FIS - Fidelity National Information Services: Why Does Seth Klarman Own 4.3% Of FIS?

2023-06-19 08:51:35 ET

Summary

- Fidelity National Information Services (FIS) appears undervalued with potential for significant capital appreciation in under three years, making it an attractive option for dividend growth investors.

- Despite its strong performance in the past, FIS has underperformed the market due to the Merchant segment that came from the Worldpay acquisition.

- The new management plans to divest this problematic segment to return to its roots.

- With new management in place and a focus on reducing costs and improving margins, FIS's future looks brighter, and analysts predict steady recurring revenue growth and consistent margin expansion.

Introduction

Seth Klarman should not need any introduction. He is a well-known deep-value investor, founder and CEO of the hedge fund Baupost Group, managing $30 billion in assets and as of 2018 was the 17th highest-earning hedge fund manager . He was even compared to Warren Buffett as the Oracle of Boston .

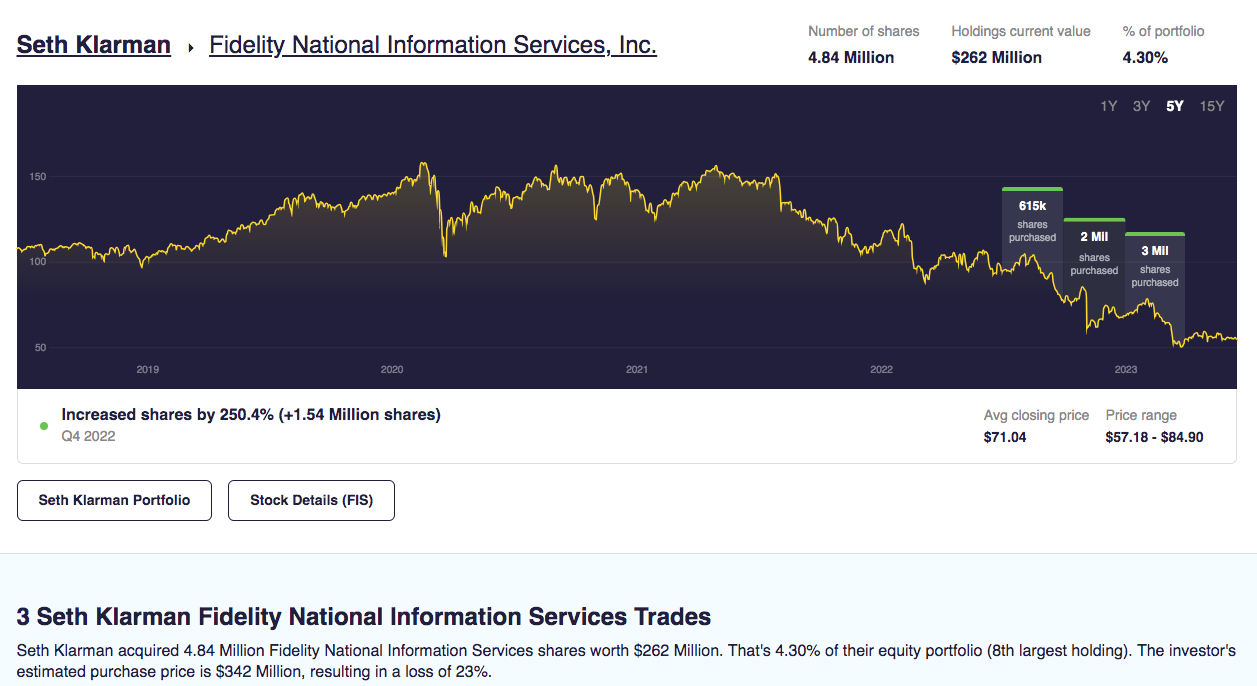

Therefore, when Seth Klarman starts a new position in Fidelity National Information Services (FIS), and a large one at that at 4.3% of his portfolio, I pay attention.

{kind=link}

At first glance, one might be surprised at his investment in FIS.

In slightly over two years from April 2021 to June 2023, FIS managed to lose 64% of its share price while SPY gained more than 10%. Why would anyone buy a stock that has been underperforming even the SPY?

{kind=link}

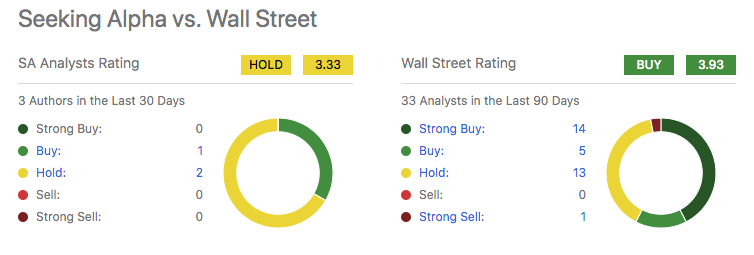

Moreover, most of the analysts on Seeking Alpha and almost half on Wallstreet have been cautiously calling for a HOLD rather than issuing BUY calls.

