FDUS - Fidus Investment: Attractive Yield Of 14% Yet A Thin Margin Of Safety

2023-12-25 09:41:02 ET

Summary

- Fidus Investment is a BDC that provides customized debt and equity financing solutions to lower mid-cap businesses.

- The company prefers conservative investments, with niche market leaders, diversified customer and supplier bases, and strong management teams.

- The financial conditions of FDUS portfolio companies are strong with average net leverage of only 5.3x and interest coverage of 3.0x.

- Despite the obvious defensive characteristics of FDUS's portfolio, the current dividend yield stands at ~14%, which is very high for BDC segment.

- Yet, a major part of the dividend is covered by unsustainable equity component, which, coupled with a notable exposure to non-first lien investments, make the overall investment case suboptimal.

Fidus Investment (FDUS) is a BDC, which, as most BDCs, provides customized debt and equity financing solutions mostly to lower mid-cap businesses.

The investment objective is also the same as across the BDC space - i.e., key focus on high yielding current income streams with a secondary objective to preserve and steadily grow the NAV over time.

In terms of the investment policy, the outlined criteria imply that FDUS seems to prefer quite conservative investments, which, in my opinion, is a good thing. Many other BDCs tend to assume relatively huge risk positions through inherently risky companies (e.g., life science early stage companies, biotech etc.) thereby rendering the BDC factor exposure more unpredictable from an already aggressive (risk-on) base.

So, in FDUS's case the target company characteristics are as follows:

- Niche market leaders with defensible market positions

- Diversified customer and supplier bases

- Strong free cash flows or asset support

- Significant enterprise value / equity cushions

- Strong management teams with meaningful equity ownership or incentives

As we can see, we are not talking here about cash burning companies, whose financial prospects are highly unpredictable. Instead, FDUS puts an emphasize on rather defensive names, which should result in a more stable cash generation and lower write downs.

FDUS Investor Presentation

The portfolio breakdown per industry level indicates a relatively high degree of diversification across the board, with an expectation of the IT services component. The remaining sectors could to a large extent be deemed conventional and stable without a meaningful bias towards speculative risks.

{kind=link}

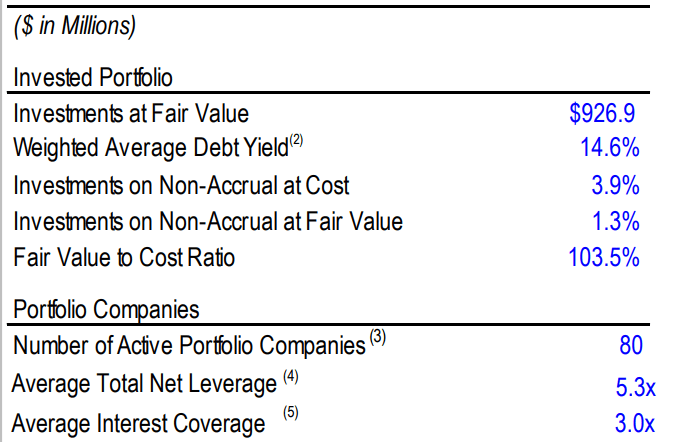

The most crucial and FDUS-specific aspect in the context of the underlying portfolio characteristics is the quality of portfolio companies. As it is reflected in the table above, the average net leverage and interest coverage levels of FDUS companies are very impressive - 5.3x and 3.0x, respectively (as of Q3, 2023).

Typically, a net leverage of ~5x is considered a sweet spot of many businesses to keep the capital structure at optimal levels. Similarly, interest coverage of 3x could also be deemed safe and indicative of a sound financial position.

As a result, the non-accruals at fair value has been rather minimal and stable over time (e.g., only 1.3% as of Q3, 2023).

According to Edward Ross, CEO, FDUS still remains committed to its prudent investment underwriting policy (as per most recent earnings call ):

As we added debt and equity investments to our portfolio, we continue to carefully select high-quality companies that generate excess levels of cash flow to service debt and to structure our investments with a high percentage of equity cushion in an effort to manage downside risk, which is especially important in today's higher rate environment.

Thesis

Now, once we have established that FDUS is a relatively conservative BDC, the question becomes whether the offered yield is sufficient in the context of the assumed risk.

{kind=link}

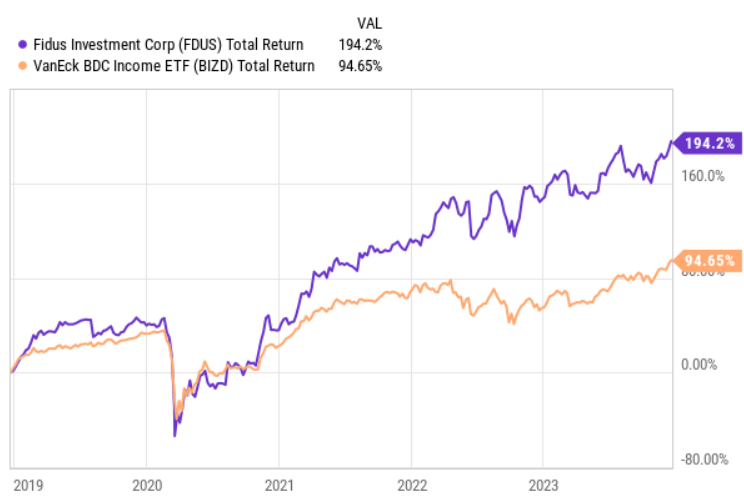

Historically, FDUS has managed to outperform the broader BDC index by a huge margin. There are two obvious sources of alpha:

First, FDUS has carried a huge external leverage load that has boosted the returns under the COVID-19 recovery period.

