FIS - Fidelity National Information: Shedding Value Pre-Spinoff But Future Valuation Not Yet Clear

2023-05-18 11:13:20 ET

Summary

- FIS announced earlier this year that it intends to spin off its Merchant Solutions business.

- This move will immediately remove about 1/3 of the firm's revenue and adjusted EBITDA.

- The stock has been trading down for some time and has lost more than 33% of its value in this year alone, creating a potential buying opportunity for long-term bulls.

- Yet, completing the spin-off could yield a return to higher historical multiples or little price action; it is not yet clear which way things will proceed.

- As such, I would rate this stock a hold while the air clears further.

Overview

Fidelity National Information Services ( FIS ) is in many ways the godfather of today's financial technology industry. In operation since 1968, the company has gone through many transformations and acquisitions to become the diversified industry goliath that it is today. In the last decade alone, FIS acquired capital markets technology provider SunGard for $9.1B (2015) and payments provider Worldpay (2019) for a whopping $35B.

With a present market cap in excess of $32B, FIS continues to be one of the largest purely financial technology companies in the market today. It is a component of the S&P500 and a long-running stalwart in the space, with 92.37% of its shares held by institutions as of this article.

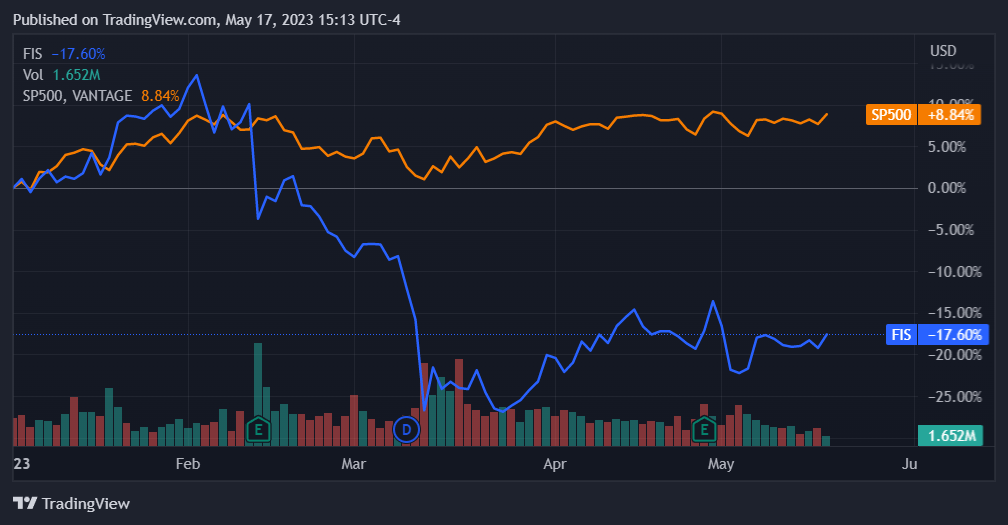

Scale doesn't guarantee price performance, however, and FIS has depreciated well in excess of the S&P 500 this year. This occurred against the backdrop of the firm outperforming consensus across its last two earnings reports and came down to conservative guidance on 'macroeconomic deterioration' throughout the year ahead.

The other critical factor to note here is the firm's intent to spin off its Merchant Solutions (payments) business in its entirety.

{kind=link}

In advance of this move, FIS already wrote down the value of its merchant solutions (payments) segment in its most recent quarter. Management was explicit about the factors driving underperformance in this segment, noting that its SMB customers transitioning to embedded payments of the type offered by Stripe and Square (SQ).

{kind=link}

This had the effect of absolutely crushing FIS' net income for the period.

{kind=link}

These headwinds for its payments business remain significant and are a complicating factor as the company reverses its previous merger with WorldPay and spins the entity out on its own. This article will review the fundamental impact that spinning off this business would have and estimate a market valuation for the slimmed-down FIS that will result.

