FITBO - FFC: Preferred Equity CEF Up More Than 10% YTD

Summary

- Flaherty & Crumrine Preferred and Income Securities Fund is a closed end fund focused on preferred equity.

- The CEF is a leveraged take on banking and insurance preferred shares.

- The fund is fairly leveraged at 38% and is down -16% in the past year as rates have risen.

- The CEF is a better alternative to some individual names and has posted a total return in the past year close to some of the higher quality mREIT preferred shares.

Thesis

The Flaherty & Crumrine Preferred and Income Securities Fund (FFC) is a closed end fund focused on preferred equity. The CEF is part of the Flaherty & Crumrine fund family, a boutique premier asset manager in the preferred securities space with an enviable track record.

The vehicle invests its cash in a portfolio of preferred securities, mainly from highly rated banking and insurance corporates. For large banks, preferred securities represent a form of Tier 1 capital in many instances, meaning that it will take a banking / financial crisis for these shares to be written-down in order to absorb losses. To that end we can have a quick look at one of the fund's largest holdings, namely the BNP Paribas (BNPQF) 7.375% (USF1R15XK367) holding:

The Prevailing Outstanding Amount of the Notes will be written down if the Issuer's CET 1 Ratio on a consolidated basis falls below 5.125 per cent (each term as defined in Condition 2 (Interpretation) in "Terms and Conditions of the Notes"). Holders may lose some or all of their investment as a result of a Write Down. Following such reduction, some or all of the principal amount of the Notes may, at the Issuer's discretion, be reinstated, up to the Original Principal Amount, if certain conditions are met. See Condition 6 (Write-Down and Reinstatement) in "Terms and Conditions of the Notes". If a Capital Event or a Tax Event has occurred and is continuing, the Issuer may further substitute all of the Notes or vary the terms of all of the Notes, without the consent or approval of Holders, so that they become or remain Compliant Securities (as defined in Condition 7.5).

Currently, BNP's CET 1 Ratio is 12.1%, so quite well above the threshold. Make no mistake, bank preferred shares are not risk free, however, since the Great Financial Crisis ('08-'09) regulators have really been prescriptive around risk within the banking sector, hence we feel it is quite well contained these days. The current/upcoming recession will not be a banking one, so we feel FFC contains mostly duration / rates risk.

The fund is fairly leveraged at 38%, and is down -16% in the past year as rates have risen. We view FFC as a nice diversified vehicle to take a long position in a leveraged way in high quality banking/insurance preferred shares. In the current environment FFC's moves have been mostly driven by rates, but a true financial services crisis can seriously affect the price of this fund.

Analytics

AUM: $1.3 billion.

Sharpe Ratio: 0.14 (5Y).

Std. Deviation: 14.2 (5Y).

Yield: 7%.

Premium/Discount to NAV: +1%.

Z-Stat: 0.5.

Leverage Ratio: 38%

Performance

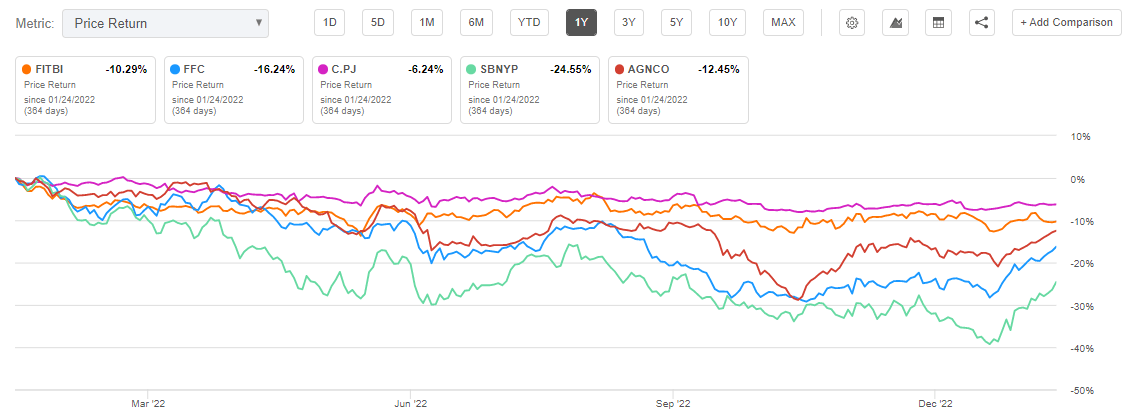

The CEF is down -16% in the past year:

{kind=link}

We are looking in the above graph at price performance only, across a number of individual preferred shares and FFC:

- FITBI is a preferred issuance from Fifth Third Bancorp (FITB) and is actually a holding in the FFC portfolio.

