FQVTF - FeverTree: Quality Business But Not Today

2023-04-21 06:12:10 ET

Summary

- FeverTree Drinks PLC is a British company that specializes in the development and supply of premium mixer drinks.

- FeverTree has grown revenue at a rate of 36%, as it expands overseas and benefits from industry tailwinds.

- The company has suffered from margins tightening as its production costs spiral. Profitability today is not attractive but there is a route to returning to prior levels.

- Beverage businesses are highly attractive and show that FeverTree can consistently achieve its historical margins.

- FeverTree's valuation upside is not enough given the risks around margins. Long term, it is highly attractive and likely a takeover target.

Company description

FeverTree Drinks PLC ( FQVTF ) is a British company that specializes in the development and supply of premium mixer drinks such as Indian tonic water, ginger beer, and cola distillers. The company operates globally and sells its products to pubs, bars, and restaurants. Its products are sold under the brand name Fever-Tree.

Share price

FeverTree's share price has seen a mixed performance. Between the listing and its all-time high, the share price gained over 2,200%. Since then, shareholders have lost over 50% of their value. The initial gain and underlying interest in the business have been driven by its rapid growth of the business.

Financial analysis

FeverTree Financials (TIkr Terminal)

{kind=link}

Presented above is FeverTree's financials for the last decade. The company has been able to grow quickly and is now moving toward a mature profitability profile.

Revenue

Revenue has grown at an impressive CAGR of 36%, with strong double-digit growth achieved up until 2018, following which things have softened.

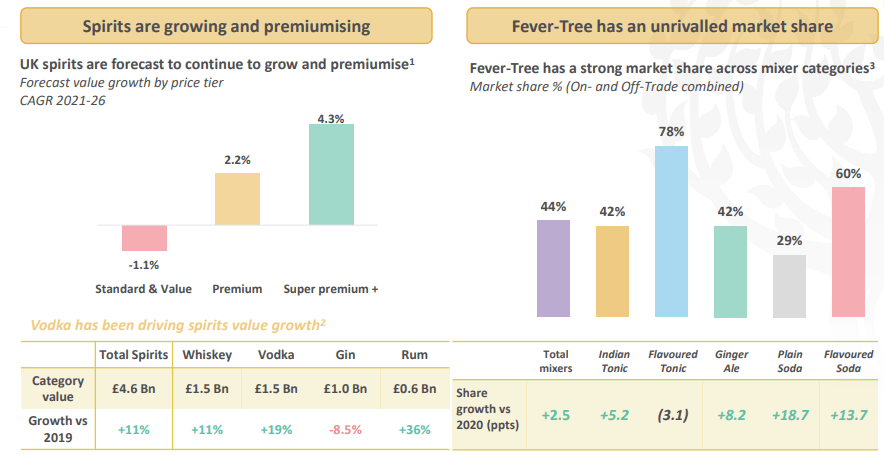

With greater choice and product understanding, consumers have been more selective about their choice of drinks, contributing to an increase in demand for premium and craft spirits. This trend has driven the growth of the mixer drinks market, as consumers seek high-quality mixers to complement their premium spirits. This has been part of a "premiumization" trend in the beverage industry as a whole, as consumers are willing to pay a premium for high-quality and premium products. This is the segment in which FeverTree specializes, allowing the business to ride the trend. As the following shows, this is not short-term but is forecast to continue into 2026, with FeverTree positioned well due to its diversified product offering. From our analysis of other beverage businesses, this "premiumization" is better considered a structural change rather than a trend, placing FeverTree in the front seat for revenue outperformance.

Spirit premiumization (FeverTree)

{kind=link}

Another trend driving revenue is the rise of a cocktail culture that has led to a surge in demand for high-quality mixers. Consumers are looking for unique cocktail experiences with paying the price of high-end establishments. FeverTree's vast offering has allowed the business to be a one-stop-shop for these products, importantly having the flavor to match.

Cocktail (FeverTree)

Direct-to-consumer [DTC] online sales have become an important distribution channel for beverage businesses as it allows them to improve their margins, while also creating a direct relationship with their end user. Businesses that have been better at this are the new ones born in the social media era, as they have achieved their growth by speaking directly to the end user. FeverTree is no exception to this, operating a popular e-commerce store.

FeverTree has done a fantastic job becoming the leading premium mixer provider in the UK and has leveraged its fundamental product superiority to expand overseas. The US now represents 28% of revenue, while growing at strong double-digits across all products.

US Growth (FeverTree)

The European expansion has come later but the results are the same, FeverTree is gaining market share quickly.

EU (FeverTree)

This is a reflection of the fundamental quality of the products FeverTree produces but more importantly for us, quells any concerns that the business with remain constrained by the size of the UK market. With continued expansion on the horizon, strong growth is likely. It should be highlighted that this creates greater FX risk.

Economic conditions could pose short-term headwinds. Inflationary pressures are reducing consumers' discretionary income, contributing to a decline in spending across many sectors. Social spending is one of those industries impacted as its an expense that can be foregone. Excluding the year of the pandemic, FY22 was the second slowest year in growth, suggesting the company is already feeling the impact of this.

Margins

FeverTree has seen a rapid tightening of margins across the historical period, declining 12ppts. Much of this occurred in the last year, losing 6%. FeverTree has suffered massively with inflation, as energy, glass, and freight prices bite. As the business is not a large-scale global producer, it has found itself overly exposed with an inability to mitigate the impacts. Management has guided further struggles in FY23, before seeing subsequent improvements. Our view is that this is an issue but it's difficult to blame anyone as it does not look like something Management could have mitigated. The key will be how Management is forecasting to improve margins, which we will touch on in the outlook section of this report.

