FFC - FFC: A High-Yielding Fixed-Income Fund With A Huge Discount

2023-09-10 11:09:28 ET

Summary

- Flaherty & Crumrine Preferred and Income Securities Fund offers a high level of income with a 7.35% yield, higher than most other options in the market.

- The fund's shares have declined 19.11% over the past year, underperforming domestic indices.

- The fund's leverage and allocation to the banking sector may pose risks, but it is trading at an 11.75% discount to its net asset value.

- The fund could continue to underperform if interest rates continue to increase, which is likely in the near term.

- The current distribution is probably sustainable going forward.

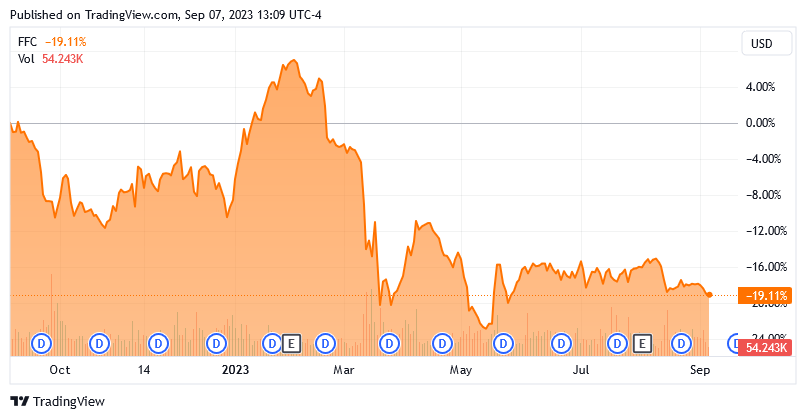

The Flaherty & Crumrine Preferred and Income Securities Fund ( FFC ) is a fairly popular closed-end fund that many investors are using to obtain a high level of income from their assets. The fund is reasonably good at providing such an income, as its 7.35% yield is higher than most other things in the market. It is also one of the few securities outside of the traditional energy space that actually boasts a positive real yield. Unfortunately, the fund’s shares have not been performing very well in the market as they have declined a whopping 19.11% over the past twelve months:

{kind=link}

While we have seen weakness across many market sectors since the start of 2022, this is a worse performance than just about any domestic index. That is something that will probably prove to be disheartening to many investors. However, this poor performance may have also created an opportunity. In my last article on this fund, I pointed out that the shares were trading at a price that was below their intrinsic value back in April. This discount has increased since then, and in fact, the fund’s shares appear to be offering a very attractive value proposition right now. As such, it could be worth revisiting this fund in order to determine whether or not buying the shares makes sense today.

About The Fund

According to the fund’s webpage , the Flaherty & Crumrine Preferred and Income Securities Fund has the objective of providing its investors with as high a level of income as possible without taking on excessive risk of loss. This is a very common objective for a fixed-income fund, which the name of the fund would imply. The fund’s description of its strategy from the webpage reinforces this assumption:

“The fund’s investment objective is to provide its common shareholders with high current income consistent with the preservation of capital. Under normal market conditions, the fund invests at least 80% of its managed assets in a portfolio of preferred and other income-producing securities. Preferred and other income-producing securities may include, among other things, traditional preferred stock, trust preferred securities, hybrid securities that have characteristics of both equity and debt securities, contingent capital securities, subordinated debt, and senior debt.”

The fund’s asset allocation fits pretty well with this description of its strategy. As we can see here, 58.77% of the fund’s assets are currently invested in preferred stock with much of the remainder invested in bonds:

CEF Connect

As just stated, it is not particularly uncommon for fixed-income funds to include capital preservation as part of their objectives. In fact, as I have pointed out before, it is not possible to lose money on a bond if a fund holds it for its entire life unless the bond issuer defaults. This is because the bond will always pay out its face value at maturity, so unless the bond was purchased with a negative yield-to-maturity, the investor will always make something. Now, that does not mean that the investor is guaranteed to earn a positive real return, as there were a number of bonds issued over the past decade or so that had yields insufficient to cover recent inflation rates. However, investors still received a positive nominal return.

For the most part, it is the same with preferred stock. The difference is that preferred stock does not have a maturity date. However, preferred stock does still have a face value. This face value dictates the price that the issuing company has to pay if it wants to force you to sell the preferred stock. As long as you purchase the preferred stock for less than that price, you are likewise guaranteed not to lose money unless you willingly choose to sell the asset following a price decline. Basically, fixed-income securities are not like common stocks that can become permanently impaired by increasing competition or a change in the business environment. As long as the issuing entity remains solvent, you are guaranteed not to lose money unless you willingly choose to sell the fixed-income security at a loss.

