FIS - Fidelity Shares Finally Look Attractive (Ratings Upgrade)

2023-11-11 22:32:02 ET

Summary

- Fidelity National Information Services has faced challenges including margin pressure, higher rates, management change, and divestitures, causing its shares to fall.

- FIS reported 4% organic growth in the quarter, driven by recurring revenue growth in its banking and capital markets units.

- The company plans to sell a majority stake in its Worldpay merchant solutions business, using the proceeds to pay down debt and buy back stock, potentially creating upside for investors.

Shares of Fidelity National Information Services ( FIS ) have had a difficult year, falling 18%, as the company has battled margin pressure, higher rates, management change, and divestitures. Last year, I recommended investors sell FIS stock, and since then, shares have fallen nearly 30% while the S&P 500 has risen by 22%. Ultimately, even challenged businesses can be attractive investments at the right price. Given the magnitude of the underperformance, now is an opportune time to revisit FIS given its recently reported results.

{kind=link}

In the company’s third quarter , Fidelity earned $0.94 in adjusted EPS as revenue from continuing operations rose by 3.3% to $2.5 billion. There is a lot to dissect given its planned sale of Worldpay. I think it is best to look first at the remaining business, and then view the impact of this sale separately.

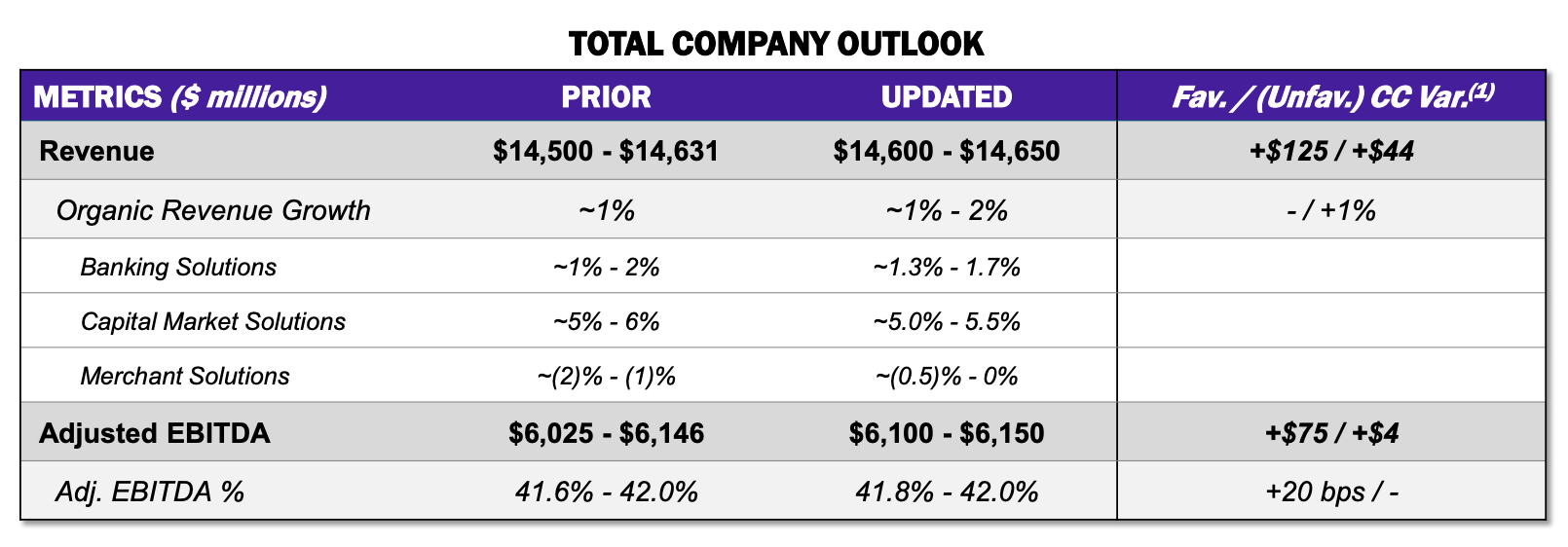

In the quarter, the company reported 4% organic growth, driven by 7% recurring revenue growth. After the sale of Worldpay, FIS will have just two units, where it provides fintech and payment processing solutions for banking and for capital markets with about 75% of revenues coming from banking and the remainder capital markets. Capital markets was up 6% while banking was up 3%. That said, banking received a 4% benefit from servicing pandemic relief programs. That provided a tailwind, which should fade over the next year, and absent this, growth was flat, a continuation of sluggish activity from last year. The remaining FIS has a $22.7 billion backlog, or about 2.5 years of business. This should enable steady revenue results with modest growth potential.

On the bright side, in the face of slower growth, management has focused on rationalizing costs, and we are seeing some benefits from these efforts. EBITDA margins were up 70bps to 43%. Despite this, EPS was down 7%. This is primarily because of floating rate debt having interest rates rise. Interest expense has more than doubled from $78 million to $162 million, a ~$0.10 headwind to EPS, accounting for more than all of the decline.

