FNF - Fidelity National: High Mortgage Rates Limit Upside

2023-11-17 12:41:02 ET

Summary

- Fidelity National Financial's shares have performed well despite pressure from slowing housing activity as its stake in F&G has grown in value.

- The company's title insurance business has been affected by declining home sales and reduced inventories.

- Fidelity has downsized expenses and focused on managing headcount to adapt to the current market conditions and is allocating capital to F&G.

- Given high rates, home sales are likely to remain slow, limiting the potential for a recovery in title insurance sales.

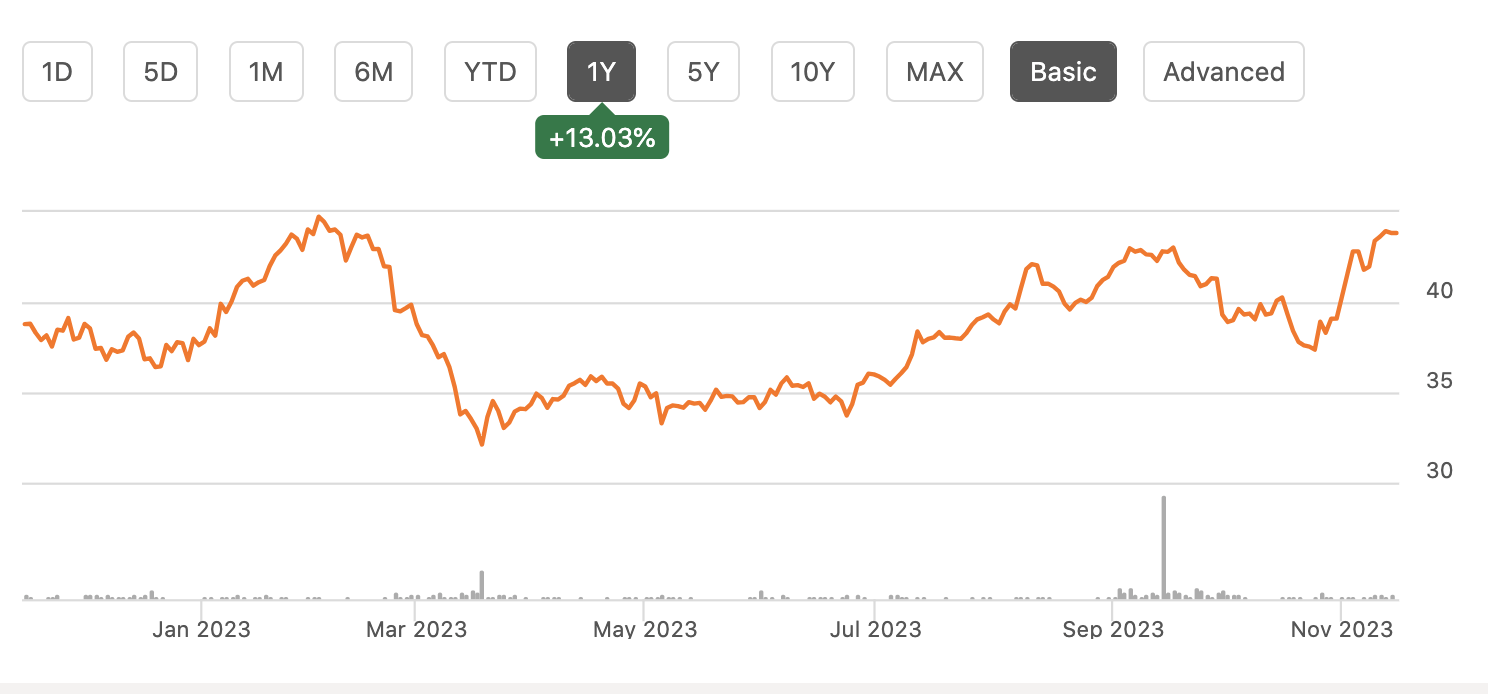

Shares of Fidelity National Financial ( FNF ) have been a solid performer over the past year, rising about 13%, despite the fact its underlying business has been facing significant pressure from slowing housing activity. It has been aided by the fact Fidelity has an 85% stake in F&G Annuities ( FG ) whose stock has surged. At about 10.5x stand-alone earnings, I see shares as roughly at fair value, given ongoing pressures.