When we consider the above and the fund’s stated objective of preserving its capital, we might assume that it does not sell the securities in its portfolio very often. This is certainly the case, as the fund only has an 8.00% annual turnover right now. That is a very low turnover even for a fixed-income fund and it might actually be the result of maturing bonds forcing the fund to buy new assets. In fact, the annual turnover of the iShares Core U.S. Aggregate Bond ETF ( AGG ) is 104.00% and the annual turnover of the iShares Preferred and Income Securities ETF ( PFF ) is 16.00% according to Morningstar, so that supports the overall idea that the Flaherty & Crumrine Preferred and Income Securities Fund is not engaging in more trading activity than it needs to because of security maturations and similar events. This is a positive thing as it should help to keep the fund’s trading expenses down.

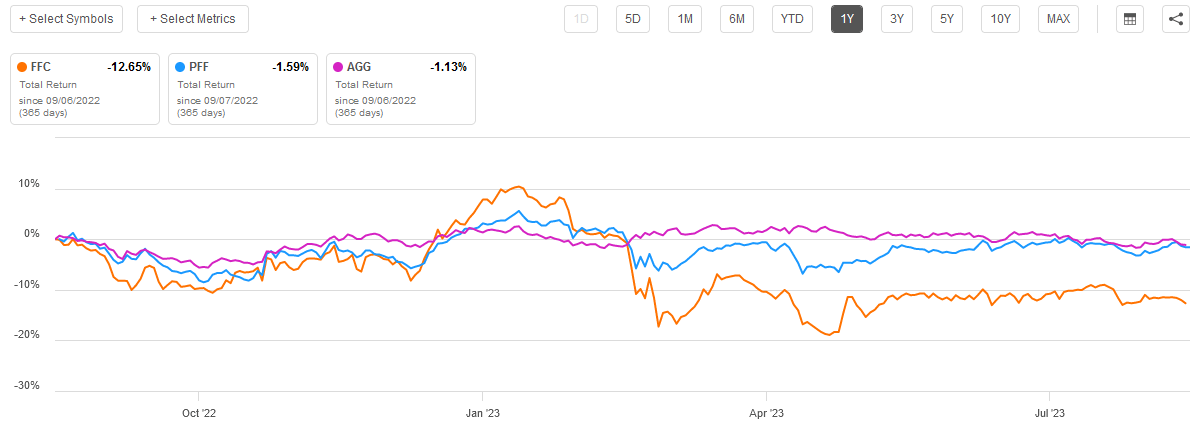

One criticism of closed-end funds is that they frequently underperform their industry benchmarks. This has been the case with this fund over the past year. This chart shows the total return of the Flaherty & Crumrine Preferred and Income Securities Fund against both the index exchange-traded funds that were just mentioned:

{kind=link}

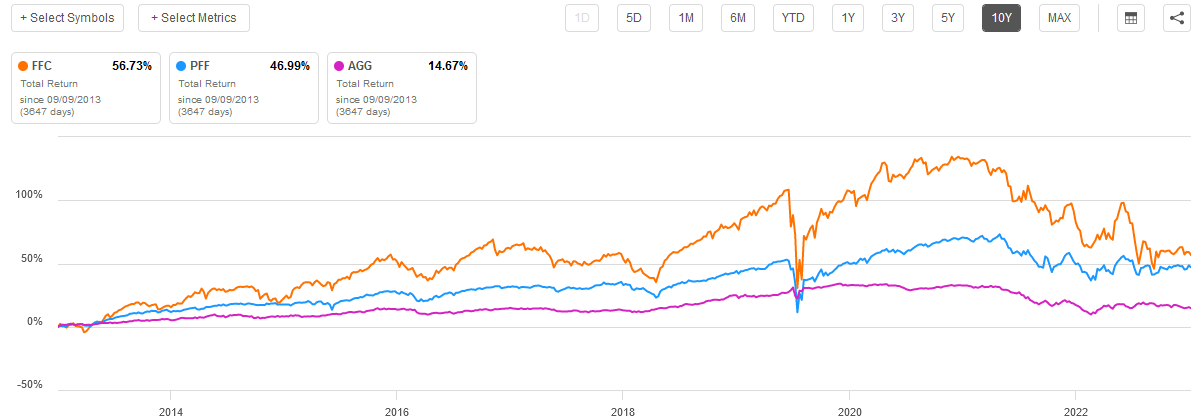

As we can see, the Flaherty & Crumrine Fund handed its investors a much greater loss than either of the two indices over the one-year period. However, this switches when we look at a longer period of time. For example, the closed-end fund substantially outperformed the index over the past ten years:

{kind=link}

This is due to a combination of the fund’s much higher yield than either of the indices and its use of leverage. We will discuss the fund’s leverage in more detail later, but in short, it will cause this fund to outperform during bull markets and decline much more than either index during a bear market.

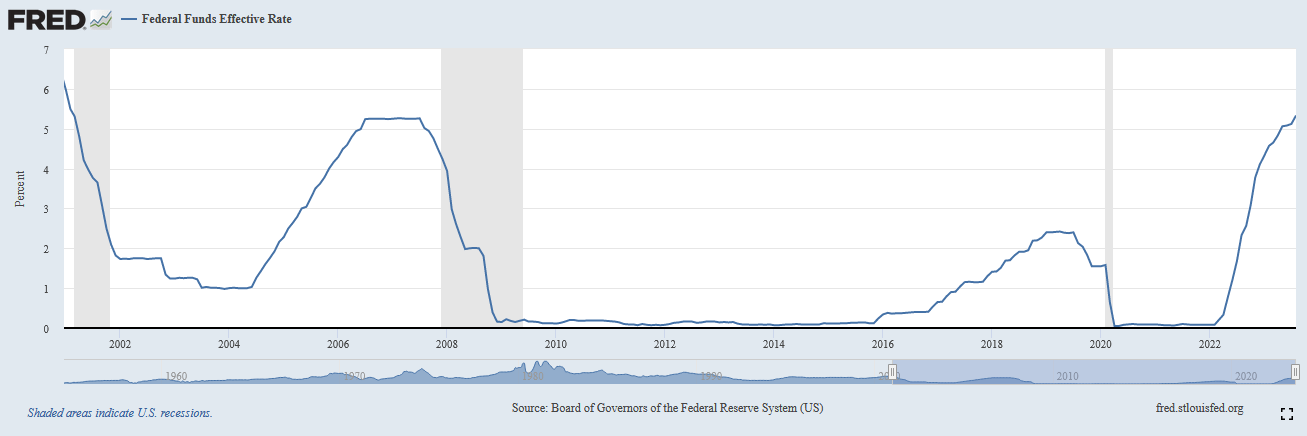

The big question right now is the direction of the fixed-income market, as that will have a significant effect on the ability of this fund to beat the indices going forward. This mostly depends on interest rates, since both bonds and preferred stocks move in the opposite direction to interest rates. The Federal Reserve has been very aggressively raising interest rates over the past eighteen months in an attempt to reduce the high level of inflation that has been devastating the American economy since the middle of 2021. As of the time of writing, the effective federal funds rate is 5.33%, which is the highest level that we have seen since the technology bubble in 2001:

{kind=link}

This is the reason why the fixed-income markets delivered a negative total return since the start of 2022 as the rising interest rates pushed down security prices by more than the yield of these securities.

Chairman Powell implied in his recent speech from Jackson Hole that the Federal Reserve may raise rates further as inflation still is not under control. However, it is uncertain whether or not inflation can be brought under control using monetary policy alone. Peter Schiff, CEO and chief global strategist of Euro Pacific Capital recently stated that inflation will not be brought under control unless the Federal Reserve continues to raise rates and the Federal Government cuts spending. If the Federal Reserve has to go alone, it will require much higher rates than we see now.

