FFC - FFC: Understanding The Plunge Staying On The Sidelines

2023-06-30 07:10:36 ET

Summary

- FFC has seen a significant drop in performance due to its high exposure to the financial sector.

- The fund's reputation has been damaged, leading to it trading at an 8% discount to its Net Asset Value (NAV), the widest in years.

- Despite the fund trading at a discount, there are factors that could lead to further losses for the fund, making it a risky investment at this time.

A few months ago, I wrote a cautious article on the Flaherty & Crumrine Preferred Securities Income Fund (FFC). My caution stemmed from an analysis of FFC's portfolio, which showed a high concentration of long-duration assets. Since my view at the time was for a 'higher for longer' monetary policy from the Federal Reserve, I worried that FFC's portfolio may face headwinds. Since my article, the FFC fund has plunged, delivering almost -20% total returns (Figure 1).

Figure 1 - FFC has declined by almost 20% since my article (Seeking Alpha)

What happened and is now a good time to buy the FFC fund on the cheap?

FFC Dragged Down By Financials Exposure

In my opinion, the root cause of FFC's poor performance has been its outsized exposure to the Financials sector. As of January 31, 2023, 54.9% of the fund's portfolio was invested in Banks, with a further 22.5% invested in Insurance companies.

Figure 2 - FFC sector exposure as of January 31, 2023 (preferredincome.com)

Since my article in February, the U.S. banking sector had experienced a regional banking crisis sparked by the sudden collapse of SVB Financial in March, followed by the forced merger of Credit Suisse with UBS (wiping out alternative tier 1 contigent capital securityholders), and the seizure of multiple large regional banks.

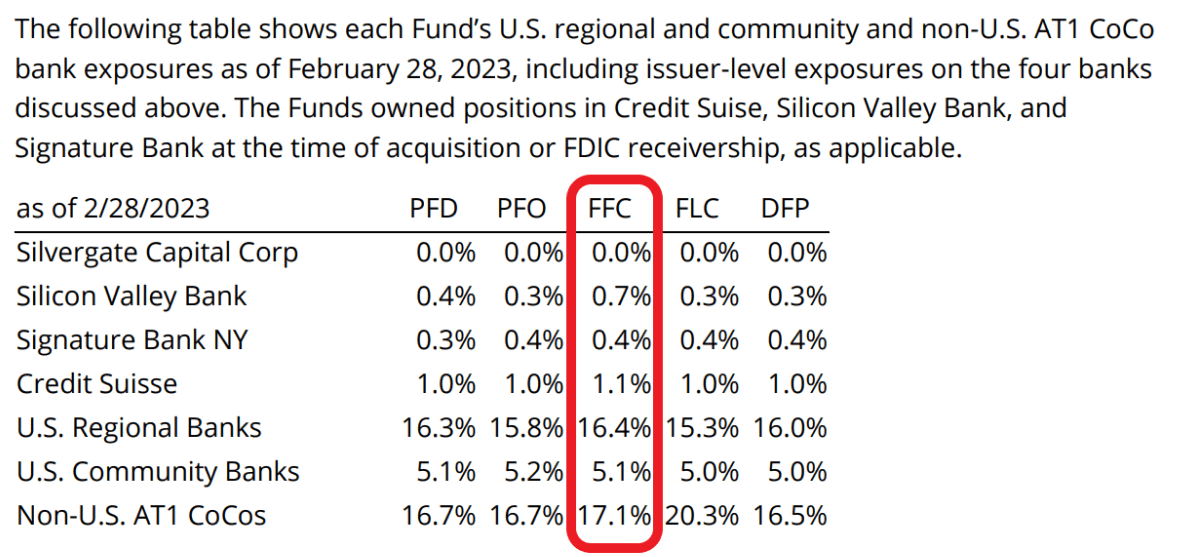

In fact, as explained in a special update from the fund manager, the FFC fund appears to have been particularly exposed, with direct exposures to SVB Financial, Signature Bank, and Credit Suisse, as well as large exposures to U.S. regional banks and Non-US AT1 CoCos (Figure 3).

