FIS - Fidelity National Information Services: Market Sentiment Is On The Wrong Side Again

2023-09-22 16:16:19 ET

Summary

- After losing nearly 60% of its value, FIS has turned into a bitter disappointment for shareholders, but this is likely to change.

- The management has made a major step in the right direction with the decision to sell its controlling stake in Worldpay.

- FIS appears too conservatively priced relative to its business fundamentals.

Fidelity National Information Services ( FIS ) has been nothing short of utter disappointment for shareholders over the past few years.

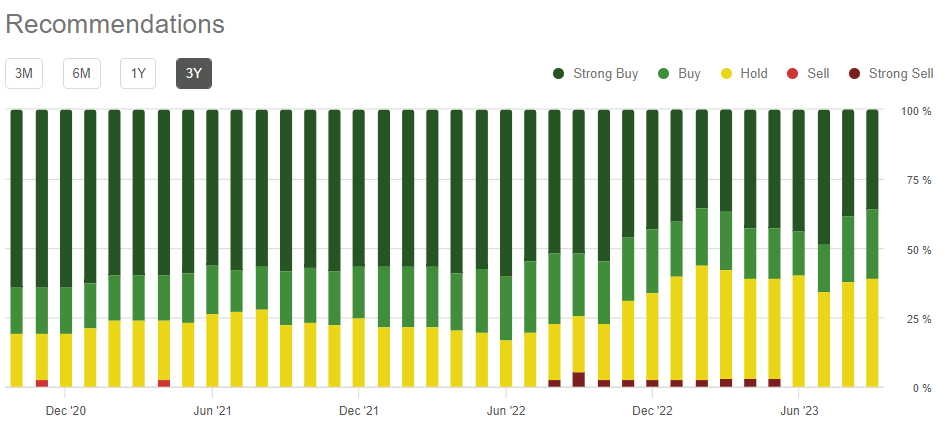

As usual, Wall Street Analysts have been caught once again on the other side of the fence with most of them covering the stock for the past few years being very optimistic about potential returns.

{kind=link}

Seeking Alpha

While almost all analysts have been optimistic on the stock for the past 3-year period, FIS lost more than 60% of its value at a time when the market appreciated by more than 30%.

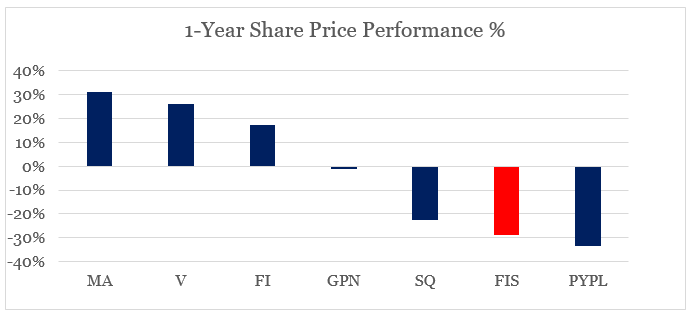

While various excuses about the sector could be given as an excuse for these embarrassing ratings, FIS has also become the second worst performer within its broader peer group.

{kind=link}

prepared by the author, using data from Seeking Alpha

The reason for this disparity between FIS's actual performance and analyst ratings is mostly due to capital allocation.

What analysts are usually pretty good at is assessing operational performance and forecasting financials over the next few months. But in the case of FIS, the main problem has been long-term capital allocation, which is rarely taken into account and has an impact on shareholder returns beyond the short-term.

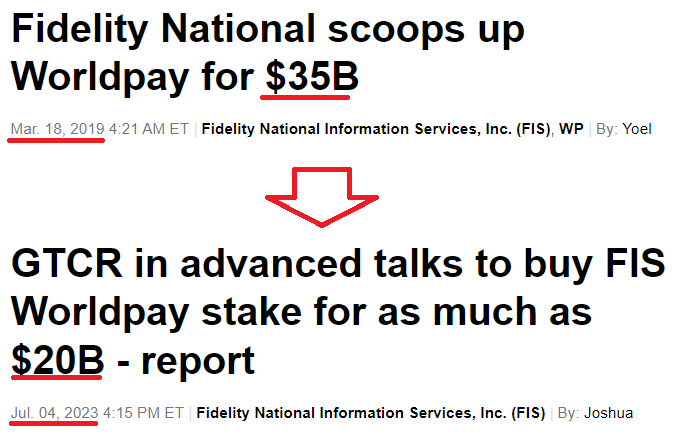

The topic of FIS's recent deal to sell the majority stake of Worldpay has been widely discussed, but in a nutshell it reverses a large deal to acquire the aforementioned company at a much lower price.

