ETV - FFA: An Interesting Play In The Call Writing Space

- FFA utilizes a call writing strategy split between index writing and covered calls.

- The fund has only one distribution cut in its history and has what I believe is a reasonable ~7% distribution rate on its NAV.

- The fund's current valuation makes it a tempting alternative to ETV, a similar fund.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on July 29th, 2022.

First Trust Enhanced Equity Income Fund ( FFA ) is a covered call fund that I had run across a year ago. Since taking an initial look at the fund , it has provided some solid results relative to the broader market. Though, at that time, I didn't have a strong opinion in one way or another on the fund.

FFA Performance (Seeking Alpha)

I compared it to the more popular option-based Eaton Vance Tax-Managed Buy-Write Opportunities Fund ( ETV ). ETV writes options against indexes, whereas FFA utilizes index writing options and individual positions. For tax purposes, it doesn't have the same track record of regular return of capital either. For some investors, that's one of the sole reasons to own ETV for the generally non-destructive ROC the fund produces.

In that article, I had noted that FFA was actually the outperforming fund. Since that posting, however, ETV has slipped ahead in terms of performance. It was only marginal on a total NAV return basis in the course of around a year and a half. Admittedly, a rather arbitrary timeframe since it's going back to February 22nd, 2021.

Ycharts

One thing that should be noted is that ETV's total share price performance has been beating FFA by an even wider margin. For investors looking at relative value, I believe that FFA is worth looking at while at a nearly 4% discount when ETV is at a nearly 12% premium. Even on a relative discount/premium basis, FFA is looking like the more attractive call writing fund at this point in terms of valuation.

For those holding for the tax advantages that ETV typically provides via ROC distributions, then a switch probably doesn't make sense.

The Basics

- 1-Year Z-score: -2.04

- Discount: -3.85%

- Distribution Yield: 7.30%

- Expense Ratio: 1.12%

- Leverage: N/A

- Managed Assets: $358.6 million

- Structure: Perpetual

FFA's objective is to "provide a high level of current income and gains and, to a lesser extent, capital appreciation." It attempts to do this by investing in "a diversified portfolio of equity securities." So we are looking at a rather simple portfolio. It then utilizes an option strategy "on an ongoing and consistent basis... on a portion of the Fund's Managed Assets."

The fund is smaller, which can provide some issues for investors with larger portfolios that want to take a large position immediately. However, for most retail clients, the volume should still be sufficient. Additionally, the fund isn't leveraged. In a rising interest rate environment, that can be beneficial. Despite being smaller, the fund's expense ratio is still rather reasonable in the CEF space.

Performance - Attractive Discount

Often during times of volatility, we can see CEF discounts widening out. ETV definitely bucked that trend and has actually recently expanded its premium quite materially. On the other hand, FFA has held its own but has slipped to a minor discount after flirting with a premium. As we can see in the chart below, the divergence in valuation here is primarily what is catching my attention on FFA again.

Ycharts

Even if ETV can outperform in the next year and a half to a slight degree, it isn't likely to pay off for shareholders if the valuation comes back down. FFA's one-year z-score of -2.04 is attractive. That can be compared with ETV coming in at a one-year z-score of 3.66.

Over the past five years, FFA's discount is around its average of 3.49%. ETV's average comes to around a 3.95% premium. Which does mean that ETV is elevated over its longer-term historical average.

Longer term, FFA is still outperforming too. That isn't guaranteed to be the case going forward. However, as I highlighted in my original piece, one reason for this is that FFA is not being overwritten as aggressively as ETV in terms of their options. ETV writes against a nearly 100% notional value of its portfolio. FFA utilizes covered calls and index writing closer to the 50% mark. The latest figure is coming in at 53.32%.

Ycharts

The reason that a reduced overwrite policy can outperform is that there is less "drag" on the portfolio when markets are running higher. Positions aren't being called away, limiting the upside, and index writing isn't producing losses for the portfolio if less is overwritten.

That makes ETV slightly more defensive and could be why, on a YTD basis, ETV is marginally outperforming.