{kind=link}

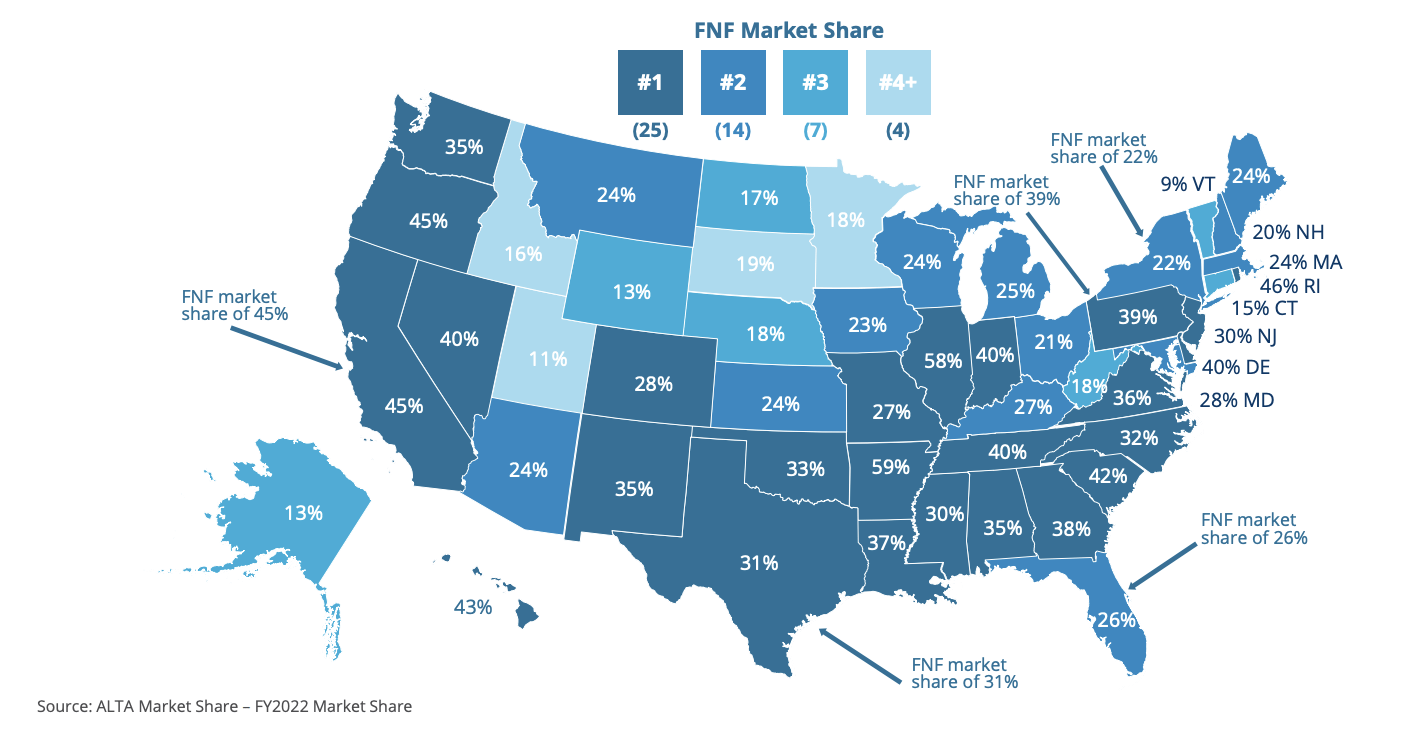

In the company’s third quarter results announced on November 7th, Fidelity reported adjusted earnings of $1.23, $0.08 ahead of estimates even as revenue fell 13% to $2.8 billion. FNF has 31% market share nationally in title insurance, making it the sector’s largest player. As the number of home sales has declined given higher rates, there have been fewer sales of title insurance. Whenever you get a mortgage, you need to buy title insurance to protect from someone claiming to actually own the property. In the event they actually do, the insurance will cover the losses. As you can see below, FNF is the biggest or second biggest insurer across most states.