{kind=link}

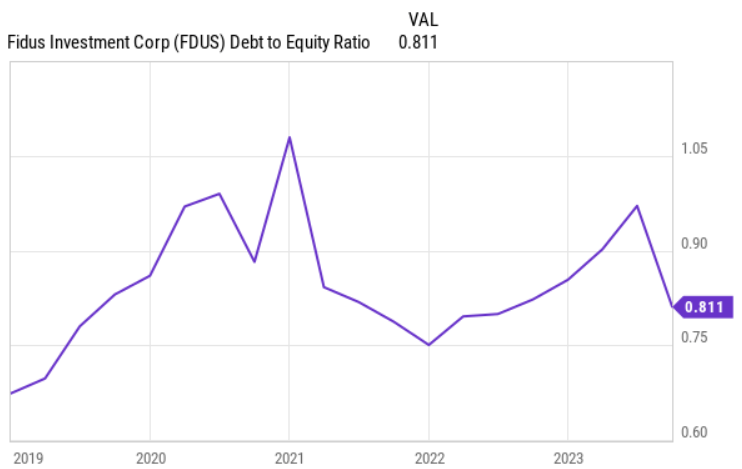

Then, going into 2022 FDUS had timed the de-leveraging process quite well having much smaller exposure to external leverage once the interest rates started to rise. This did not only protect FDUS spreads, but also ensured attractive conditions, where the Management could source in additional debt (without overleveraging the balance sheet) to capitalize on the recent tailwinds in the industry.

{kind=link}

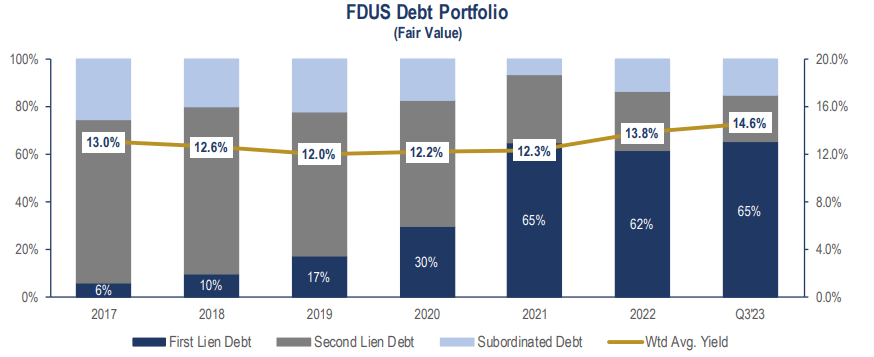

Second source of alpha was the gradual uptick in the first lien debt exposure, which contributed to an even more de-risked FDUS's profile allowing the markets to reprice the position accordingly.

FDUS Investor Presentation

Having said that, the current portfolio of FDUS is still overly skewed towards other positions than first lien debt, which is the safest position to be in as a lender or BDC. Ca. 60% of AuM in first lien is a relatively small part compared to the BDC peer average, where commonly we can observe 70-85% in first lien.

In this situation, FDUS holds rather considerable allocations into more unprotected and riskier debt positions - i.e., second lien and subordinated debt together account for ~34% of the total asset value.

{kind=link}

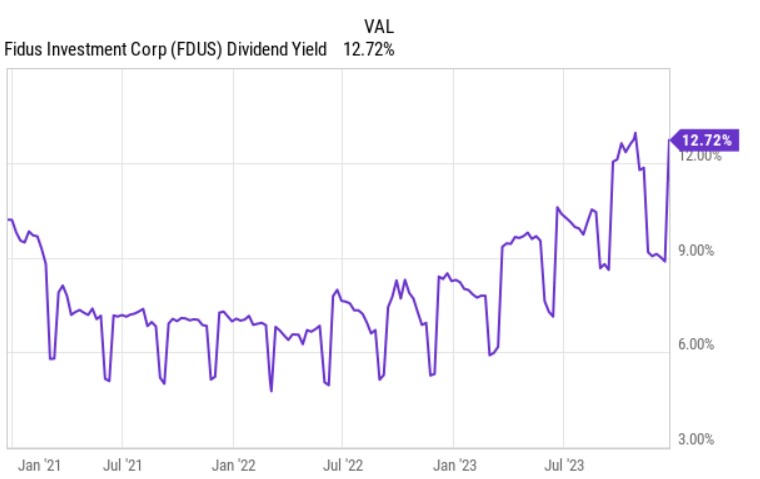

From the dividend yield perspective, FDUS has managed to improve its profile during this high interest rate environment reaching ~14% (based on the TTM quarterly and special dividend payouts). This is a very high level compared to the other BDC players, which on average maintain a yield of 10.5 - 12%.

{kind=link}

However, looking at the recent dividend coverage history, the pattern does not seem great. Namely, in the trailing 4 quarters FDUS has distributes greater dividend than it has earned via NII. This difference has been funded by the realized gains via asset (FDUS's equity investment) sales, which had nicely appreciated in value. So, it is not that FDUS has suddenly decided to go an unsustainable route by paying dividend in excess of its capacity (or the generated value), but investors have to be aware of the fact that the net realized gain element is inherently unpredictable and sooner or later will diminish or even become negative.

The bottom line

While FDUS is a sound BDC with rather resilient portfolio companies in terms of the leverage and industry risks, the current dividend yield of ~14% seems unsustainable as a notable part of it is covered by profitable equity sales.

Plus, FDUS's concentration in non-first lien categories renders the Fund not as conservative as other peers, which also prefer to avoid investments in speculative companies and follow prudent investment underwriting principles.

In my opinion, FDUS offers a subpar exposure to the conservative end of BDC space.

For further details see:

Fidus Investment: Attractive Yield Of 14% Yet A Thin Margin Of Safety