{kind=link}

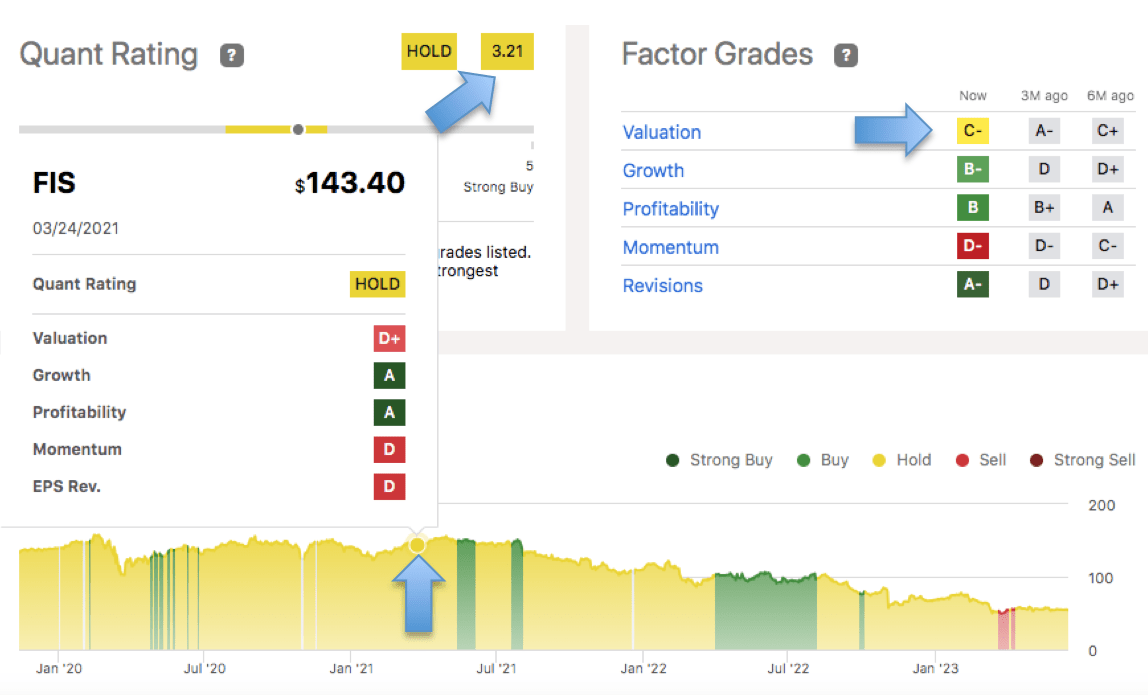

Seeking Alpha's very own quant system gave this stock a HOLD rating score of 3.21 (correct as of 18 June 2023) and it had called for a HOLD on FIS for most of the past three years. Seeking Alpha's Valuation grade has also deteriorated over the last three months.

{kind=link}

Lastly, more "Smart money" has been dumping FIS shares in the last seven months . From September 2022 to April 2023, the top 20 funds that sold shares of FIS sold 42,223,798 shares, with 17 of these 20 selling 100% of FIS shares. From December 2022 to March 2023, the top 20 institutions that sold shares of FIS sold 72,163,233 shares, with 7 of these 20 selling 100% of FIS shares and another 7 selling more than half of the FIS shares they own. Those figures representing the amount of FIS shares that were sold far exceed the FIS shares that were purchased by funds (20,697,845) and institutions (48,203,391).

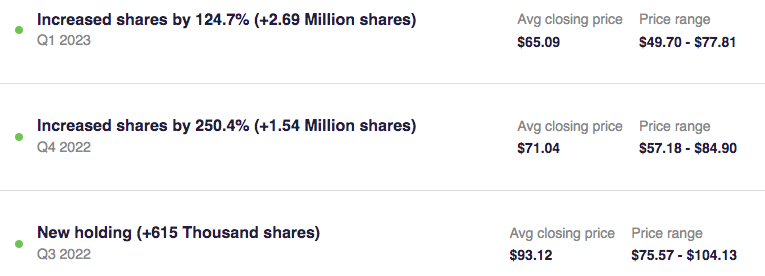

Yet, Seth Klarman bought FIS shares not just once but three times over consecutive quarters starting from Q3 2022 even as the stock price slid even more. And his largest infusion was done in the latest recorded purchase in Q1 2023 when he bought 2.69 million shares.

{kind=link}

In this article, I will seek to unravel the reasons behind Seth Klarman's decision to invest in Fidelity National Information Services ((FIS)).

To do that, we will need to have some appreciation of his investment philosophy.

Seth Klarman's Investment Philosophy

He is a value investor. In his book "Margin of Safety" (link to Amazon for a used copy is here ), he explained value investing as the process of determining the value underlying a security and then buying it at a considerable discount from that value.

In chapter six he delved into the concept of the margin of safety,

Because investing is as much an art as a science, investors need a margin of safety. A margin of safety is achieved when securities are purchased at prices sufficiently below underlying value to allow for human error, bad luck, or extreme volatility in a complex, unpredictable, and rapidly changing world. According to Graham, “ The margin of safety is always dependent on the price paid. For any security, it will be large at one price, small at some higher price, nonexistent at some still higher price ."

Once a bargain is found, the value investor then simply adopts the “buy a bargain and wait” strategy.

In one of his letters written to the limited partners who invested in his fund, he wrote,

The market is often a tease. When it's acting well is usually the worst time to invest, and when it acts poorly is usually the best . True investors don't continuously dart in and out of the market, they invest for all seasons.

Based on what could be gleaned from the above, does this mean that FIS has been so (1) undervalued that it offers Seth Klarman a margin of safety? Does this mean (2) he understood the potential of the business and the reasons for its underperformance (3) so he is buying it during a period of maximum pessimism , and (4) he was buying even more after he has seen some positive signs and he is confident that the downside is minimized while waiting for the upside ?

Let's examine those four premises.

FIS Is Deeply Undervalued

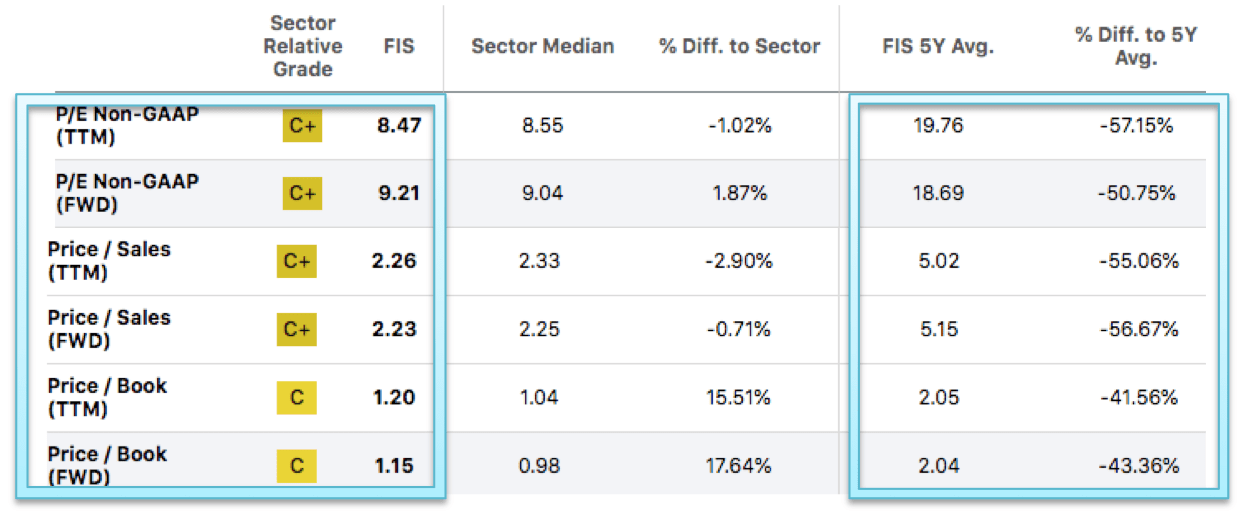

At a glance, you can see that Fidelity National Information Services ((FIS)) is undervalued . Making reference to traditional valuation metrics like P/E (non-GAAP), P/S and P/B, FIS is currently trading below its 5-year average of all these valuation metrics by around 41% to 57% each.

