FQVTF - Fevertree Drinks: Still Expensive After A Sharp Price Decline

2024-01-15 23:46:23 ET

Summary

- Fevertree Drinks saw an expectedly sharp price decline in the past half-year as its market multiples became unsustainable.

- The company's weakening performance and reduced guidance further kept it firmly on the downward slide. Even now, the trough is unlikely to have been reached.

- Still, FQVTF has a strong position and past financial history. If its outlook for FY24 is realistic but positive, it can still be one for the portfolio.

When I last wrote about the UK-based mixer-drinks company Fevertree Drinks (FQVTF), the lack of upside to the stock was obvious. While there was still a case for it in the medium term, prompting a Hold rating on it, it was clear that any investor who bought the stock in the past year would do well to sell it.

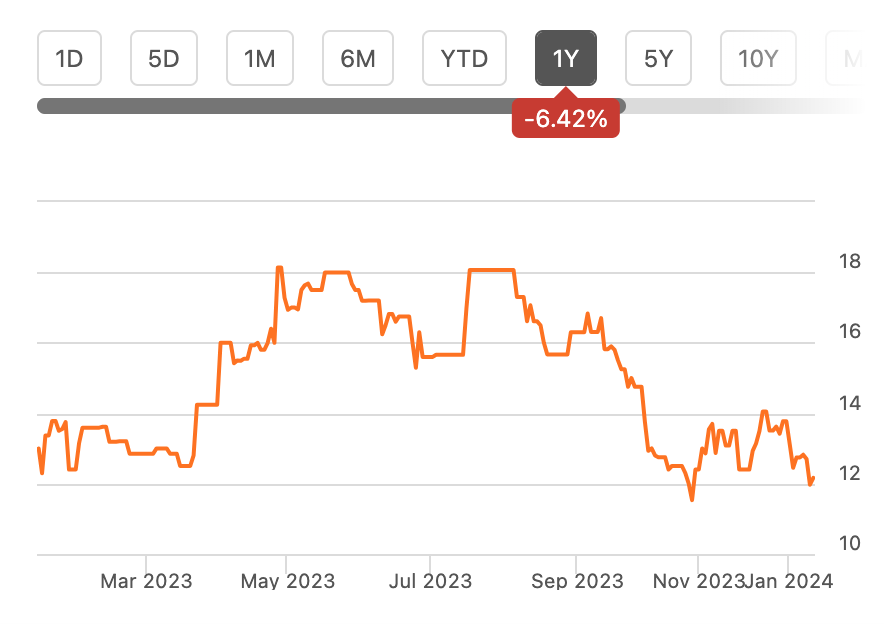

That has come to pass, with its price taking a nosedive, with a 37% fall since. Even though the decline over the past year isn't the worst at 6.4% (see chart below), the gyrations in the past year are glaring. For context, in July it had made 46% year-to-date [YTD] gains.

Here I discuss whether the extent of price decline is warranted and whether there's a possibility of an uptick anytime soon.

Price Chart (Source: Seeking Alpha)

{kind=link}

Why has the price fallen?

The company's interim results released in September, showed reduced financial performance and impacted the outlook for the remainder of the year. This of course was enough reason to trigger investor pessimism, and this is evident in the price movements since. But the stock had started declining even before this.