- C.PJ is a preferred stock from Citigroup (C)

- AGNCO is one of the higher quality preferred holdings from an mREIT namely AGNC (AGNC)

- SBNYP is a preferred issuance from Signature Bank (SBNY), an issuer which has been in the news as of late due to outflows from its crypto business deposits

So the idea here is to see how FFC did versus just investing outright in the respective individual issuances. We can see that from a pure price perspective FFC is in the middle of the cohort. The worst performing name is SBNYP (where the market was assigning fundamental issues), while the best performing one is C.PJ. The other banking name, FITBI is down -10%. Given that FFC has 38% leverage it makes sense that it is down more than FITBI. What is interesting is the fact that FFC actually performed in line with one of the preferred shares from AGNC.

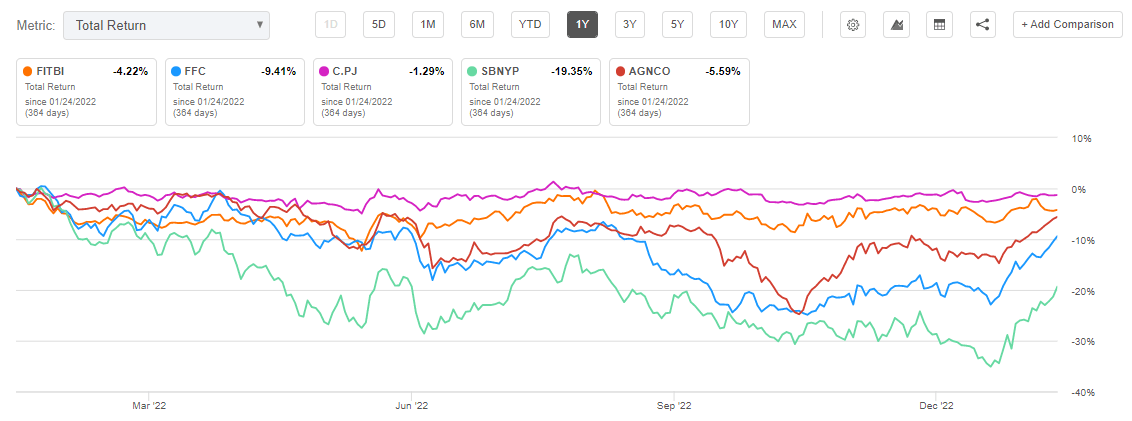

Let us switch to a total return profile (i.e. dividends included) and see how the performance fared:

{kind=link}

- FFC is down ~ -10% on a total return basis in the past year

- The higher quality bank preferred shares from Citi and Fifth Third Bancorp are down only -2% and -4% respectively (if an investor had bought them directly)

- The higher quality mREIT preferred AGNCO is down only -5.5%

Leverage has magnified FFC's move, this time on the downside versus the individual names in the portfolio. The drawdown profile is also very different, with FFC down over -20% at some point in the end of September 2022. For FFC do expect diversification, but also volatility as driven by its leverage.

Conclusion

FFC is a preferred equity CEF. The fund focuses mainly on banking and insurance shares and runs a high 38% leverage. The main risks for FFC are credit and interest rate risk. During this market downturn the credit risk has been muted given we are not experiencing a banking crisis. FFC takes direct hits when bank's capital ratios decrease substantially. The fund's moves have been almost entirely driven by rates. Duration has seen a massive rally in 2023, with FFC up more than 12% already this year. The CEF represents a diversified way to invest in preferred banking shares with leverage, and has a total return profile very akin to the higher quality mREIT preferreds (individual risk there though). The CEF moved to a discount late in 2022 as the market experienced risk-off moves, but is now back at a premium. Don't expect outsized yields here as the CEF cut its distribution to maintain a stable NAV on the back of a poor 2022. Do expect very good long term results though. We are of the opinion the worst is not yet over here and 2023 is going to be tricky, but the next risk-off bout might be a good entry point to start dollar cost averaging into FFC. Long term this is a very robust CEF.

For further details see:

FFC: Preferred Equity CEF Up More Than 10% YTD