GSM - Ferroglobe: The Valuation Is Too Low To Ignore And Benefit From

2023-05-19 04:27:26 ET

Summary

- Ferroglobe PLC had a tough start to the year with revenues falling and EBITDA taking a 66% decrease compared to the year before.

- The market outlook seems strong; however, I think the relatively risk-free valuation of the company makes it very appealing.

- The company is prioritizing paying down debt to gain a better financial state, and paired with the strong margins, I think this is a buy right now.

Investment Summary

Ferroglobe PLC ( GSM ) is a prominent manufacturer of crucial raw materials such as silicon metal, silicon-based alloys, and manganese-based alloys, that are necessary for several industries like automotive, construction, and energy. The company boasts a diverse product portfolio, including ferrosilicon, silicon-based alloys, manganese-based alloys, and other specialty alloys, which is one of its main advantages.

{kind=link}

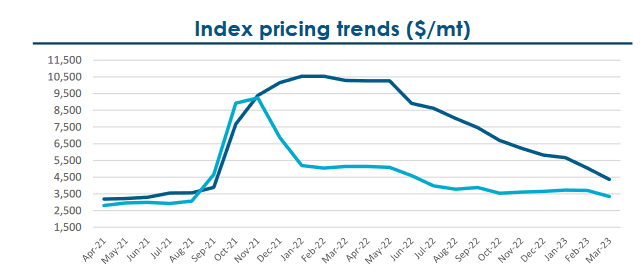

Prices seem to be going down as a result of a softer demand from the market which the company also noted in the last earnings report . The company managed to pay off 12.5% of the long-term debts in the quarter and increase the cash position by $20 million which I think highlights some of the resilience of the company. They are able to make meaningful advances even if the market is not what it used to be. The valuation paired with the strong margins makes it hard to pass up on GSM. I will be rating them a buy as I see the potential of a significant share appreciation here fueled by top-line growth translating into further investments to help in the future supply the demand for silicon metal.

Market Outlook

Much of the demand that GSM is seeing comes from the battery and solar market where the silicon metal they provide is widely used. The market on its own is expected to see a CAGR of around 5.8% between 2022 and 2030 which should be seen in the top-line revenues for GSM too.

{kind=link}

The trend of companies moving back manufacturing to the US will help benefit GSM quite a lot as the proximity of themselves to these potential customers should be a significant benefit. It helps cut down on shipping length and there should be fewer interruptions in the supply chain as a result. Where GSM is ensuring investors they are still viable is the increase in margins despite an estimation of lower revenues and EBITDA for 2023. EPS was $0.11 per share in the first quarter, representing $25 million in net income and a 267% QoQ growth. For the year 2023, the EBITDA guidance is between $270 - 300 million. It's far off from the nearly $800 million generated in 2022 thanks to the much more favorable commodity prices seen. Looking on the bright side, GSM is still doubling its EBITDA from 2021, which is no small feat in my book.

Risks

The most prominent risk with GSM might be the share dilution over the last few years. Of course, the volatility of the market has made the earnings reports for the company inconsistent but the long-trend seems certain in that the market will continue growing as a result of the adoption of solar panels , but a number of other tailwinds too, like EV manufacturing increasing.

Back to the dilution, this is often a common move by newer companies yet to establish strong cash flows. But with GSM they already have a 19% FCF margin which brings to question why the dilution is even necessary. A more organic growth in the business I think would be better, where they take the cash they are generating for investments, and not hurt the investors in the company. It should be said dilution isn't that extreme, only up around 10% since 2020. In the coming quarters, I will be looking at this primarily when risk assessing, as I want a potential long-term position in the company not to be hurt by this.