{kind=link}

But surely, a super-investor like Seth Klarman should not be basing his purchase of FIS simply based on depressed prices from its all-time-high alone, because if that is the only criterion then there are plenty of companies that had declined more than the 64% that FIS suffered.

He Understood The Potential of FIS's Business and the Reasons for Underperformance

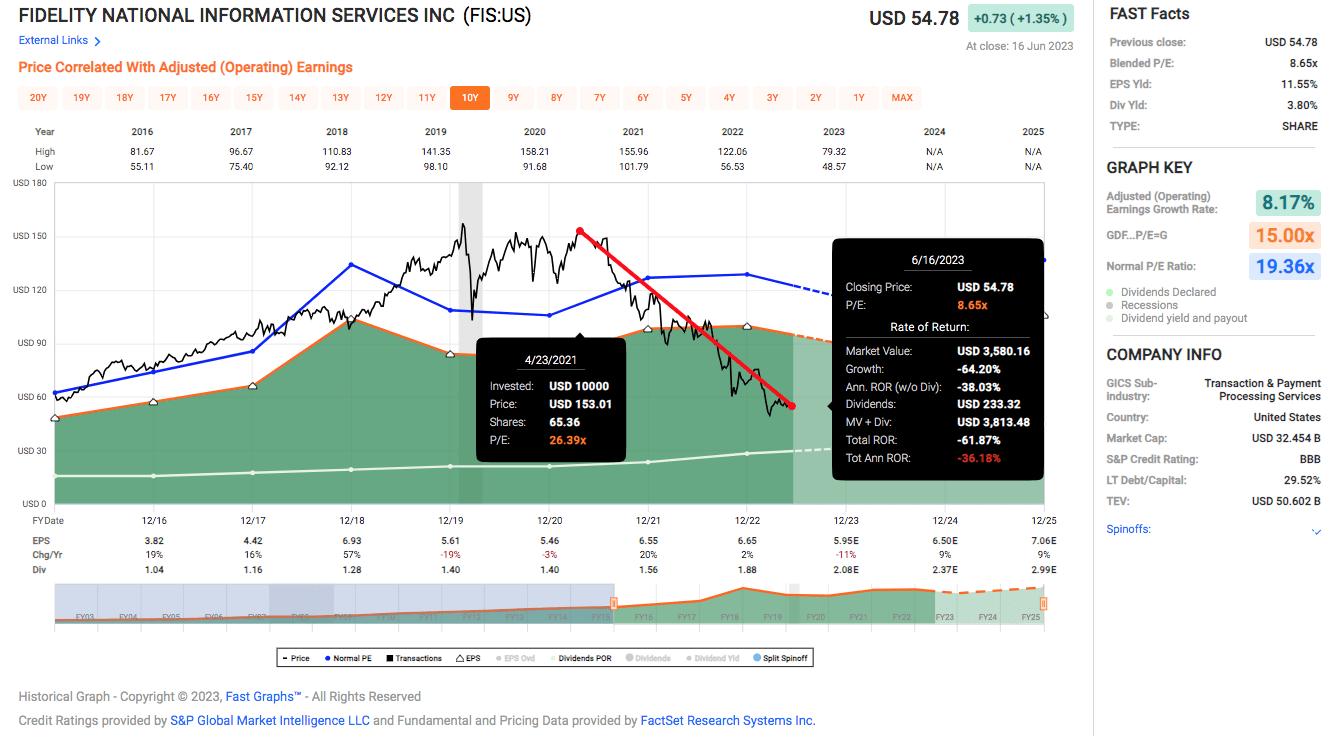

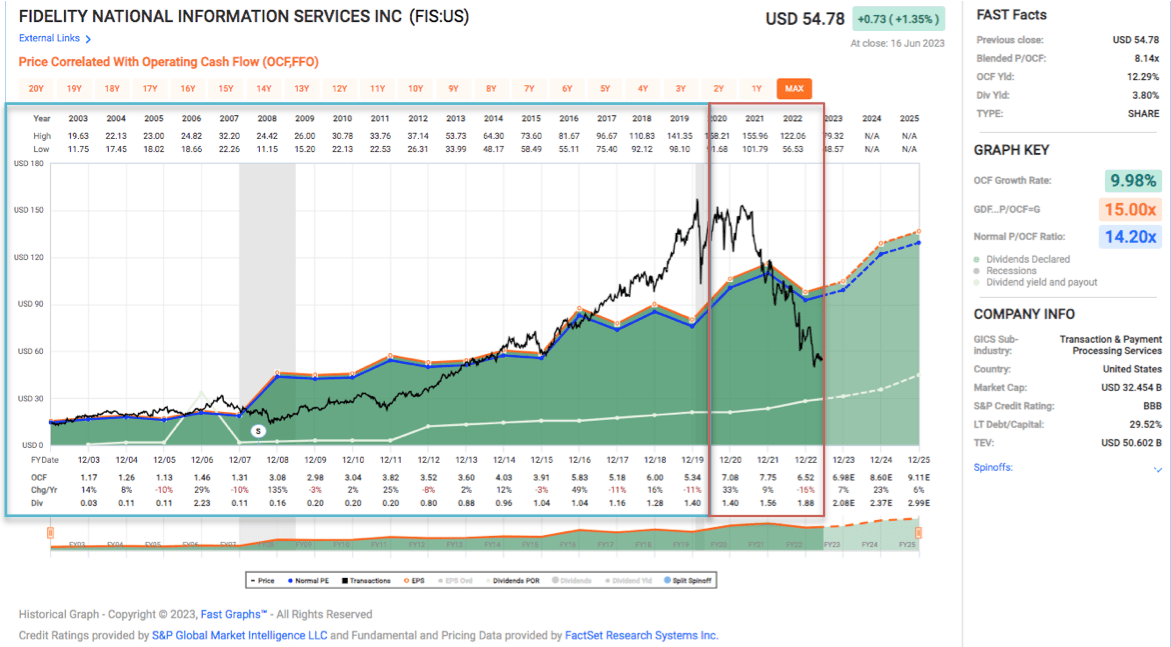

Studying the Fastgraph below, FIS was doing well up till the pandemic, so at first glance, the decline it suffered was due to the pandemic. However, that does not explain the decline from April 2021 to June 2023.

