ADYEY - Fidelity National Information Services: A Fair Yield And A Fair Price

2023-06-27 05:58:31 ET

Summary

- Fidelity National Information Services has strong fundamentals but has experienced a significant pullback due to issues with its Worldpay acquisition.

- New management is focusing on cost-cutting and operational streamlining, which should boost results and stabilize the stock price.

- Selling put options on FIS presents an attractive strategy to capitalize on the current market situation, with a high probability of success and immediate cash-on-cash return to investors.

When it comes to quality operations and robust business models, Fidelity National Information Services (FIS) consistently stands out amongst the crowd. Despite its strong fundamentals, recent fumbles with the company's Worldpay acquisition have dented cash flow, and the stock has experienced a significant pullback in recent months, placing it in an oversold territory. New management has seen the light, which presents a compelling case for adopting a short put strategy to generate income and mitigate risk. This strategy not only allows us to capitalize on the current market sentiment around FIS, but also serves as an optimal entry point into this potential high-quality name, should shares get assigned.

Let's jump in.

Financial Results

In the most recent quarter, FIS reported mixed financial results.

On the positive side, the company reported beats across the board, with EPS coming in 9 cents higher than expected, at $1.29. Revenue of $3.5 billion also beat by almost $100 million. However, not remains rosy for investors.

Revenue did end up beating, but revenue growth came in at only 0.52% YoY, which is extremely meager for a company with such a strong moat and overall operational advantages.

