GSM - Ferroglobe: The Company Is Deeply Undervalued With Current Fundamentals

2023-05-15 00:46:11 ET

Summary

- Ferroglobe has reported sales of $400.86 million, decrease of 43.95% compared to $715.26 million in Q1FY22.

- GSM has planned to expand its quartz mine in Spain and has signed a letter of intent for acquiring a new high-quality quartz mine.

- After comparing the forward P/E ratio of 8.65x with the sector median of 13.12x, we can say the company is undervalued.

Investment Thesis

Ferroglobe ( GSM ) deals in the production of silicon metal, silicon-based alloys, and manganese-based alloys. The company has recently reported its first-quarter results and performed comparatively weaker than the previous year. This performance has resulted from a challenging macroeconomic environment. However, Ferroglobe is significantly undervalued with current fundamentals as per the P/E valuation method. Also, the company has ample growth opportunities in the long term due to the tailwinds in the industry and its recent expansion activities, which can help it gain momentum in the coming years.

About GSM

Ferroglobe is a leading manufacturer of silicon metal, silicon-based alloys, and manganese-based alloys worldwide. The company also owns quartz mining operations in Spain, the United States, Canada, and South Africa, low-ash metallurgical quality coal mining operations in the United States, and hydroelectric power interests in France. It provides silicon compounds used in the chemical industry, aluminum, automotive parts, electronic semiconductors, ductile iron, photovoltaic (solar) cells, renewable energy, and steel, all of which are critical components in the production of a wide range of industrial and consumer products.

Ferroglobe manages its operations in eight operating segments: North America- Silicon Metals, North America- Silicon Alloys, Europe- Manganese, Europe- Silicon Metals, Europe- Silicon Alloys, South Africa- Silicon Metals, South Africa- Silicon Alloys, and Other segments. Each segment contributes 24.03%, 13.06%, 25.69%, 19.66%, 9.50%, 0.63%, 4.46%, and 2.97%, respectively, to the company's total sales. The company's North America-Silicon Metal and North America-Silicon Alloys segments include the combination of the operating segments of Silicon Metals in the United States & Canada and Silicon Alloys in the United States & Canada. These operating segments have been combined because they have similar long-term economic features, competitive & operating risks, and political environments in the United States & Canada.

Financials

Solar energy plays a crucial role in the transition of the electricity sector and aims to achieve net-zero emissions by 2050. According to the International Energy Agency (IEA) , the solar industry accounts for over two-thirds of global net power capacity. I believe this portion can grow in the coming years as the need for renewable energy is rapidly increasing to reduce carbon emissions. In the US, the industry is estimated to install 200 GW of new solar power up to 2027, which is more capacity than has been deployed. In addition, the demand for electric vehicles is also rising rapidly as electric vehicles are the critical technology for decarbonizing road transport, which is responsible for 16% of world emissions. I believe the sale of electric vehicles can grow exponentially in the coming years as several governments are increasing their sales targets and commitment to the electrification of vehicles.

All the favorable long term growth factors in these two industries has created demand in the silicon industry in the long term, and I believe it can further exponentially grow as silicon is the most commonly utilized semiconductor in solar cells and is also used in the production of EVs. This growing long term demand has created ample opportunities for the participants in the industry. However, it has also induced intense competition among the participants.

Identifying these scenarios, Ferroglobe has planned to expand its quartz mine in Spain and has signed a letter of intent to acquire a new high-quality quartz mine. Quartz is the most essential raw material utilized in manufacturing high-purity silicon metal. I believe this expansion can act as a primary catalyst to boost its growth as it can significantly improve its ability to control its supply chain. As per my analysis, this expansion can help the company to gain a competitive advantage by lowering its dependency on third parties for raw materials. The company has finalized two multi-year energy contracts that will enable it access to 100% renewable energy at competitive prices. It expects these contracts to accelerate its production levels, which I believe can expand its profit margins in the coming years. The company has strong growth prospects in the long term. However, currently it is facing a low demand in the final market, which is also reflected in the latest quarterly result of the company.

US Solar PV Deployment Forecast (Website of Solar Industry Research Data)