Figure 3 - FFC was highly exposed to troubled banking preferreds (preferredincome.com)

{kind=link}

Furthermore, as of February 28, 2023, FFC had direct exposure to First Republic Bank, another large regional bank that was seized and sold to JPMorgan ( JPM ) in early May, wiping out preferred shareholders in the process.

All-in-all, 2023 has been annus horribilis so far for Flaherty and Crumrine, with all of their preferred share funds 'blowing up'.

Could This Have Been Foreseen?

To be fair, almost nobody foresaw the regional banking crisis. However, in my prior article, I did warn:

However, FFC's long-term NAV progression does highlight a potential risk that is not often discussed, namely, its heavy concentration in the financial services sector.

As highlighted in figure 4 below, the 2008/2009 Great Financial Crisis ("GFC") was a terrible period for FFC, as many banks and insurance companies were forced to suspend their preferred dividends. In fact, some financial companies like Lehman Brothers even went bankrupt, wiping out preferred stock holders. While ultimately, most banks and insurers returned to financial health and resumed paying preferred dividends, FFC's NAV never returned to its pre-GFC peaks, indicating permanent loss of capital from the episode. If the global economy suffers a financial crisis similar in scale to the GFC, then FFC shareholders could be at risk due to its heavy concentration in financial services.

Figure 4 - FFC's NAV saw a steep drop during GFC (morningstar.com)

So what we experienced in March was a mini-financial crisis, as the Federal Reserve's interest rate increases in the past year placed strain on banks' balance sheets through unrealized losses on investment securities. Furthermore, higher short-term interest rates led to money-market funds yielding more than bank savings deposits, which caused a mass exodus of depositors and forced banks to unload those investment securities and crystallize the unrealized losses.

Distribution Cut Compounds Problems

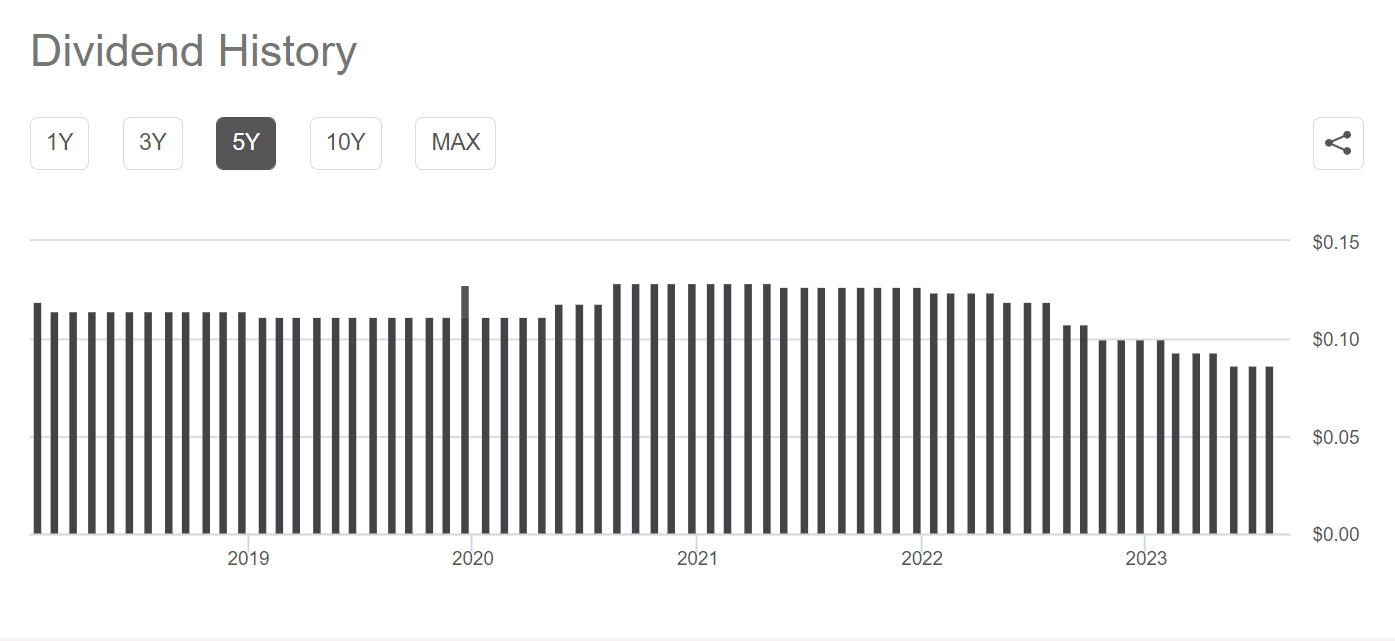

To compound problems with the FFC fund, distributions for the fund have been cut in recent months to $0.087 / month, which annualizes to a 7.0% distribution yield on NAV (Figure 5).