S&A expenses have also seen a rapid expansion, growing at a rate of 38% across the historical period. Our view is that this is actually quite good. The reason for this is that it reflects the ongoing overseas expansion, both marketing and otherwise, as well as improving brand awareness in the UK. The business is still small in the beverage world and so will need to continually invest in improving reach.

These factors contribute to an EBITDA margin of 11%. This is not a good level for a premium beverage business and is reflected in the company's underperformance again historical levels. The company should be aiming for mid-to-high 20s, which it has shown it can achieve. Hypothetically, if these short-term inflationary headwinds are just that, our view is that FeverTree's financials are quite attractive.

Balance sheet

FeverTree's declining margins are reflected in its efficiency metrics, which were at highly attractive levels between 2015-2018. The company certainly has the ability to return here.

The idea of slowing demand is reflected in the company's inventory turnover, which has declined in the most recent period and remains below the levels achieved before Covid-19.

FeverTree is well financed, operating with little debt. Management has been careful with its cash allocation, initiating a soft dividend in recent years.

Outlook

FeverTree Outlook (Tikr Terminal)

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are guiding continued revenue growth, although at a lower level of 8%. With businesses growing at 10%+, analysts tend to be more conservative in their view, seeking continual evidence before increasing their long-term view. We can see the coming years at a 10-15% rate across a cycle based on the commercial superiority of the business thus far.

Analysts' margin guidance is a noticeable improvement on current levels but far below that historically achieved by the business. At an EBITDA margin of 13-16%, the company remains 10-15% below our target level. Again, a degree of this will be conservatism from analysts but primarily reflects their discussions with Management and opinion.

Management's margin improvement initiative includes the following:

- 5% Price increases globally.

- Producing US products in the US rather than importing from the UK.

- Improving glass supply chain to gain economies of scale. 80% of the sales mix is glass, a commodity that has seen inflationary pressures (44%+ Y/Y glass bottle cost increase).

- Expanding production overseas for other geographies.

- Other operational improvements and subsiding of inflationary pressures.

We have conducted a back-of-the-napkin calculation of what we think these factors are worth:

Potential margin improvements (Author's calculations)

Our view suggests FeverTree can reach an attractive level in the next 5 years but is weighted heavily toward gaining operationally in the US and finding operational improvements, likely through an inflationary reversion. The prudent view would be to await some evidence of these factors playing out.

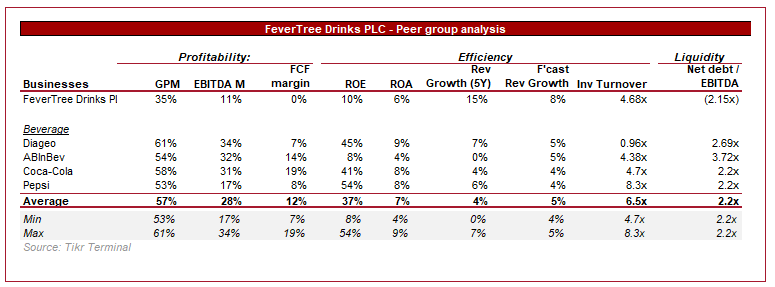

Peer comparison

Peer comparison Beverage (TIkr Terminal)

{kind=link}

Presented above is the performance of a cohort of Beverage businesses. The purpose of displaying this is not to compare FeverTree, as we know the company is currently underperforming its normalized level. Instead, it is a benchmark for where FeverTree could reach.

The peers look concentrated around an EBITDA margin of 30%, with only PepsiCo (PEP) underperforming this. ROE is high and growth is strong for what is a mature industry. Management's margin improvement plan looks to return FeverTree to this level but the company will lack the scale economies of the other companies, which makes it a little less plausible.

Valuation

Valuation (Tikr Terminal)

Presented above is the valuation of these businesses, with FeverTree trading at 38x its current EBITDA. This is not surprising as investors generally price in aggressive multiple contractions via growth and so price today aggressively for what is a profitable future. Importantly, this table tells us the business can normalize as c.18x if margins return wholly.

To assess FeverTree's valuation, we have conducted a DCF valuation based on our view of how margins will play out. We will not assign a view on likelihood, instead assume they occur in the year they do and see what the upside is. This allows the reader to make their own judgment as to whether the upside available presents a risk-to-reward ratio they are comfortable with.

To summarize our views on the business and our assumptions:

- Revenue growth of c.10% in the medium term, with a perpetual growth rate of 3%.

- Margin improvement as per the table above.

- An exit multiple of 18x and a discount rate of 11%.

Based on this, we derive an upside of 11%. At this level, the risk does not look worth it.

Takeover target

What is an interesting idea is FeverTree being an acquisition target. The company's only problem is production issues, which any of the 4 businesses above could solve in a heartbeat. This would allow the business to immediately see its margins return to its prior heights while supporting growth. From the buyers' perspective, they get a business which worse case might be slightly dilutive in margins but highly accretive in growth. For Diageo (DEO), it could be a fantastic complement to its current brand portfolio. With the synergies and commercial value present, FeverTree would easily sell in excess of its current market cap, which has upside on a standalone basis.

Final thoughts

We are fans of FeverTree. It is a high-growth business built on a quality commercial foundation. The market looks strong and is facing natural tailwinds. The Company's profitability profile has shown itself to be attractive and we see the route back to these levels, the issue is of course in execution. FeverTree's valuation does suggest some upside but our view would be caution until evidence suggests margin will improve. It is unlikely that the share price will run away until then.

For further details see:

FeverTree: Quality Business But Not Today