High market valuation

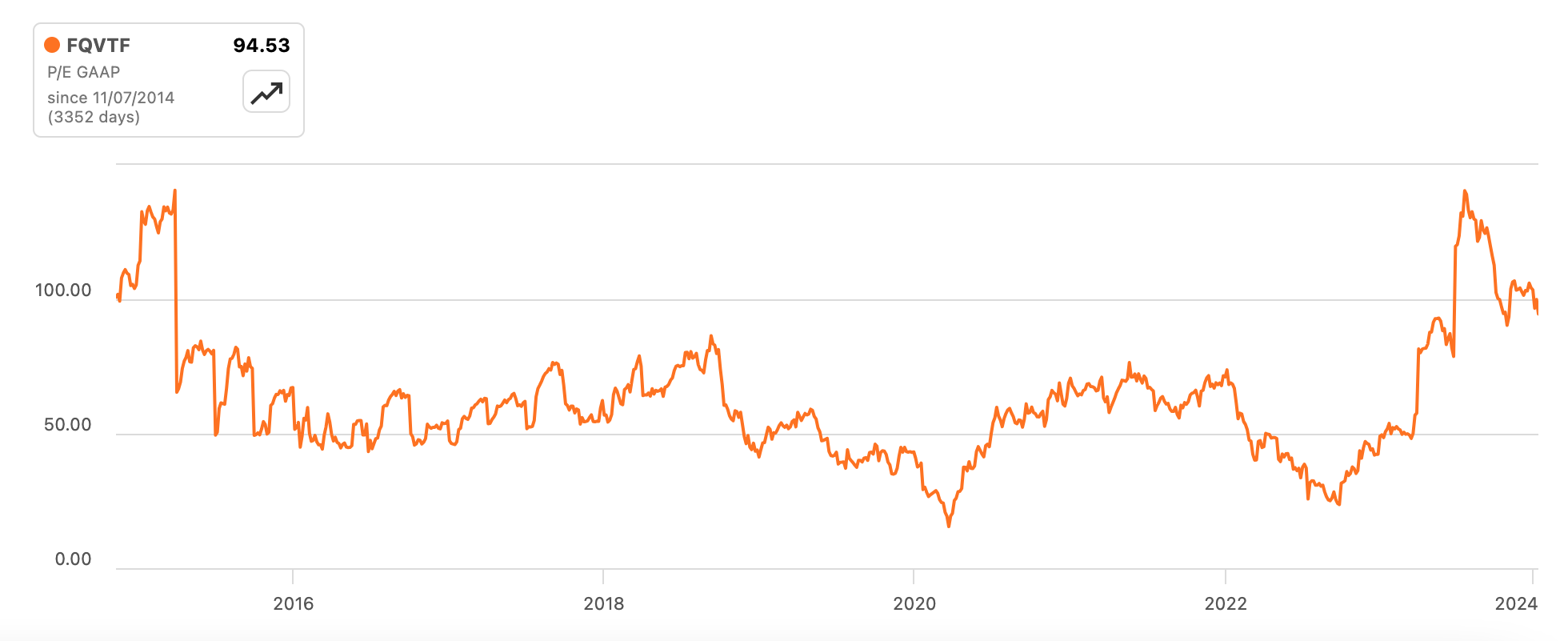

This brings me to the first reason for the price decline. The higher price-to-earnings (P/E) ratio. By the end of July, the stock was trading at a GAAP trailing twelve months [TTM] P/E of over 140x, which is the highest in the past decade, except in March 2015, when it was at around the same level.

Much like in 2015, the stock saw a sharp tumble after considering that it had gotten ahead of itself. The median P/E ratio for the stock is already at a high 51x on average for the past five years but was close to three times even this level. This fact was already glaring when I wrote about it.

Long-term P/E ratio (Source: Seeking Alpha)

{kind=link}

Reduced guidance

There could have still been room for a pickup in the stock if the company's guidance was sustained or upped. Instead, Fevertree Drinks' reduced guidance only fueled the price fall. Specifically, here's what the company now expects:

- As I had pointed out the last time, the revenue guidance was a stretch. Indeed, the company has reduced its expectations, with the number now expected to rise by 11.8% year-on-year (YoY) at the midpoint of the guidance range compared to the 15% projected earlier. Not only did its 11% growth in FY22 indicate otherwise, but continued macroeconomic weakness in its biggest market, the UK, made the likelihood of reaching the target doubtful. Specifically, the UK food and beverage services GDP had contracted by 1.1% in May 2023, indicating strain on the sector Fevertree Drinks functions in.

- The shocker, however, is the adjusted EBITDA, which is now expected to decline by ~17% at the midpoint of the guidance range from the 1.8% fall expected as per the initial guidance. I had hoped for an improved outlook on the profit number going by declining inflation, which in turn could soften cost increases as it has for other companies.

