FFC - FFC: This CEF Is Looking More Attractive Now But The Price Is Higher Than Normal

2023-04-17 10:20:28 ET

Summary

- Investors today are desperate for income as the rising cost of living means that your money does not go as far as it once did.

- FFC invests in a portfolio of preferred stocks and other fixed-income investments to provide a very high yield to its investors.

- The fund was negatively affected by interest rate hikes over the past year, but it now appears that the worst is probably behind us.

- The fund has cut its distribution four times in the past twelve months, but it is probably sustainable at the current level.

- The fund is trading at a discount, but it is more expensive than its one-month average.

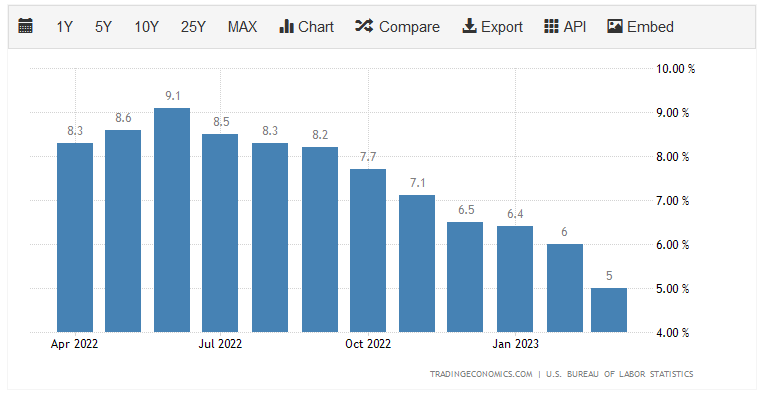

It is hardly an overstatement to say that one of the biggest problems facing the average American today is the rapidly rising cost of living. This is evident by looking at the consumer price index, which shows that inflation is at some of the highest levels that we have seen in more than forty years. In fact, over the past twelve months, there has only been one month in which the index did not increase by at least 6% year-over-year:

{kind=link}

Food and energy have been among the things that have seen the steepest increase in prices over the period. As these are generally considered to be necessities, it is understandable that people of limited means have been the most negatively impacted by this situation. We have seen many people in this category take on second jobs, enter the gig economy, or borrow money just to maintain their lifestyles. In addition, the majority of the savings that many people amassed during the pandemic have now been spent. In short, people are desperate for extra sources of income just to maintain their lifestyles in the face of rising prices.

As investors, we are certainly not immune to this inflation because we too need money to support ourselves. However, we can be a bit more flexible in how we obtain it. This is because we have the ability to put our money to work for us in order to generate an income. One of the best ways to do this is to purchase shares of a closed-end fund that specializes in providing its investors with an income. These funds are not very well-followed in the investment world, nor are they familiar to most investment advisors. This is rather unfortunate because they offer a number of advantages over open-end mutual funds and exchange-traded funds, such as the ability to employ certain strategies that have the effect of boosting their returns well beyond that of any of the underlying assets. This allows these funds to have some of the highest yields available in the market.

In this article, we will discuss the Flaherty & Crumrine Preferred and Income Securities Fund ( FFC ), which is one fund that investors can use to earn an income. This fund is certainly a reasonable source of income as its 7.64% yield should allow even a modest portfolio to generate enough income to support a middle-class lifestyle, and it still beats many other things in the market. I have discussed this fund before, but several months have passed since that time so naturally several things have changed. This article will therefore focus specifically on those changes, as well as provide an updated analysis of the fund’s finances. Let us investigate and see if this fund would be a reasonable addition to an income portfolio today.

About The Fund

According to the fund’s webpage , the Flaherty & Crumrine Preferred and Income Securities Fund has the stated objective of providing its investors with a high level of current income, while still preserving the value of its principal. This is not especially surprising as the name of this fund implies that it is a fixed-income fund. That would fit well with the description of the fund’s strategy that is provided on the webpage:

“Under normal market conditions, the Fund invests at least 80% of its Managed Assets (defined below) in a portfolio of preferred and other income-producing securities. Preferred and other income-producing securities include, among other things, traditional preferred stock, trust preferred securities, hybrid securities that have characteristics of both equity and debt securities, contingent capital securities, subordinated debt, and senior debt.”

