FPL - FIF: This Excellent Energy Infrastructure Fund Is A Good Fit For Any Portfolio

2023-09-21 16:29:58 ET

Summary

- First Trust Energy Infrastructure Fund focuses on investing in companies in the energy infrastructure sector, which are critical for modern life but taken for granted.

- The fund has outperformed its peers, possibly due to its ability to invest in electric utilities and renewables when opportunities exist.

- The fund's portfolio consists primarily of common equity and has a reasonable level of leverage.

- The fund's distribution yield is comparable to the Alerian MLP Index and appears to be sustainable.

- The fund is currently trading at a very attractive valuation.

First Trust Energy Infrastructure Fund ( FIF ) is a closed-end fund, or CEF, that focuses on investing in the companies that perform much of the effort that we all take for granted every day. These companies include things like the midstream natural gas and petroleum companies that transport crude oil and natural gas from the wells in the ground to refineries, midstream companies that move processed gasoline from the refinery to the fueling station where we purchase it, and even those companies that produce electricity and ensure that it is available in our homes and businesses. In short, the companies that this fund invests in are critical for modern society to function, even though many of us do not think about them very much.

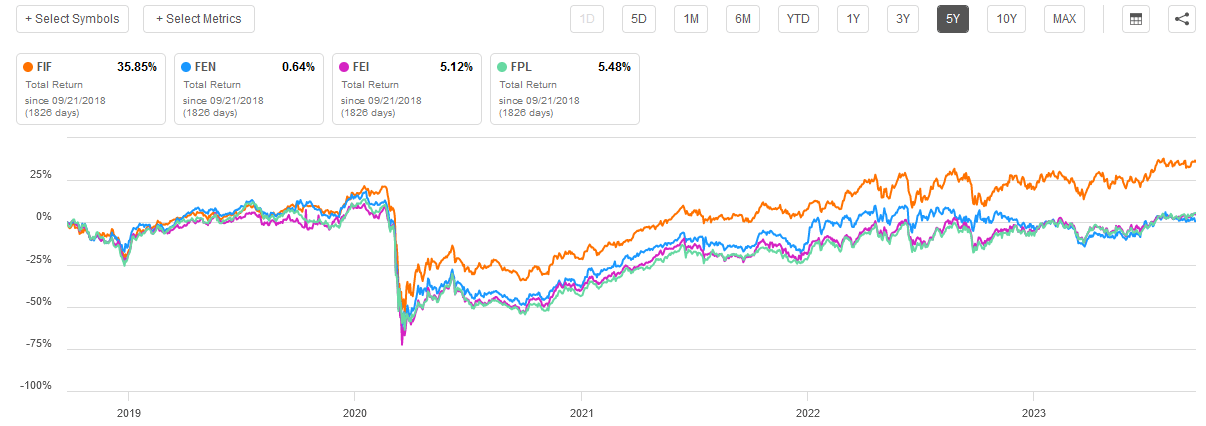

As I pointed out in a recent article , First Trust has a few different funds that invest in energy infrastructure companies but this one has probably the best track record of any of them. We can see this quite clearly in this chart, which shows the total return provided by each of the First Trust energy infrastructure funds over the past five years:

{kind=link}

We can clearly see that First Trust Energy Infrastructure Fund has outperformed its peers by a pretty significant margin. This may be due to this fund’s willingness to leave the fossil fuel energy space and invest in electric utilities during periods in which that makes a great deal of sense. We can see this very easily by looking at this fund’s performance in 2020, as it recovered much more rapidly than its peers following the initial crash that started with the pandemic lockdowns. As you may recall, for much of 2020, crude oil prices remained suppressed, and pretty much anything related to the traditional fossil fuel energy space was not particularly attractive to the market. However, renewable energy companies and electric utilities performed comparatively well as young idealistic people entered the market using their government-provided stimulus checks. The fact that First Trust Energy Infrastructure Fund was able to take advantage of that situation better than its more fossil fuel-oriented peers could have been the deciding factor that accounts for much of the five-year performance difference.