FIS Payments

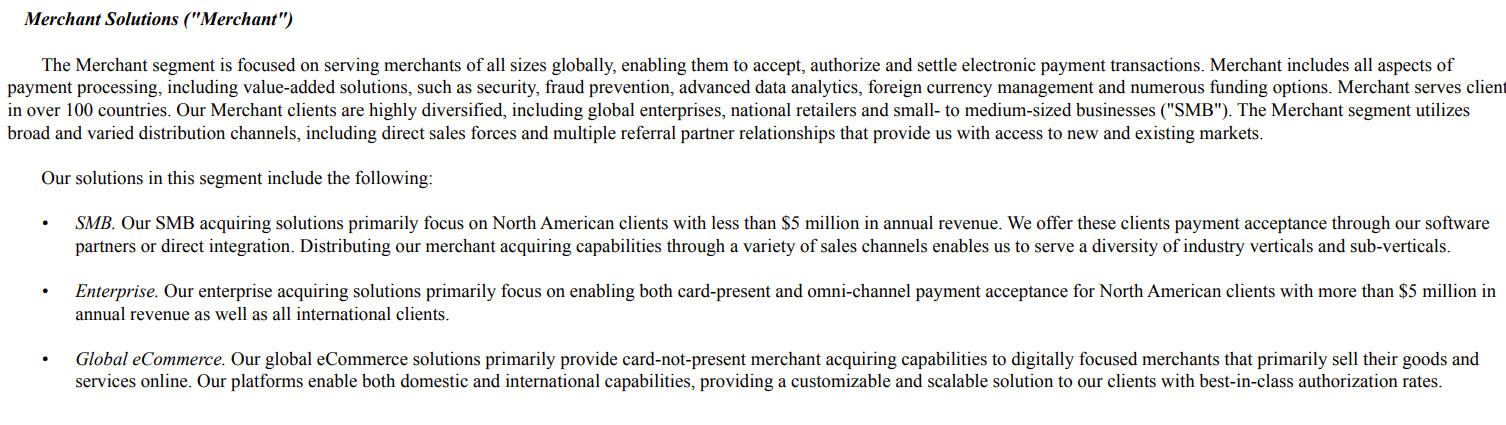

Given the size and complexity of FIS, it is first worth understanding the exact definition of FIS' Merchant Solutions business. FIS provides multiple payments products across its operating segments, including for its financial services customers. Payments for financial services firms are placed under the Banking Solutions segment. These offerings are wholly distinct from the Merchant Solutions business.

{kind=link}

{kind=link}

The Merchant Solutions segment, on the other hand, is not for financial entities. It is a payments and auxiliary services offering for any other type of business.

{kind=link}

We can now look at the relative contribution of the Merchant Solutions segment for FIS. Merchant Solutions has maintained positive growth y/y for the last 3 years but also appears to have experienced a material slowdown as of last year, with y/y growth dropping from 19.35% to 6.16%.

{kind=link}

| 2020 |

| 2021 |

| 2022 |

| Merchant Solutions Growth y/y |

| 19.35% |

| 6.16% |

| % of Consolidated Revenue |

| 30.01% |

| 32.40% |

| 32.85% |

Source: Excel, FIS

As of 2022, the Merchant Solutions business represented 32.85% of FIS' consolidated revenue. Doubly concerning here is the fact that growth has collapsed in this business, even as it became a somewhat larger piece of the company's overall revenue over the last 3 years.

The most recent quarter saw accelerating weakness for this business segment, with Merchant Float decreasing 6.23% y/y. A decrease in Merchant Float is a particularly damning signal, as it is the best metric to act as a proxy for overall payment network utilization. This is because the metric is a snapshot of money 'in the pipes', i.e., currently flowing through the payment network while concurrently representing a line item for the payer and payee.

{kind=link}

Given how metrics have been progressing for the Merchant Solutions business, it is sensible that management is taking steps to disaggregate the segment. The next section will present FIS financials with this segment removed.

Post Spin-Off Financials

While FIS does not report overly detailed segment-level financial metrics, we do have adjusted EBITDA and revenue for each segment. With these numbers, we can establish a reasonable estimate of the present and forward valuation for the firm.

|

|

| 2021 |

| 2022 |

| FIS Gross Revenue |

| $13,877 |

| $14,528 |

| FIS Gross Adj. EBITDA |

| $6,768 |

| $6,773 |

| Merchant Solutions Segment Revenue |

| $4,496 |

| $4,773 |

| Merchant Solutions Segment Adj. EBITDA |

| $2,262 |

| $2,258 |

| FIS Revenue ex Merchant Segment |

| $9,381 |

| $9,755 |

| FIS Adj. EBITDA ex Merchant Segment |

| $4,506 |

| $4,515 |

Source: Excel, FIS

Taking out the revenue contribution of the Merchant Solutions segment, we arrive at $9.4B and $9.8B revenue for FIS in 2021 and 2022, respectively.

Taking out the adjusted EBITDA contribution of the Merchant Solutions segment, we arrive at $4.51B and $4.52B adjusted EBITDA for FIS in 2021 and 2022, respectively.

This spin-off will eliminate roughly 33% of the fundamental value of the enterprise.

| FIS ex Merchant Segment Revenue Gross % |

| 67.60% |

| 67.15% |

| FIS ex Merchant Segment Adj EBITDA Gross % |

| 66.58% |

| 66.66% |

Source: Excel, FIS

The way that this will be reflected in FIS forward-looking valuation is less clear. Given that this is a mature stock and a company with an extensive track record of operations, I think the market will end up pricing it on a P/E basis. This means that a 1/3 decrease in FIS earnings should theoretically yield 2/3 of its valuation at identical multiples.