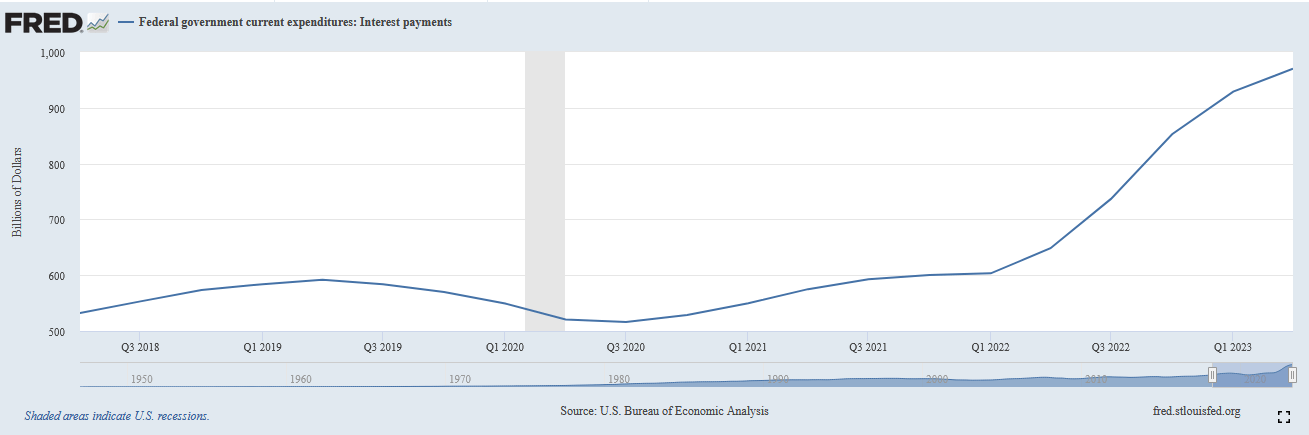

At the same time, the Federal Government’s deficits and the need to roll over debt are causing the government’s interest expenses to surge. The Federal Reserve currently states that the U.S. Federal Government is on track to spend $969.986 billion on debt service this year:

{kind=link}

That number is likely to increase fairly rapidly as the government rolls over the low-rate debt that was issued during the last fifteen years. In addition, spending on mandatory budget items like Social Security and Medicare will keep budget deficits elevated. The question is then how long the Federal Reserve can keep rates at levels close to today’s level without the nation having some sort of financial crisis? This may be the factor that dictates how long it will be until rates are cut and fixed-income securities, such as those held by this fund, begin to take off. For now, though, the Federal Reserve is stating that rates will remain elevated until inflation is crushed. That could take quite some time due to the stimulative policies coming out of Washington, D.C. that are offsetting the monetary tightening policies of the Federal Reserve.

In my previous article on this fund, I pointed out that 54.00% of its assets were invested in bank stocks. The banking sector continues to be overrepresented in this fund today, but its weighting has actually increased since April:

Flaherty & Crumrine

As we can see, the fund has increased its allocation to the banking sector by eighty basis points in the past five months. This is something that may be concerning to more risk-averse investors when we consider that this year has been one of the worst in history in terms of bank failures in the United States. However, as I pointed out in a recent article , these securities are probably going to be reasonably safe. First of all, the Federal Reserve and the Federal Deposit Insurance Corporation have set up a number of special vehicles meant to protect the nation’s banking system against bank runs of the sort that led to the collapse of Silicon Valley Bank. The most important of these programs is the Federal Reserve’s Emergency Lending Program, which allows the nation’s banks to pledge their depreciated assets to the Federal Reserve as collateral for loans. This prevents the banks from having to sell things such as Treasury bonds at a loss in the market in the event of a bank run. In addition, we saw back in 2008 and 2009 that the Federal Government will frequently step in to save banks on the verge of collapse. As such, there probably is not too much that preferred stockholders of these entities need to worry about. If this were a real problem, preferred stock funds in general would not enjoy the general popularity that they do because the banking sector is by far the largest issuer of preferred stock in the market. Thus, every preferred stock fund has an outsized allocation to the banking sector.

Leverage

Earlier in this article, I stated that the leverage of the Flaherty & Crumrine Preferred and Income Securities Fund was a major reason for its performance differences relative to the index. I explained how this works in my previous article on this fund:

“Basically, the fund is borrowing money and using that borrowed money to purchase preferred stocks and other income-producing securities. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not employ too much debt as that would expose us to too much risk.”

The second paragraph in the above quote is particularly important when we consider this fund. As we saw earlier, the fund significantly underperformed the indices over the past year. This is because the leverage amplified the losses that the fund took when the market price of the securities declined following the interest rate increases. The reverse occurred over most of the preceding ten years. That was a period of time characterized by ultra-low interest rates and a strong bull market for preferred stock and fixed-income securities. The fund’s leverage amplified the gains that the fund experienced in this situation. The same will happen going forward, which is why we do not want this fund to be using too much leverage as it seems more likely that interest rates will go up than go down in the near future. Unfortunately, this fund currently has a leverage ratio of 40.89%, which is quite high for the current environment. The risks here may be more than most investors that are looking to avoid losses will want to assume.