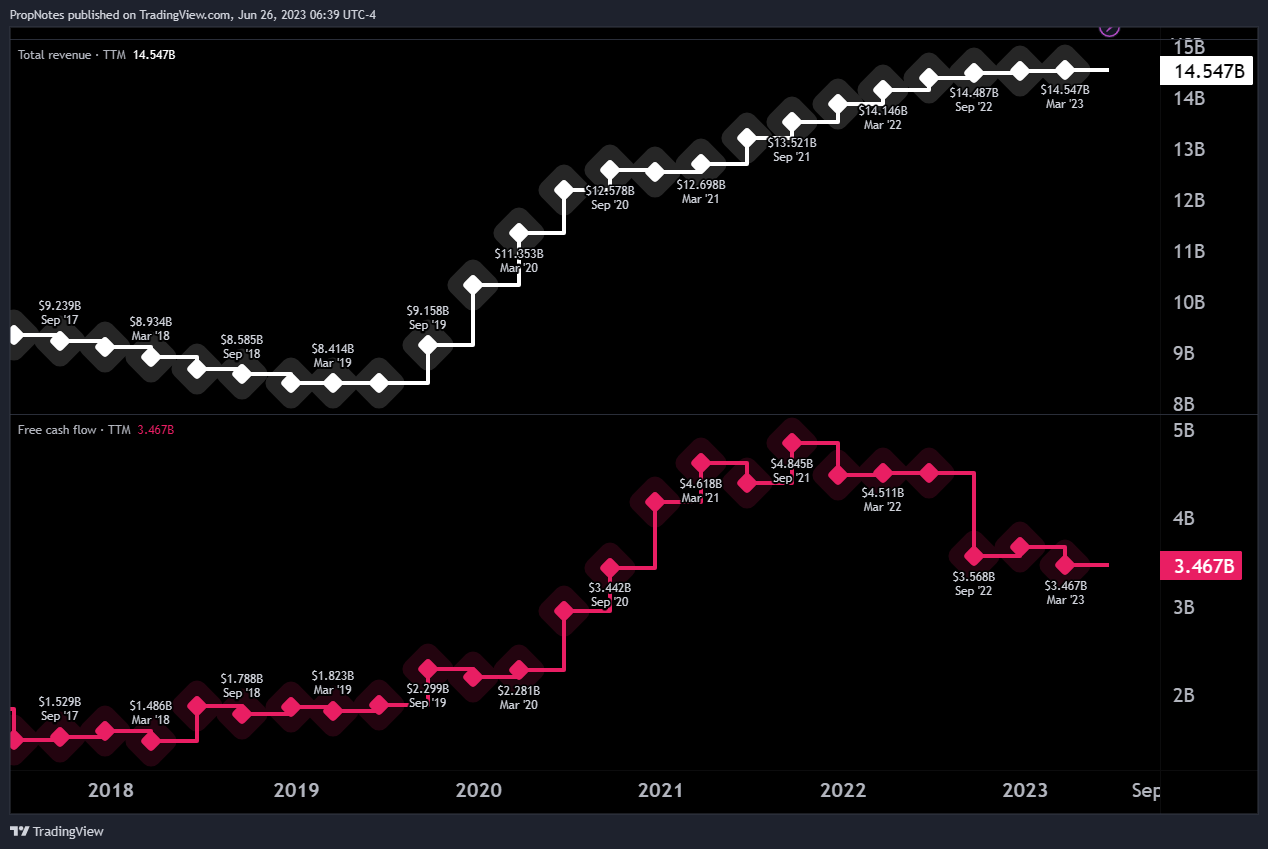

Additionally, free cash flow continued to trend sideways, indicative of middling cash conversion and worsening margins:

Seeking Alpha

Zooming out, we can see these data points are part of a larger trend.

TTM Revenue growth has been decelerating, and free cash flow has actually declined significantly to $3.46 billion vs. highs in 2021 close to $5 billion:

{kind=link}

But what's behind this recent slowdown? As James Long explained in his excellent recent article dissecting problems with the stock, the primary cause of the margin and FCF deterioration has to do with the company's recent Worldpay acquisition:

FIS [bit off] more than it could chew with this acquisition because the global scale of this Merchant Solutions segment, which ranges in size from small retailers to large enterprises spread across more than 140 countries, requires an enormous sales team in order to meet and service clients.

The 40.6% revenue boost post-Worldpay from FY 2019 to FY 2022 came at the cost of incurring far higher Selling, General, and Administrative expenses which increased by 71.1%.

In short, Worldpay increased revenue considerably by adding a new "Merchant" segment, but it also added significant new complexity to FIS's business and overall operational structure. This has sent profits lower.

Thankfully, new management has seen the light. Stephanie Ferris, formerly the CFO of Worldpay and the new CEO of FIS, had the following to say in a recent earnings call :

FIS is returning to its roots ... As a quality compounder, FIS will emphasize steady recurring revenue growth, consistent margin expansion and disciplined capital return to shareholders.

This essentially means significant cost cutting and operational streamlining will be top priority for management in the short and medium term. This should boost results and stabilize the cratering stock price.

Technicals

And crater, it has.

