PSEC - Fidus Investment: A Hold With A 13% Yield (Downgrade)

2023-12-28 12:48:52 ET

Summary

- Fidus Investment Corporation faces concerns over overpaid dividends and potential lower NII in a low-rate environment.

- I'm considering modifying my stock classification to sell if the margin of dividend safety erodes.

- Limited income and dividend growth potential moving forward leads to a hold rating for FDUS.

Fidus Investment Corporation ( FDUS ) has enjoyed rapid growth in the last ten years, but an overpaid dividend and potential for lower NII in a low-rate environment are issues of concern as the year draws to a close.

I still own Fidus Investment in my passive income portfolio, but I have placed the BDC on my watch-list and might modify my stock classification to SELL if the margin of dividend safety erodes.

As of right now, my stock classification for FDUS is Hold as I do see limited income and dividend growth potential moving forward.

My Rating History

Fidus Investment originally attracted my interest as a passive income BDC investment in 2022 due to the company's First Lien focus, which I proposed represented a protective layer against a recession.

Other things I liked included a relatively low pay-out ratio based on NII and a tiny discount to net asset value. With the central bank proposing to slash key interest rates next year and with the margin of dividend safety set to erode, I think that the risk/return relationship has suffered.

Particularly, I think that NII growth will be harder to come by moving forward which opens up the possibility of Fidus Investment selling again at a discount to net asset value.

A Diversified Secured Lending-Focused Portfolio With A Positive Long-Term Growth Trend

Fidus Investment is an investor in Debt and Equity and predominantly focuses on lower middle market companies based in the United States. These companies tend to have the largest challenges to overcome in securing funding from traditional banks because they limited lending to lower middle market companies after the Great Recession.

Fidus Investment primarily provides capital to lower middle market companies in order to facilitate change of control transactions, recapitalizations, and acquisitions.

Lower middle market companies are those with annual revenues between $10 and $150 million and that have limited access to public markets. The middle market sector, thus, offers BDCs like Fidus Investment the opportunity to earn attractive risk-adjusted returns for its investors.

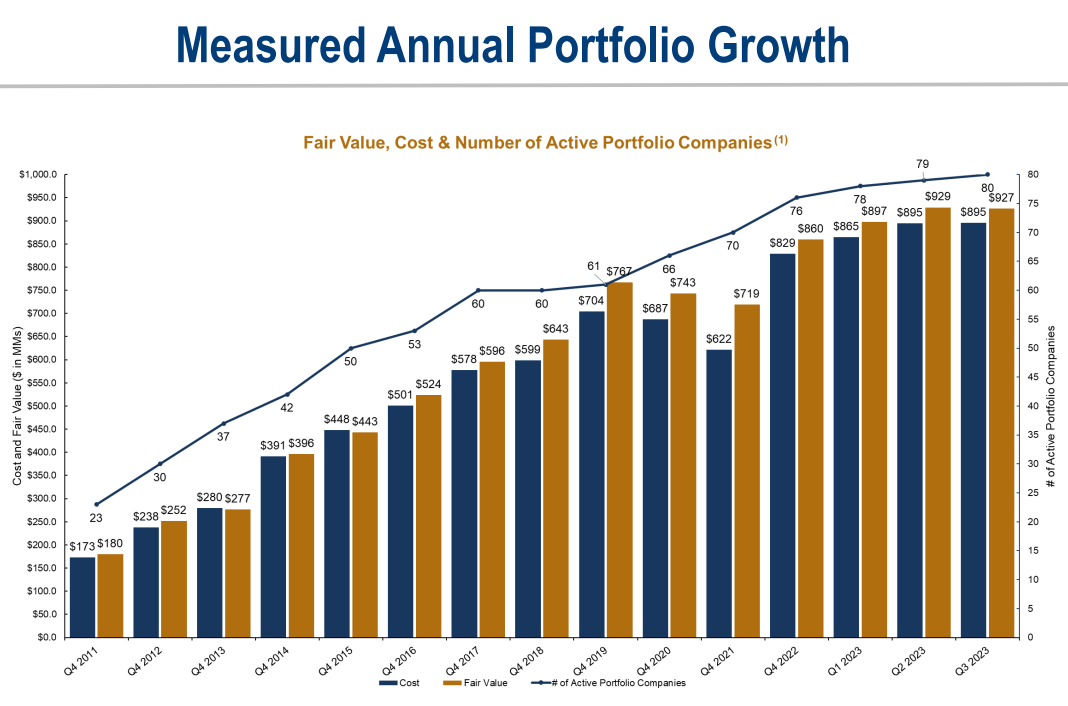

Fidus Investments' portfolio developed in lockstep with these industry trends and the BDC reported its second-highest ever portfolio value in the third quarter.