{kind=link}

The bear market of 2022 also could not explain that continued decline in the same time period since its peer FI declined by only 1.81% while SPY gained 13.47%.

When I reexamined the Fastgraph again, this struck me: FIS was doing pretty well before 2020. Even ignoring the exuberant optimism that came as a result of the $43 billion acquisition of Worldpay in 2019, FIS was a great compounder to own from 2003 to 2018.

{kind=link}

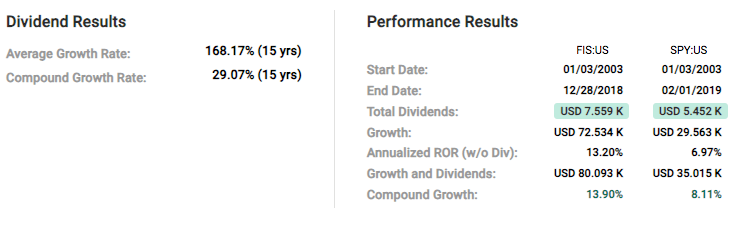

The venerable FIS was a stable growth stock with a total compound growth rate of 13.9% annually, beating SPY's 8.11% easily. For comparison, that kind of return is on par with Costco (13.69%) and better than Microsoft (9.41%) in that time frame.

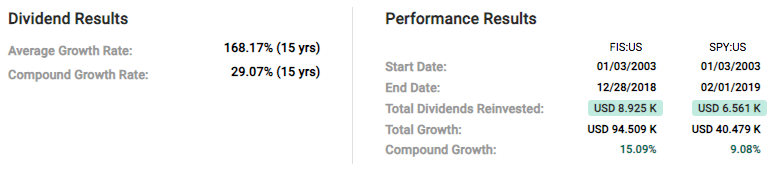

FIS would also be an attractive candidate for dividend growth investors because dividends grew at an average rate of 168.17% over 15 years, or at a compound growth rate of 29.07% annually.

And if the dividends were reinvested, the total returns would be boosted from $80093 to $94509.

{kind=link}

This is the potential that Seth Klarman probably saw in FIS that once it is rid of its baggage it could return to being a compounder again .

In my opinion, the problem for the sustained decline in stock price for the past two years was due to the fateful acquisition of Worldpay to enhance the Merchant Solutions segment.

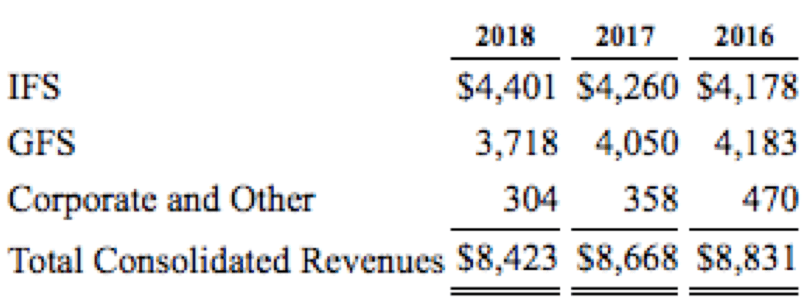

Prior to the acquisition of Worldpay, FIS reported its revenue into Integrated Financial Solutions ((IFS)), Global Financial Solutions ((GFS)), and Corporate and Others.

{kind=link}

According to the 2018 10K,

The IFS segment is focused primarily on serving North American clients for transaction and account processing, payment solutions, channel solutions, digital channels, fraud, risk management and compliance solutions, lending and wealth and retirement solutions, and corporate liquidity, capitalizing on the continuing trend to outsource these solutions. Clients in this segment include regional and community banks, credit unions and commercial lenders, as well as government institutions , merchants and other commercial organizations.

The GFS segment is focused on serving the largest global financial institutions and/or international financial institutions with a broad array of capital markets (including asset managers, buy- and sell-side securities and trading firms), asset management and insurance solutions, as well as banking and payments solutions.

You will observe that among the two largest segments, the one that was growing is the IFS segment. The driving reason for the growth in IFS was the expanding digital business from banks by providing their clients with mobile banking solutions among other offerings. What was distinctly missing from the revenue streams was e-commerce from the merchant's side of the business . There was no mention of "e-commerce" in all the earnings call transcripts in 2017 and 2018. That was the missing piece that FIS wanted to plug in with Worldpay, to ride the e-commerce wave, and with the acquisition of Worldpay, FIS got what it wanted. Currently, FIS reported its business in 4 segments: Banking Solutions, Merchant Solutions, Capital Market Solutions, and Corporate and Other.

2022 10K

The newly created Merchant segment mattered to FIS.

Characteristics of the Merchant segment ( on page 17 of 2022 10K ):

The Merchant segment is focused on serving merchants of all sizes globally, enabling them to accept electronic payments, including card-based payments, contactless card and mobile wallet, originated at a physical point of sale, as well as card-not-present payments in eCommerce and mobile environments. Merchant services include all aspects of payment processing, including authorization and settlement, customer service, chargeback and retrieval processing, electronic payment transaction reporting and network fee and interchange management. Merchant also includes value-added services, such as security and fraud prevention solutions, advanced data analytics and information management solutions, foreign currency management and numerous funding options. Merchant serves clients in over 140 countries. Our Merchant clients are highly diversified, including global enterprises, national retailers and small- to medium-sized businesses.