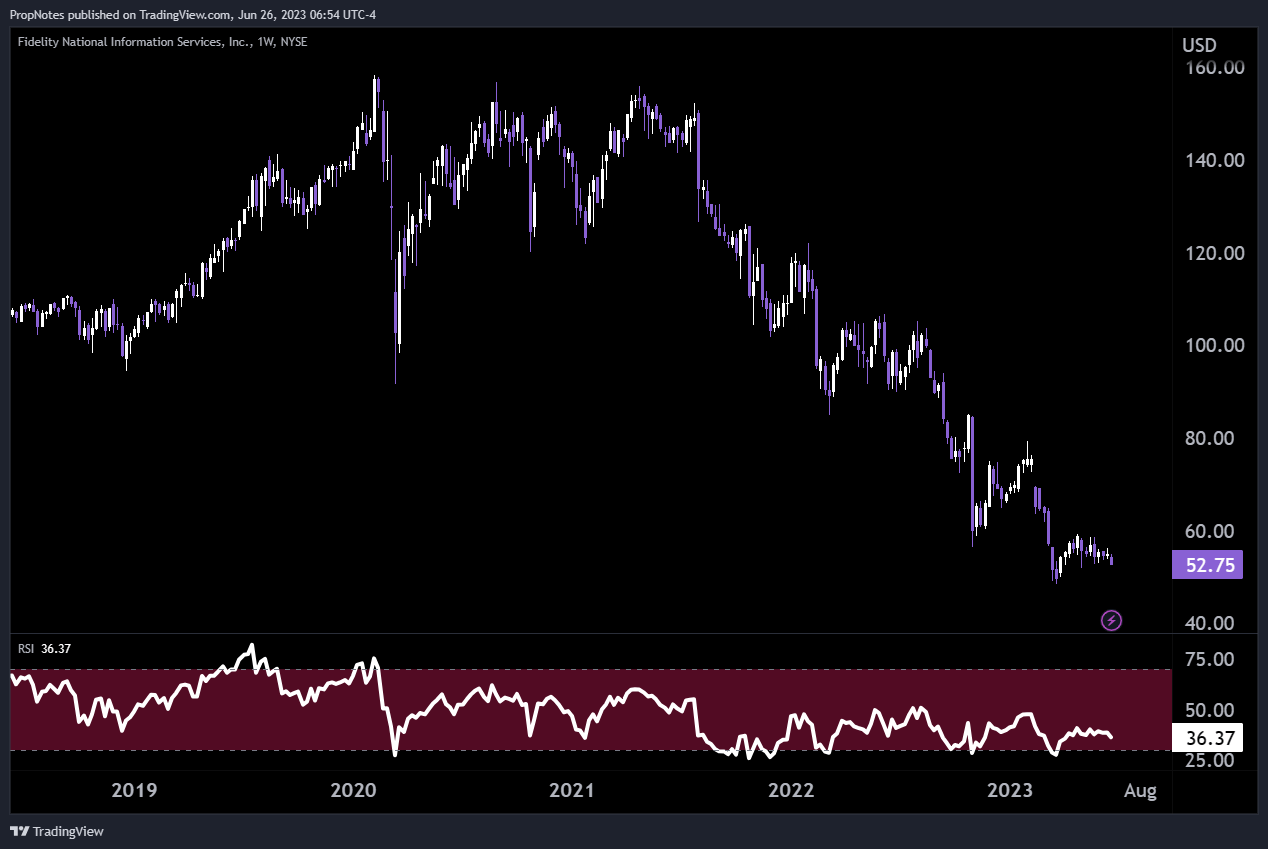

For the last two years, FIS's stock has gotten beat up, declining more than 66% from highs in 2022 through Friday's close:

{kind=link}

Additionally, the 14-week Relative Strength Index ((RSI)) has dipped below, and is now hovering just above, 30, indicating that the stock is in oversold territory and could be due for a bounce.