Figure 5 - FFC's distribution continues to be trimmed (Seeking Alpha)

{kind=link}

While this was a prudent move in light of the fund's losses, it no doubt left a bad taste in many unitholders' mouths.

Tarnished Reputation; FFC Trading At Deep Discount

At the end of the day, I believe this latest crisis episode may have tarnished Flaherty & Crumrine's reputation permanently. Recall, Flaherty & Crumrine prides itself on having a dedicated credit research team and avoiding "potential problems... at relatively little cost when they are recognized early" . So if anyone should have foreseen the securities problems with regional banks, it should have been Flaherty & Crumrine.

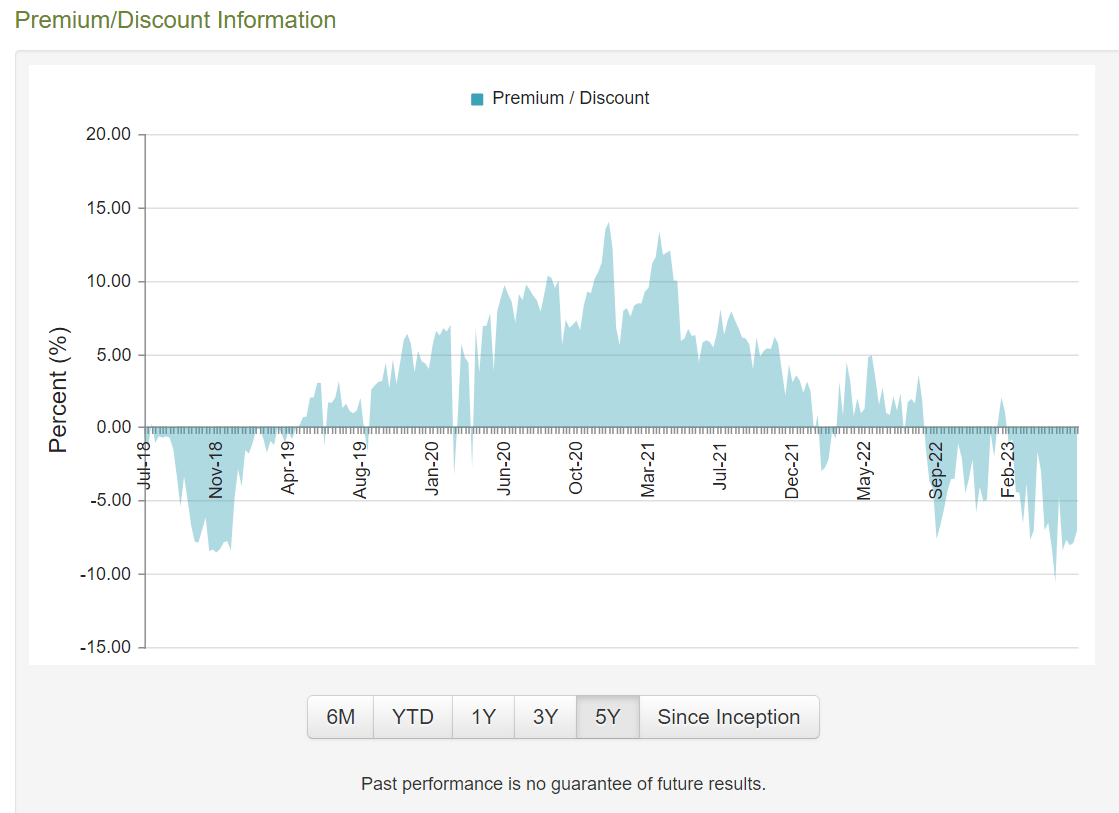

Investors seem to agree with my assessment, as they have sold off the FFC fund, taking the fund to an 8% discount to NAV, the widest in years (Figure 6).

