FIS - Fidelity National Information Services Is An Interesting Long-Term Play

2023-05-07 06:11:12 ET

Summary

- Shares of Fidelity National Information Services are trading for an attractive valuation.

- Investors in the financial sector are concerned regarding sector stability, yet Fidelity National Information Services is poised to stay stable.

- Therefore, I believe Fidelity National Information Services is a BUY in the current environment.

Introduction

As an investor in a dividend growth company, I seek new investment opportunities in income-producing assets. I often add to existing positions when I find them attractive. I also use market volatility to my advantage by starting new positions to diversify my holdings and increase my dividend income for less capital. In this article, I will look into a new company I do not own yet.

The financial sector is attractive nowadays as it is constantly in the media. There is a great fear regarding the strength of the banking system, mainly smaller regional banks that have taken significant risks. The entire sector suffers from negative sentiment, and it is an excellent time to seek resilient investments in the industry. Fidelity National Information Services ( FIS ) is one of them, as it provides services to the sector.

I will analyze Fidelity National Information Services using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company's fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it's a good investment.

Seeking Alpha's company overview shows that:

Fidelity National Information Services provides technology solutions for financial institutions and businesses worldwide. It operates through Banking Solutions, Merchant Solutions, and Capital Market Solutions segments. The Banking Solutions segment provides core processing and ancillary applications for mobile and online banking, fraud, risk management, and compliance. The Merchant Solutions segment offers small- to medium-sized businesses acquiring, enterprise acquiring, and e-commerce solutions. The Capital Market Solutions segment provides investment operations and data, lending, trading and processing, and treasury and risk solutions.

Fundamentals

Sales are up almost 150% over the past decade. The company is increasing sales by increasing software prices, reaching more clients, and acquisitions. The company acquired Worldpay in 2018 for $43B. The combination of organic and inorganic growth led to this phenomenal growth. In the future, as seen on Seeking Alpha, the analyst consensus expects Fidelity National Information Services to keep growing sales at an annual rate of ~4% in the medium term.

The EPS (earnings per share) when using non-GAAP metrics increased by 135% over the same period. However, the GAAP EPS has declined significantly as the company wrote down $17.6B of its investment in Worldpay. The acquisition failed due to the immense price paid and the non-cash impairment. The company is still generating significant cash, and the one-time write-off does not affect the daily business as the FCF per rose by 83% over the past decade. In the future, as seen on Seeking Alpha, the analyst consensus expects Fidelity National Information Services to keep growing EPS at an annual rate of ~10% in the medium term.

The company is a consistent dividend payer. The current dividend payment is $2.08 per share, following an 11% increase in February. The dividend seems safe as the payout ratio is roughly 35% when using non-GAAP EPS. The company has not decreased the dividend for almost twenty years, offering its investors a dividend increase almost yearly. Therefore, this 3.5% yield is extremely attractive.

In addition to dividends, companies return capital to shareholders via buybacks. Buybacks help companies support EPS growth by lowering the number of shares outstanding. Over the last decade, the number of shares outstanding has doubled. This is the result of share issuance used to finance acquisitions. Since the acquisition of Worldpay, the company has slowly decreased the number of shares and is executing buyback plans which are taking advantage of the current valuation.