As regular readers will likely recall, we previously discussed the First Trust Energy Infrastructure Fund back in January (full subscribers to Energy Profits in Dividends have more recent analyses available). As such, there is the potential for a great many things to have changed since that time. This article will focus specifically on these changes as well as provide an updated analysis of the fund’s results.

About The Fund

According to the fund’s webpage , the First Trust Energy Infrastructure Fund has the stated objective of providing its investors with a high level of total return. The fund’s website describes its strategy and objectives thusly:

First Trust Energy Infrastructure Fund is a non-diversified, closed-end management investment company. The investment objective of the fund is to seek a high level of total return with an emphasis on current distributions paid to shareholders. The fund pursues its objective by investing primarily in securities of companies engaged in the energy infrastructure sector. These companies principally include publicly-traded master limited partnerships and limited liability companies taxed as partnerships, MLP affiliates, YieldCos, pipeline companies, utilities and other infrastructure-related companies that derive at least 50% of their revenues from operating, or providing services in support of, infrastructure assets such as pipelines, power transmission and petroleum and natural gas storage in the petroleum, natural gas and power generation industries.

The fund’s statement above does not specifically state what securities issued by energy infrastructure companies can be included in its portfolio. Companies in this category have been known to issue bonds, preferred stock, common stock, and other hybrid securities due to their very high need for capital. As the description above does not specify any securities that may be included or excluded, presumably it can invest all across the capital stack. However, the fund is currently only invested in common equity as we can see here:

CEF Connect

As we can see, 92.70% of the fund’s portfolio currently consists of common equity with the rest in cash. This is a fairly substantial cash allocation for a closed-end fund, as the overwhelming majority of them are fully invested. However, I can think of a few reasons why a fund manager might want to maintain such a large cash position. These include:

- A lack of good opportunities to deploy cash. There are times when management cannot find any opportunities in the market that are trading at a reasonable valuation. As such, it may sometimes make sense to simply sit back and wait for a good opportunity to possess itself. When we consider current money market yields, the opportunity cost of doing this is much less than it was only a few years ago.

- Holding funds for distribution. The fund may be holding cash that is earmarked for distribution to the shareholders. If it has no cash, then it has to either borrow money or sell some assets whenever it needs to make a distribution. This could force it to either become more leveraged than its managers desire or sell securities at an undesirable price. The better solution is simply to keep sufficient cash on hand to pay the distribution.

It would not be uncommon to think of cash as a drag on the performance of a portfolio. After all, for most of the past decade, that was indeed the case. However, it is far less so nowadays, and as we can see there are some very good reasons for the fund to be holding such a large cash position.

The fact that the fund’s portfolio consists entirely of common equity despite its apparent ability to invest in a greater variety of securities is not necessarily a bad thing, particularly in the energy infrastructure sector. I discussed the reasoning behind this statement in a previous article :

The high yield on the common equity in most cases gives master limited partnerships a higher yield on the common equity than on the preferred. In such an environment, it makes no real sense for a fund seeking total return to purchase the preferred equity over the common equity. After all, the common equity has a higher yield and significantly better capital gains potential so it will almost always be the higher returning investment. The only real reason to purchase the preferred is that the preferred equity will be somewhat less volatile than the common equity. This could be advantageous during certain circumstances but generally, the common equity of midstream companies has reasonably low volatility. In addition, the preferred equity is theoretically safer in a bankruptcy or forced liquidation scenario. However, in most bankruptcy situations, the assets of the company are insufficient to cover all of the debt so both the common unitholders and the preferred unitholders will get wiped out. Additionally, I doubt very much that most people who want to buy a midstream fund are expecting bankruptcy. Thus, there is no real reason for a fund like this to purchase anything except for the common equity of midstream companies.

