AGG - FFC: Better Yields Can Be Obtained Elsewhere

2023-11-15 09:59:06 ET

Summary

- Flaherty & Crumrine Preferred and Income Securities Fund yields 7.41%, lower than other preferred stock closed-end funds.

- The fund has experienced a recent price surge due to market expectations of the Federal Reserve cutting interest rates.

- The fund's performance has been lackluster but has outperformed the S&P 500 Index over the past two months.

- The market's expectations for interest rates may not pan out because of fiscal policy.

- The fund can probably cover its distribution at the current level and the valuation is reasonably attractive.

The Flaherty & Crumrine Preferred Securities Income Fund ( FFC ) is a closed-end fund that specializes in providing its investors with a very high level of current income. This is evident in the fact that this fund yields 7.41% at its current price, which is significantly higher than most American indices. However, this is nowhere near as impressive of a yield as it once was, as this fund’s yield does fail to match that of several other well-regarded preferred stock funds:

| Fund |

| Current Yield |

| Flaherty & Crumrine Preferred Securities Income Fund |

| 7.41% |

| Cohen & Steers Preferred & Income Fund ( PSF ) |

| 8.26% |

| John Hancock Preferred Income Fund ( HPI ) |

| 10.41% |

| First Trust Intermediate Duration Preferred & Income Fund ( FPF ) |

| 8.65% |

| Cohen & Steers Limited Duration Preferred & Income Fund ( LDP ) |

| 8.98% |

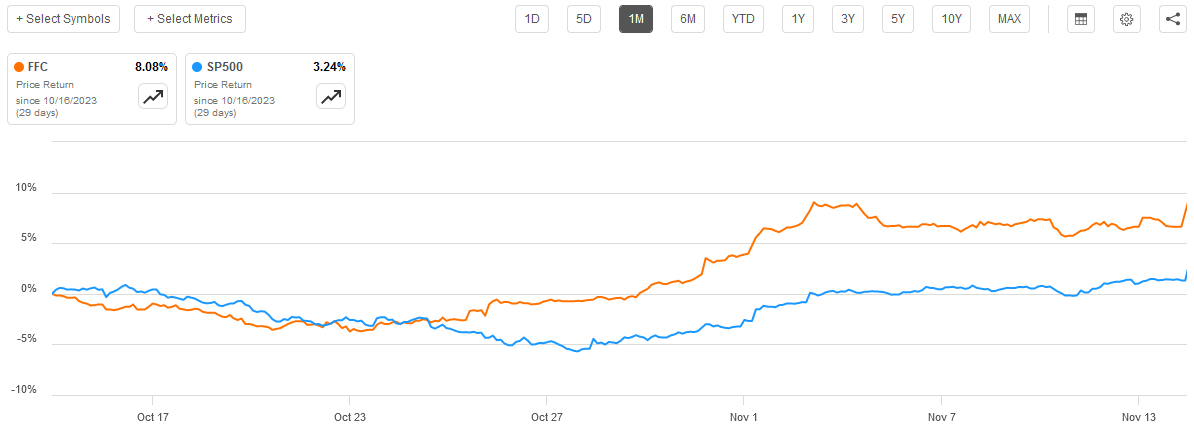

As such, this fund may be considered a second-tier choice by income-focused investors right now, despite its recent price surge. Over the past month, the Flaherty & Crumrine Preferred and Income Securities Fund has gained 8.08%, which is substantially more than the 3.24% gain of the S&P 500 Index ( SP500 ) over the same period:

{kind=link}

This steep increase is largely due to the market’s expectations that the Federal Reserve will shortly begin cutting interest rates. That would, of course, push up the value of the fixed-income securities that are held by this fund. However, there are some signs that interest rates may not be completely within the Federal Reserve’s control, as it would be very difficult for it to cut interest rates without unleashing inflation once again. This is due to the declining appeal of U.S. Treasury securities as a safe investment, which I discussed in an article on a related fund from Flaherty & Crumrine earlier this week.