Slower revenue growth and a shrinking adjusted EBITDA for the full year FY23 at a time when the P/E was already high, was yet another sign why the price needed to correct more.

Worse than expected profits

The reduced guidance was based on weaker performance in the first half of the year (H1 FY23) as revenue growth slowed to 9.1% YoY (H1 FY22: 14%). This could still be acceptable at a time of relatively soft demand, but a 92% decline in net profit is a little too hard to digest.

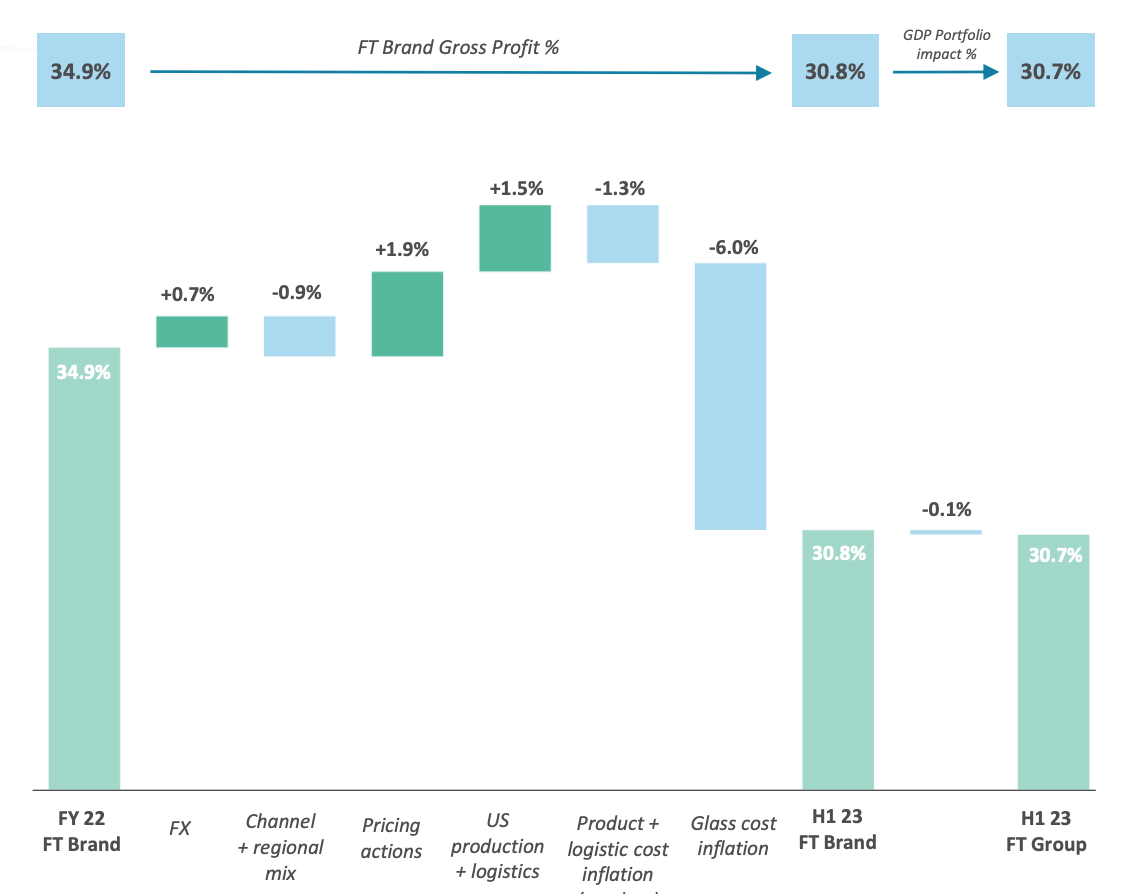

Consider this. The company points to two key reasons for slowing margins. The first is the price of glass, which is a big input for it. If it weren't for supporting factors like pricing, US production logistics and currency trends, glass price inflation alone would have reduced gross profit margin by 6 percentage points (see chart below).