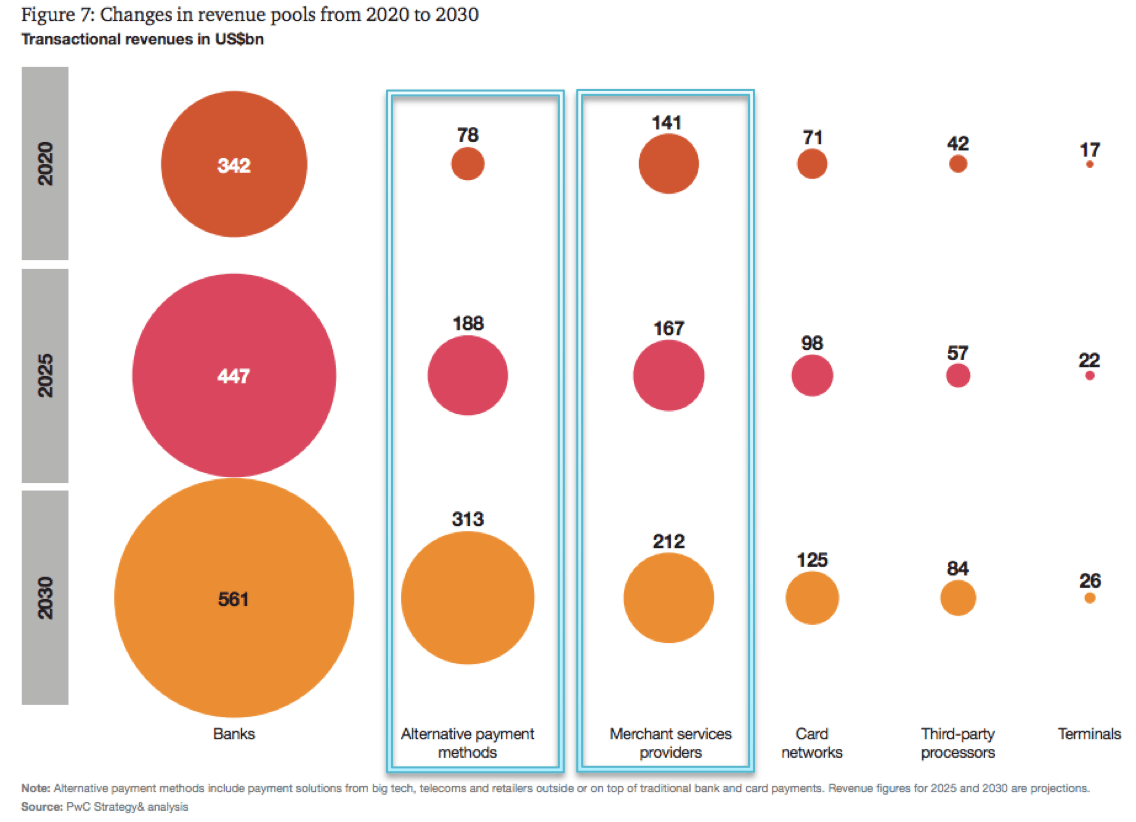

According to PwC Strategy and Analysis research in 2020, the Merchant Segment was the second largest revenue pool in 2020 after banks, and that was almost certainly the driving force behind FIS's acquisition of Worldpay in the first place.

PwC Strategy and Analysis 2020

{kind=link}

With the acquisition of Worldpay in 2019, revenue for Merchant Solutions increased immediately by 94%.

Data gathered from 2022 and 2021 10Ks

{kind=link}

Even during the pre-covid era, the rise of e-commerce both locally as well as globally was already foretelling of the times to come, and with more retailers both small and big going online to sell their goods, be it 100% online or as an omnichannel setup, the revenue that comes from providing payment solutions to these merchants would be on a global scale.

In the same report , the authors estimated that global e-commerce sales will expand from $3.535 trillion in 2019 to $5.695 in 2022 and to $6.542 trillion in 2023.

InsiderIntelligence

And based on the latest figures from Statista , global retail e-commerce sales in 2022 have already exceeded $5.7 trillion and are on track to keep growing.

Former CEO Gary Norcross had these in mind as part of the rationale for the massive acquisition. In the Q1 2019 earnings call , he explained the Worldpay acquisition like this,

As a reminder, the new revenue opportunities for the combined organization include expanded global offerings for merchants with innovative e-commerce solutions ; deeper and broader solutions for financial institutions, such as fraud tools, payment processing and a global merchant referral network; and enhanced and innovative payment solutions creating a faster payments community for high-volume retail and high-value commercial payments.

When FIS attempted to capture this huge market in the merchant segment, it made sense from the point of view of multi-year tailwinds from the growth of e-commerce and the transition to digital payment and digital currencies. Many countries have been moving in that direction, China most notably with its extensive use of super-apps like WeChat and AliPay.