{kind=link}

Seeking Alpha

After struggling to live up to the expectations, the exceptionally large deal for Worldpay has uncovered problems within FIS's capital allocation process and shareholder value was ultimately destroyed.

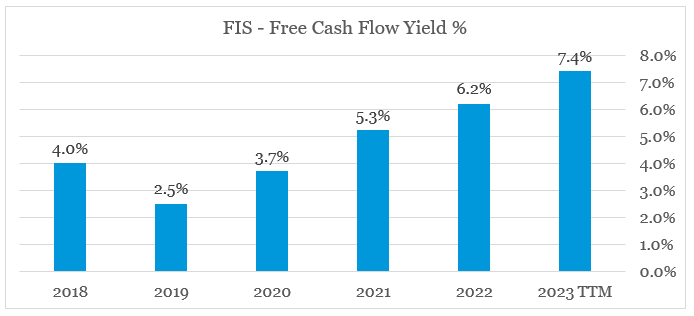

Having said that, however, the management has now changed, the company is being restructured and last but not least it is trading at one of the most attractive levels in a very long time. As we see down below, FIS now offers a free cash flow yield of 7.4%, which is nearly twice as high as it was back in 2018.

{kind=link}

prepared by the author, using data from SEC Filings and Seeking Alpha

Solving Capital Allocation

As I said already, the issue of capital allocation is already behind us. Although a significant amount of shareholder value has been destroyed as part of the Worldpay acquisition, it is now of crucial importance to look into the future.

Following the deal, Worldpay will be better positioned to grow as GTCT is committed to providing additional funds for inorganic growth opportunities and at the same time FIS will retain roughly half of the business.

{kind=link}

FIS Investor Presentation

More importantly, however, FIS will use the proceeds from the deal to significantly reduce its debt burden.

Second, the upfront proceeds of at least $11.7 billion will allow us to de-lever the balance sheet quickly, while simultaneously accelerating capital returns to shareholders at unique, attractive valuation levels.(...)

FIS will remain focused on reducing debt, paying an appropriate dividend and using excess capital for share repurchase or tuck-in M&A .

Source: FIS Q2 2023 Earnings Transcript

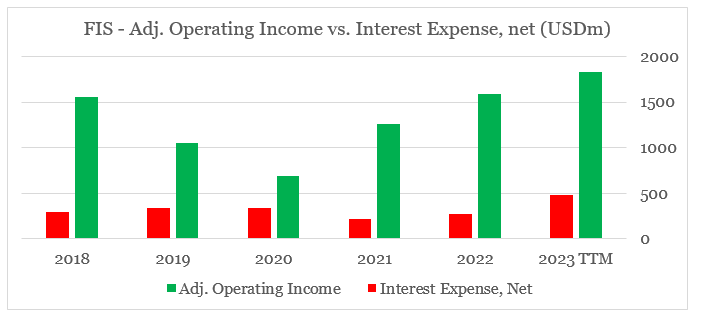

FIS's current debt load is under control at the moment, but as interest rates increase and are projected to remain high, the overall debt burden to FIS would have become much heavier. Net interest expense has nearly doubled since FY 2022 and now sits at less than 4x adjusted EBIT.

{kind=link}

prepared by the author, using data from SEC Filings

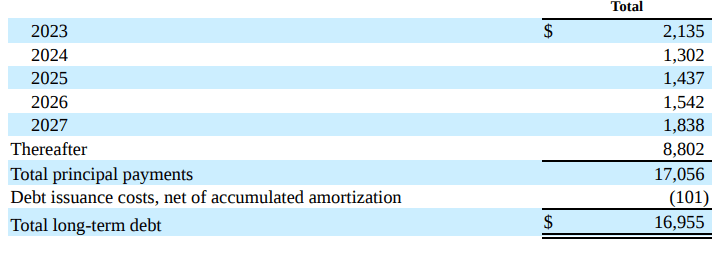

Although this might appear sustainable, the real problem that FIS faces when it comes to debt is the principal amounts due over the coming years.