Factors Impacting The Gross Margin (Source: Fevertree Drinks)

{kind=link}

It also mentions an exceptional cost on account of an inventory buyback of GBP 3.3 million as it changed its distribution model in Australia, which affected the operating income.

Now, let's assume for a second that neither the glass prices nor the inventory buyback costs were factored in. In fact, let's assume that the gross profit margin came in at 34.9%, the same as that for the full year FY22. This would make the actual gross profits higher by GBP 7.5 million and along with the addition of the buyback costs, the net income would come to GBP 11.9 million. Even this is a 15.7% YoY reduction in profit, driven by slowing revenue growth and higher operating expenses.

What's next for the price?

We have already witnessed a decline in price as a result of the above numbers. But the key question now is, has the stock declined enough or is it still too high? All said and done, Fevertree Drinks is still growing at a decent rate and is still profitable, albeit not as much as one would hope.

Dividend cut possible

The declining profits do make the stock vulnerable to a dividend cut though, even though as of H1 FY23, the company increased dividends by 2%YoY. This is because of the unsustainable dividend payout ratio. It was already relatively high at 75.5% as of FY22, it's now at 4x. The possibility is also reflected in the forward dividend yield of 1.15% compared to the TTM ratio of 1.67%. While the dividends are hardly the most rewarding feature of the Fevertree Drinks stock, a cut can still impact the price at the margin.

Weak earnings, high market multiples

Further, even after the sharp price correction already witnessed, the stock's TTM P/E is still higher at 93.8x compared to the long-term average of 61x. The forward P/E doesn't look encouraging either.

To estimate it, I've calculated net profit for FY23 in two ways with the following assumptions:

- The adjusted EBITDA comes in at USD 33 million, as per the midpoint of the revised guidance for both estimates

- For the first estimate, the net profit to adjusted EBITDA ratio remains at its low of 10.8% as seen in H1 FY22.

- For the second estimate, the net profit to adjusted EBITDA ratio is expected to improve. In H2, it's assumed to be at 62.7%, the level seen in FY22. This results in a 46.7% ratio for FY23.

In the first estimate, the net income figure comes to GBP 3.6 million or USD 4.5 million, resulting in an exceptionally high forward P/E of 315.5x. In the second estimate, the net profit comes to GBP 15.4 million or USD 19.6 million. The forward P/E is commensurately much lower at 72.4x. But going by the historical TTM figure, it's still quite high. This indicates that the stock can fall by another 40% now.

How to approach the Fevertree Drinks stock now

With a fair bit of downside to the stock even now, the short-term position still remains one to Sell. However, even for the medium term, I'm less confident now despite the company's position as a leading mixer drink provider with a growing US market.

One reason is the weak macro economy, which can particularly impact cyclical businesses like hospitality, and in turn, impact the company. With the US now as its biggest market, there's a risk of a slowdown impacting its revenues there in 2024 as well. Additionally, its costs remain elevated even as inflation overall is on the decline. It has taken steps to curb its glass costs with a contract that is expected to improve the current trend.

Next, even though it's hopeful for FY24, expecting an adjusted EBITDA margin of 15% compared to the 8.75% now seen for FY23, I have less faith in its projections now. This is even more so since the net earnings would have seen an appreciable decline even if it weren't for the outlier cost increases.

Still, there's something to be said for being among the leaders in its category, and its 12.1% CAGR for revenues over the past five years. Its income has been affected during the pandemic and has also fluctuated over the past decade, there's something to be said for the 15x rise between 2014 and 2022. Also, if the guidance hadn't been as high as it was earlier and neither were the market multiples, the latest results wouldn't have affected the stocks as much.

I think much hinges on the company's outlook for FY24. If it looks achievable, especially if the net income can be estimated to grow, it would imply that Fevertree Drinks can bounce back from its recent troubles. Until then I'd Hold.

For further details see:

Fevertree Drinks: Still Expensive After A Sharp Price Decline