This description sounds like this fund invests primarily in preferred stock and bonds, although there may be things like floating-rate debt securities in the portfolio. The fund’s actual composition appears to support this, as currently the majority of the portfolio is invested in preferred stock:

CEF Connect

Preferred stock is something of a hybrid between common stock and bonds. As is the case with bonds, these securities pay a regular amount to their shareholders at a given interval. This payment is generally linked to interest rates and has little to do with the actual financial performance of the issuing company. As such, we cannot expect them to deliver much in the way of capital gains as the issuing company grows and prospers. This is why the fund’s focus on current income is not unexpected, as these securities will deliver the overwhelming majority of their total return in the form of direct payments to the investor. The fund will then aggregate these payments from the preferred stock and bonds in its portfolio and distribute the money to its investors.

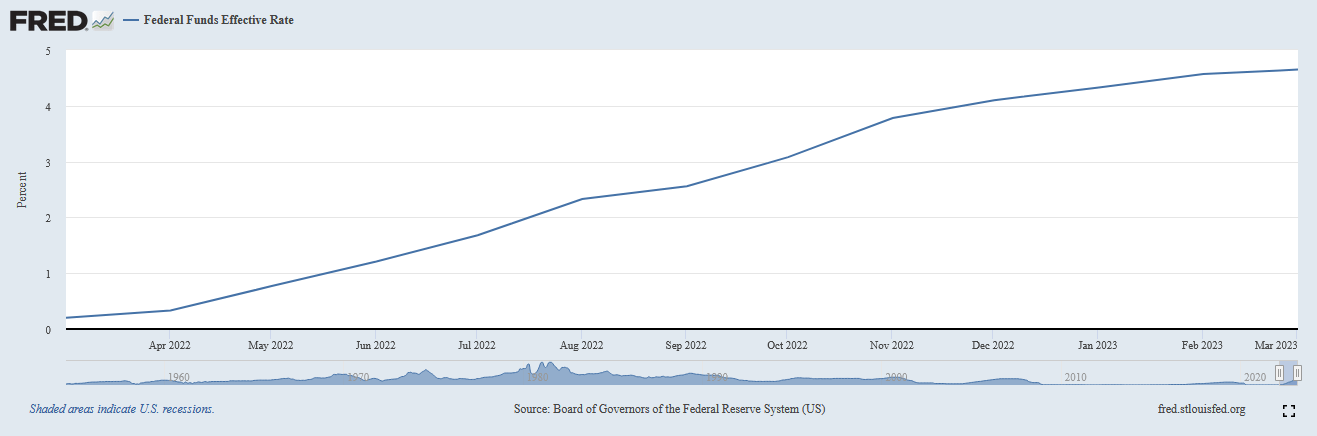

Although these securities do not really benefit from the growth of the issuing company, it is possible to get capital gains from them in certain circumstances. This is because the price of both bonds and preferred stock is correlated to interest rates. In short, when interest rates go up, bond and preferred stock prices go down. The reverse also happens, as lower interest rates push bond prices up. As everyone reading this is certainly well aware, the Federal Reserve has been aggressively raising interest rates over the past year in an effort to combat the high level of inflation that is currently running rampant throughout the economy. In March 2022, the effective federal funds rate was 0.20% but it has since risen to 4.65% today:

{kind=link}

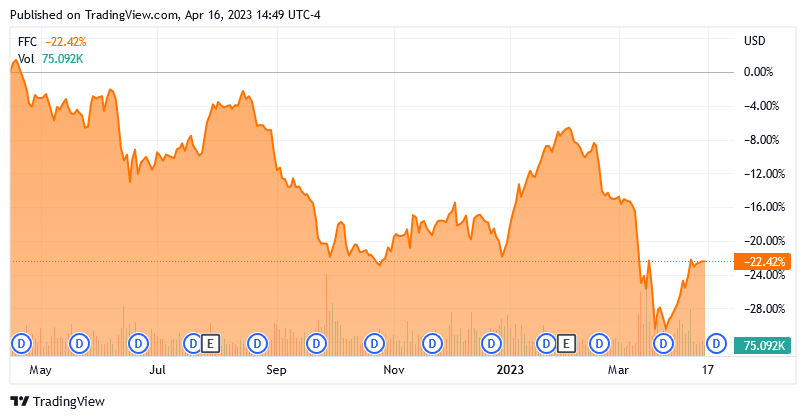

As of today, interest rates are at the highest level that we have seen since 2007. This has had a very noticeable effect on bond and preferred stock prices, as both have declined significantly over the past year. The reason for this should be fairly obvious. These securities are issued with a fixed dividend or distribution that gives them a specified yield at their issuance price. As interest rates rise, newly issued securities will naturally have higher yields, so nobody will be interested in buying the existing securities. As such, the price of the existing securities must decline so that they give the same effective yield as a brand-new security with identical characteristics. This is reflected in the price of the fund, which is down 22.42% over the past year:

{kind=link}

This is certainly not the kind of performance that will endear many people to the fund, but fortunately, it appears that the worst is behind us. Over the past few months, we have seen the inflation rate decline, although that is mostly because of declining energy costs as the market begins to worry that the economy will soon drop into a recession. In addition to this, we have seen that the nation’s banking system is starting to encounter trouble as the sharply rising rates have technically rendered any bank that is holding long-term Treasuries insolvent. Thus, we are probably nearing the top of the Federal Reserve’s rate hiking cycle. The market is currently pricing in a 0.25% rate hike in May and then a pivot that will result in rates being much lower by September. I personally doubt that since such a rate cut will cause inflation to take off again and Chairman Powell has stated repeatedly that there will be no rate cut this year. However, a rate cut will likely cause the shares of this fund to appreciate in value so that would not hurt an investor in the fund. The important thing for timing our purchase is to avoid buying at a time in which the central bank is hiking rates, and it looks like we are very near to the end of the rate hike cycle. Thus, other investors have already taken the losses here and there probably will not be too much more to lose.

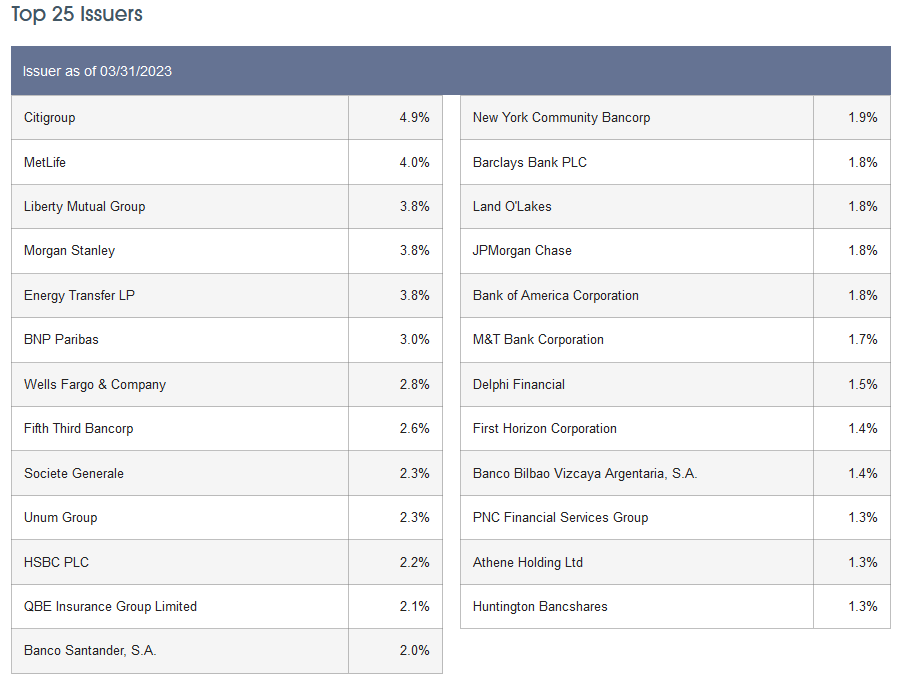

In my last article on this fund, I pointed out that the fund is heavily invested in financial stocks. That is still the case today. Here are the largest positions in the fund’s portfolio:

{kind=link}

We can see a few companies here, such as Energy Transfer ( ET ), that are not financial institutions, but overall, the majority are banks or insurance companies. In fact, 54.0% of the fund is invested in bank stocks and 23.5% is invested in insurance companies. That is hardly unusual for a preferred stock fund since the banking sector is by far the largest issuer of preferred stock in the market. One reason for this is international banking regulations. As a result of Basel III, banks are required to maintain a certain percentage of their assets in the form of Tier One capital. This is defined as that portion of a bank’s capital that is not simultaneously a liability to somebody else, such as a depositor. This is essentially the bank’s “own money.” Whenever regulations require a bank to increase its Tier One capital, it has to issue either common stock or preferred stock. Most bank managers will opt to issue preferred stock in these situations in order to avoid diluting the common stockholders. In other industries, there are no regulations such as this and so most companies will opt to issue debt instead of preferred stock because debt is quite a bit cheaper to service. Thus, by default banks are the largest issuers of preferred stock, and any preferred stock fund will be heavily invested in the banking sector.

