FQVTF - Fevertree Drinks: The Curse Of High Expectations

2023-07-22 01:25:24 ET

Summary

- Fevertree has rallied strongly this year, largely the result of a re-rated multiple.

- Earnings are most likely headed higher this year, but the recovery path isn’t straightforward.

- Ultimately, there’s a lot of optimism priced in at ~60x P/E, and investors will need to be mindful of market expectations.

Fevertree ( FQVTF ), the leading UK-based premium mixer brand (think the tonic water that partners premium spirits), could be in some trouble heading into the rest of the year. The last trading statement issued by management, ahead of its annual general meeting, noted an upbeat start to the year, led by solid performances across key growth markets like the US. But for the most part, the core UK market remains a source of uncertainty, particularly in light of the current cost-of-living crisis. Management hasn’t left too much buffer on the cost side either in its reaffirmed full-year EBITDA guidance range of GBP36-42m, while the big payout last year (including a GBP50m special dividend) has narrowed the runway significantly.

Long-term, there is clearly growth potential as the company expands beyond the UK, but I wonder if the market has assigned too much credit at the current ~60x P/E valuation. In sum, Fevertree Drinks is working against some very lofty expectations despite the macro headwinds; in my view, the risk/reward heading into this month’s trading update skews very much to the downside.

Top-Line Buoyed by the ‘Next Wave’ but ‘Stronghold’ UK Market Remains a Concern

The last investor communication from Fevertree ahead of this month’s H1 trading update was management’s AGM update, citing strong top-line numbers in the first full year of post-COVID normalization. To a large extent, the release focused on Fevertree’s growth markets (i.e., its ‘Next Wave’ geographies comprising North America, Germany, France, and Australia, among others), where growth has been categorically strong - no doubt helped by the brand’s extensive investments in marketing and distribution. In tandem, management has reaffirmed the full-year guidance (first outlined in March) of revenues between GBP390-405m and EBITDA between GBP36-42m.

The key uncertainty, though, remains the revenue path of the ‘stronghold’ UK business, coming off an underwhelming last year. To reaccelerate growth here, management is implementing strategic changes, including new product variants and expansion into the premium adult soft drink market. So far, so good, as management noted strong momentum in the UK on-trade channel (i.e., on-premise), the largest revenue contributor pre-COVID. Off-trade (i.e., off-premise consumption) momentum, however, has lagged, though current guidance calls for momentum here to build later in the year.

Yet, amid the ongoing UK cost of living crisis, discretionary spending is likely first on the chopping block, and Fevertree’s premium offerings, which retail significantly above the mid-market (Schweppes) and lower-end (supermarket own brand), is at real risk of being traded down. Hence, Fevertree’s top-line guide may well be at risk of a UK-led downward revision sooner rather than later.

Post-COVID Margins Will Recover, but Return to Pre-COVID Levels is Far from a Given

Through the pandemic-impacted years, Fevertree margins came under significant pressure from supply chain disruptions and on the raw material front. While these ‘transitory’ headwinds are undoubtedly fading this year, recent port strikes in North America threaten to derail the near-term margin recovery path – note the subsequent move higher in freight rates (albeit still well below the COVID-driven peak). Also pressuring the P&L are persistent glass bottle shortages , as well as the increased cost of doing business from the nationwide UK strikes.

Given Fevertree’s high fixed cost base, these pressures entail operating deleverage, particularly if you also incorporate potential pricing headwinds from trade-down risk outside of the UK (note many of its European ‘next wave’ markets are also going through a cost-of-living crisis). So while a return to pre-COVID levels would imply massive EPS upside (high-20% operating margin vs. ~7% currently), the path to getting there isn’t straightforward; I would be very cautious about underwriting anything more than a gradual margin recovery.

Big Distributions at the Expense of the Cash Runway

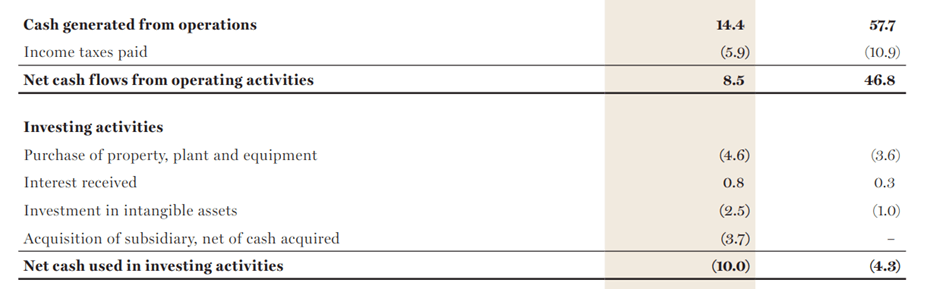

Per the 2022 annual report (released in conjunction with the AGM), cash levels are now down to ~GBP95m (from GBP166m previously) due to dividend payouts over the course of the year. Most of the distribution came from a massive GBP50m special, in addition to an ~GBP19m ordinary dividend (adding up to GBP69m). By comparison, net earnings for the year were ~GBP25m – barely enough to cover the ordinary. With the company also free cash negative last year, the distribution seems ill-advised. Even normalizing for the one-off GBP3.7m acquisition outlay for US-based mixer brand Powell & Mahoney , there isn’t a lot of cash flow to cover for the dividend.

{kind=link}

To be fair, Fevertree is likely on track for a stronger 2023 from a cash flow perspective (unlikely enough to cover the dividend, though), But this needs to be weighed against the additional cash commitments - management plans to allocate capital to accelerate its expansion in ‘next wave’ markets like the US this year. This will only add to the cash burn. Hence, getting a payoff on its US-related growth investments will be crucial to not only driving a profit recovery but also funding the capital return commitment; any disappointments here could result in a surprise dividend cut.

The Curse of High Expectations

Fevertree has been on a tear this year, far outpacing the broader FTSE index on hopes of a big earnings boost. The positive post-AGM trading update has only fanned the flames of expectation, with management highlighting solid performances across the board. But the bar is high heading into the H1 update later this month, where investors will finally get some insight into Fevertree’s performance through the key summer months. Embedded in the full-year EBITDA target range of GBP36-42m is a swift reversal of the margin declines seen through the supply chain and raw material impacts of last year, along with UK resilience (despite the 'sticky' inflationary pressures this year).

And judging by the earnings multiple (~60x P/E ), the market appears to have extrapolated this near-term optimism into the long-term as well. So while there is admittedly positive momentum here, the equity risk/reward isn’t great for a company nowhere close to generating the growth needed to justify its valuation. Pending a meaningful reset, I much prefer sitting on the sidelines.

For further details see:

Fevertree Drinks: The Curse Of High Expectations