Valuation

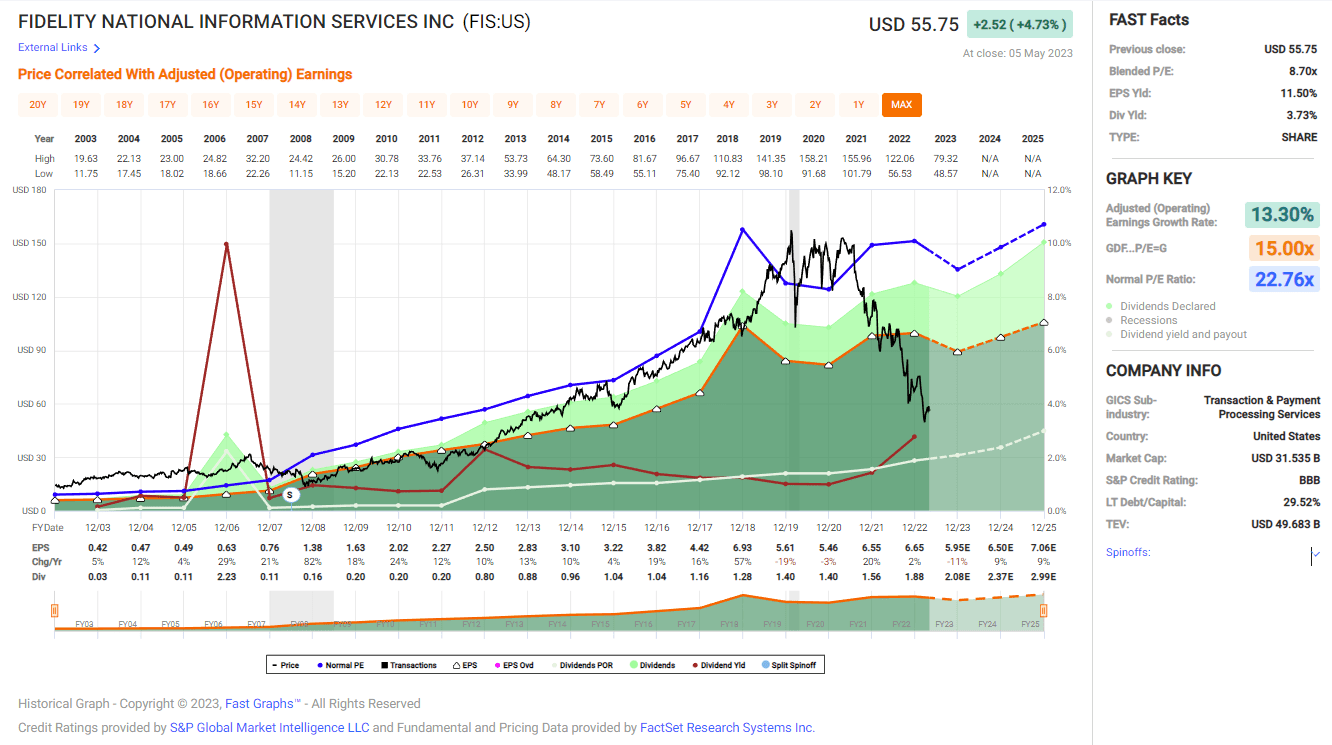

The company's P/E (price to earnings) ratio is 9 using the 2023 earnings estimate. Paying nine times earnings for a growing company seems attractive to me. Moreover, as the chart below shows, the current valuation is close to the lowest we have seen over the last twelve months. The ability to lock on a low valuation helps investors increase their margin of safety.

The graph below from Fast Graphs also emphasizes how attractively valued the share of Fidelity National Information Services share is at the moment. Over the last two decades, the company's shares traded for an average P/E ratio of 22.8. The current P/E ratio is more than 50% lower. In addition, the average growth over that period was 13.3% a year, and the current growth expectations are ~10% a year. Therefore, while some discount is needed, the company's current valuation is extremely attractive.