Figure 6 - FFC discount to NAV the widest in years (cefconnect.com)

{kind=link}

The question now is whether the FFC fund is a great buy trading at a steep discount?

Is Now A Great Time To Buy?

There is an old investment saying that investors should buy when there is blood on the streets, even when that blood is your own. The FFC fund has certainly spilled plenty of blood in recent months, with the market price of the fund down by ~20% since February.

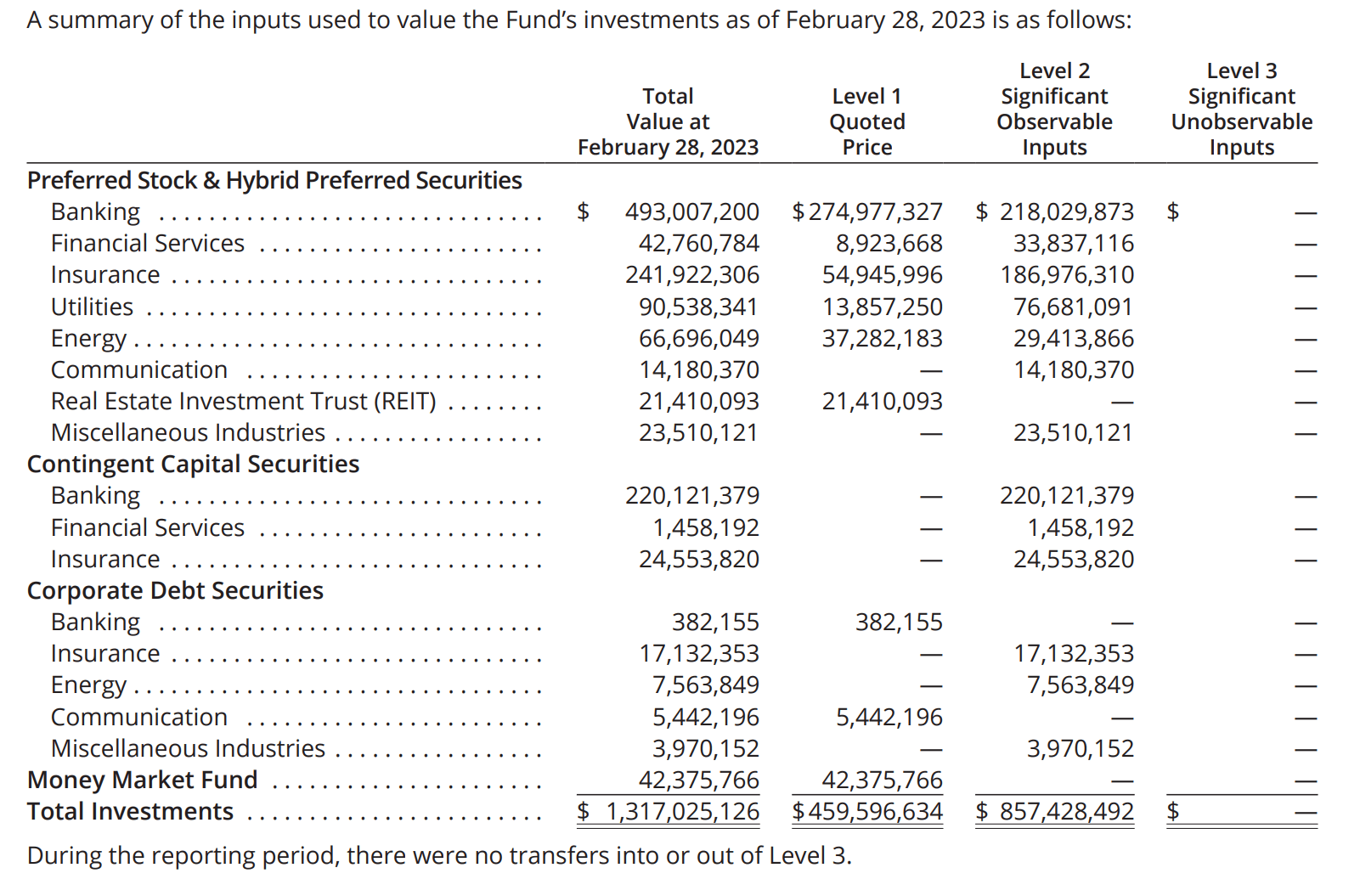

On the positive side, FFC's portfolio consist of mostly preferred shares, hybrid securities, CoCo securities, and corporate bonds. These either have quoted prices or can be easily priced with observable inputs (Figure 7).

