FQVTF - Fevertree Drinks: Valuation Is Too High With Execution Risks

2023-04-18 12:03:40 ET

Summary

- Margins are becoming more crucial than the US growth opportunity for the equity story.

- The current valuation is too high, suggesting that a lot of expectation is embedded in FQVTF's growth potential.

- A neutral stance is appropriate for the time being until either valuation decreases significantly or earnings surge dramatically.

Thesis

Fevertree Drinks PLC ( FQVTF ) is a beverage company. The Company produces soft drinks and mixers. FQVTF occupies a unique position in the premium mixers market and has significant opportunities for long-term growth, particularly in the US. The more lucrative UK market has shown signs of weakness, but FEVR's top line has been gaining steam thanks to new capacity expansion in the US. However, profit warnings have been issued due to margin pressures, indicating that there are concerns about margin delivery and profitability. With downtrading possibly putting pressure on demand at the premium end of the market and on-trade frequency likely to decrease, as well as cost inflation pressures, FY23 is not likely to provide much relief. Moreover, the valuation is not cheap across various measures, with EV/fwd EBITDA at 32x and fwd PE at 50+x. To become an attractive long, either valuation needs to decrease significantly, or earnings need to surge dramatically. Therefore, for the time being, a neutral stance is appropriate.

4Q22 results

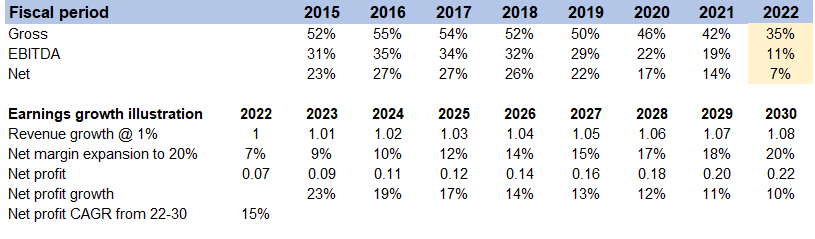

The most important thing I've learned from the most recent results is that FQVTF is nearing the margin inflection point. For the equity story, I now see margins as more crucial than the US growth opportunity. To put this in perspective, EBITDA margins have dropped from a peak of 35% to just 10% in FY22, leaving a massive "room" for expansion or normalization and a compelling story for equity buyers. While top-line growth is still critical to the equity story and FQVTF valuation, reversion of margins ahead (depressed from commodity pressures and logistics in 2022 and 2023) will be a key driver of earnings and the investment case. Below I provided an illustration of what I mean by margin is now the key driver. Suppose revenue were to only grow at 1% until 2030 and net margin were to revert back to 20% (700bps below peak), net income can grow at a CAGR of 15% easily. While execution is key to this margin expansion, it is not an impossible feat. My illustration expects a linear progression of margin expansion which is unlikely the case as I expect continued margin pressures into 2023. In 2023, decreased gross margin is likely due to increased glass costs. However, I anticipate margin expansion to resume in 2024 and beyond as glass pressures ease and production is brought fully onshore in the US. As a result, I am not in favor of going long at the present time from the standpoint of timing of margin expansion.

Management's forecast of continued margin contraction in FY23 is consistent with my own analysis. The £36 million to £42 million forecast for EBITDA in FY23 remains unchanged, indicating an EBITDA margin of 9.2 to 10.4% and a margin decline of 100 to 200bps year over year due primarily to the effect of higher European energy prices on glass. Management also expects significant inflation for important materials, but they plan to partially counteract this with measures such as adjusting prices, increasing local production in the US, and implementing cost-saving strategies.

{kind=link}

Cost impact on margin

I estimate that the price of glass constitutes about a quarter of total raw material costs. In 2022, the company was unable to meet consumer demand because of rising costs and limited supplies of glass. The unhedged exposure to rising gas prices was hit hard last year, despite the fact that roughly 70% of glass costs were hedged. The company probably incurred higher H2 glass surcharges as a result of this. Consequently, I anticipate that the knowledge gained by management in FY22 will convince them to increase their hedging in FY23, mitigating the cost impact from glass even further.

As for the logistics costs in the United States, I believe that the company had to import product from Europe because US production lines ran below the expected roll-out, making the company dependent on certain key routes, the costs of which have increased significantly over the past year. Although international freight rates normalized in H2, they stayed high for the UK-US route. Margin is also further negatively affected by the fact that the management is facing a shortage of personnel to unload products from ships, and when the congestion eases, there is also a lack of drivers and warehouse space to handle the increased demand. Combined, I think these dynamics have had a negative effect on margins, which is an issue with execution. What this also means is that there is a way out of the problem and the margins can return to normal.

Valuation

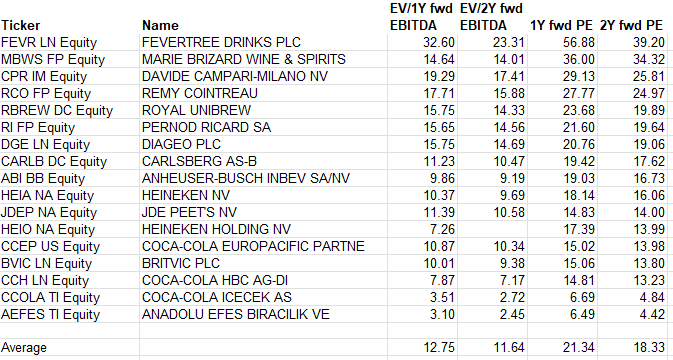

In order to give a better sense of how high FQVTF valuation is, I did a simple screen to compare across other beverage players in the EU. While the earnings growth story for FQVTF is attractive and does deserve a premium in valuation, I believe the current valuation (even on a 2Y forward basis) is too high (more than 2x the average). This tell me that a lot of expectation is embedded that FQVTF will grow earnings rapidly, which if it does not, the floor to valuation re-rating downwards can be more than 2x (back to peer’s average).

{kind=link}

Conclusion

FQVTF position in the premium mixers market presents significant opportunities for long-term growth, particularly in the US. The company's recent 4Q22 results suggest that margins are becoming more crucial than the US growth opportunity for the equity story. However, the current valuation is too high, suggesting that a lot of expectation is embedded in FQVTF's growth potential, and therefore a neutral stance is appropriate for the time being until either valuation decreases significantly or earnings surge dramatically.

For further details see:

Fevertree Drinks: Valuation Is Too High With Execution Risks