{kind=link}

Opportunities

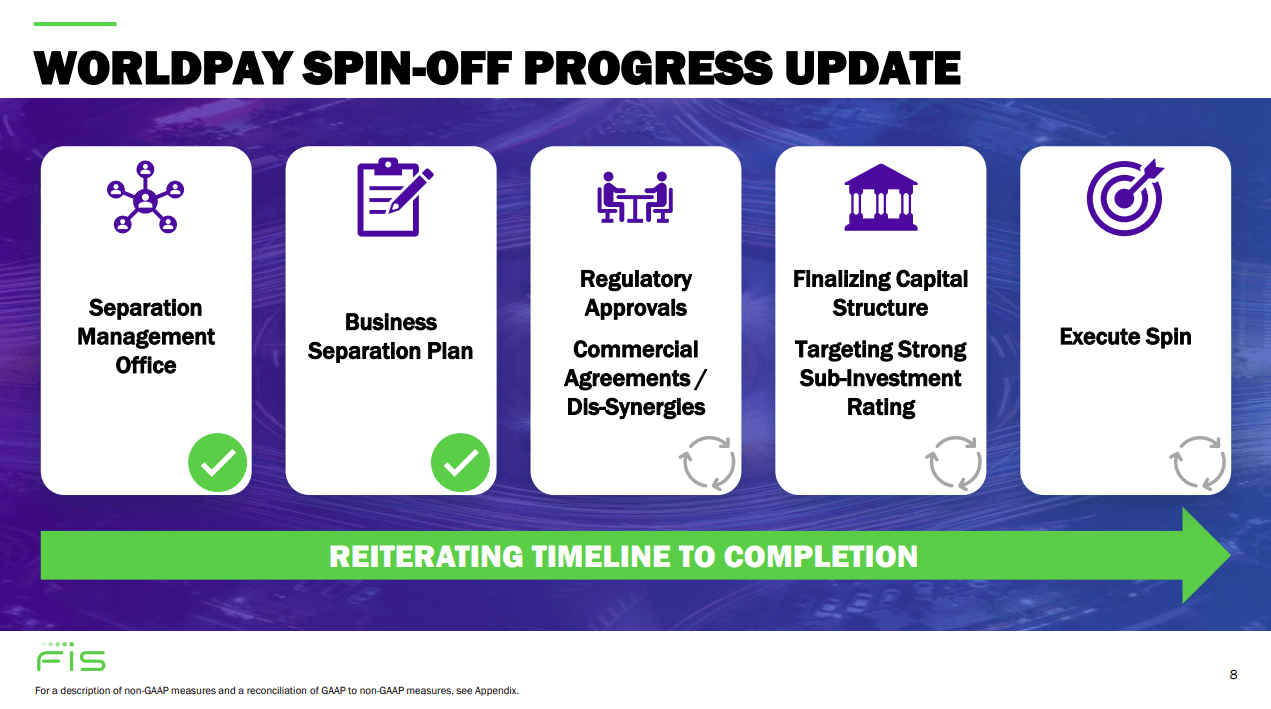

The spinoff of Worldpay is the first opportunity. The spinoff will be beneficial for the company for two reasons. The first reason is that it will end the saga. The acquisition wasn't successful, and the company will shift its resources back to its core business, where it excels, instead of investing more into the new business. Moreover, we, the shareholders, can unlock value in Worldpay as an independent company. Studies have shown that spinoff companies tend to outperform the broader market.

{kind=link}

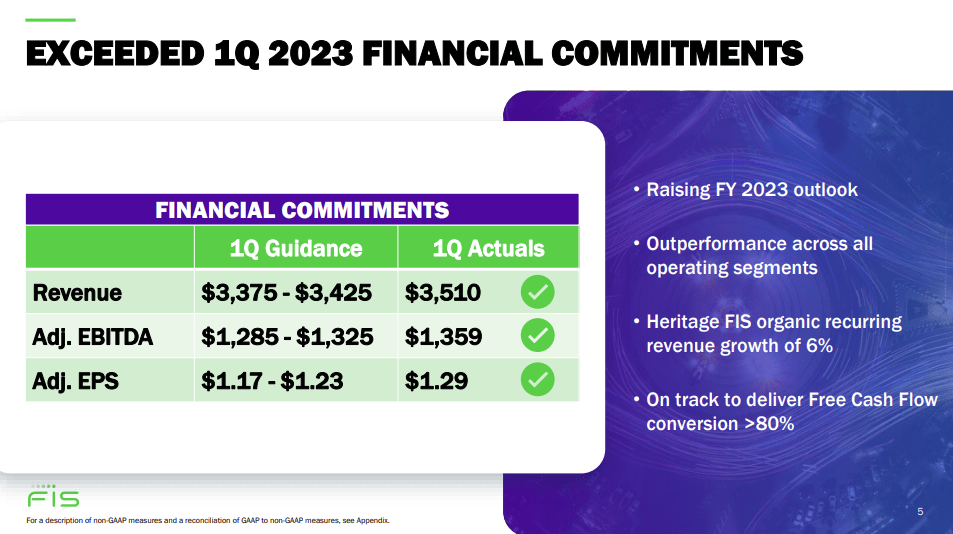

Improving outlook is another short-term opportunity. The company's valuation is depressed, as seen in the valuation section. The company performed well, and it beat the Q1 guidance significantly. It also raises the outlook for 2023. As the company keeps exceeding expectations and raising its outlook, we are more likely to see multiple expansions as investors realize that despite the challenges in the banking sector, FIS performs well.

{kind=link}

Another opportunity for the company is its product stickiness. The company offers banking and investment institutions a wide range of software solutions. It makes sense for the clients to use FIS for several use cases, and as the company is getting used to the software, it becomes much harder to replace it. Therefore, the company can raise prices, offer additional services to current clients, and enjoy an advantage over its peers.

Risks

The first risk for FIS is the world of Fintech. Many tech companies are trying to take market share from traditional banking and investment firms. These startups use their technology and software and are less likely to use FIS. This may hinder FIS's ability to grow sales and EPS as the traditional banking market may grow slower and even contract.

In addition, the current banking crisis may push toward the industry's consolidation. The banking industry is already consolidating, and a faster trend may create larger banks with more bargaining power and possibilities to address and solve their information technology needs. Some may do it in-house, while others may negotiate a better deal.

Moreover, FIS may see limited growth because 40% of its revenues are transaction-based. If we see fewer banks and a recession, there will be less action and usage: fewer money transfers and fewer stock transactions. In addition, growth may also be slowed due to the high cleavage as the company cannot grow using acquisitions before it deleverages. The management is committed to repaying debt quickly, but it is still a long process.

Conclusion

Fidelity National Information Services is a great company. It has made a mistake with the acquisition of Worldpay, and it now fixes it with a spinoff. Yet, the fundamentals are still excellent, and the valuation is extremely attractive. The company has several growth opportunities as it enjoys high stickiness and the ability to focus on its core business. There are several risks, but they do not jeopardize the positive outlook.

Therefore, I believe Fidelity National Information Services shares are a BUY at the current valuation with the current safe dividend yield. Investors can lock on an excellent dividend yield and take advantage of the low valuation. In addition, they will get shares of Worldpay that they can keep as a bonus. Combining the dividend with the EPS growth offers a decent opportunity.

For further details see:

Fidelity National Information Services Is An Interesting Long-Term Play