As regular readers can no doubt recall, we last discussed this fund on September 10, 2023. That was a very challenging period for the market as it was characterized by rapidly rising yields as investors began to become accustomed to the very real possibility that high-interest rates may be with us for quite some time yet. As such, this fund’s performance since the date that the previous article was published has not been anything to write home about, although it has managed to outperform the S&P 500 Index over the period:

{kind=link}

When we consider the fund’s distribution, investors who purchased the shares of this fund on the date that my last article was published have been almost perfectly flat. The Flaherty & Crumrine Preferred and Income Securities Fund has had a total return of just 0.47% since September 10, 2023. While that is not particularly impressive, it is still a gain and thus is better than what many other assets have managed to deliver over the same period.

About The Fund

According to the fund’s website , the Flaherty & Crumrine Preferred and Income Securities Fund has the primary objective of providing its investors with a very high level of current income. This makes a lot of sense considering the fund’s investment strategy, which is described on its website:

Under normal market conditions, the Fund invests at least 80% of its Managed Assets in a portfolio of preferred and other income-producing securities. Preferred and other income-producing securities may include, among other things, traditional preferred stock, trust preferred securities, hybrid securities that have characteristics of both equity and debt securities, contingent capital securities, subordinated debt and senior debt. “Managed Assets” are the fund’s net assets, plus the principal amount of loans from financial institutions or debt securities issued by the Fund, the liquidation preference of preferred stock issued by the Fund, if any, and the proceeds of any reverse repurchase agreements entered into by the Fund.

Thus, this fund is basically a preferred stock fund, although its portfolio may include debt securities as well, should Flaherty & Crumrine believe that debt securities offer a better risk-reward trade-off at any given moment. We can see that the fund does not specifically state how it will balance its assets between preferred stock and debt, so that appears to be at the discretion of the fund’s management team.

Currently, the fund’s portfolio is more weighted to preferred securities than to debt:

CEF Connect

This makes a certain amount of sense from an income perspective. After all, preferred securities are junior to debt securities in a company’s capital stack so they should have a higher yield to compensate for the higher risk. As of the time of writing, the Bloomberg U.S. Aggregate Bond Index ( AGG ) has a thirty-day SEC yield of 4.76%, which is admittedly pretty terrible compared to money market funds. The ICE Exchange-Listed Preferred & Hybrid Securities Index ( PFF ) has a thirty-day SEC yield of 7.33% right now, which is actually higher than this fund’s current yield. We can see that the fact that the fund is more heavily weighted to preferred stock should therefore give it a greater amount of income than if the fund were more heavily weighted towards bonds.

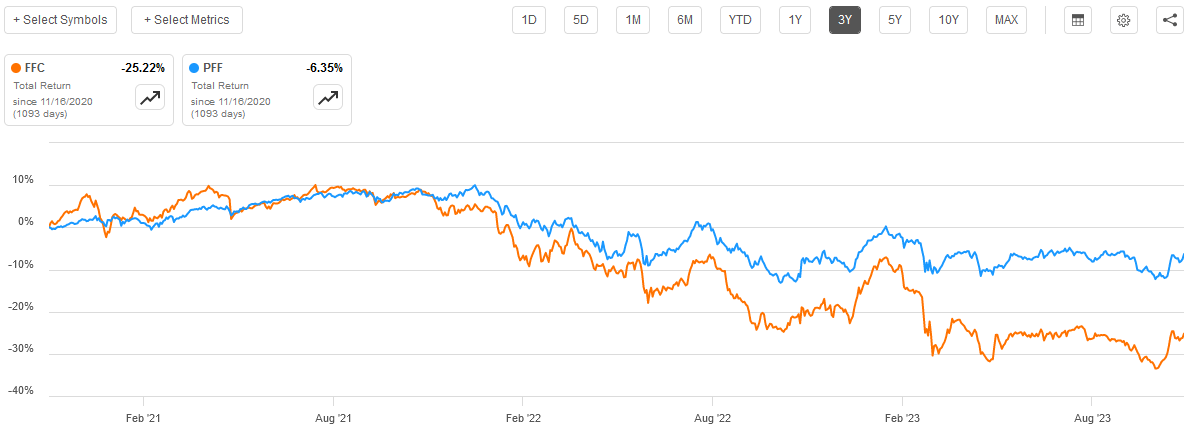

The fact that the iShares Preferred & Income Securities ETF currently has a higher yield than this fund is something that will undoubtedly be disappointing to any income-focused investor. This is particularly true when we consider that the index fund has substantially outperformed the Flaherty & Crumrine Preferred and Income Securities Fund on a total return basis over the past three years:

{kind=link}

One big reason for the poor performance of this fund relative to the index is that it employs leverage as a method of boosting its effective portfolio yield. That works pretty well when asset prices are stable or rising, but it also causes the fund to take outsized losses when asset prices fall, as they did over most of this period. We will discuss this in more detail later in this article.

In my previous article on the Flaherty & Crumrine Preferred and Income Securities Fund, I pointed out that it has very substantial exposure to the banking sector. That continues to be the case, and in fact, the fund has increased its exposure to this sector over the past two months:

Flaherty & Crumrine

The last time that we discussed this fund, it had a 54.8% weighting to banks and a 22.4% weighting to insurance companies. Thus, the fund’s allocation to these two sectors is a bit higher than it used to be. The banking sector has been a point of concern for many market participants ever since the Silicon Valley Bank collapse, but this fear certainly does not appear to be at the forefront of most investors’ mindsets right now as it was a few months ago. However, there are still some concerns regarding the sector considering that just about every American bank is technically insolvent right now. After all, after two decades of incredibly cheap money, these banks are sitting on mortgage loans, Treasury securities, and other assets paying 4% at a time when the cost of money is 5.33% (effective federal funds rate) or higher. The Federal Reserve has implemented extraordinary measures to ensure that bank runs will not collapse the banks, so we probably do not really have to worry about this. It is difficult to deny that investors will have fears about it.

The iShares Preferred & Income Securities ETF states that it has 74.31% exposure to financial institutions right now:

{kind=link}

Unfortunately, it does not break it down by banks versus insurance companies, so it is difficult to determine if the Flaherty & Crumrine Preferred and Income Securities Fund is over-allocated to banks compared to the index. If we consider both banks and insurance companies to be “financial institutions,” then we get a 77.8% weighting to this sector for the Flaherty & Crumrine Fund. That is obviously a bit higher than the index. Investors should probably be comfortable with investing in the banking sector before purchasing this fund; or adjust the rest of their portfolios to compensate for this fund’s high exposure.

Interest Rate Outlook

As the Flaherty & Crumrine Preferred and Income Securities Fund invests almost exclusively in fixed-income securities, its performance is heavily influenced by interest rates in the United States. This is perhaps the biggest reason why the fund’s performance has been very bad over the past two years. As such, the fund’s forward performance will almost certainly be dependent on where interest rates go from here.