As my regular readers on the topic of closed-end funds are likely well aware, I do not typically like to see any individual position in a fund account for more than 5% of the fund’s assets. This is because that is approximately the point at which a given asset begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio, then this risk will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market does not, which could result in an overweighted asset dragging the entire fund down with it. As we can see above though, that does not appear to be a concern here as there is no asset that accounts for an outsized portion of the portfolio. With that said though, Citigroup ( C ) is pretty close and could expose the fund to some idiosyncratic risk. Honestly though, if Citigroup’s preferreds were to decline due to financial problems at the bank or something like that, the entire financial sector would probably collapse with it. Overall, I doubt that there is too much single-company risk here. While we are certainly exposed to problems with the banking sector, the government has a tendency to bail out banks when they get into trouble, and this helps to alleviate any real concerns. There is probably little risk with this fund other than interest-rate risk.

Leverage

As mentioned in the introduction, closed-end funds like the Flaherty & Crumrine Preferred and Income Securities Fund have the ability to employ certain strategies that have the effect of increasing their effective yields beyond that of any of the underlying assets in the portfolio. One of these strategies is the use of leverage. Basically, the fund is borrowing money and using that borrowed money to purchase preferred stocks and other income-producing securities. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not employ too much debt as that would expose us to too much risk. I generally like to see a fund’s leverage remain under a third as a percentage of its assets for this reason. Unfortunately, this fund fails that requirement. As of the time of writing, the fund’s levered assets comprise 40.91% of the portfolio, which makes this one of the most highly levered closed-end funds on the market. This is quite disappointing, and it could be a clear sign that the fund is exposing its investors to too much risk. Granted, fixed-income funds such as this one generally can carry higher leverage than common equity funds due to the safety of their assets, this is still more than I am really comfortable with as it could lead to an outsized level of losses should something go wrong.