Figure 7 - FFC's NAV should be trustworthy (FFC quarterly holdings report)

{kind=link}

FFC's NAV should be accurate and be readily convertible to cash, so FFC's discount to NAV should close over time.

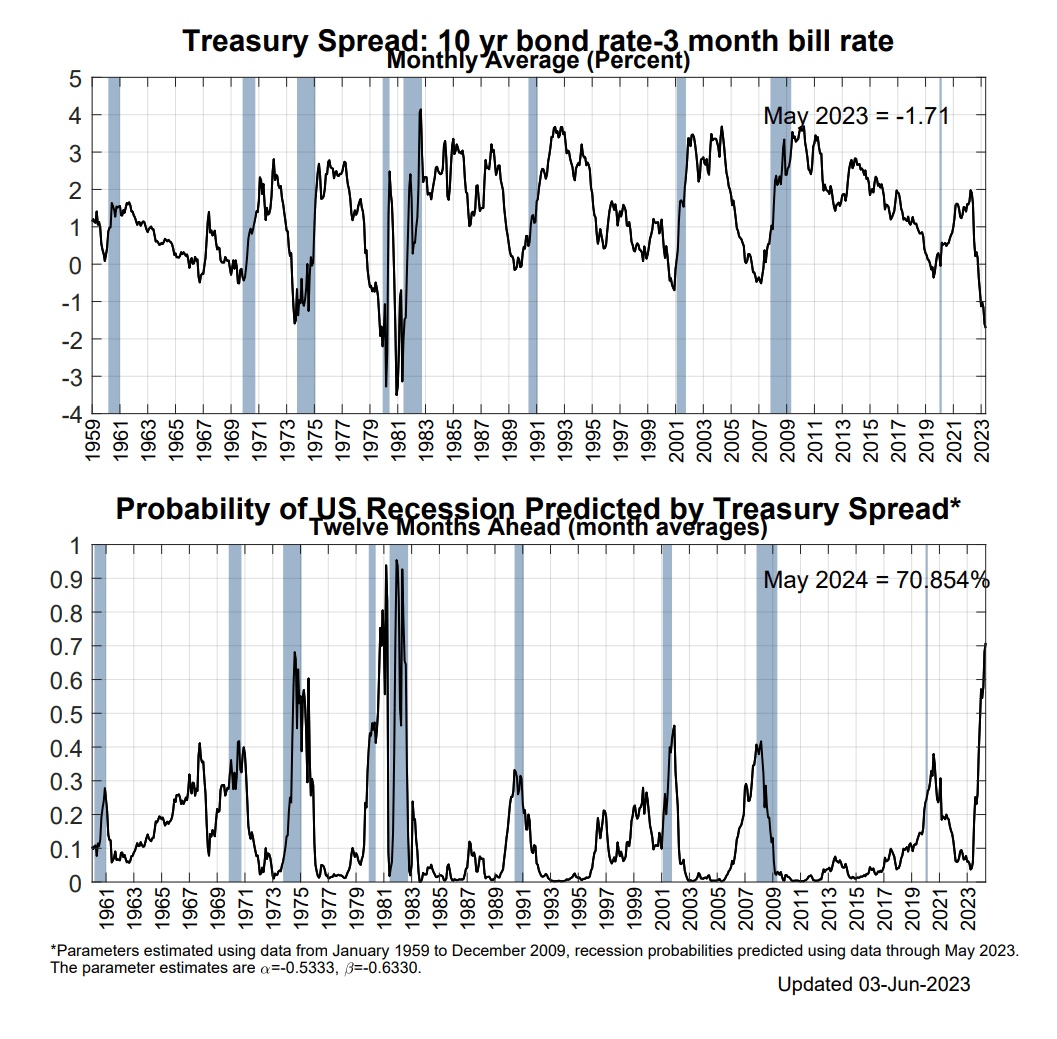

However, on the downside, many economists believe a global recession is just around the corner. In fact, the spread between the 10 Year treasury bond and 3 Month treasury bills suggest a 71% probability of a recession in the next twelve months (Figure 8). This measure has never been this high without coinciding with a recession.