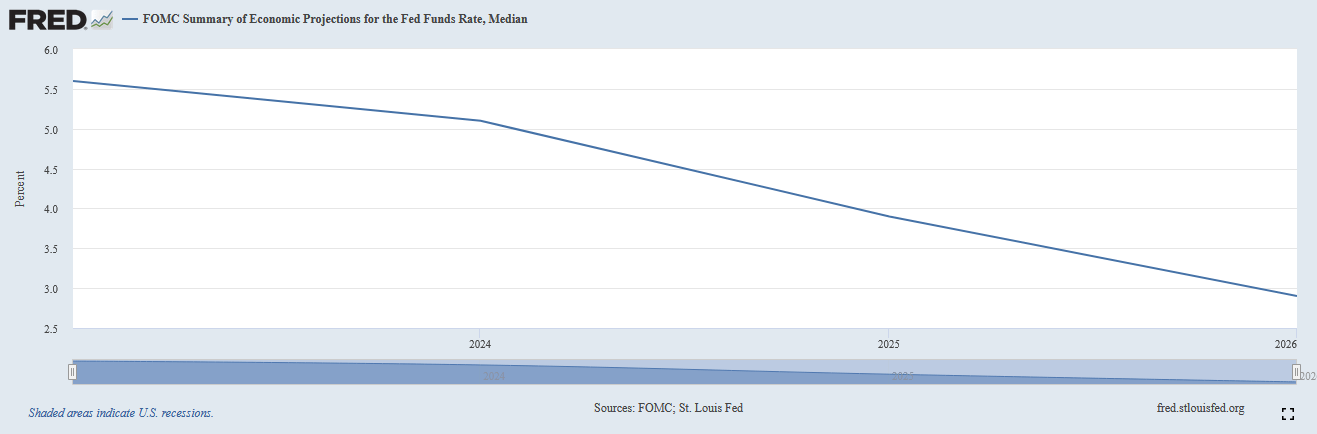

As of right now, the members of the Federal Open Market Committee expect that the federal funds rate will decrease over the next few years. The median prediction by the committee’s current members is that the federal funds rate will slowly decline to 2.9% by 2026:

{kind=link}

The market appears to agree with this assessment right now. Earlier today, the Bureau of Labor Statistics released its monthly inflation report, which showed that the headline Consumer Price Index increased by 3.2% year-over-year. That was considerably below economists’ expectations of 3.3% and it sparked a massive market rally. After all, this report allowed the market to believe the narrative that the Federal Reserve has won the inflation fight and will soon be able to cut interest rates. This is despite the fact that a 3.2% inflation rate is still well above the sustained 2.0% that the Federal Reserve is targeting.

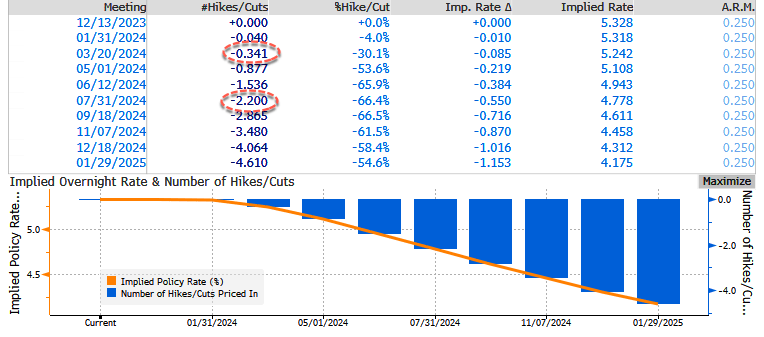

The market’s expectations immediately shifted, and as of right now it is expected that there will be no more rate hikes and that cuts will begin as early as March 2024:

{kind=link}

That chart shows how fed funds futures are currently trading.

This narrative suggests that the Flaherty & Crumrine Preferred and Income Securities Fund should start seeing the value of its assets improve going forward. That certainly explains the share price jump that we saw today (the fund’s shares closed up 1.36%).