{kind=link}

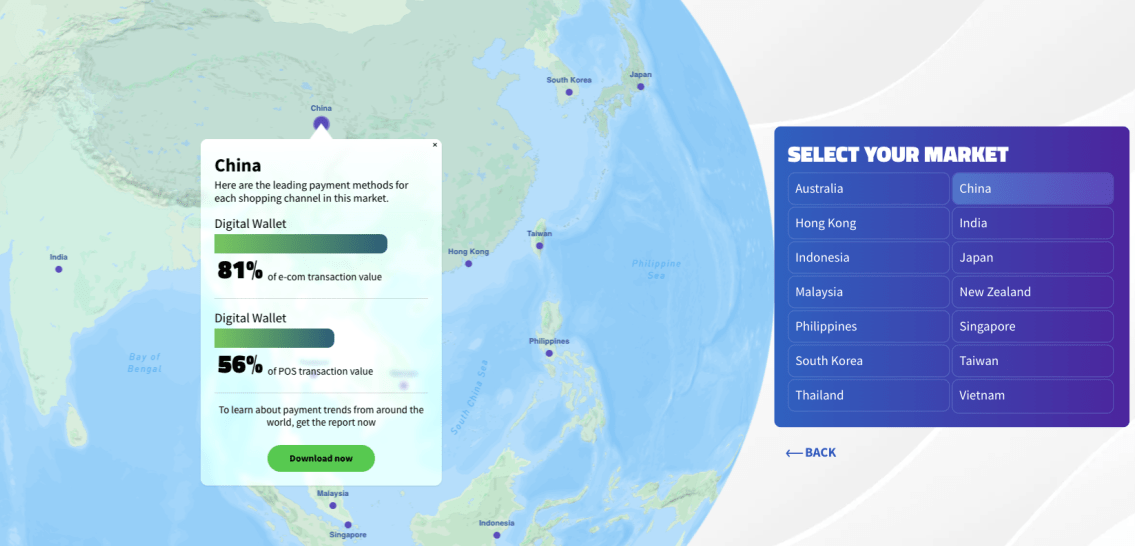

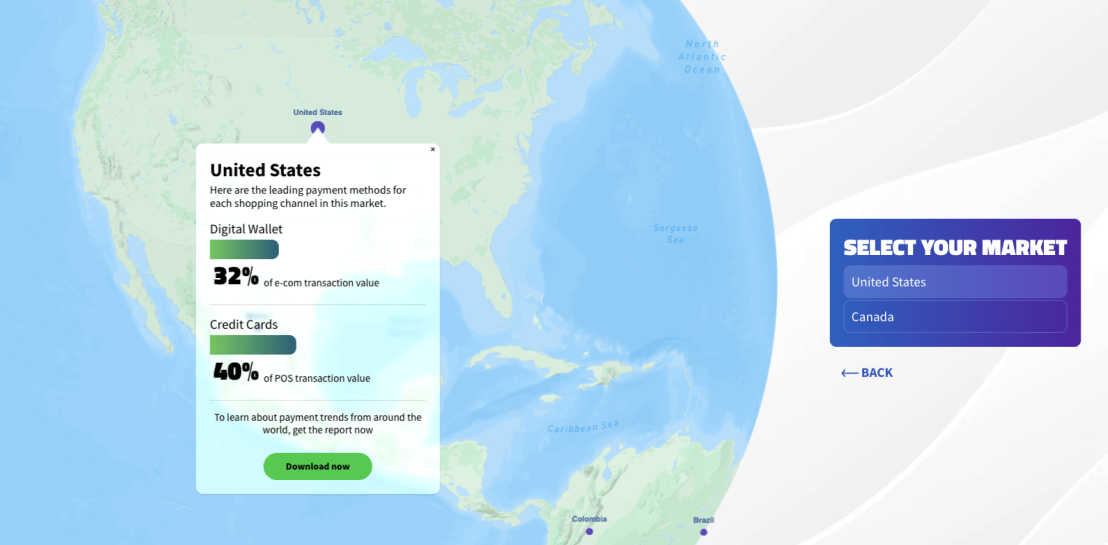

Based on FIS's own global payment report, the leading payment method in China is the use of digital wallets for online or in-person transactions. Compare that high level of penetration with the United States, with less than a third using digital wallets for online transactions and 40% of the in-person transactions still dependent on credit cards.

{kind=link}

In short, there were plenty of opportunities to grow revenue in the Merchants solution segments.

What went wrong?

However, FIS could have bitten off more than it could chew with this acquisition because the global scale of this merchant solution segment which ranges in size from small retailers to large enterprises spread across more than 140 countries requires an enormous sales team in order to meet and service clients.

{kind=link}

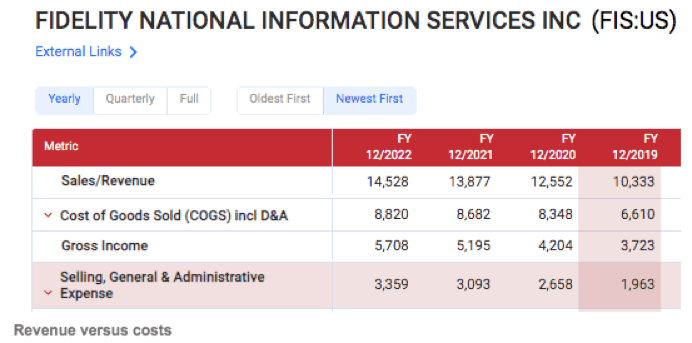

The 40.6% revenue boost post-Worldpay from FY 2019 to FY 2022 came at the cost of incurring far higher Selling, General, and Administrative expenses which increased by 71.1%.

Furthermore, according to the research from the earlier report , the fastest-growing segment is not the Merchant services providers segment but the Alternative Payment Methods segment, which is anticipated to leapfrog the Merchant Segment by 2025. This fast-growing Alternative Payment Methods segment presents a direct challenge to the services that FIS aims to provide to these "merchants of all sizes globally" . If all budding entrepreneurs like dog walkers or home bakers need to accept payments from customers is a payment platform, they can just go to companies like Stripe or Ayden to subscribe to their platform to start accepting payments be it online , in-app , in-person , cross-channel , cross-border , and if a point-of-sales ((POS)) device is needed, entrepreneurs can go to Square . Signing up for these services is relatively fuss-free, there is no need to go to FIS. These companies like Stripe and Ayden work with e-commerce retailers like Etsy (check out my article here), eBay (my article on eBay ), Shopify, Amazon, and many others, so an entrepreneur or small-to-medium size business who wants to sell on these platforms can start selling with ease as these e-commerce giants would have integrated various payment solutions within their e-commerce sites.

The global economic slowdown in the past two years as a result of problems such as supply chain disruptions, the war in Ukraine, high inflation, and the exchange rate risk due to the strong dollar, turned more customers away from discretionary spending to big-box retailers to spend on necessities. Even as revenue in the Merchants segment increased, margins became depressed as expenses rose.

{kind=link}

While the company managed to improve the gross margins from around 33% pre-Worldpay to around 38% in the last 3 years, the net margins fell from around 10-14% pre-Worldpay to under 3% in the last 3 years.

Then, FIS started to report impairment charges; $202 million in Q3 of 2021, then $58 million in Q1 of 2022, $29 million in Q2 of 2022, and $17 million in Q3 of 2022, before the final straw that broke the camel's back, the $17.6 billion impairment cost in Q4 of 2022.