{kind=link}

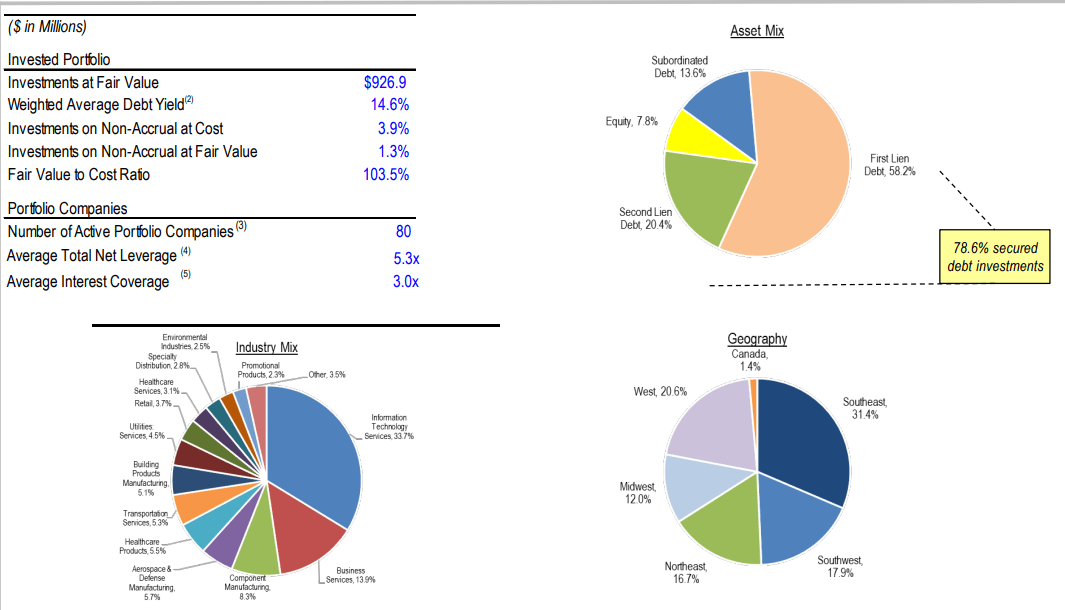

Fidus Investment is not the largest fish in the pond with an equity value of $555 million and a total investment portfolio of $927 million, but the BDC has seen, as was just demonstrated, long-term growth in its portfolio.

As of the end of the third quarter, Fidus Investment was primarily invested in First Liens, which made up 58.2% of the company's total investment portfolio. Second Liens accounted for 20.4% of investments, making FDUS a senior secured BDC whose secured investments amounted to 78.6% of all portfolio investments.

{kind=link}

Narrowing Margin Of Dividend Safety

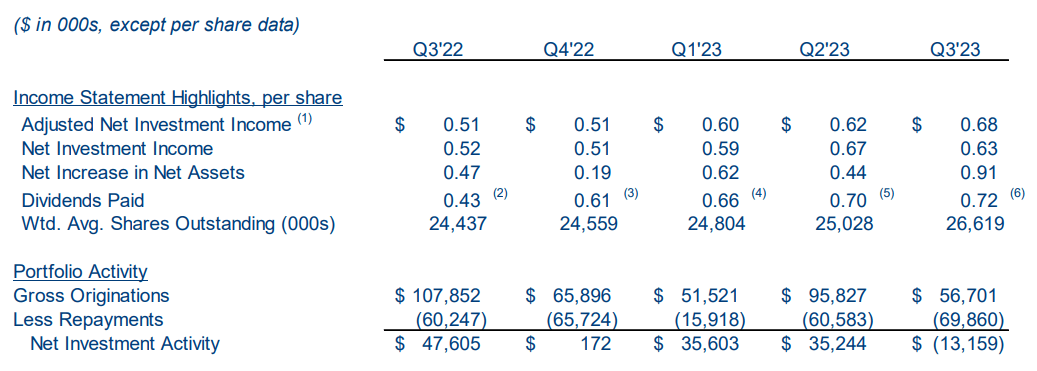

Fidus Investment earned $1.90 per share in adjusted NII in the three quarters of 2023 and paid out $2.08 per share which leads us to a NII pay-out ratio of 109% which is indicative of lower total dividend returns moving forward.

The BDC paid a boatload of special dividends throughout the year which have boosted Fidus Investments' total dividends, and these special dividends have been fueled by the BDC's large increase in adjusted NII compared to last year, thanks to the central bank pushing key interest rates higher. In 3Q-23, Fidus Investments' adjusted NII per share was 33% higher than in the third quarter of 2022.

I do think, however, that with the central bank shifting its rate policy, the potential for special dividends in a low-rate environment is greatly diminished which is also the reason why I expect BDCs to sell at larger discounts to net asset value in 2024 than they are today.

{kind=link}

1% Premium, Limited Upside

The potential shift from premium to discount valuation, which I hinted at lately in my article on Prospect Capital Corp. ( PSEC ) is one reason why I am scaling back my exposure to the BDC sector in general. I am particularly adamant about reducing my exposure to those BDCs that are still trading at premiums to net asset values.

In the case of FDUS, the premium is rather tiny, at 1%, but taking into account the central bank's policy shift, I think the time for cyclical NII expansion is mostly over for the BDC sector. The same argument can be applied, obviously, to other BDCs which I am also in the process of down weighting.

Downside Risks Are Larger Than FDUS' Upside Potential

In my view, Fidus Investment is going to see lower NII in the next 12 months. With that being said, the central bank may take its time with its rate adjustment process, thereby allowing BDCs to still earn decent NII to support their dividends. Thus, the realization of a NAV discount valuation may take longer than expected.

My Conclusion

Fidus Investment's investment portfolio kept growing throughout 2023 and the company reported its second-highest portfolio value ever in the third quarter.

This does not change the fact, however, that the central bank is putting the screws to the BDC and financial sectors and limiting its NII growth potential by announcing that it will slash key interest rates next year.

Thus, the margin of dividend safety is set poised to decline in 2024. I also consider it probable that we will see more BDCs in the future that will sell at discounts to net asset value, as opposed to premiums to net asset value, in a low-rate environment. Hold.

For further details see:

Fidus Investment: A Hold With A 13% Yield (Downgrade)