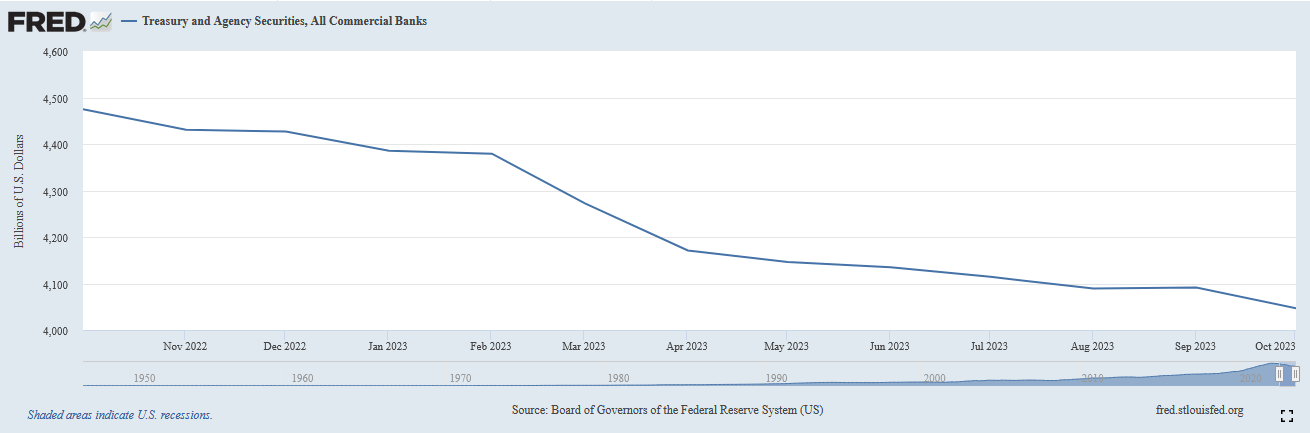

However, there is a big problem with this narrative. That is the Federal Government’s spending addiction. As I explained in a previous article (linked in the introduction), the Federal Government is currently competing against the private sector for money. It is also experiencing a shortage of buyers, as several foreign nations have either stopped purchasing Treasuries or have even started dumping them. American commercial banks have also been reducing their Treasury holdings:

{kind=link}

This is one big reason why recent Treasury auctions have not been going particularly well. For example, the thirty-year Treasury auction last week was horrible on all counts. As such, the U.S. government is being forced to offer higher yields just to get people to actually lend it money. As the rate of pretty much everything else is based on Treasury rates, this implies that interest rates are likely to rise regardless of the fed funds rate.

The Federal Reserve could, of course, force rates down by increasing the money supply and buying newly issued Treasuries itself. That would also cause inflation to take off once again.

In short, the only realistic way that interest rates can go down from here is to introduce inflation. The U.S. Federal government cannot realistically cut its spending due to political reasons, so at some point, the Federal Reserve will have to decide whether it wants to accept high interest rates or high inflation. Personally, I suspect that it will opt to accept a high level of inflation and cut interest rates along with monetizing the debt.

This scenario would certainly benefit the Flaherty & Crumrine Preferred and Income Securities Fund. However, I am not as sure about when the Federal Reserve will pivot. It may keep rates at today’s levels for longer than the market currently expects.

Leverage

As is the case with most closed-end funds, the Flaherty & Crumrine Preferred and Income Securities Fund employs leverage as a method of boosting its effective yield beyond that of any of the underlying assets in the fund. I explained how this works in my previous article on this fund:

Basically, the fund is borrowing money and using that borrowed money to purchase preferred stocks and other income-producing securities. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not employ too much debt as that would expose us to too much risk.

As of the time of writing, the Flaherty & Crumrine Preferred and Income Securities Fund has levered assets comprising 41.43% of its portfolio. This is clearly well above the one-third maximum level that I usually like to see. It is, however, true that fixed-income funds can frequently carry a higher level of leverage than common equity funds due to the fact that fixed-income securities are less volatile than common equities. However, this fund’s current leverage is still well above that of most comparable funds from any fund sponsor other than Flaherty & Crumrine.

This fund house seems to be using a considerable amount of leverage compared to others, and as such its funds will probably prove to be more volatile. This is something that most conservative income-focused investors do not really want, especially because it is not that difficult to get a higher yield from a less leveraged closed-end fund right now.

Distribution Analysis

As mentioned in the introduction, the Flaherty & Crumrine Preferred and Income Securities Fund has the primary objective of providing its investors with a very high level of current income. In order to achieve that goal, the fund invests in a portfolio that consists of preferred stock, various forms of debt, and other securities that primarily deliver their investment returns through direct payments to their investors. The fund then borrows money in order to purchase more of these securities than it could otherwise buy simply with its own money. It collects all of the dividend and interest payments made by the securities in its portfolio and then pays them out to the shareholders, net of its own expenses. In some cases, the fund may also be able to exploit changes in security prices and generate capital gains, which adds more money to the amount that it can pay out. As such, we can assume that this fund should have a very high yield, especially considering the current yield on most of the securities in its portfolio right now.