Ycharts

Distribution - Steady And Reasonable

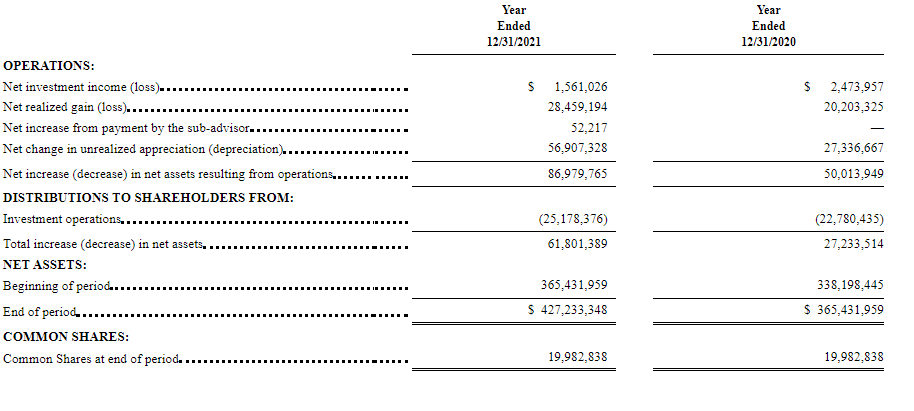

As an equity fund, they will require capital gains to fund their distribution. Due to the overwrite strategy, that's one source of gains that can come even during a down year as we've been experiencing for the markets. Last year the options written resulted in total realized losses of around $600k. Even for a small fund, that wasn't too sizeable and was more than offset by over $29 million in realized gains.

A loss on a call writing strategy can happen when closing a position at a loss, not to have a stock called away. An additional way is that options written on an index are cash-settled. In theory, the losses could be infinite as the index can rise forever. The actual underlying portfolio holdings then offset these losses. If an index is rising, its constituents that make up the said index are also rising.

Now that stocks have been declining more broadly, I suspect they should have contributed to gains when we see the next report.

The fund reported NII coverage of around 6.20% in the prior year. That was a decline from the coverage in the year prior as NII came down and total distributions went up.

FFA Annual Report (First Trust)

{kind=link}

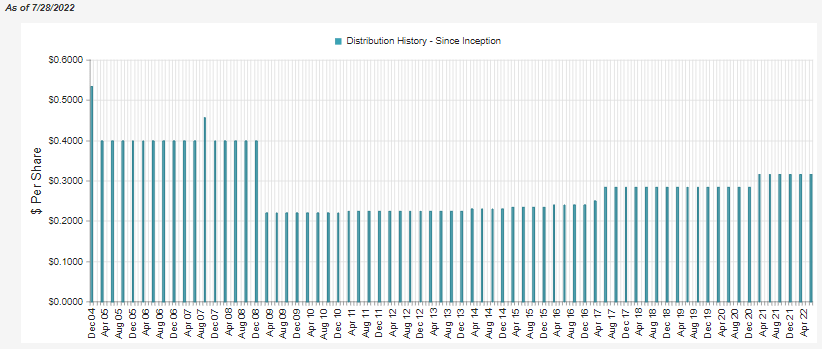

That might be concerning at first, but based on the current quarterly distribution of $0.315, that works out to a distribution yield of 7.30%. On an NAV basis, that comes to a reasonable 7.02% distribution. At these levels, I wouldn't anticipate that they would need to cut at all. In fact, this fund only cut once in 2008.

FFA Distribution History (CEFConnect)

{kind=link}

For the distribution classifications, we can see that most distributions were long-term capital gains for both prior years. Ordinary income was also listed, but nearly 80% of that was considered qualified for 2021 . So these are still relatively tax-friendly tax classifications for an investor. However, it might not be as good as the ROC classification that can defer tax obligations.

FFA Tax Character (First Trust)

{kind=link}

FFA's Portfolio

The portfolio turnover isn't too aggressive. They last reported a 14% rate. However, that was the lowest in the last five years, with 2018 showing a high of 45%. Relatively speaking, this is even more active than ETV, but it isn't uncommon to see a low turnover rate for call writing funds. They focus more on initiating those options positions rather than moving their portfolio too much.

One of the reasons for this is that they have to mirror the indexes somewhat that they are writing against to hedge properly. As I mentioned, index options are cash-settled. If they don't hold a basket of positions that are more or less aligned with what the index might do, they could lose both their options strategy and the underlying portfolio.