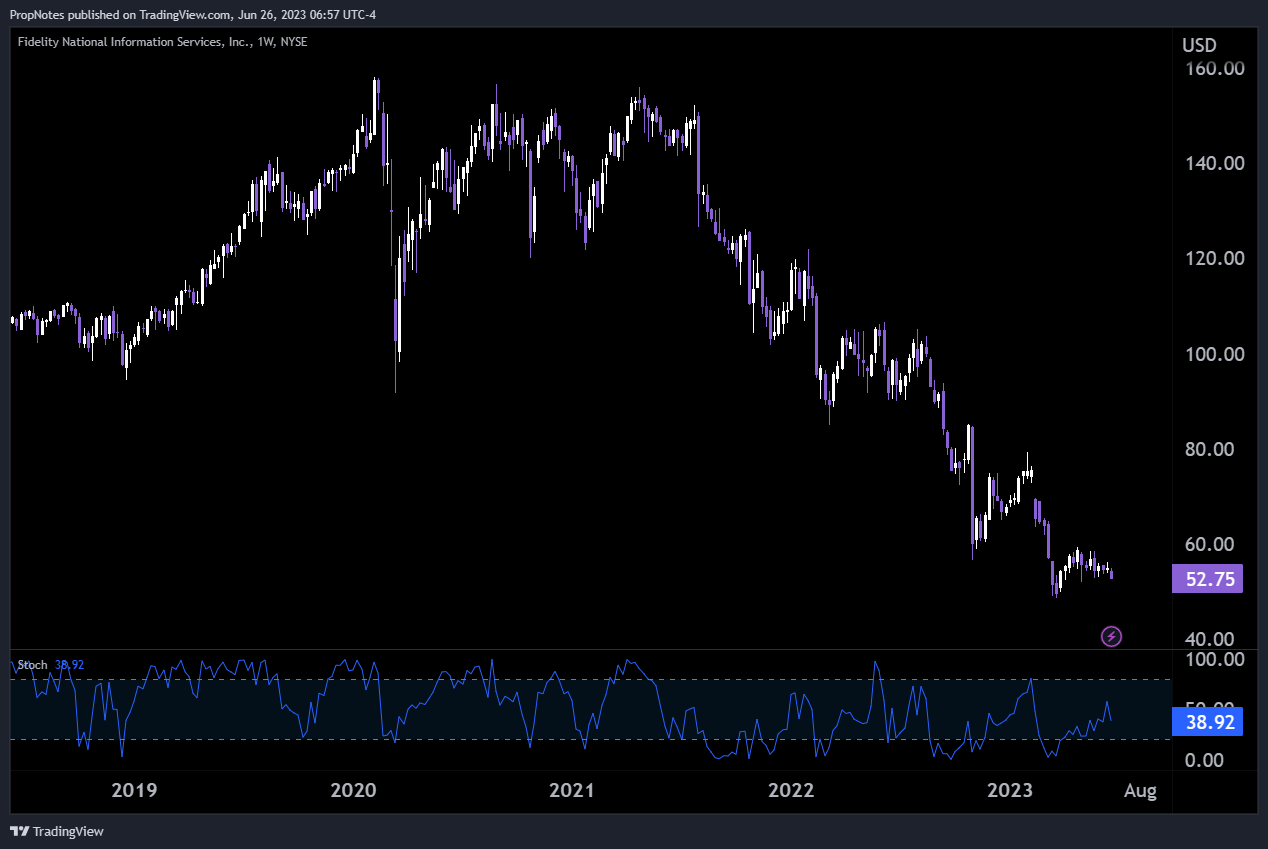

Adding probability to this thesis, the stock's stochastics are also hovering in the just above the oversold range, further supporting the notion that selling pressure may have limited remaining effect on the stock:

{kind=link}

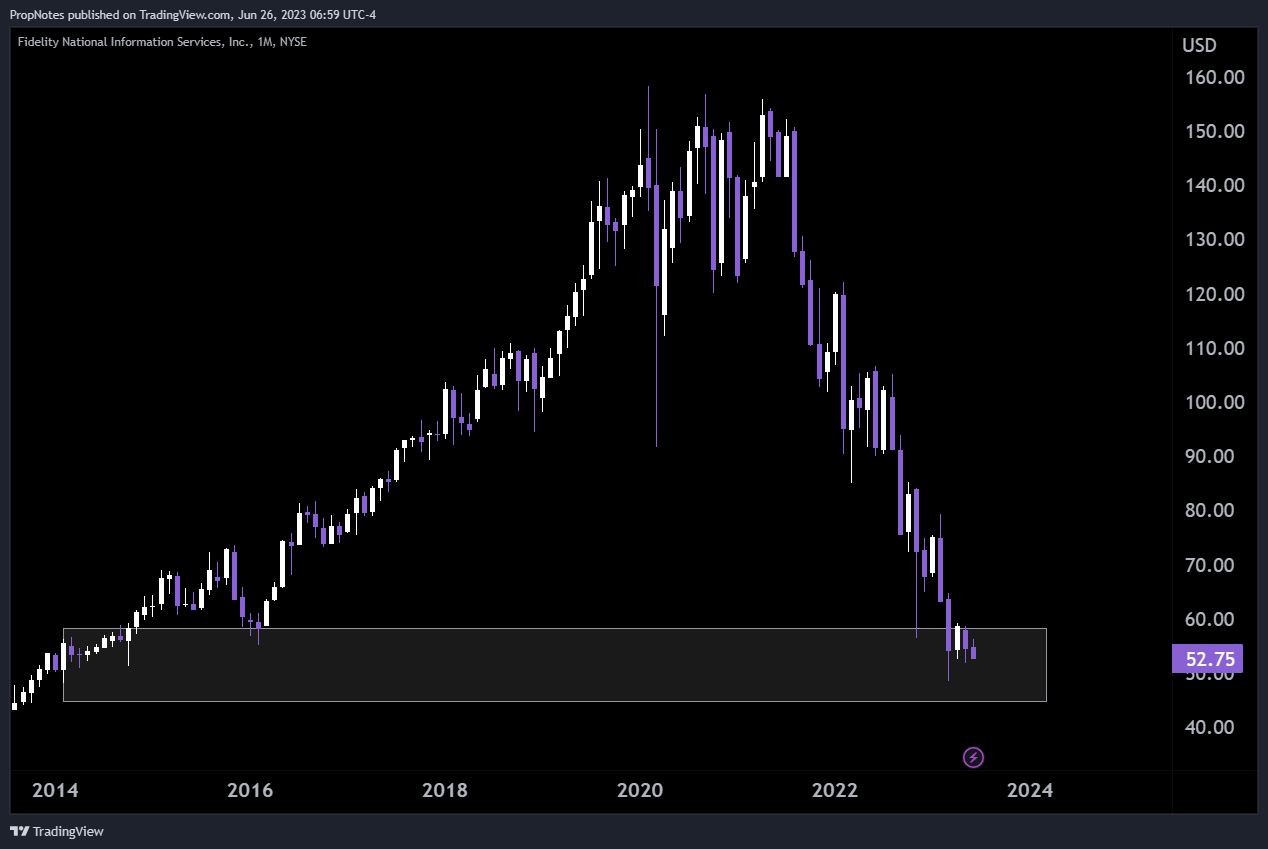

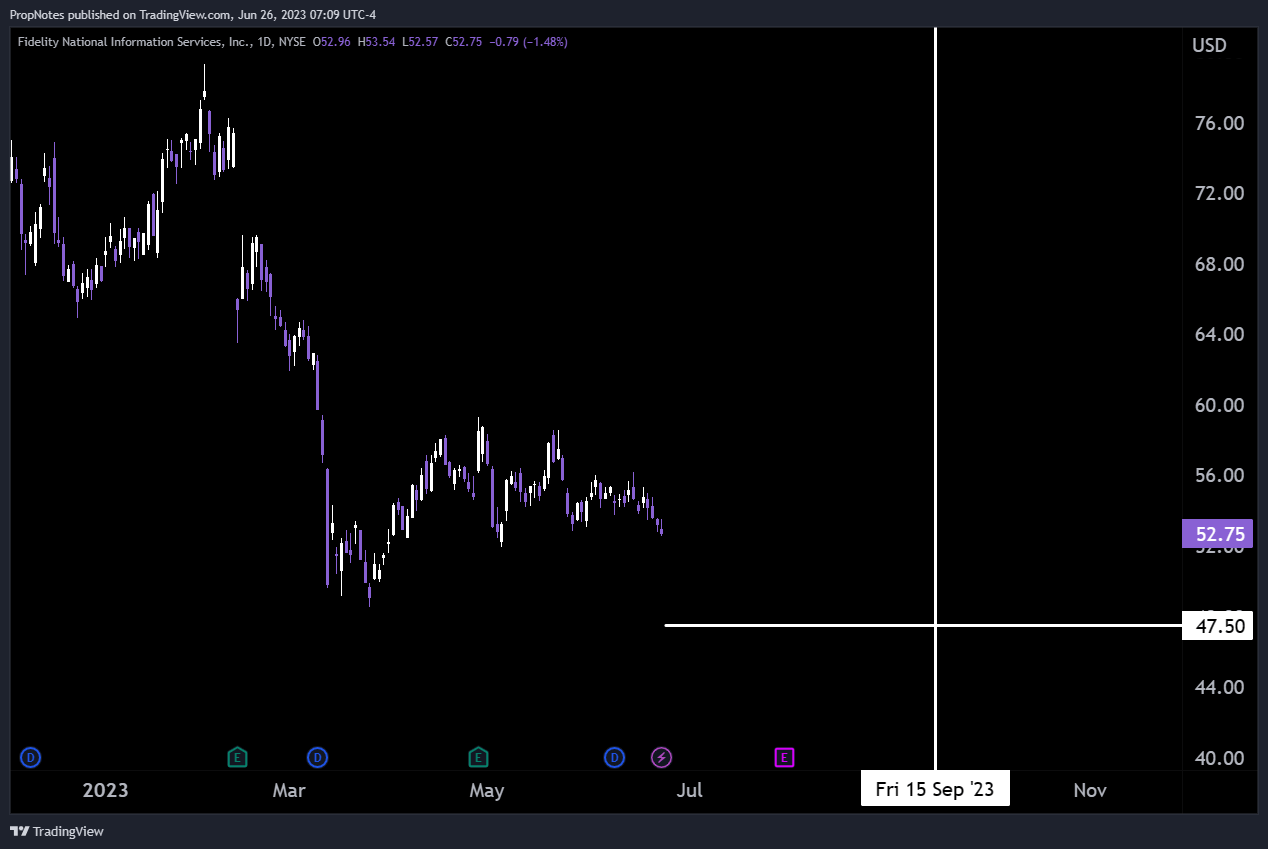

Last but not least, the stock is trading into a significant level of support between $45 and $60 per share, which can be seen here:

{kind=link}

Taken together, these technical readings and levels indicate that sellers are possibly becoming exhausted, which could allow for buyers to step in, causing a rebound in the stock price.

At the very least, they indicate that selling in the name may be slowing, and near-term risks could be mitigated with an opportunistic option strategy.

The Trade

Given the current market conditions, an attractive strategy to capitalize on FIS's situation is selling put options. For those unfamiliar, selling a put option means you're agreeing to buy shares of a stock at a specific price, known as the strike price, up until a specified expiration date.

In exchange for taking on the risk of being a guaranteed buyer at a given price, you get paid a premium, which serves are your return on the trade.

Currently in FIS, we like the September 15th, $47.5 strike put options as candidate for a put sale:

{kind=link}

They are currently bid at $1.50, which translates to a 3.2% cash-on-cash return over the next 81 days. This annualizes to 14.6%, which seems quite attractive.

Should FIS's stock stay above $47.5 by September 15th, our put option will expire worthless, meaning that we keep the full premium, no strings attached. If the stock falls below $47.5, we're obligated to buy the shares at that price. Given the recent positive developments around the company's expense structure and the advantageous technical setup, we think this trade looks like a solid win-win, either in earning the return, or acquiring the shares under $50.

Risks

While the trade idea presents a high probability of success, boasting more than a 75% chance of max profit by expiry, one always needs to be aware of the risks associated with a given trade idea or equity story. Here's a few key risks we're wary of:

Business Execution : FIS's needs to effectively manage its costs very carefully over the next few quarters. As a result of the Worldpay acquisition, costs have ballooned, and if the CEO's aforementioned intentions don't match actions with regards to improving free cash flow, then the market will likely re-rate this stock lower.

