OKE - FIF: Solid Discount For This Diversified Infrastructure Fund

2023-06-29 12:49:44 ET

Summary

- FIF is invested in both the energy and utility sectors, with some of the largest holdings being MLP positions.

- The fund had been raising its distribution slowly but more recently gave a big bump in its payout.

- The fund is deeply discounted and provides diversified exposure to the infrastructure space.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on June 15th, 2023.

First Trust Energy Infrastructure Fund ( FIF ) bumped up its distribution significantly since our previous update. We noted that they would likely continue raising their distribution because of strong coverage. They had previously been raising for several months at a pace of $0.0005, but they ended that streak with a 52.7% increase . That brought it up to $0.10 per month, where we currently remain and are likely to remain at this level for the foreseeable future.

The fund is attractively priced with a deep discount and now offers a more competitive distribution rate. Although, the fund's heavier allocation to energy and utilities has meant some soft performance so far in 2023.

Since our last update , FIF has seen losses on a price basis, but on a total return basis, results have been pretty flat. Some of these declines were from the fund's discount widening during this time.

FIF Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: -0.58

- Discount: -14.63%

- Distribution Yield: 8.43%

- Expense Ratio: 1.45%

- Leverage: 21.20%

- Managed Assets: $331.7 million

- Structure: Perpetual

The objective of FIF is "to seek a high level of total return with an emphasis on current distributions paid to shareholders." They intend to achieve this through "investing primarily in securities of companies engaged in the energy infrastructure sector. These companies principally include publicly-traded master limited partnerships and limited liability companies taxed as partnerships, MLP affiliates, YieldCos, pipeline companies, utilities and other infrastructure-related companies that derive at least 50% of their revenues from operating, or providing services in support of, infrastructure assets such as pipelines, power generation industries."

To sum up, in fewer words, they invest in anything infrastructure-related in the energy and utility sectors. That leaves them quite flexible in investing within these sectors. They also write call options against some of their underlying holdings, which can bring in additional capital gains for the fund's distribution.

FIF is rather modestly leveraged, but given the volatility in the energy space, it's probably best we don't see them get too aggressive with leverage. When including the fund's leverage expenses, the total expense ratio comes to 2.03%.

With the Fed increasing interest rates, the costs of their borrowings have also been rising. Another good reason to be only mildly leveraged as these costs are starting to become quite material as we move out of a zero-rate environment in the last year or so. As of their last annual report for the period ended November 30th, 2022 , the borrowing costs were at 4.75%.

Fortunately, some of their leverage was hedged through interest rate swaps.

{kind=link}

The bad news is that the majority of this hedging expires in just over a year, and we are still likely to be in a higher-rate environment. While the latest saw the Fed pause , they anticipate two more hikes through this year. That would mean any interest rate swaps they may enter into would be more expensive and potentially not worth it if the Fed cuts rates in 2024. To be fair, even the Fed expects to cut interest rates next year, but things can change as we move forward.

Performance - Deep Discount

Since the fund's inception, returns have been much better thanks to the last few years that really drove up the results of this fund. Longer-term results had been much weaker, but thanks to energy getting a massive lift in 2020 and 2021, it's lifted all the annualized returns.

{kind=link}

This fund took significant losses during Covid but had mostly rebounded to pre-Covid levels. For most energy funds, that hasn't taken place. What makes FIF a bit different is that they were more mildly leveraged and held significant exposure to utilities. They had to deleverage like many other energy funds, but to a lesser degree due to these factors. That left them in a position to rebound with more assets. I've always liked that mix because the utilities should have been the hedge to the more cyclical energy exposure.

However, that logic for 2023 is not working. Instead, both the energy and utility sectors are down on a YTD basis. Energy is the worst-performing sector due to commodity prices declining and probably some pressure from an anticipated recession before too long. Utilities have been weaker because, at least partially, due to a rising rate environment. Utilities can become relatively less attractive when interest rates rise because their borrowing costs rise. Utilities are capital-intensive businesses, so they generally go to the debt market to take on new projects. Additionally, higher interest rates mean higher risk-free yields from Treasuries and other safer alternatives.

That being said, while FIF's results aren't anything to brag about on a YTD basis, they are mostly thwarting the drop to put up flat total return results. Heavier exposure to MLPs seems to have helped.

YCharts

Where FIF is attractive is the fund's discount. It's trading well below the long-term average discount for the fund. The only other period that traded below this level for a fairly sustained period of time was during Covid.