{kind=link}

The following was taken from page 14 of the 2022 10K ,

A significant portion of our revenue is derived from transaction processing fees. The global transaction processing industries depend heavily upon the overall level of consumer, business and government spending. Any change in economic factors, including a sustained deterioration in general economic conditions or consumer confidence, particularly in the U.S., or inflation and increases in interest rates in key countries in which we operate may adversely affect consumer spending, consumer debt levels and credit and debit card usage, and as a result, adversely affect our financial performance by reducing the number or average purchase amount of transactions that we service. Rising interest rates, inflation, and slowing economic growth in the U.S. and Europe began to negatively affect revenue growth and profitability in 2022, particularly in our Merchant Solutions segment. These effects began to accelerate in the fourth quarter of 2022 and are expected to continue to adversely affect our future financial performance. These expectations contributed to our fourth quarter 2022 goodwill impairment in our Merchant reporting unit, and further deterioration in macroeconomic conditions beyond our current expectations could contribute to further impairment .

As the goodwill is caused by the Worldpay acquisition, it indicates that the buyout is not working out as planned. Impairment is a message to investors that the value of the acquired assets (FIS paid $43 billion for Worldpay) has fallen below the amount that the company initially paid, and FIS has to write down as much as $17.6 billion in the current assets line.

And it was amidst all the pessimism and chaos in the company which included the involvement of two activist shareholders demanding a strategic review of the company's plans that Seth Klarman started taking a position in FIS in Q3 2022.

Yes, Seth Bought More Because He Saw Positive Changes Coming

On 18 October 2018, FIS's board of directors appointed the 28-year fintech veteran Stephanie Ferris and former CFO of Worldpay as the new CEO of FIS.

Stockcircle

And in Q4 of 2022, when it became clear to Seth Klarman that the reasons for FIS's underperformance - the Worldpay part of the business and the people who orchestrated that acquisition - were going to be removed, he stepped up his purchases and added another 2 million shares.

In the Q4 2022 earnings call, Stephanie Ferris shared her vision for FIS for her first earnings call as FIS's new CEO,

FIS is returning to its roots. This focus will allow the company to maintain its competitive advantage in delivering innovative next-generation technology solutions to the most complex financial institutions. Additionally, FIS will be in a better position to balance return of capital to shareholders with organic investment and complementary M&A. We remain committed to our investment grade ratings, conservative capital structure and growing dividends. Putting it altogether, we are returning FIS to its historical quality compounder model which is more closely aligned with the way that FIS operated before the Worldpay acquisition. As a quality compounder, FIS will emphasize steady recurring revenue growth, consistent margin expansion and disciplined capital return to shareholders.

Having a new CEO in place whose first order of business was to reduce headcount in order to rightsize the company (i.e. to reduce the high SG&A costs and improve operating margins), there seems to be a brighter future for the company.

Analysts agree. In their most recently revised sales forecasts, they reverted the decline in sales in FY 2023 from 3 months ago and increased that slightly. The same optimism was projected out to FY 2024 and 2025 as well.

{kind=link}

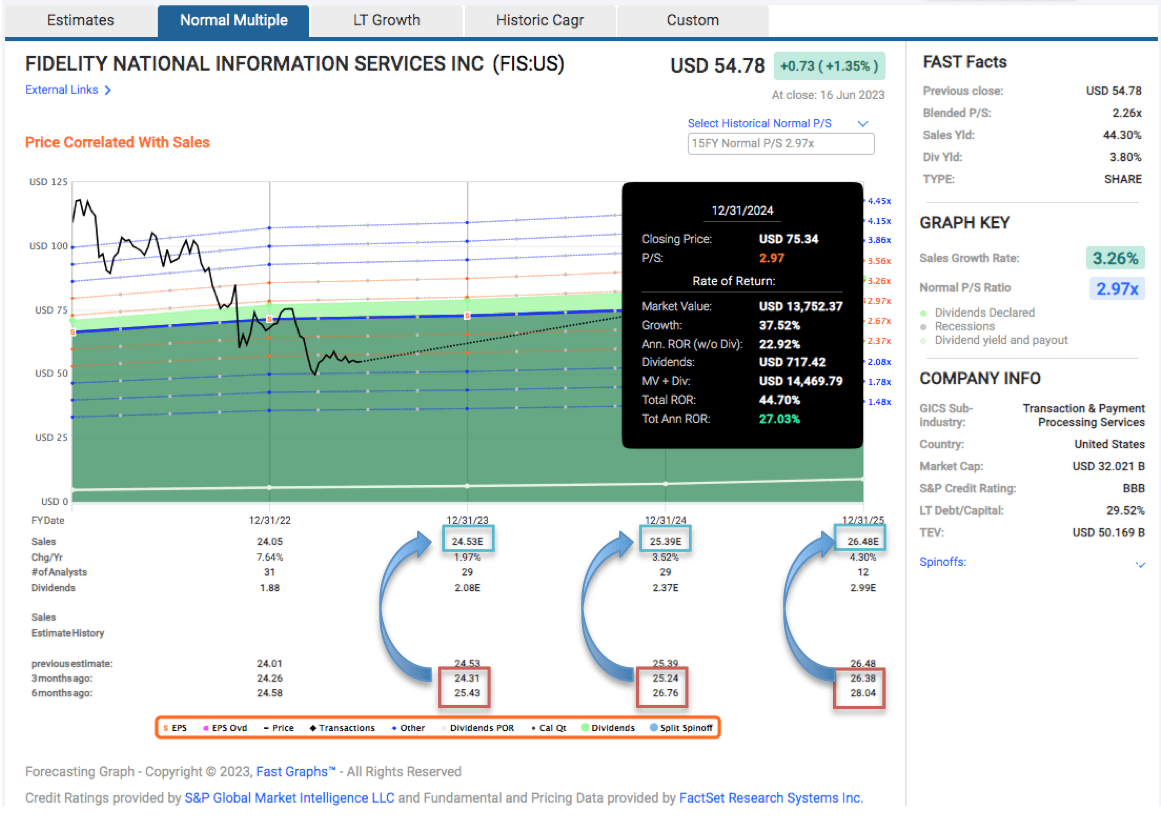

I believe that FIS is undervalued today, even after the 10% gain from 24 March 2023 to 16 June 2023. FIS is trading at a blended P/S of 2.26 now, which is way below its past 5-year P/S of 3.7, and close to its normal P/S of 2.14 between 2006 and 2016 when it was trading at far more reasonable valuations. Buying FIS now definitely offers much more value and a wider margin of safety.

