UAA - Finding Hope Amidst Under Armour's Challenging Outlook

2023-06-22 15:48:14 ET

Summary

- Under Armour's Q4 results and 2024 outlook are disappointing, with flat to slightly increased revenue expected.

- The key issue for the company is brand perception, as it struggles to compete with rivals like Nike and Lululemon.

- Despite these challenges, I upgrade the rating from "Sell" to "Hold" due to the potential for a slight growth in sales as consumers seek lower-priced brands.

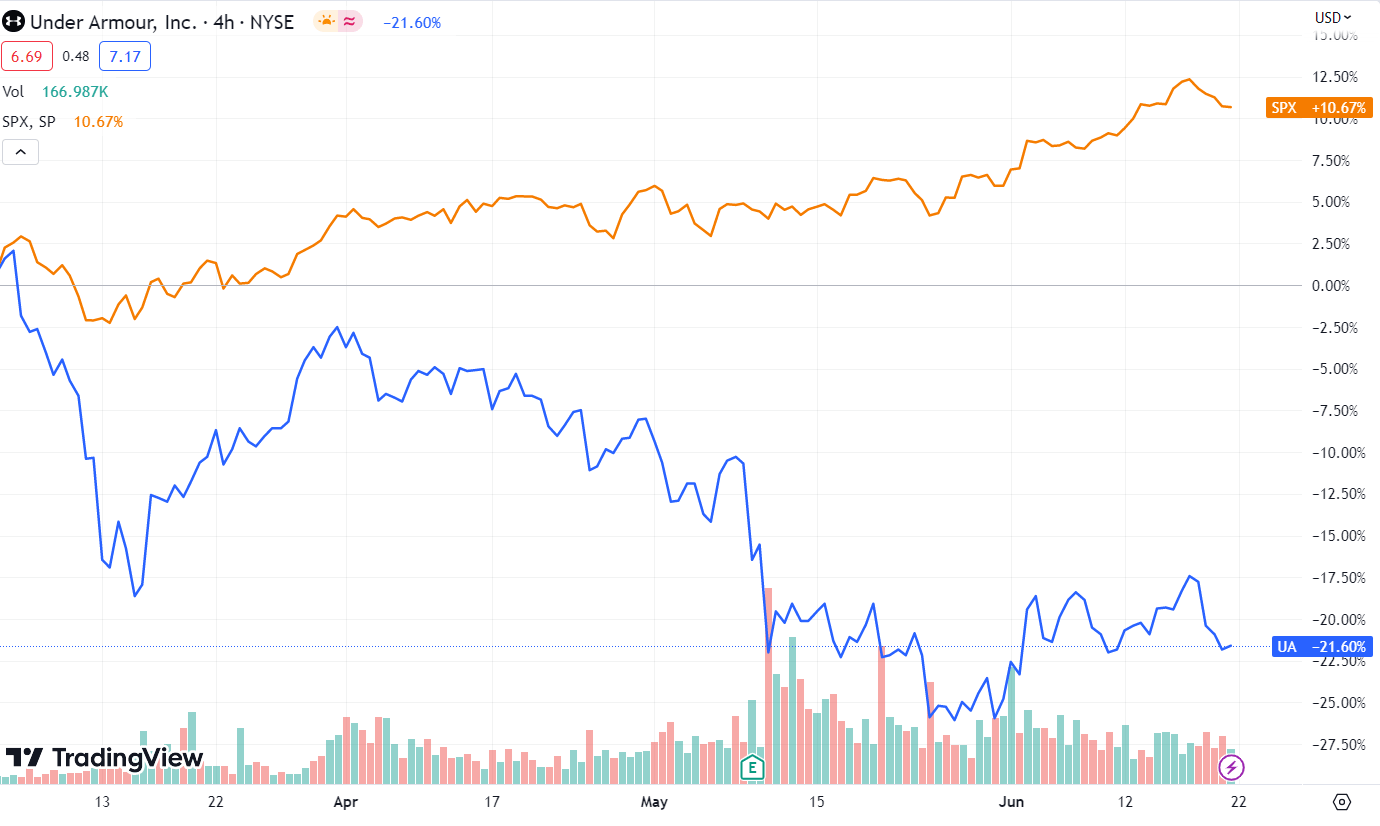

Since my last article on Under Armour ( UAA ) ( UA ), which you can find here , the company's fundamentals have not only remained unchanged but have actually worsened slightly. In my previous article, I assigned a "Sell" rating to the company. Since then, from March 6, 2023, Under Armour has experienced a decline of 19.29%, while the S&P 500 has shown a positive return of 7.84% during the same period. These developments bring the stock closer to my previously determined price target.