YCharts

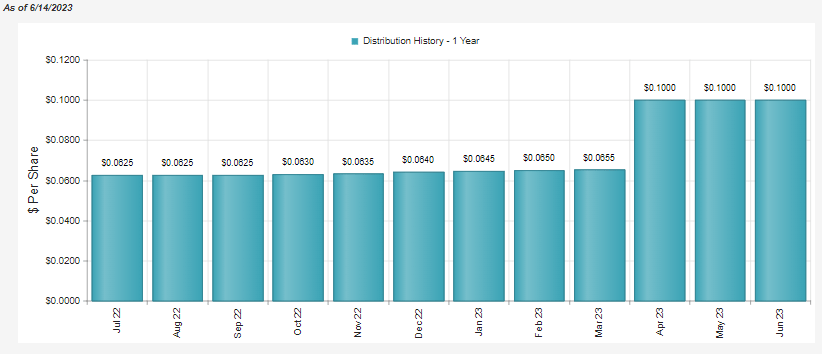

Distribution - Big Bump

In our prior update, we noted that they were raising their distribution every single month. The only problem was that they were raising it at a pace of $0.0005 per month. However, they've more recently bumped it up a more meaningful amount. I would note that this is still below the $0.11 per month pre-Covid.

{kind=link}

The distribution rate for the fund had previously been fairly low relative to other closed-end fund peers. This now puts them in a place where they are competitive in terms of their distribution rate.

Of course, the downside would be that the fund's coverage would now drop meaningfully. The last report showed us a net distributable income of nearly 80%. That would be considered strong coverage in the equity CEF infrastructure space, which is why it seemed clear that further increases were possible.

Based on the last number of shares outstanding and assuming this latest distribution remains going forward, they'll be distributing out around $18.826 million annually. That would put NDI at around 52% based on the latest numbers. However, even that is a bit too high because we know borrowing costs have been rising too. That's why we saw net investment income in their previous report drop.

Given that coverage and expectation for coverage to drop going forward, we are unlikely to see any increases going forward at this point. At the same time, the fund's current distribution rate after that move is more competitive with peers, which could make it more appealing to investors and potentially narrow that discount.

For tax purposes, the fund's distribution has generally shown characterizations of ordinary income and return of capital.

{kind=link}

They had capital loss carryforwards of over $30 million, meaning that they should continue to be able to offset any potential capital gains. ROC, in this case, could also be contributed to by the MLPs that the fund owns. Since they generally pay ROC distributions and FIF is a regulated investment company, those classifications can pass through.

FIF's Portfolio

In looking at the fund's breakdown, they are fairly split between petroleum product transmission, natural gas transmission and electric power & transmission. They also carry a fairly meaningful weight to crude oil transmission too. So they are a well-rounded infrastructure play, but becoming even more balanced was a recent change. While the fund had the heaviest exposure to these same three categories before, they had carried 30%+ in both electric power & transmission and petroleum product transmission.

FIF Industry Breakdown (First Trust)

This was from a prior change where electric power & transmission was over 35% of their portfolio. That's been one area where they've been taking down their exposure, meaning they have been shifting away from utility to more pipeline. Some of this change could be that MLPs had been outperforming utilities in the last year or so.

In looking at the top ten holdings, we see that it's fairly heavily weighted towards these top positions. These represent nearly 52% of the portfolio. According to CEFConnect, they hold 69 total positions.

FIF Top Ten Holdings (First Trust)

This has generally been the case historically. However, at the end of 2022, the top ten accounted for around 46%, meaning we've seen a bit more concentration in the top holdings since.

Enterprise Products Partners ( EPD ) was previously the largest holding, but that's been passed by Magellan Midstream Partners ( MMP ). No doubt, the bid from ONEOK ( OKE ) for MMP has caused this change. Both MLPs had been performing much better than their energy counterparts throughout this year. Then OKE put in a bid to acquire MMP, and MMP received a huge lift. It remains to be seen if this merger will take place as investors push back against the big tax bill that could come with it.

YCharts

In FIF's top ten, we see that Sempra ( SRE ) is the only utility position; previously, the only listed utility position was American Electric Power ( AEP ). They hold more electric gas and multi-utility positions, but they seem to concentrate on several large positions in MLPs and midstreams mostly. Then they have a more diversified pool of utility names.

Conclusion

FIF is a solid infrastructure name offering an attractive discount. The current discount provides a potential opportunity to enter a position in this fund. FIF ramped up its distribution significantly with its latest raise in the payout. With an increased payout, the coverage isn't as strong as it once was. However, as an equity infrastructure fund, it's still anticipated to be at a reasonable level relative to peers.

For further details see:

FIF: Solid Discount For This Diversified Infrastructure Fund