Competitors : Not necessarily in the banking segment, but in the Merchant segment there are a number of competitors, including PayPal ( PYPL ), Block ( SQ ), Adyen ( ADYEY ) and Stripe. If these vendors begin taking share away from FIS's Worldpay brand, then top line growth could be hurt and investors may sell the stock, putting downward pressure on the share price.

Debt : With a sub-1 current ratio and a long term debt pile standing at more than $10 billion, the company needs to monitor its debt risks closely. The CEO has affirmed her commitment to maintaining an investment credit rating from the agencies, but should that change, it's likely the stock would see material downside.

Earnings : Company earnings are due out on the first of August, and the event may cause a large swing in the price of the stock. Over the last year, previous market reactions to earnings have been relatively explosive, which leads us to believe that put sellers may end up acquiring shares at a higher-than-market average price, which could cause losses.

Technical Sentiment : As we laid out in the article, we believe that FIS's stock is significantly oversold. However, trends are trends for a reason, and there's no reason to suspect that we have called the exact bottom here - further selling momentum may exist in the stock, which could send shares below the strike price we mentioned in the trade idea. If the stock breaks the recent support level around $48.5, we would expect further downside.

Summary

In conclusion, FIS presents a compelling opportunity in the current market context. Despite facing some recent challenges, the firm's robust historical performance, characterized by strong revenue growth, impressive cash flow generation, and capital return to shareholders, should be achievable once again.

In the likely event that happens, the current valuation (9x FCF) and oversold condition make a short put trade at the current moment a highly attractive scenario; either yielding an excellent short-term return, or a great long-term entry.

For further details see:

Fidelity National Information Services: A Fair Yield And A Fair Price