Figure 8 - Treasury spread suggest a high probability of a recession (newyorkfed.org)

{kind=link}

A recession could lead to deteriorating credit performance, which, given FFC's heavy exposure to financial companies, may mean more NAV losses as those companies run into trouble.

Furthermore, if the U.S. economy avoids a recession, then we still have to contend with a Federal Reserve that has pledged to stay 'higher for longer' in order to stamp out inflation. Importantly, at the recent ECB Sintra Forum , Fed Chair Powell suggested inflation may not return to the Fed's 2% target until 2025, and the Fed will maintain course until the job is done. Reading between the lines, this means the Fed will keep interest rates higher for longer unless a recession short-circuits the economy. This should act as a headwind for the long-duration FFC fund.

For me personally, I am troubled by the double negatives for the FFC fund. If a recession occurs, the fund will suffer losses. If no recession occurs, then higher interest rates will mean duration headwinds for FFC. This seems like a 'tails I lose and heads you win' situation.

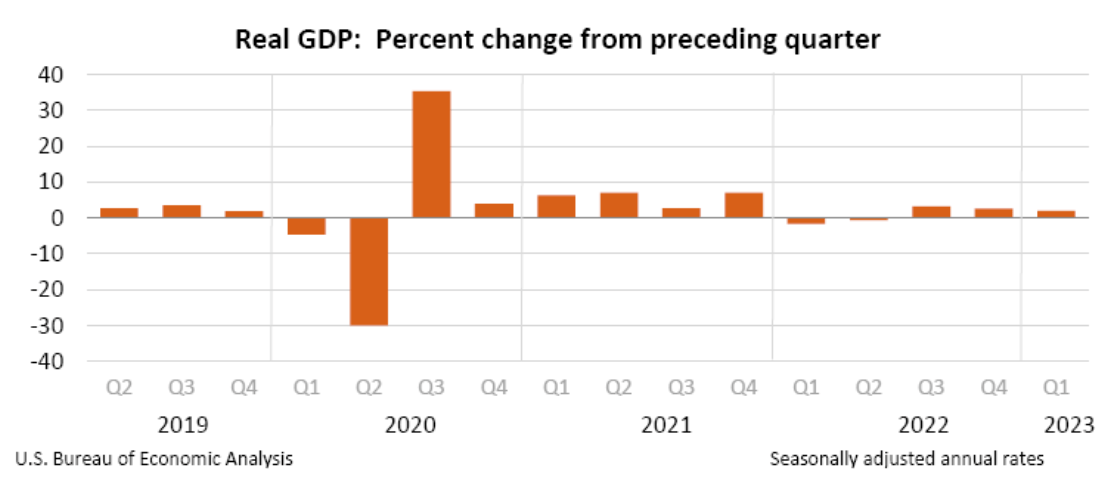

For example, on June 29th, the Bureau of Economic Analysis revised Q1/23 GDP for the U.S. economy to 2.0%, above last month's 1.3% estimate (Figure 9).