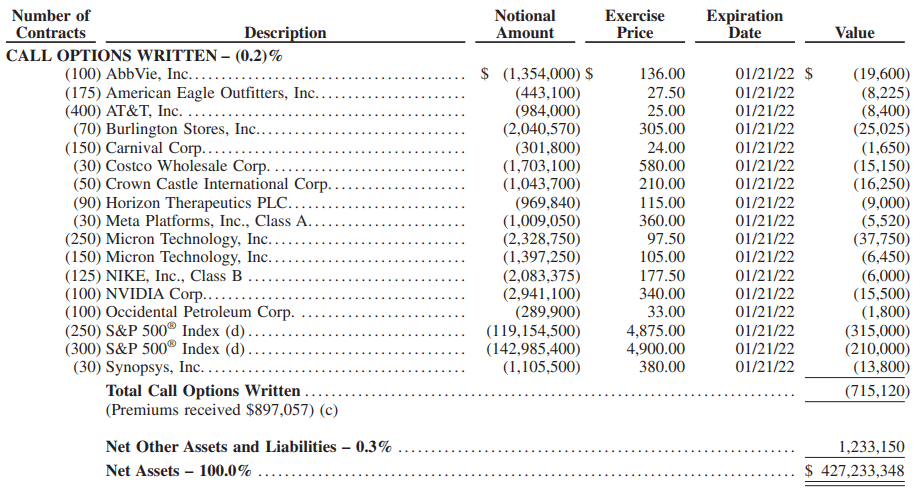

Below is how they were sitting with their options at the end of 2021. These have all expired by now and have probably changed drastically. That being said, it can still provide us with a clue of how they are positioned. While utilizing covered calls, they also have a sizeable allocation dedicated to the S&P 500 Index options.

FFA Call Options Written 2021 (First Trust)

{kind=link}

Naturally, since the S&P 500 is overweight tech, FFA is overweight tech. For those interested, ETV benchmarks against the S&P 500 and the Nasdaq 100. At the end of 2021, ETV had a 36.8% weighting. So they can go even more heavily into tech weightings to properly hedge their options strategy. Below is the sector weighting for FFA as of the end of June.

FFA Sector Weighting (First Trust)

That type of weighting and those familiar with the S&P 500 can probably guess most of their top positions.

FFA Top Ten (First Trust)

If you said Microsoft ( MSFT ), Apple ( AAPL ) and Alphabet ( GOOG ) (GOOGL) were going to be amongst the top, you'd be absolutely correct. One of the only ones that we are missing at the top is Amazon ( AMZN ). Interestingly, even when we looked last year, AMZN wasn't in one of the top positions for the fund.

If you go back through their previous reports, they haven't owned AMZN anytime recently either. Yet, it shows up in their reports when they are discussing performance as being a primary result of why they are detracting from the broader benchmarks. Here's what they had to say in their June 30th, 2018, semi-annual report .

Within the portfolio, the largest detractor to relative performance was the Consumer Discretionary group with stock selection within the group responsible for most of the underperformance. Holdings in Carnival Corp. (-12.40%), Lions Gate Entertainment (-27.67%) and Comcast Corp. (-18.53%), as well as not owning Amazon.com (+45.35%) and Netflix, Inc. (+103.91%) were the culprits.

That being said, MSFT, AAPL and GOOG have certainly provided them with some positive results over the last few years. NVIDIA ( NVDA ) and UnitedHealth Group ( UNH ) would have also provided some solid results for the fund over the last few years. AbbVie ( ABBV ) would have also contributed more, but it was a more recent addition to the portfolio. It first appeared in 2021.

Ycharts

In total, the fund carries just 63 positions at the end of June. The average market cap comes to a monstrous $533.86 billion. Of course, those mega-cap tech names would greatly boost that sizeable market cap average.

Conclusion

FFA is a fairly attractive fund at this time based on its valuation. The split between the index and covered call writing is fairly interesting. It allows them a bit more flexibility, but with flexibility comes responsibility. This can lead to taking advantage of opportunities, but they could also make the wrong move. Over the longer term, it seems to have resulted in outperformance against ETV. ETV is a fund that I generally tend to consider the "gold standard" in terms of CEF writing funds.

Based on today's valuation, one could potentially consider swapping ETV for FFA to wait for ETV to come back down from its elevated premium. On the other hand, FFA hasn't provided the type of regular ROC that ETV has for its investors. That would be a serious consideration to weigh for one's own individual situation.

For further details see:

FFA: An Interesting Play In The Call Writing Space