{kind=link}

UA vs SPX (Tradingview)

As I had highlighted in my previous article, in the coming months (so March, April and May 2023), I expected the challenges for Under Armour to exacerbate due to inflationary pressures and inventory issues. However, the most significant concern lies in the problems related to brand perception, which would further compound the effects of these issues. Unfortunately, for those who had long positions in the company, the outcome has aligned with my initial expectations.

So, in this article, I will delve into the analysis of Under Armour's Q4 results and the outlook for 2024, and present a bold theory suggesting that the brand's issues might paradoxically contribute to slowing down the decline in share price before eventually going below $6.00.

Q4 Results and 2024 outlook are disappointing

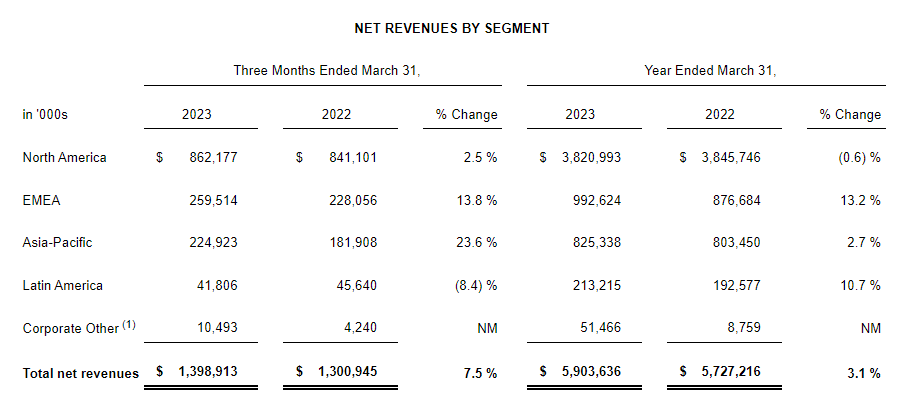

Let's delve into the results of Q4 2023 . Despite experiencing an 8% revenue growth compared to the same quarter in 2022, the full-year revenue for 2023 only increased by 3%. This growth rate is relatively low, especially when considering the expansion of the market (which is estimated to be +6.7%) and the growth of competitors.

When examining the Q4 results in detail, we find that while North America saw a modest growth of only +2.5% compared to the previous year, Under Armour was saved by the EMEA segment, which recorded a growth of +13.8%, and the Asia-Pacific segment, which experienced an impressive +23.6% growth. This significant growth in the Asia-Pacific region can be attributed to the reopening of China and an increase in consumer spending in the region.

{kind=link}

UA Revenues by Region (Under Armour Q4 Results)

However, despite these positive aspects, the overall results remain disappointing, particularly in North America, which constitutes 61.6% of Under Armour's revenue. Competitors such as Nike and Lululemon have outperformed Under Armour by a wide margin in this region.

The company's results were in contrast to industry peers Nike Inc and Lululemon Athletica, which have seen a steady demand for their products in the recent quarter despite an inventory glut.

"Under Armour brand does not generate the same levels of loyalty or traction as some competitors and so it is far easier for customers to deprioritize it when times get tough," said Neil Saunders, managing director at GlobalData.

(Source: Reuters)