{kind=link}

FIS 2022 10-K SEC Filing

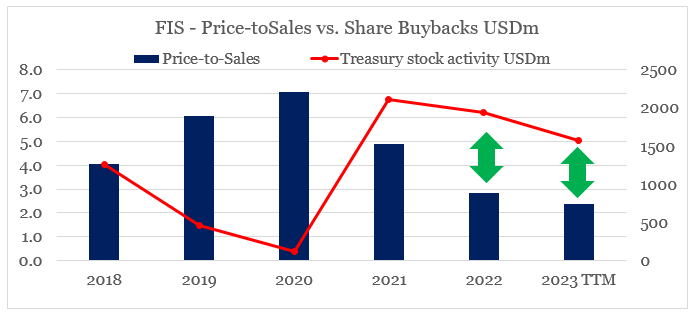

In addition to reducing its debt load, FIS management has made clear that they would use the proceeds from the deal for share repurchases. Historically, the company has a good track record of doing more share repurchases when the Price-to-Sales ratio is low and as we see from the graph below now is a very good time for the company to buyback more shares at lower multiples.

{kind=link}

prepared by the author, using data from SEC Filings and Seeking Alpha

Having said all that, the decision to dispose of the controlling stake in Worldpay is a step in the right direction for FIS's new CEO. It is also encouraging that the company would take a very different approach to its capital allocation process.

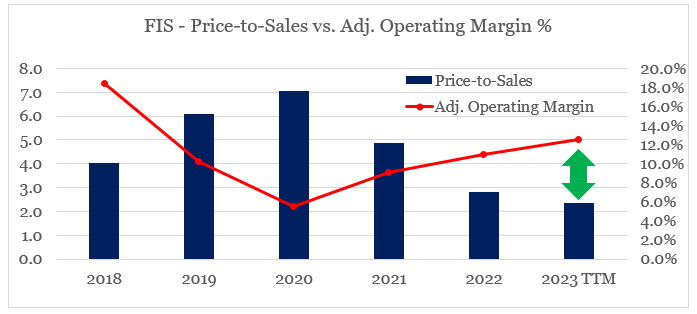

Better Business For Lower Price

Down below, we could see the same graph as the one above, but instead of plotting the total amount of share buybacks in red, I have shown FIS's Adjusted Operating Margin.

As opposed to the 2020 period, when price to sales reached 7x and FIS's margin stood at mid-single digits, now these two variables have reversed. Adjusted operating margin is now nearly 13%, while at the same time the company trades at slightly above 2x sales.

{kind=link}

prepared by the author, using data from SEC Filings and Seeking Alpha

In hindsight, 2020 has been a very bad period to go long FIS, but instead investors flocked into the stock at record levels. The opposite is now occurring, with the narrative around the company turning negative at the exact moment when it is becoming attractively priced relative to fundamentals.

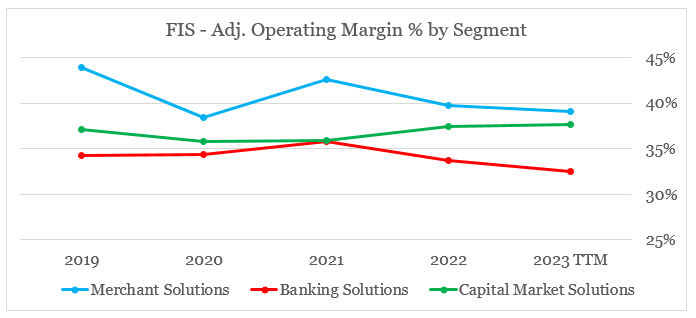

Looking ahead, we should recognize that with the sale of the controlling stake of Worldpay, FIS would give up more than half of its most profitable segment - Merchant Solutions and with that overall profitability will decline.

{kind=link}

prepared by the author, using data from SEC Filings

FIS management, however, sees margins at these two segments improving through the rest of 2023 which could largely offset the aforementioned decline.

On a combined basis, the Banking and Capital Markets businesses posted healthy recurring revenue growth of 4%. This represents a more normalized rate of growth within our 3% to 5% cycle range. Building on the profitability improvements we delivered in the second quarter, we are confident in our ability to deliver sequential adjusted EBITDA margin improvement over the course of 2023, led by improvement in the Banking Solutions segment .

Source: FIS Q2 2023 Earnings Transcript

By selling the controlling stake in Worldpay, FIS would also reduce its exposure to an area of the market where competition is intensifying and topline growth is hard to achieve.

{kind=link}

FIS Investor Presentation

Instead, FIS will focus on the segments where it has stronger competitive advantages and which will benefit heavily from a higher for longer interest rate environment.

Conclusion

After a painful decision to dispose of its controlling stake in Worldpay, FIS seems to be taking the right decisions to steer the business in the right direction. At the same time, profitability is likely to remain stable and the company trades at extremely conservative levels. In my view, the market is once again on the wrong side as FIS finally appears as an attractive long-term investment.

For further details see:

Fidelity National Information Services: Market Sentiment Is On The Wrong Side Again