{kind=link}

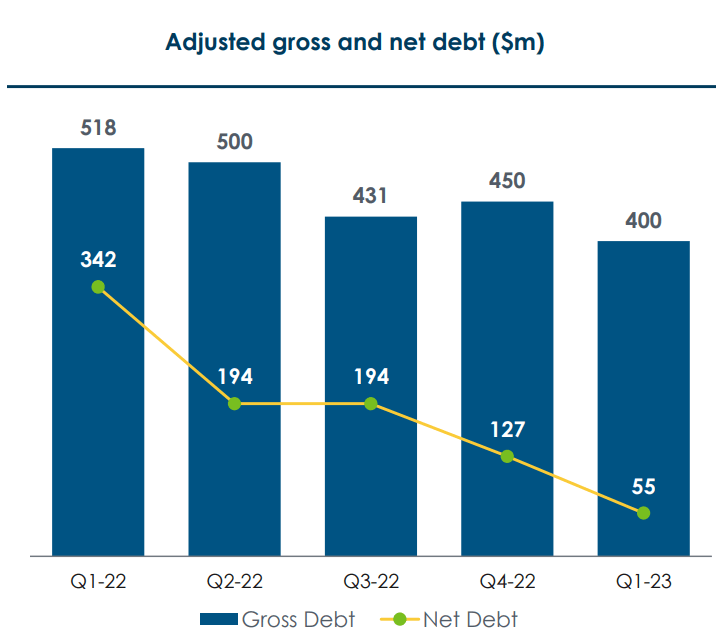

Ferroglobe recently reported its first-quarter results . It reported sales of $400.86 million, decrease of 43.95% compared to $715.26 million in Q1FY22. This decline was mainly driven by reduced volumes throughout its product portfolio and lower pricing in its primary products. Adjusted EBITDA stood at $44.76 million, compared to $241.11 million in Q1FY22. The company reported net income of $151.16 million, a decline of 86.11% YoY compared to $20.99 million in the same period last year. Reduced net income resulted in diluted EPS of $0.05, compared to $0.88 in the previous year. Net debt decreased to $55 million in Q1FY23, compared to $127 million in Q4FY22 and $342 million in Q1FY22. It ended its first quarter with $344 million in cash.

The results were impacted by the challenging macroeconomic environment, which caused a downturn in the sales volume. However, I believe the positive tailwinds in the industry and recent major expansions can help it recover in the next quarters. Ferroglobe has reiterated its full-year adjusted EBITDA target of $270 to $300 million. I believe these estimates are a bit high, and the company might decrease its guidance in the coming period as it is experiencing a slow demand throughout its product portfolio.

According to Seeking Alpha, Ferroglobe's revenue for FY2023 might be $1.84 billion. I think this revenue estimate perfectly captures the impact of the challenging macroeconomic environment. Therefore, I estimate the company's revenue to be $1.84 billion for FY2023. I am considering the EBITDA margin of FY2018 while calculating the EBITDA of FY2023, as I believe the last four years were significantly affected by the pandemic. The market is normalizing again, and I think the EBITDA margin of FY2018 is appropriate while calculating the EBITDA of FY2023. The EBITDA margin of 10% gives EBITDA of $184 million. I believe the company's net profit margin for FY2023 might be significantly higher than FY2018's net profit margin as it has dramatically reduced its debt in Q1FY23. Therefore, I estimate the company's net profit margin to be 5.5%, giving the EPS estimate of $0.54.

Adjusted Gross and Net Debt (Investor Presentation: Slide No:11)

{kind=link}

What is the Main Risk Faced by GSM?

One of the company's most important production components is electricity. Electricity prices are determined by the domestic jurisdiction and are affected by supply and demand dynamics. Electricity prices may be affected by changes in local energy policy, energy scarcity, climate conditions, contract termination or non-renewal, and other factors. If the electricity prices increase, it could negatively impact the company's cost of production and reduce its profit margins.

Valuation

As the solar energy and electric vehicle market is booming due to decarbonizing, it has created significant opportunities in the silicon industry. In addition, Ferroglobe is expanding its access to raw materials, which can help it to increase its production levels. These positive factors can push the stock upwards, and we can expect a long-term upside.

After considering all the above factors, I am estimating revenue of $1.84 billion and net profit margin of 5.5%, which gives the EPS estimate of $0.54 for FY2023. The EPS estimate of $0.54 gives the forward P/E ratio of 8.65x. After comparing the forward P/E ratio of 8.65x with the sector median of 13.12x, we can say the company is undervalued. In my opinion, it might gain significant momentum due to its recent expansion activities in Spain and long term growth prospect, which can help it to increase its production and help it to trade at its sector median P/E Ratio. Therefore, I estimate the company might trade at a P/E ratio of 13.12x, giving the target price of $7.08, a 51.9% upside compared to the current share price of $4.66.

Conclusion

I believe Ferroglobe can grow exponentially in the long term as the electric vehicle and solar industries are experiencing strong growth, which can ultimately increase demand in the silicon industry. In addition, the company's recent expansion activities can help it increase its production and cater to the increasing demand in the long term. It recently reported its first quarter results which were negatively affected by the challenging macroeconomic environment.

However, Ferroglobe is experiencing a slow demand in the short term, which is also reflected in its latest quarterly result. I estimate that the company can maintain the EBITDA margin of FY2018 as the last four years were significantly affected by the pandemic. The EBITDA margin of 10% gives the EBITDA estimate of $184 million. The company's net profit margin might be higher than in FY2018 as it has significantly reduced the debt. The net profit margin of 5.5% gives the EPS estimate of $0.54. Many analysts would find my estimate conservative. However, even with these estimates, the company is deeply undervalued, and all these tailwinds can push the stock upwards by 51.9%. After analyzing all the above factors, I assign a buy rating to Ferroglobe.

For further details see:

Ferroglobe: The Company Is Deeply Undervalued With Current Fundamentals