Please note that the above comments apply exclusively to midstream companies. The preferred stock of utilities typically has a much higher yield than the common stock of the same company. As such, it could make sense for the fund to purchase preferred stock issued by utility companies as a way to boost its income. However, as we can see here, only 24.52% of the fund’s assets are invested in utilities:

First Trust

There might immediately be a few people who point out that natural gas utilities might be included in the “natural gas transmission” category. It is, however, important to keep in mind that there is a big difference between transmission and distribution in this respect. A natural gas transmission company is a natural gas-focused pipeline operator like The Williams Companies ( WMB ). A pure-play natural gas utility is considered to be a natural gas distribution company. With that said, many of the large natural gas utilities also own midstream companies so there will be a great deal of overlap. However, for the most part, the “Electric Power & Transmission” category encompasses all the companies that the average person would call a utility.

One thing that we notice here is that the electric utility weighting has decreased substantially from the time of our last discussion in January. At that time, 31.01% of the fund’s assets were invested in electric utilities but today only 24.52% are invested in such companies. Thus, it appears that the fund sold down its electric utility holdings over the past several months. However, there might be another cause for this. As I pointed out in numerous previous articles, the utility sector has been struggling somewhat in the high-interest rate environment. This is partly because utilities, which are frequently bought because of their high yields, are much less attractive today than they were eighteen months ago. After all, the majority of utilities currently have a yield that is well below that of money market rates.

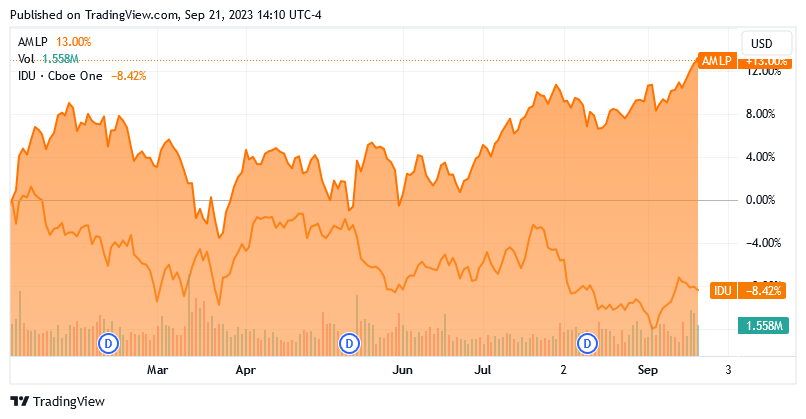

Midstream companies do not have that problem, as most of them still have much higher yields than the money market. As we can see here, the Alerian MLP Index ( AMLP ) has substantially outperformed the U.S. Utilities Index ( IDU ) year-to-date:

{kind=link}

Thus, the decline in utilities as a percentage of the fund’s total assets could be caused by the utilities in the fund substantially underperforming the other holdings in the fund. This situation might not be entirely caused by the fund’s management actively attempting to change the weighting of the portfolio in favor of better-performing assets. With that said though, the fund does have a 60.00% annual turnover, so there is definitely a certain amount of intentional trading between low-performing and high-performing assets occurring within the fund’s portfolio.

In my last article on this fund, I explained why the annual turnover is so important:

This is something that could be important because it costs money to trade stocks or partnership units. These costs are ultimately billed to the shareholders and create something of a challenge for management. After all, management needs to generate sufficient returns to both cover these added costs and still deliver a return that is comparable to a similar index fund. This is a task that very few management teams manage to achieve and as such most actively managed funds underperform their benchmark indices.