Assuming FIS stock can trade up from the current P/S of 2.26 to a P/S of 2.97 this will represent a 37.53% price appreciation in just 18 months, and after factoring in dividends the total return could potentially be 44.7%.

FIS Is On Solid Footing To Recover From Mishaps

In Q1 2023, Seth Klarman bought 3 million shares of FIS, more than the previous two buys combined.

Why?

On 10 January 2023, the rating agency Fitch affirms FIS's BBB rating and indicates that the outlook is stable, maintaining that "FIS remains well positioned from a balance sheet and cash flow perspective".

Fitch acknowledges the near-term headwinds FIS faces from slowing macro conditions but applauds the actions the new CEO pledges to take, such as reducing costs in the coming year. Despite the challenges on growth and margins in 2023, Fitch believes that FIS "is fairly well positioned from a balance sheet perspective" and that "the company will continue to generate robust FCFs in 2023-2024 despite potentially weaker fundamentals".

All these mean that FIS is well positioned to recover from its past mishaps and return to "focus on identifying and optimizing incremental revenue generation, margin improvement, and cost reduction opportunities".

Without Worldpay, FIS will return to focus on generating revenue from the Banking Solutions and Capital Market Solutions segments.

According to the 2022 10K,

The Banking segment is focused on serving financial institutions of all sizes with core processing software, transaction processing software and complementary applications and services, many of which interact directly with core processing software... Clients in this segment include global financial institutions, U.S. regional and community banks, credit unions and commercial lenders, as well as government institutions and other commercial organizations... We provide our clients integrated solutions characterized by multi-year processing contracts that generate recurring revenue .

The Capital Markets segment is focused on serving global financial services institutions... Our solutions include a variety of mission-critical applications for recordkeeping, treasury, data and analytics, order management and trading, securities processing and financing, and risk and compliance. Capital Markets clients purchase our solutions in various ways including via a recurring subscription model or software as a service ((SAAS)) where the technology is cloud-hosted and managed by FIS, licensing and managing technology "in-house," and through business process as a service (BPaaS) relationships, where Capital Markets manages both the software and select managed services for the client. Our long-established relationships with many of these financial and commercial institutions generate significant recurring revenue .

By retaining these two segments and removing the Merchants segment with the more macro-sensitive and less predictable revenue contribution, FIS will be able to return to its roots, focus on growing the predictable recurring revenue streams from the multi-year contracts in the Banking and Capital Markets segments and begin the long journey to regain investors' confidence in the company.

Fitch agrees that FIS's technology solutions are mission-critical for its customers. Its products enjoy a large market share across more than 100 countries, and its clients sign long-term contracts (some as long as 5 years), and more than 90% of them renew their contracts with FIS.

Conclusion

I believe that there are four reasons why Seth Klarman started a position at Fidelity National Information Services ((FIS)) of substantial size. He did so because FIS is trading at a multi-year low valuation, at a price that reduces downside risks while maximizing upside potential. He started buying when most people including "smart money" folks were selling FIS, when nobody liked it, at prices so low that even if he gets it wrong he has protected his downside with a wide margin of safety. Of course, he made sure he understood the business and what makes it tick, so once positive signs appeared, such as a change in management with a renewed focus on improving shareholder value, the decision to axe the problematic Merchants segment and get out of that highly competitive business (with all the high expenses and lower margins) and back to its core, and the affirmation of its credit rating by Fitch, Seth Klarman increased his position in FIS.

As of now, his position in FIS is sitting on an estimated 23% loss. However, I do believe that FIS is a deep value play that fits Seth Klarman's investment philosophy. He described his pursuit of value investing beautifully in chapter 6 of his book,

The disciplined pursuit of bargains makes value investing very much a risk-averse approach. The greatest challenge for value investors is maintaining the required discipline. Being a value investor usually means standing apart from the crowd, challenging conventional wisdom, and opposing the prevailing investment winds. It can be a very lonely undertaking. A value investor may experience poor, even horrendous, performance compared with that of other investors or the market as a whole during prolonged periods of market overvaluation. Yet over the long run the value approach works so successfully that few, if any, advocates of the philosophy ever abandon it.

Readers, just because Seth Klarman invests in FIS does not mean we should. The turnaround at FIS is likely to take several quarters to right itself as the company begins to divest Worldpay while focusing on returning to the compounder that it once was.

There could also be execution risk and the new management team is untested in their roles. Both the CEO and CFO are relatively new to FIS itself, each spending less than five years there, and neither has prior experience in their roles (the CFO had just one year of experience as a CFO in 2022 before taking over). Of course, I understand that installing a brand new team rather than promoting from within the FIS lifers is the whole idea behind the move to oust the current management - to instill confidence that things will change at FIS but their lack of deep knowledge of the FIS culture could potentially lead to unforeseen delays or hiccups.

Lastly, my whole premise for investing in FIS is based on Seth Klarman's continued holding of FIS shares. The 13F filings do not show his recent transactions. Perhaps he bought even more in Q2 of 2023. He could also decide to sell them at a loss. And if he had decided to sell his FIS holdings in Q2 2023, my thesis collapses as it would likely mean that he no longer sees value and a margin of safety in FIS, and he has little confidence that FIS will recover.

In any case, owning FIS shares is not for the faint-hearted and as Seth Klarman said, the road of a value investor is a lonely one. FIS is definitely not a buy for people who wants to see returns by the end of 2023. For anyone considering holding on to or starting a position in FIS, you should first understand your reasons for doing so and understanding Seth Klarman's reasons is just a starting point. I will consider FIS to be a buy for deep-value value investors; all they need to do now is to grab a few more FIS shares and wait for the story to play out, utilizing what Seth Klarman calls the "buy a bargain and wait" strategy. And while waiting for the turnaround, investors get to collect dividends from this dividend-compounding machine.

Buying and holding is simple enough but waiting and doing nothing is probably the hardest thing to do. If you cannot do that, if you cannot stomach a few quarters of poor results, avoid FIS.

For further details see:

Fidelity National Information Services: Why Does Seth Klarman Own 4.3% Of FIS?