In other words, FIS ex-interest expense generated a small increase in EPS, but this was wiped away by higher borrowing costs on its $18.7 billion in debt. This was a reason I was negative on the stock last year when the Fed was beginning to raise rates. Now though, its rate hikes are likely largely, if not totally, complete. As such, we should not see further meaningful interest expense degradation beyond this level; that said, we are unlikely to see interest expense (pro forma for pending debt reduction, which will be discussed below) fall back to last year’s levels, given rates are unlikely to return to zero. In other words, the headwind from higher rates is largely complete, but interest rates will not be a tailwind soon.

Alongside results, management slightly lifted guidance. However, this benefit really came from merchant solutions, which is the unit being spun out. Banking and capital solutions revenue growth expectations were tightened. On the positive side, thanks to strong EBITDA margins this quarter, for the full year, margins will come in toward the top end of guidance.

{kind=link}

Turning to its divestiture, the company remains on track to sell a majority stake in its Worldpay merchant solutions business in Q1 2024. This forced a $ 6.8 billion write-down to goodwill as FIS is selling this business for less than it paid for it. Hoped-for synergies never materialized, and as noted earlier, this transaction left Fidelity burdened with $18.7 billion in debt.

FIS will receive $12 billion from the sale of its 55% stake. It will continue to hold a 45% stake, which will be worth about $5.9 billion based on the purchase price and the 2.5x debt to EBITDA leverage being added to Worldpay’s capital structure to finance the transaction.

The first thing FIS will do with its proceeds is pay down gross debt by about $8.7 billion to $10 billion. This will deleverage FIS from 3.0x debt to EBITDA today to 2.5x, restoring its balance sheet strength onto firmer footing. The company also aims buy back $3.5 billion of stock with the remaining proceeds, or about 11.5% of all shares outstanding. The company is getting a head start on this, resuming buybacks in Q4 with a $500 million plan, aided by $907 million in free cash flow generated in the third quarter.