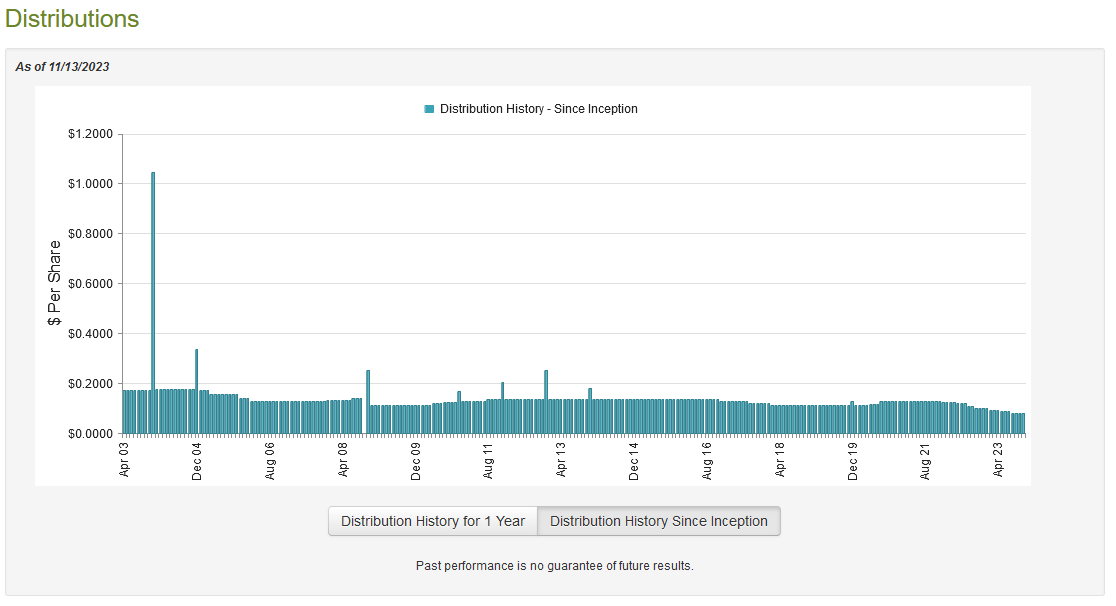

This is certainly the case, as the fund currently pays a monthly distribution of $0.0815 per share (0.978 per share annually), which gives it a 7.41% yield at the current price. This is a yield that would have been very attractive two years ago, but in today’s environment, it is beaten handily by several other funds that are using roughly the same strategy. In addition, this fund has not been especially consistent with respect to its distribution over the years. As we can see here, it has varied its payout by quite a bit over time:

{kind=link}

As is the case with other funds from Flaherty & Crumrine, we can see that this one has even had to cut its distribution multiple times over the past year. The fund has cut its distribution three times over the past twelve months, going from $0.10 per share to $0.0815 per share. That is certainly going to reduce the appeal of this fund in the eyes of any income-focused investor right now. That is particularly true considering that inflation has required that we increase our incomes, not decrease them.

However, the fund’s past history is not necessarily the most important thing for anyone who is purchasing the fund’s shares today. This is because anyone purchasing this fund today will receive the current distribution at the current yield and will not be negatively impacted by the events of the past. As such, we want to see how well the fund is managing to cover its distribution right now.

We have a reasonably current document to consult for the purpose of our analysis, although it is not as current as I might like. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. This was a rather interesting period for the market and for this fund. The majority of this time period saw a very strong market, as investors expected that the Federal Reserve would quickly reverse course on interest rates and begin cutting in the second half of that year. While this did not actually happen, it still may have provided the fund with some potential opportunities to sell appreciating securities into an optimistic market.

At the same time, this period included the collapse of Silicon Valley Bank and a few other regional financial institutions. That had a negative impact on bank preferred stock, which as we have already seen this fund is heavily invested in. Thus, this served as a drag on the fund’s performance during the period that was completely independent of the market’s view on interest rates.

During the six-month period, the Flaherty & Crumrine Preferred and Income Securities Fund received $16,005,597 in dividends along with $26,355,024 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we get a total investment income of $42,488,060 during the period. The fund paid its expenses out of this amount, which left it with $25,107,930 available for shareholders. That was, unfortunately, not enough to cover the $27,251,961 that the fund actually paid out in distributions during the period, although it did manage to get pretty close. However, we still generally would like to see a fixed-income fund completely finance its distributions out of net investment income and this fund clearly failed to accomplish that task.