The market, however, has discounted FIS significantly more than that already. The company hasn't come close to matching the price return on the S&P500 Index since late 2021 and has dropped off precipitously since.

{kind=link}

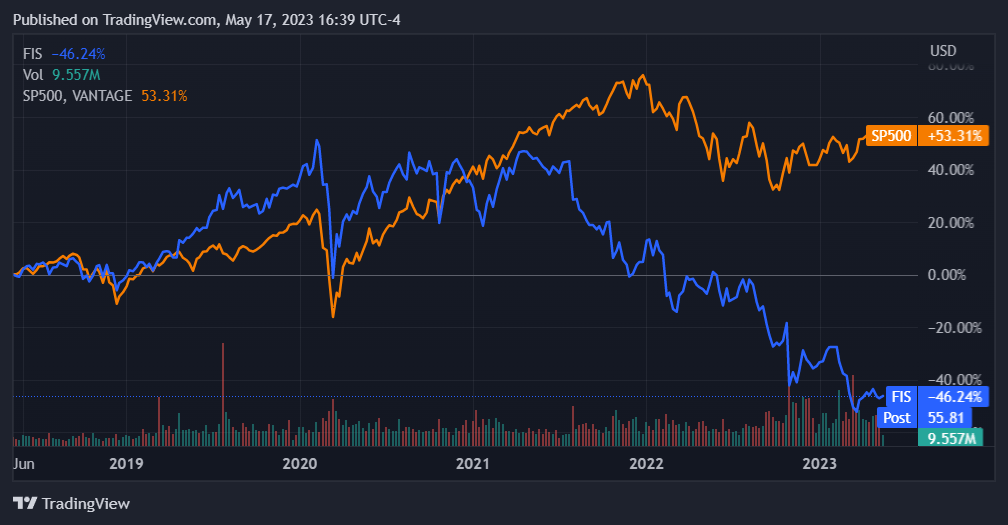

It is also trading nowhere near its historical peak.

{kind=link}

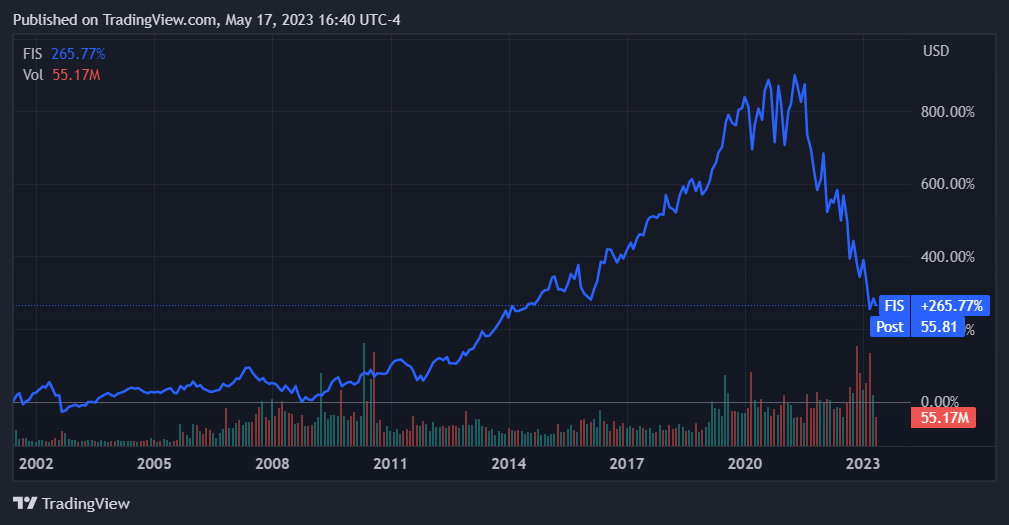

These technical trendlines are fairly stark and lead me to believe that the market has already priced in the spin-off.

Conclusion

The question around this stock is this: after the spin-off, will FIS continue to trade at the same multiples that it has had recently, or will it approach the much-higher historical multiples?

The former case yields a simple 33% discount to its current valuation. At the same multiple, earnings of 2/3 the amount yields a share price 2/3 of the amount.

This would imply that a valuation premium of 50% or more to historical norms is expensive (1/3 is 50% of 2/3, so FIS adjusted EBITDA pre-spinoff is 150% of its adjusted EBITDA post-spinoff). The stock has lost more value than that YTD and far more than that over the last few years.

As such, it is possible to conclude that it is trading cheaply for long-term bulls, although I think there is still too much uncertainty here to come to a firm buy or sell decision. To that end, I will rate FIS a hold while the air clears around the spin-off and the firm's subsequent prospects.

For further details see:

Fidelity National Information: Shedding Value Pre-Spinoff, But Future Valuation Not Yet Clear