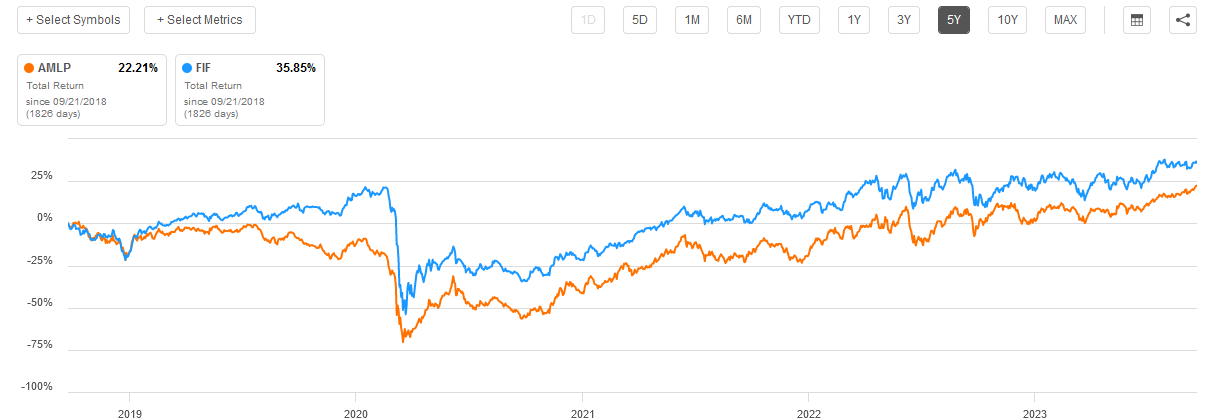

As I noted in my previous article, the First Trust Energy Infrastructure Fund is an exception to the rule regarding the underperformance of most actively managed funds against comparable index funds. As we can clearly see here, the fund has managed to outperform the Alerian MLP Index on a total return basis over the past five years:

{kind=link}

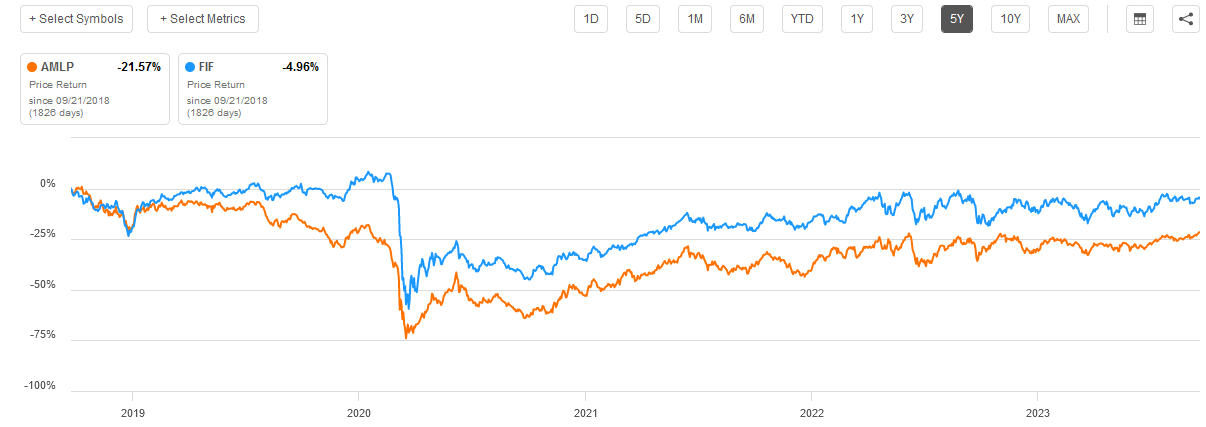

The First Trust Fund manages to outperform the index on a price return basis over the same period as well:

{kind=link}

This is probably due to the fact that the First Trust Energy Infrastructure Fund is able to include some assets that the index does not, such as the aforementioned electric utilities that outperformed in the first few months following the COVID-19 lockdowns. The improved flexibility that this fund has versus the index is thus a strength and the fund’s management appears competent about using it.

With that said, investors should never assume that past performance is a guarantee of future results. However, the fact that this fund enjoys a great deal of flexibility relative to the Alerian MLP Index is a strength that we should clearly not discount.