The fund does have other mechanisms through which it can obtain the money that it needs to cover its distributions. For example, it might have been able to generate a certain amount of capital gains during the period simply by exploiting fluctuations in fixed-income prices. Unfortunately, it failed miserably at this task. The fund reported net realized losses of $28,366,059 and had another $36,492,135 in net unrealized losses during the period. Overall, the fund’s net assets declined by $65,550,648 over the period after we accounted for all inflows and outflows.

This certainly explains the distribution cut, as this fund failed to cover the distribution over this period. However, it is possible that the fund is in better shape now. As we can see, the fund did manage to come pretty close to covering its distribution out of net investment income during that period. The distribution is lower now, so it should be less expensive. Unfortunately, the fund was forced to sell some securities at a loss, so it is probable that its net investment income is also lower now than it was during the reporting period. We therefore cannot assume that the smaller distribution will be covered just because the fund came pretty close to covering during the reporting period.

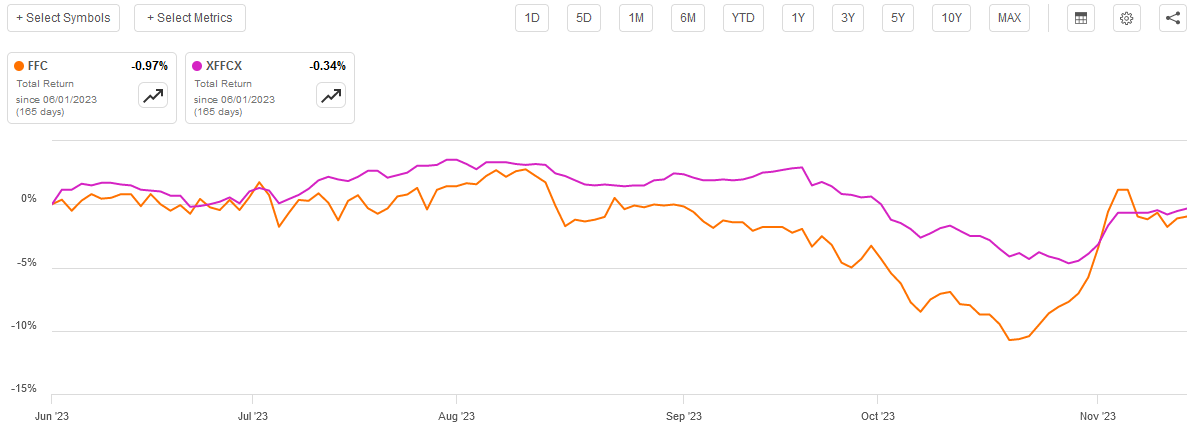

The fund’s net asset value has held up pretty well since June 1, 2023:

{kind=link}

As we can see here, the fund’s net asset value has only declined by 0.34% since June 1, 2023. This is a pretty good sign that the fund is coming very close to covering its distribution, as its monthly distributions have not been obviously destructive. We will need to wait until the fund releases its full-year report in a few months to know for certain, however.

Valuation

As of November 13, 2023 (the most recent date for which data is currently available), the Flaherty & Crumrine Preferred and Income Securities Fund has a net asset value of $14.73 per share, but the shares currently trade for $13.37 each. This gives the shares a 9.23% discount on net asset value at the current price. This is worse than the 11.62% discount that the shares have had on average over the past month, but it is still a discount. The current price could be decent if you are looking to get into this fund.

Conclusion

In conclusion, the Flaherty & Crumrine Preferred and Income Securities Fund is a generally popular fund that got severely punished over the past two years. The fund’s leverage was sufficiently high to result in it taking some fairly large losses and forcing it to cut its distribution multiple times. Unfortunately, this has caused the fund to have a lower yield than many less aggressive peers along with a still very high level of leverage. The distribution has now probably been cut enough that the fund should be able to maintain it, but investors can still obtain a better yield elsewhere.

For further details see:

FFC: Better Yields Can Be Obtained Elsewhere