch's description, and could hint at the stock as a value trap. However, due to the 42% decline in share price since September 2021/March 2022, we believe it's a good time to take a hard look. As the first chart above shows, silicon metals went through a cyclical bubble and are now normalizing with GSM still making money. Based on forward projections, the products it mines, and the industries it serves, we think Ferroglobe may appeal as a secular story for an opening position of 1% of a portfolio, and buying more on continued declines in debt and/or big share price declines. We note that the metals and mining sector currently trades for 16.4X vs. a 3 year average of 29X, putting Ferroglobe in deep value territory vs. the industry.

As well, earnings have just started to rebound for the first time in quarters. Warren Buffett states that "being the low-cost producer is all-important…when selling a product with commodity-like characteristics". Last quarter, Ferroglobe had an operating profit margin of 13.58%, which beat out main competitors Elkem's 12% and Wacker's 9.8%.

We believe Ferroglobe can generate $120m in diluted earnings over the next year in a stable to slightly up metals pricing market, providing an 12% earnings yield and a reasonable 8X P/E. Positive catalysts could be a re-rating of the multiple, and higher prices for its products now that they have corrected.

Downside risks

Risks to our thesis are problems with production from government regulations/agreements. Higher taxes (current taxes are already steep). And obviously a recession is a concern. As the Fast Graphs chart above shows, the company lost money during the last recession. Big management changes, and management not owning a significant percentage of stock are also risks.

Conclusion

We are confident that demand for silicon and other metals is going to increase as the globe transitions towards electric vehicles and solar power, though we are unsure that Ferroglobe will be able to keep up with the demand. Management seems to be driving the company in the right direction- cleaning up the balance sheet, steadily expanding, and establishing better government connections. Based on potential catalysts and a reasonable valuation, we give Ferroglobe the green light for a small buy here.

For further details see:

Ferroglobe, Secular Tailwinds For A Cyclical Miner