Financials

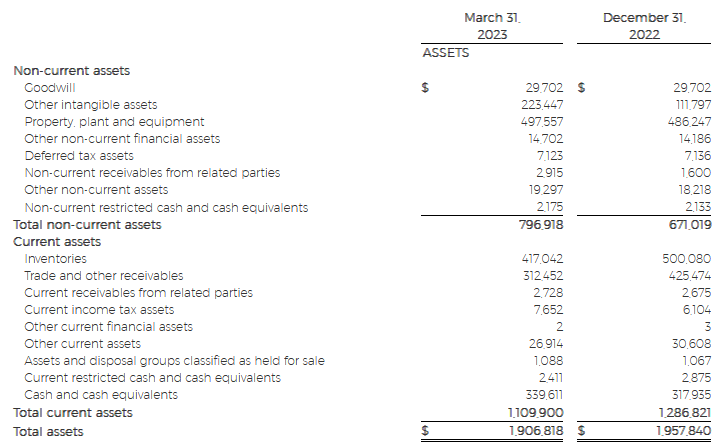

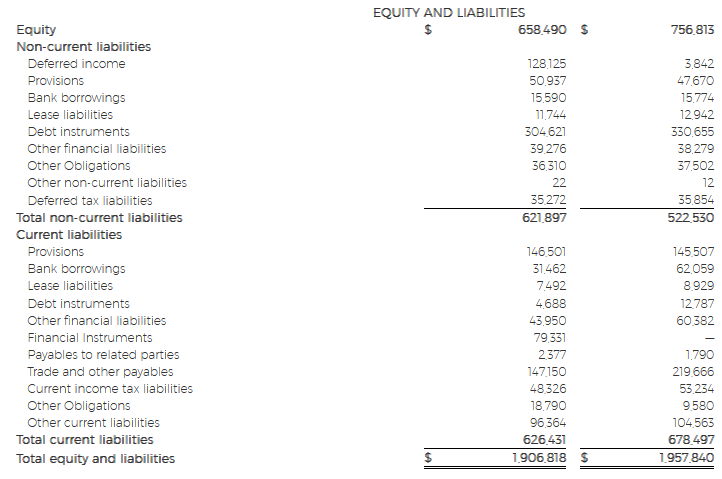

Moving over to the financials I have already praised the company for some of the moves they made in the first quarter to the start of 2023. They paid 12.5% of the gross debts, or around $50 million compared to the quarter previously. The company was also able to increase the cash position by $20 million which makes me very hopeful in their ability to continue investing in the future to help fuel growth. The already strong and established cash flow margins will be the main driver behind the growth of the company in my opinion.

{kind=link}

{kind=link}

The company sits a very solid asset/liabilities ratio of 1.52 right now and has been able to achieve a ROA of over 16% as a result of its strong investment strategy so far, primarily investing and acquiring quartz mines as noted in the last report. The finalization of a 2-year contract with Spain and the expansion of one mine here should help the company continue growth and I don't think the balance sheet will be of any hindrance. With a net debt/EBITDA sitting at just 0.42 using the 2023 guidance the company provided. I think this goes to show the stability of the company currently and the potential they have to continue investing aggressively to gain market share.

Valuation & Wrap Up

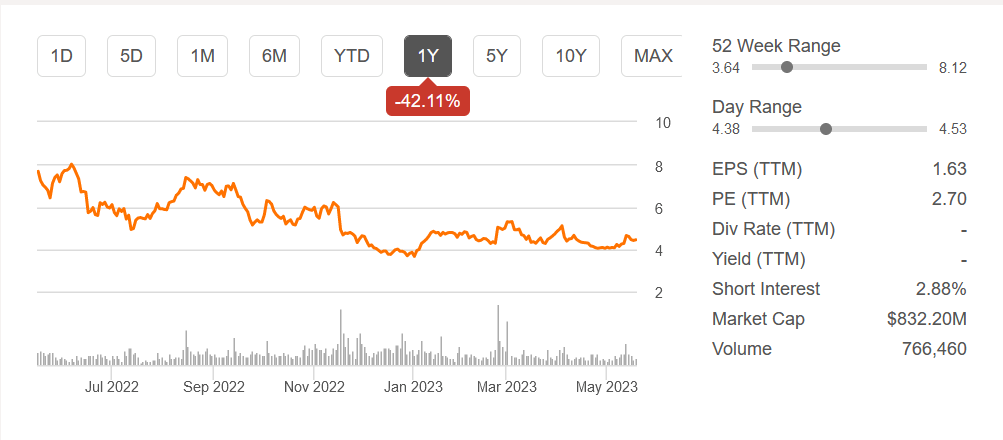

Right now the valuation of GSM seems too good to be true. Looking at the future estimates the 2026 numbers suggest the company would have a p/e of under 4 with 32% You growth in the EPS. This type of valuation brings little downside in my opinion. It's a play for the long term as the adoption of solar and EVs for example will take time. But GSM is setting itself up for the long-term with the investments they are currently making, like acquiring quartz mines to help secure supplies to satisfy the market demand.

{kind=link}

The volumes seemed to have peaked in late 2021 for the company and the trend points downwards currently but I believe that is just the nature of the commodity industry that they are in. The long-term remains strong. I will be rating GSM a buy because of the stable balance sheet they have, the strategic investments they are making so far, but also the solid margins they have been able to establish and still improve upon.

For further details see:

Ferroglobe: The Valuation Is Too Low To Ignore And Benefit From