Leverage

One characteristic of most closed-end funds is that they employ leverage as a means of boosting their returns compared to the actual performance of the assets in the portfolio. The First Trust Energy Infrastructure Fund is no exception to the use of this strategy as a means to boost the return that it provides investors. I explained how this works in multiple past articles on other closed-end funds:

In short, the fund borrows money and then uses that borrowed money to purchase the common equity issued by master limited partnerships, midstream corporations, electric utilities, and other energy infrastructure companies. As long as the total return that the fund received from the purchased assets is higher than the interest rate that it needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield and total return of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will normally be the case. However, it is important to note that this strategy is less effective at boosting returns today with borrowing rates at 6% than it was eighteen months ago when the borrowing rate was basically zero. This is because the difference between the rate which the fund pays on the borrowed money and the total return that it can receive on the purchased assets is much narrower than it used to be.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like a fund’s leverage to exceed a third as a percentage of its assets for this reason.

As of the time of writing, the First Trust Energy Infrastructure Fund has leveraged assets comprising 20.35% of its portfolio. This is well within our acceptable limit and thus represents a fairly good balance between risk and reward. It is also in line with most other closed-end funds that invest in this sector, so we should not need to worry too much about the fund’s leverage right now.

Distribution Analysis

Perhaps the biggest reason why most people purchase the common equity of midstream companies and partnerships is the incredibly high yields that these entities typically possess. As of the time of writing, the Alerian MLP Index boasts a 7.82% yield, which clearly illustrates the high yield possessed by many of these companies. The First Trust Energy Infrastructure Fund invests in a portfolio consisting primarily of high-yielding midstream partnerships and corporations like the ones that are included in that index. It then adds a layer of leverage to boost the effective yield of its portfolio assets. The fund also attempts to realize capital gains when appropriate to generate additional returns for its investors. It then pays out all of this money to its investors, net of the fund’s expenses.

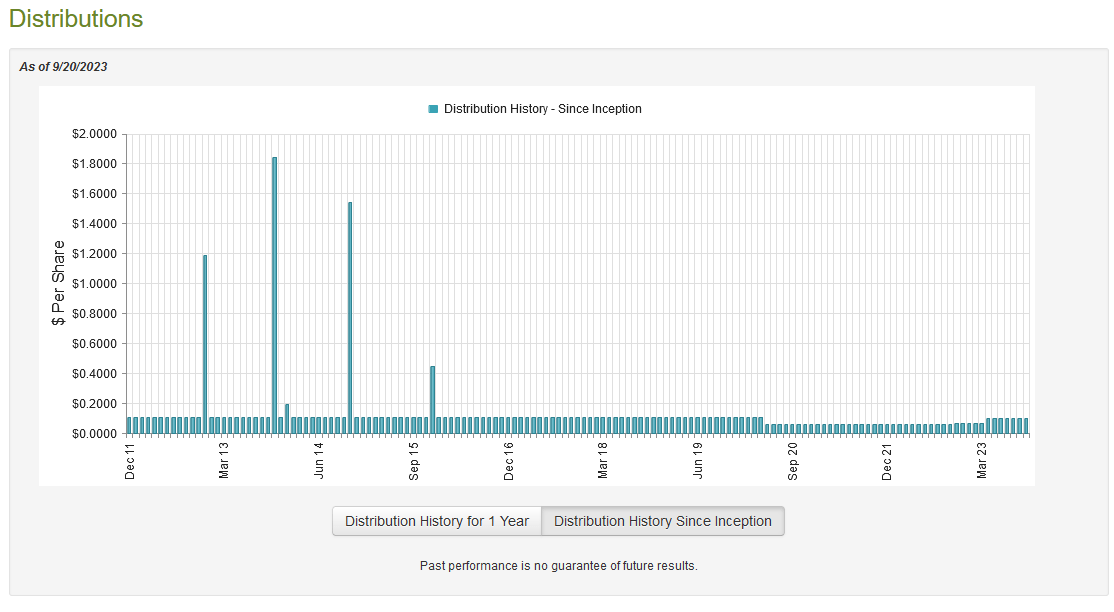

As such, we might expect that the First Trust Energy Infrastructure Fund would have a very high yield. This is certainly the case, as the fund currently pays out a monthly distribution of $0.10 per share ($1.20 per share annually), which gives it a 7.79% yield at the current price. This is a very reasonable yield that is in line with the Alerian MLP Index, which is nice. However, the fund has not been perfectly consistent with respect to its distribution over the years:

{kind=link}

As we can see, the fund has changed its distribution over the past decade, but it has still been much more consistent than most energy infrastructure funds. The only cut that we see here came in response to the pandemic, which temporarily drove down the price of everything in the market. While the utility sector recovered rather quickly, the midstream sector did not, and, indeed, anything related to fossil fuels became toxic for a while. Arguably, the sector is still somewhat toxic as indicated by the fact that most energy companies are substantially undervalued relative to companies in other sectors. Regardless, the fact that everything went down sharply forced the fund to slash its distribution to avoid paying out more money than it could afford. It has since been able to raise its distribution, although it is still about 10% lower than it was prior to the pandemic ($0.10 per share monthly versus $0.11 per share monthly).

The fund’s history may reduce its appeal somewhat in the eyes of those investors who are seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. However, it still exhibited far more consistency than First Trust’s other funds that cover this sector. As I have pointed out in various past articles though, the fund’s past is not necessarily the most important thing today. After all, anyone buying the fund today will receive the current distribution at the current yield and will not be adversely affected by the events of the past. Thus, we should investigate how well the fund is covering its current distribution and determine how sustainable it is likely to be.

Fortunately, we do have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is a much more recent report than the one that we had available to us the last time that we discussed this fund. That is nice as it should give us some insight into how well the fund handled the weak energy price environment that existed throughout most of the first half of this year. It also might give us some insight into how well the fund was able to take advantage of last year's booming energy market.

During the six-month period, the First Trust Energy Infrastructure Fund received $3,572,615 in dividends along with $418,623 in interest from the assets in its portfolio. This gives the fund a total investment income of $3,991,238 during the period. It paid its expenses out of this amount, which left it with $61,562 available to shareholders. Obviously, this was nowhere close to enough to cover the fund’s distributions, which totaled $7,192,130 during the period. At first glance, this may be concerning as the fund’s net investment income was nowhere near enough to cover the amounts that it actually paid out.

However, there are other ways through which a fund like this can obtain the money that it needs to cover its distributions. For example, it undoubtedly received some money from the master limited partnerships in its portfolio. Distributions received from these companies are not considered to be investment income for tax purposes, but they still clearly represent money that can be paid out to investors. In addition to this, the fund might have been able to achieve some capital gains that can be paid out. The fund had mixed results in this task during the six-month period. The First Trust Energy Infrastructure Fund reported net realized gains of $14,105,768 but this was offset by $33,946,470 in net unrealized losses. Overall, the fund’s assets went down by $27,304,359 during the period. However, as I have mentioned in previous articles, net unrealized losses can be quickly undone by a market correction so we can ignore them when analyzing distribution sustainability. In this case, the fund had more than enough net investment income and net realized gains to cover its distributions. In fact, the fund came pretty close to covering its full-year distribution in only the first six months of its fiscal year. As such, we probably do not need to worry about a distribution cut anytime soon. This fund looks solid right now.

Valuation

As of September 20, 2023 (the most recent date for which data is available as of the time of writing), the First Trust Energy Infrastructure Fund has a net asset value of $17.56 per share but the shares only trade for $15.36 each. This gives the fund’s shares a 12.53% discount on net asset value at the current price. This is a very reasonable discount that is a bit better than the 11.68% discount that the fund’s shares have averaged over the past month. In addition, a double-digit discount is generally a good price to pay for any fund. As such, the price certainly seems to be acceptable here if the fund interests you.

Conclusion

In conclusion, the First Trust Energy Infrastructure Fund is a very well-run fund with a great deal of flexibility. It is the best-performing of First Trust’s offerings of energy infrastructure funds, which might be because of its ability to switch its assets between utilities and midstream companies. The distribution is comparable to the Alerian MLP Index, and it trades at a very attractive valuation, which are both things that could be very attractive to any potential buyer today. Overall, this fund may be worth including in the portfolio of any energy income investor.

For further details see:

FIF: This Excellent Energy Infrastructure Fund Is A Good Fit For Any Portfolio