Distribution Analysis

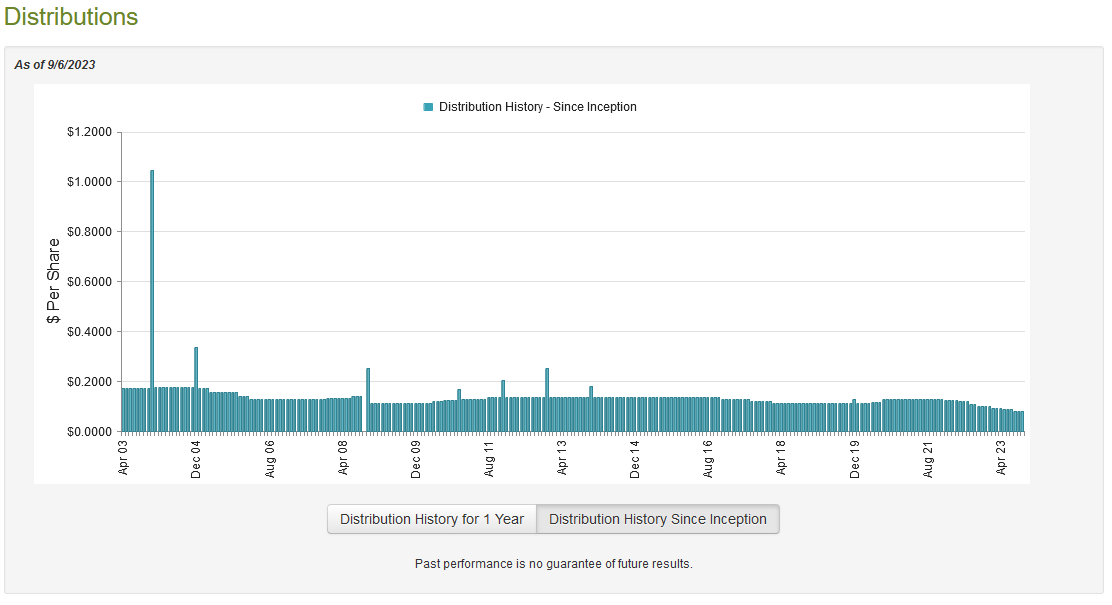

As mentioned earlier in this article, the primary objective of the Flaherty & Crumrine Preferred and Income Securities Fund is to provide its investors with a high level of current income. In order to achieve that objective, the fund invests its assets in preferred stocks and bonds that tend to deliver the majority of their investment returns via direct payments to the investors. The fund then applies a layer of leverage in an attempt to boost the effective yield of the portfolio beyond that of any of the underlying assets. As is the case with most closed-end funds, it then pays the majority of its investment profits out to the shareholders. As such, we can expect that the fund will boast a fairly high distribution yield itself. That is certainly the case as the fund pays a monthly distribution of $0.0815 per share ($0.978 per share annually), which gives it a 7.35% yield at the current share price. Unfortunately, this fund has not been particularly consistent with respect to the distribution over the years:

{kind=link}

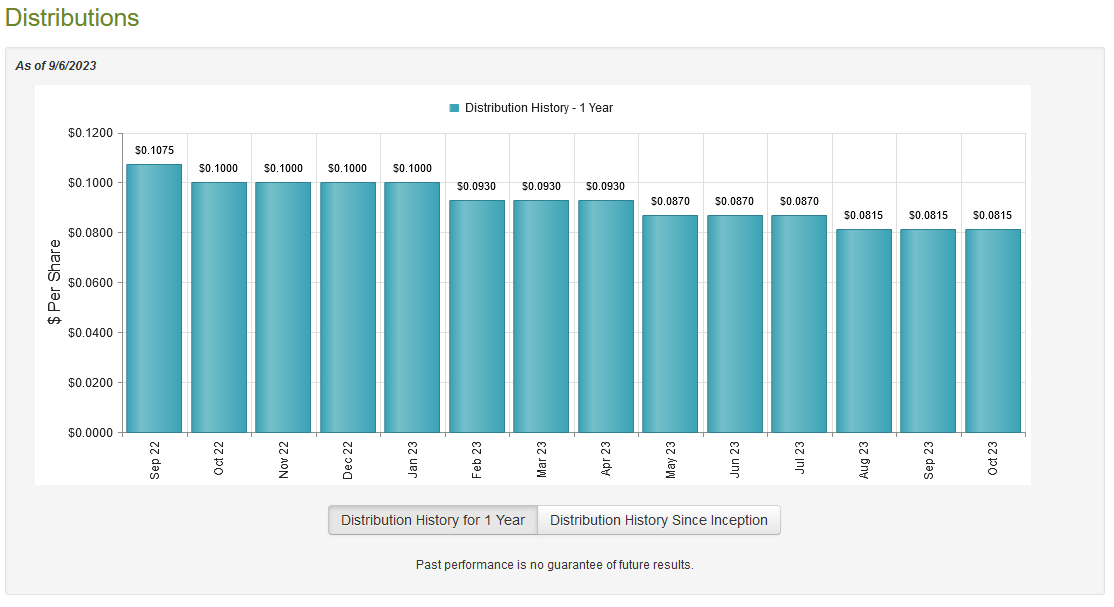

As we can clearly see, the fund’s distribution has generally varied quite a lot from period to period. In fact, the fund has cut its distribution four times over the past year alone:

{kind=link}

This is almost certainly going to reduce the appeal of this fund in the eyes of those investors who are seeking a safe and secure source of income that can be used to pay their bills or finance their lifestyles. This is a category of investor that would include many retirees, who are also among the people who are most likely to be interested in a fixed-income fund in the first place.

As I have mentioned before though, the fund’s past is not necessarily the most important thing to someone that is considering a purchase today. After all, anyone purchasing the fund today will receive the current distribution and current yield and will not really be impacted by the events of the past. The most important thing for these individuals is the fund’s ability to sustain its current distribution going forward. Let us investigate that.

Fortunately, we do have a very current document that we can consult for the purpose of our analysis. The fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is a much more recent report than the one that we had available to us the last time that we discussed this fund, which is nice as it gives us some insight into how well the fund was able to take advantage of the strong market during the first half of this year. It will also give us some insight into the causes of the fund’s distribution cuts over much of the period.

During the six-month period, the Flaherty & Crumrine Preferred and Income Securities Fund received a total of $16,005,597 in dividends and $26,355,024 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $42,488,060 during the period. It paid its expenses out of this amount, which left it with $25,107,930 available to shareholders. Unfortunately, this was not enough to cover the $27,251,961 that the fund paid out in distributions over the period, although it did manage to get very close. However, the fact that the fund was not able to fully cover its distributions out of net investment income is somewhat concerning at first glance.

Fortunately, a fund like this does have other methods that it can employ to obtain the money that it requires to cover its distributions. For example, it might have been able to earn capital gains that can be paid out to the shareholders. The fund, unfortunately, failed quite miserably at this task over the period. The Flaherty & Crumrine Preferred and Income Securities Fund reported net realized losses of $28,366,059 and had another $36,492,135 net unrealized losses during the period. Overall, the fund’s net assets declined by $65,550,648 after accounting for all inflows and outflows during the six-month period. This certainly explains why the fund kept cutting its distribution. It appears that it is attempting to bring the distribution in line with the net investment income. If it succeeds, that should make the distribution reasonably sustainable, particularly considering that this fund does not engage in very much trading. Unfortunately, we will have to wait until the next financial report is released to know for certain if it was successful, but the August distribution cut probably got it very close.

Valuation

As of September 6, 2023 (the most recent date for which data is available as of the time of writing), the Flaherty & Crumrine Preferred and Income Securities Fund has a net asset value of $15.06 per share but the shares currently trade for $13.29 per share. This gives the fund’s shares an 11.75% discount on the net asset value at the current price. This is a much larger discount than the fund had the last time that we discussed it and it is in fact more attractive than the 10.90% discount that the fund’s shares have had on average over the past month. As such, the price certainly appears to be reasonable today.

Conclusion

In conclusion, the Flaherty & Crumrine Preferred and Income Securities Fund boasts a fairly attractive yield that could appeal to income investors, although its recent performance leaves a lot to be desired. Unfortunately, the fund’s performance may continue to be somewhat weak in the near term as it seems likely that rising interest rates will weigh on its performance. The fund’s high leverage will be another drag on its performance in such an environment. Fortunately, the fund can probably sustain its distribution at the new level and it is trading at a large discount to the intrinsic value of the shares.

For further details see:

FFC: A High-Yielding Fixed-Income Fund With A Huge Discount