Distribution Analysis

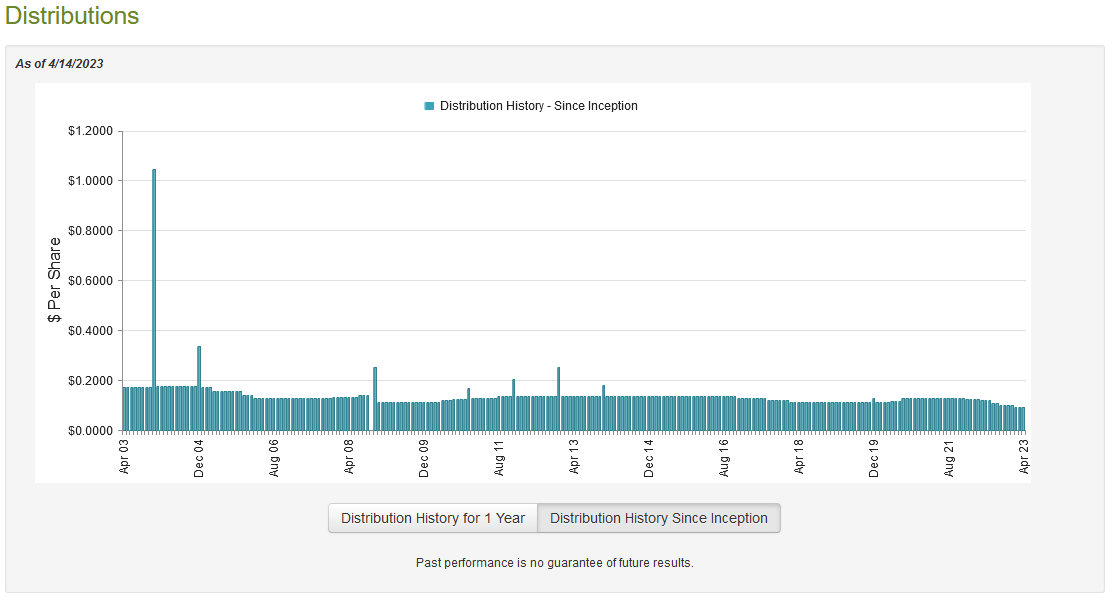

As stated earlier in this article, the primary objective of the Flaherty & Crumrine Preferred and Income Securities Fund is to provide its investors with a high level of current income. In order to accomplish this objective, it primarily invests in preferred stock, which typically has a fairly high yield. It then applies a layer of leverage to boost the yield beyond that offered by the individual securities in the fund. As such, we might assume that this fund has a fairly high yield itself. This is certainly the case as it pays out a monthly distribution of $0.0930 per share ($1.116 per share annually), which gives it a 7.64% yield at the current price. Unfortunately, the fund’s distribution has not been especially consistent as it has varied quite a bit over the years:

{kind=link}

Admittedly, it is not atypical for a fixed-income fund’s distribution to vary over time. This is at least partly due to their interest rate sensitivity. However, this history combined with the fact that this fund has cut its distribution four times in the past twelve months will likely be something of a turn-off to any investor that is seeking a safe and secure source of income with which to pay their bills or finance their lifestyles. However, it is always important to keep in mind that anyone buying shares of the fund today will receive the current distribution at the current yield. As such, a new investor will not be hurt by the fact that the fund cut its distribution in the recent past. The most important thing for these investors is that the fund will be able to maintain its distribution going forward.

Fortunately, we have a fairly recent document that we can consult for the purposes of our analysis. The fund’s most recent financial report corresponds to the full-year period that ended on November 30, 2022. As such, it will not include any information regarding the fund’s performance over the past few months, but it should still give us a good idea of how well the fund handled the challenging market environment of 2022. It is also a newer report than what we had available the last time that we analyzed this fund, which is nice because all the recent distribution cuts have created a need to review the fund’s finances. During the full-year period, the Flaherty & Crumrine Preferred and Income Securities Fund received $32,711,108 in dividends and $50,354,018 in interest from the investments in its portfolio. When we combine this with a small amount of income from other sources, the fund had a total income of $83,271,395 during the period. The fund paid its expenses out of this amount, which left it with $64,533,975 available for the shareholders. Unfortunately, this was not enough to cover the $66,512,756 that the fund actually paid out in distributions during the period, but it did get very close. However, it may still be a bit concerning that the fund did not have sufficient net investment income to cover the distribution.

Fortunately, the fund does have other methods through which it can earn money in order to cover the distribution. For example, it might have capital gains that can be paid out to the shareholders. As we can probably guess from the weak fixed-income market that existed over the year though, the fund generally failed at this task. Over the period, it reported net realized losses of $252,264 and had another $218,916,586 in net unrealized losses. After accounting for all inflows and outflows, the fund’s assets declined by $206,535,621 over the course of the year, which certainly explains the distribution reduction. The fund almost managed to cover its distributions out of net investment income, so it is quite likely that its cuts were an attempt to accomplish that more completely. The fund can probably maintain its current distribution as long as its investment income remains at the current level, which is a reasonable assumption considering that rising interest rates do increase the fund’s income as the yields of purchased securities will be higher than they were a year ago. Overall, things are probably okay here in terms of sustainability.

Valuation

It is always critical that we do not overpay for any asset in our portfolio. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Flaherty & Crumrine Preferred and Income Securities Fund, the usual way to value them is by looking at the net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of April 13, 2023 (the most recent date for which data is currently available), the fund had a net asset value of $15.04 per share but the shares only trade for $14.60 each. This gives the shares a 2.93% discount to net asset value at the current price. This is not a very large discount, and it is quite a bit smaller than the 7.05% discount that the shares have averaged over the past month. Thus, it may make sense to wait a bit and watch the price to see if a more attractive entry point gets presented.

Conclusion

In conclusion, investors today are starved for income as the rising cost of living has resulted in our money not going nearly as far as it did only a few months ago. The Flaherty & Crumrine Preferred and Income Securities Fund could be one solution to that problem as its attractive 7.64% yield is sufficient to add an income boost to any portfolio and it appears to be sustainable at the current level. The fund is also trading at a discount to the net asset value, although it is more expensive than its average. The fund has certainly had some hard times over the past year, but it, fortunately, appears that the worst is behind us so it might make sense to purchase the shares should a more attractive entry price appear.

For further details see:

FFC: This CEF Is Looking More Attractive Now, But The Price Is Higher Than Normal