{kind=link}

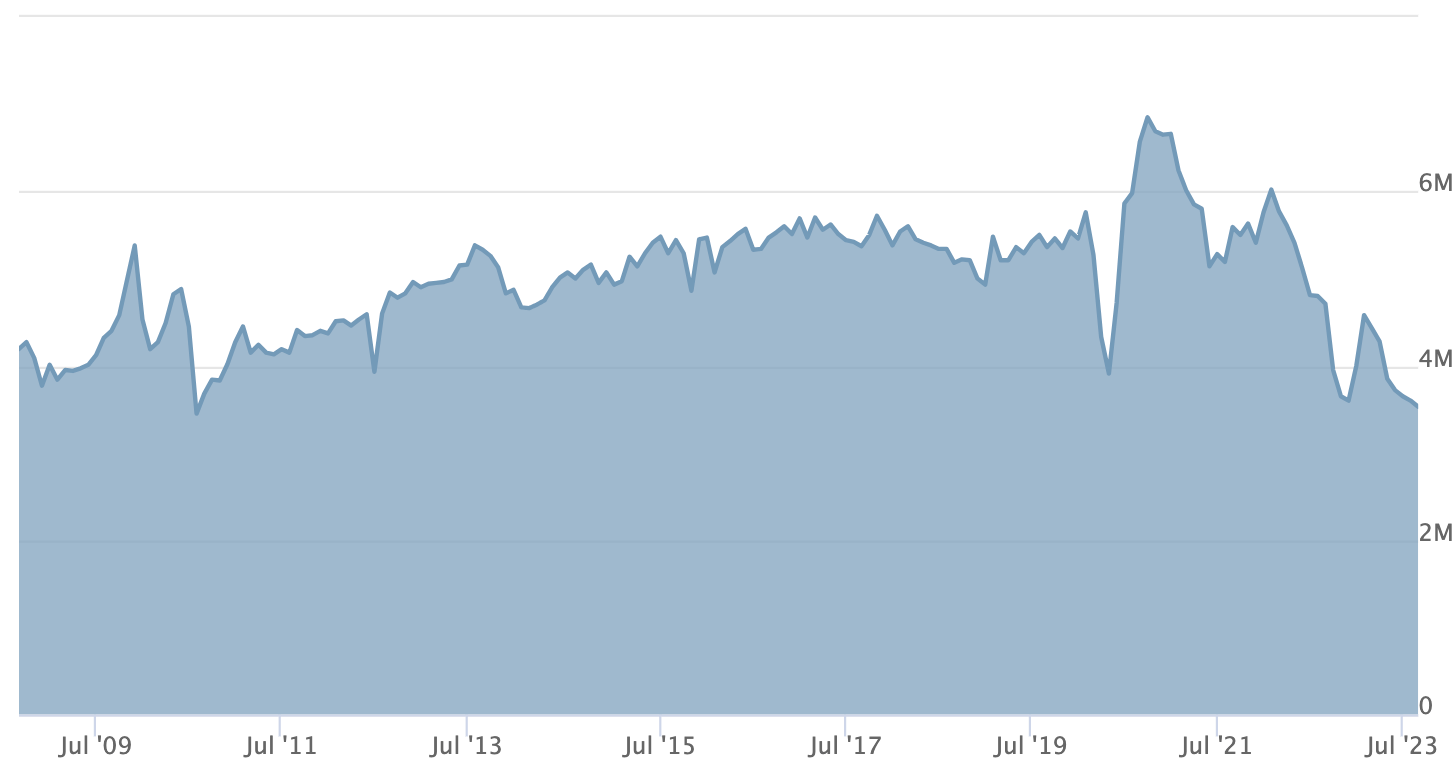

Because of its large size, FNF is relatively immune to different geographical trends with its results driven by national housing market activity. Unfortunately, this has slowed significantly. As you can see below, existing home sales have fallen sharply and are now below pre-COVID levels. Homeowners with a low mortgage essentially have “golden handcuffs” as moving means they would replace a 3-4% mortgage with a 7-8% one. As such, existing owners are loathe to sell, reducing inventories and transactions.

{kind=link}

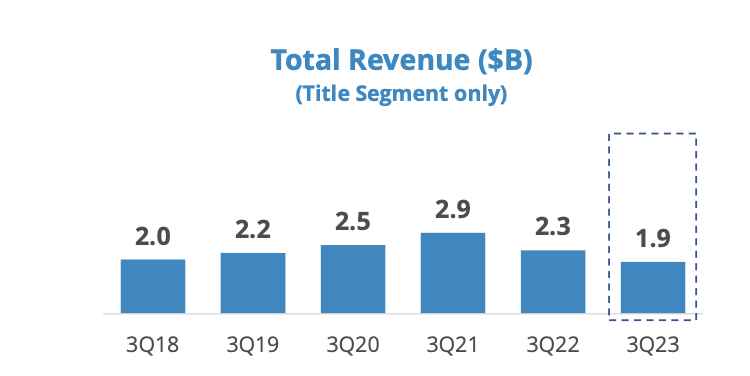

This is evident in Fidelity’s results. Title revenue fell 18% to $1.9 billion. Of this, about 82% of premiums comes from the residential market and 18% from commercial transactions. Open purchase orders ended the quarter down 7%, open refi orders down 25%, and open commercial orders down 10%. There is seasonality to the business as most home buying occurs in Q2/Q3. As such, open orders were down 6% in October from September at 4,600 per day, a similar decline as seen last year. As you can see below, title revenue has unwound all of it COVID gains and is now running below 2018 levels, in keeping with lower existing home sales.