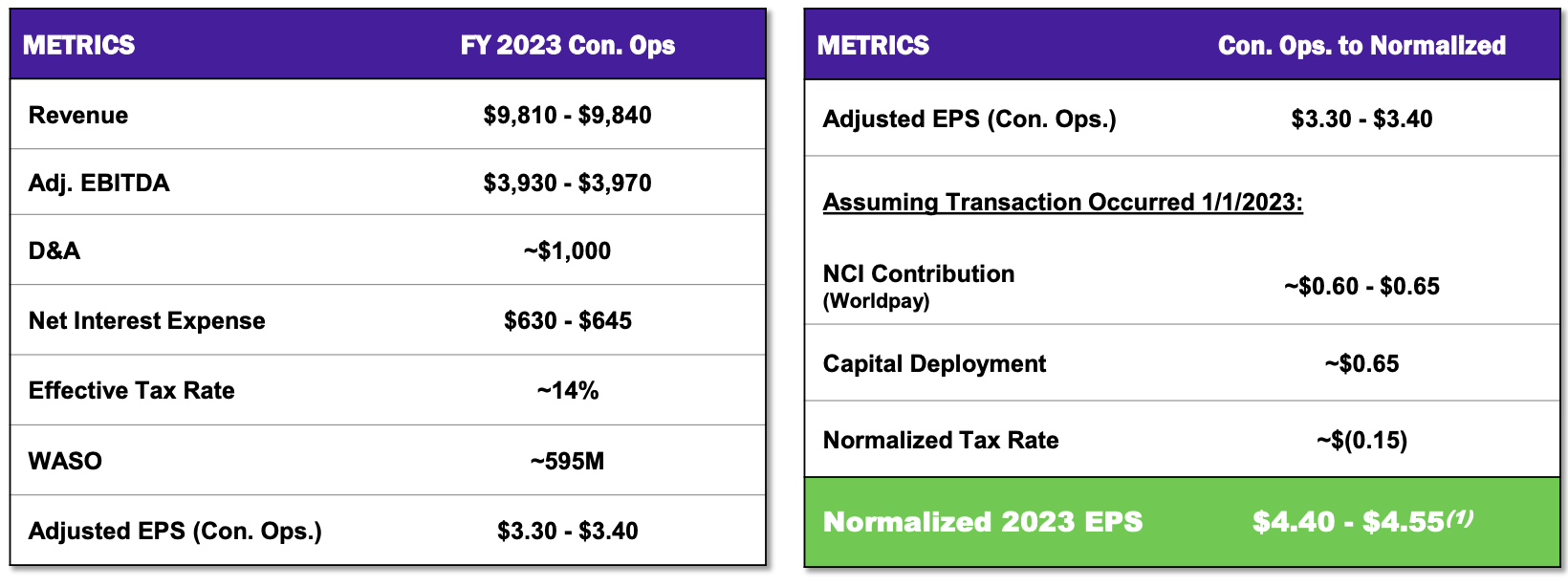

When all of these transactions are complete, there will be a simpler FIS, with a reduced share count, better balance sheet, and a nearly $6 billion stake in the private merchant solutions business. Essentially, it will be undoing the actions of the past few years. The question is what this new FIS should be worth. Continuing operations are on track to earn $3.30-$3.40 in EPS this year. This does understate FIS’s true earnings power though because this EPS is weighed down by interest on $18.7 billion of debt, not $10 billion, and by a higher share count. Management has attempted to bridge these results to what they will look like when FIS is transformed, and they get to $4.40-$4.55.

{kind=link}

Personally, I think the best way to value FIS is to exclude EPS from its minority interest in Worldpay, value the remaining business, and just add the $5.9 billion equity value at the sales price. So, with benefits of lower debt and share count, FIS has about $3.85 in earnings power. Its equity stake in Worldpay will be worth about $10/share. Excluding this, FIS is trading at $42/share or about 11x earnings.

Another way to think about it is that FIS sold a large chunk of its business at 9.8x EBITDA. If we use that same valuation for remaining FIS at $3.95 billion in EBITDA, it is worth about $39 billion. If we add to this the $5.9 billion in Worldpay plus the $3.5 billion in cash received to reduce the share count, FIS should be worth about $47.4 billion. Taking out its $10 billion in remaining debt, its equity is worth $37.4 billion today or about $64 a share, representing 20% upside.

At $64 a share, it would be trading at 14x EPS, after subtracting its stake in Worldpay, not an overly aggressive multiple. At its current price, shares are reflecting the exasperation investors feels after value-destructive M&A. However, as the company executes on this simplification plan, I see upside with the pro-forma business at just 11x earnings. As it reduces debt and buybacks stock, I expect shares to converge toward a 10x EV/EBITDA multiple, or $60-64 a share, creating 20% upside. Shares may not go back to past highs, but they have now been beaten up enough to become a buy, in my view.

For further details see:

Fidelity Shares Finally Look Attractive (Ratings Upgrade)