{kind=link}

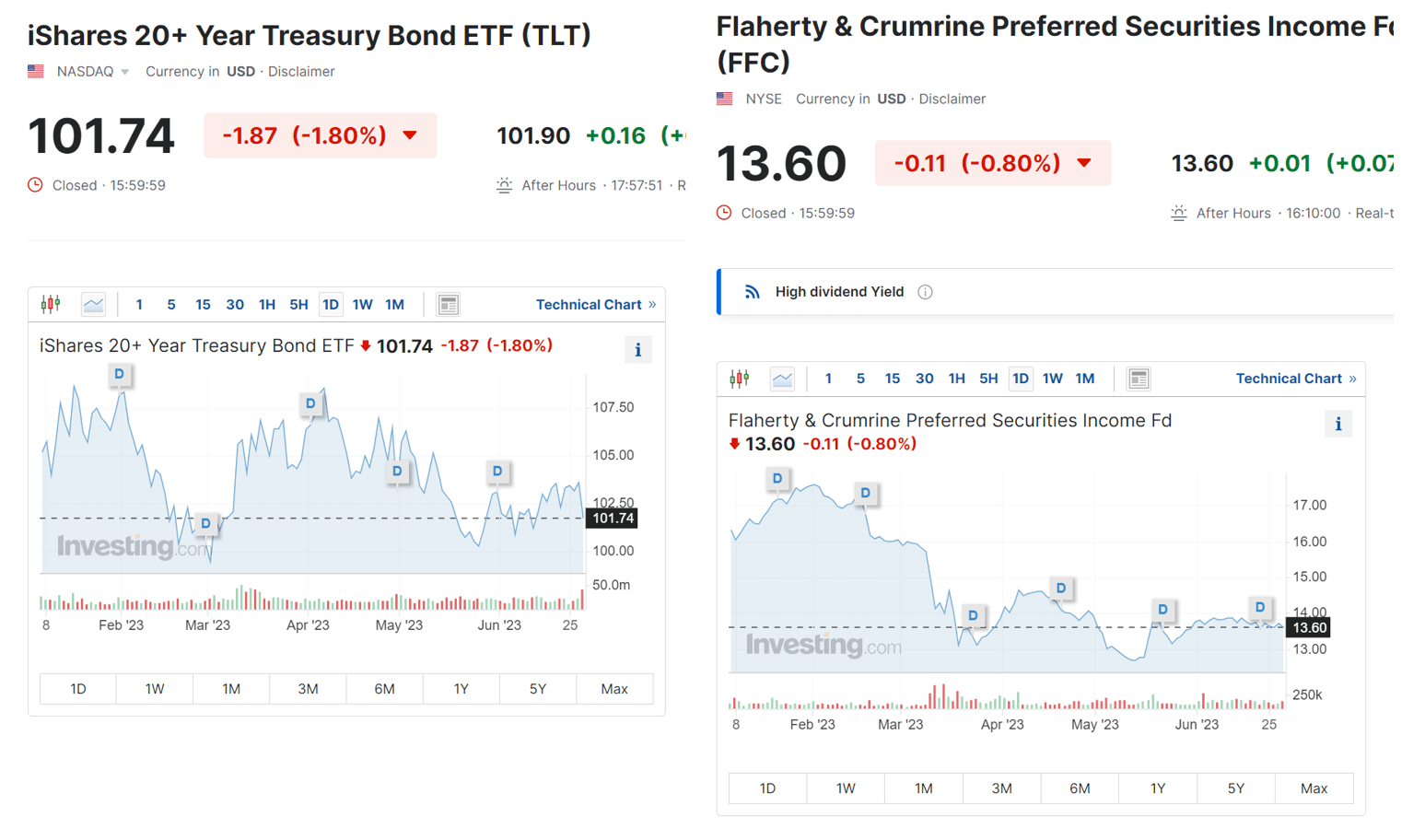

A stronger economy should be good news, right? Instead, both bonds (as modeled by the iShares 20+ Year Treasury Bond ETF) and the FFC fund sold off as investors worried about a 'higher for longer' Fed (Figure 10).

Figure 10 - Both TLTs and FFC sold off on the revision higher in Q1 GDP (investing.com)

{kind=link}

Conclusion

The Flaherty & Crumrine Preferred Securities Income Fund have suffered large losses in the last few months due to its large financials exposure and as investors lost confidence in the manager. Investors who have a positive view of the economy may wish to take advantage of the shares of the FFC fund, as they are currently trading at a steep 8% discount to NAV.

However, I am personally worried about elevated recession risks and/or a 'higher for longer' Federal Reserve, both of which are headwinds for the FFC fund. I am staying away from the FFC fund for now.

For further details see:

FFC: Understanding The Plunge, Staying On The Sidelines