{kind=link}

In response to this, FNF has tried to downsize its expenses. Field operations headcount has been reduced from 12,000 to 10,400. Still, just given how sharply demand has fallen, personnel costs were 35.8% of title revenue, up from 31.8% last year, even as they fell from $725 million to $654 million. This loss of operating leverage has pushed adjusted pre-tax margin to 16.2%, down from 17.1% last year. FNF has been able to keep pricing stable, at least, with average fees at $3,618.

Accordingly, pre-tax earnings were down to $311 million from $400 million in the quarter with adjusted net income of $245 million from $298 million last year. The lone offsetting positive was that interest and investment income rose to $92 million up from $62 million last year.

FNF has a small investment portfolio, holding $5.4 billion of tangible assets against its insurance reserves. Its investment portfolio is very high quality, primarily sitting in cash and short-term securities, with yields implicitly tied to the Fed funds rate. As the Fed has raised rates, FNF’s interest income has grown.

Fidelity National

Still, even with its higher interest income and lower title premiums, interest only accounts for about a quarter of net income. This is a helpful boost, but it will not drive results by itself. Given the short duration of its portfolio, FNF has enjoyed the vast majority of higher rates with further tailwinds unlikely to be more than $10 million per quarter.

Going forward, the company is focused on expenses and will manage headcount to demand levels. Importantly, the holding company has $949 million of cash and short-term investments. This provides ample capital and liquidity to provide returns to shareholders. Out of caution, FNF has essentially halted buybacks with only $4 million in repurchases so far this year. Alongside earnings, FNF raised its dividend by 7% to $0.48, giving shares a 4.4% yield. This costs the company about $500 million. Given excess liquidity at the parent and the fact the company is still solidly profitable, this dividend is quite secure in my view.

In last year’s Q4 , FNF earned $180 million in adjusted earnings. Given the fact orders are down from last year but interest expense is higher, we are likely to see a modest decline in earnings to about $150-$170 million. FNF has generated $586 million in adjusted earnings this year from its title business, meaning full year earnings will be about $740-750 million.

Having reviewed the title business, let me briefly discuss Fidelity’s 85% ownership of F&G. At today’s market levels, this stake is worth about $4 billion. Fidelity just announced plans to invest a further $250 million into F&G to accelerate its growth prospects, given the strong spread its investment portfolio is generating and the demand for annuities. That will reduce holding company cash to $700 million. Essentially, FNF is moving excess capital out of its struggling title unit an into its growing annuities company, which makes sense. I recently wrote on F&G where I saw 13% upside, or about $500 million for Fidelity’s stake. In terms of valuing FNF, I recommend looking at its business ex-F&G and then adding the market value of its stake. For those interested in a more in-depth view of F&G, I recommend my analysis on that company.

I would also note that FNF will keep at least an 80% ownership stake of F&G. By doing so, FNF can spin out these shares to its shareholders in a tax-free transaction since it has control, under IRS rules. FNF has to wait five years since acquiring control to do so, which will happen after 18 months from now. The ultimate end-game may be a spin-out or it may hold F&G for longer, but it is unlikely to do anything to reduce its stake and thereby limit its options until Q2 2025.

At its current share price, FNF has a $12 billion market capitalization. Taking out it $4 billion stake in FG, FNF’s title unit is being value at $8 billion or about 10.5x this year’s earnings. That is not a bad valuation. Frankly, I do not think the title business can do that much worse with revenue having fallen below 2018 levels. However, given the rate environment, I struggle to see an argument for why the volume of home transactions will increase anytime soon. As I’ve discussed when looking at other companies, I think we are likely to see persistently little housing turnover given how many have very low-rate mortgages.

As such, while FNF’s earnings are unlikely to fall much further, particularly if it can reduce headcount, I expect them to remain in the $750-$800 million level ex-F&G through 2024, if not longer. That will support the dividend safely but I do not think investors should be eager for exposure to home transaction volumes. Fidelity’s management is moving capital out of FNF and into FG with this just-announced $250 million transaction. I recommend following their lead; and when you can buy FG directly, there is no need to own FNF. Shares likely have limited downside at this valuation, but are likely to be dead money in my view.

For further details see:

Fidelity National: High Mortgage Rates Limit Upside