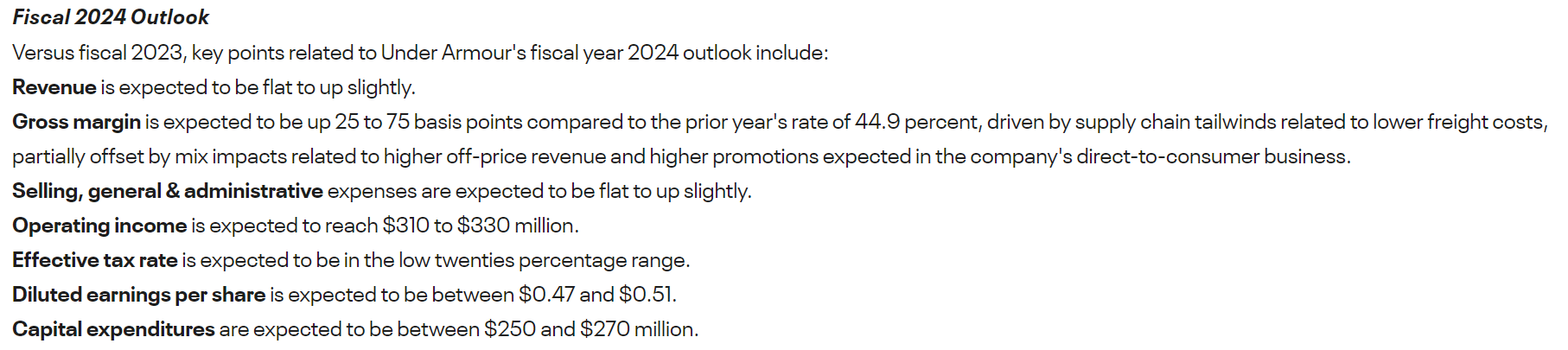

Undoubtedly, 2023 has been a challenging year for Under Armour, and unfortunately, it appears that 2024 is following a similar trajectory.

{kind=link}

UA FY24 Forecast (Under Armour press release)

According to the latest press release:

Revenue is expected to be flat to up slightly.

(Source: Under Armour press release )

This forecast is certainly not a positive sign for investors.

The brand perception is still the key issue

However, the perception consumers have of the Under Armour brand remains the most crucial factor to consider. To illustrate this point, let's quickly compare Nike and Apple, examining their respective multiples. Currently, Apple has a PE ratio of 30.80, which is justified by its strong brand and the industry it operates in. On the other hand, Nike has a higher PE ratio of 34.08, surpassing even that of Apple. While PE ratio is not indicative of the health of a company, it serves to me to highlight one important aspect: brand value matters significantly! A company with a powerful brand like Nike is valued on the same level as one of the largest and most renowned companies in the world. Nike has become a status symbol for many by entering mainstream fashion, attracting a highly loyal customer base.

However, the same cannot be said for Under Armour. Despite the high quality of its products, the brand is undervalued in comparison to its main competitors.

Another significant problem for the company arises from a snowball effect that has been occurring for some time, primarily due to high inventory levels and the implementation of promotions to clear excess stock.

In my previous article, I expressed my concerns:

What concerns me the most, is that Under Armour's inventory levels increased by 50% YoY to $1.2 billion, which could be due to weak sales or overproduction. Moreover, the company's gross margins declined YoY by 650 bps to 44.2%, due to the shift towards e-commerce sales and higher promotions. This activity may be necessary to drive sales, but it is not sustainable in the long run!

Therefore, Under Armour must quickly address inventory levels and focus on improving gross margins to remain competitive in the industry before it is too late, as this situation could lead to an oversupply and further margin reductions.

(Source: Under Armour: Still In Troubled Waters)

Although the inventory in Q4 came out slightly below estimates, increasing by 44% to $1.2 billion instead of the anticipated 50%, this still had a significant impact on the gross margin, which declined to 43.4% (a drop of 310 basis points!). To clear excess inventory, management had to offer greater product discounts. However, in the eyes of consumers, these discounts may diminish the perceived value of the brand, exacerbating the existing crisis surrounding the Under Armour brand.

Therefore, if this downward spiral is not effectively controlled, it risks further deteriorating the company's position, despite the efforts made by management in the last few years.

The parachute effect (my bold theory)

However, Under Armour's discounts and brand perception could potentially stem the free fall in the company's share price that has occurred in the last few months. There is one concept: despite the improvement in inflation, which reached its lowest since November 2021 (CPI at +4%, while CPI Core at +5.3%), credit conditions still remain precarious, while the Fed (fed funds at 5-5.25%) is preparing for further hikes in the coming months. These factors ultimately impact consumer spending.

...the least well-off increasingly rely on credit in their day-to-day lives. Roughly 29% of households earning less than $50,000 per year are using credit cards to finance their spending, according to economists at the Bank of America Institute.

Analysts at the New York Federal Reserve report record levels of credit card debt in 2023.

(Source: CNBC )

Consequently, consumers are becoming more cautious about their expenditures, striving to save wherever possible.

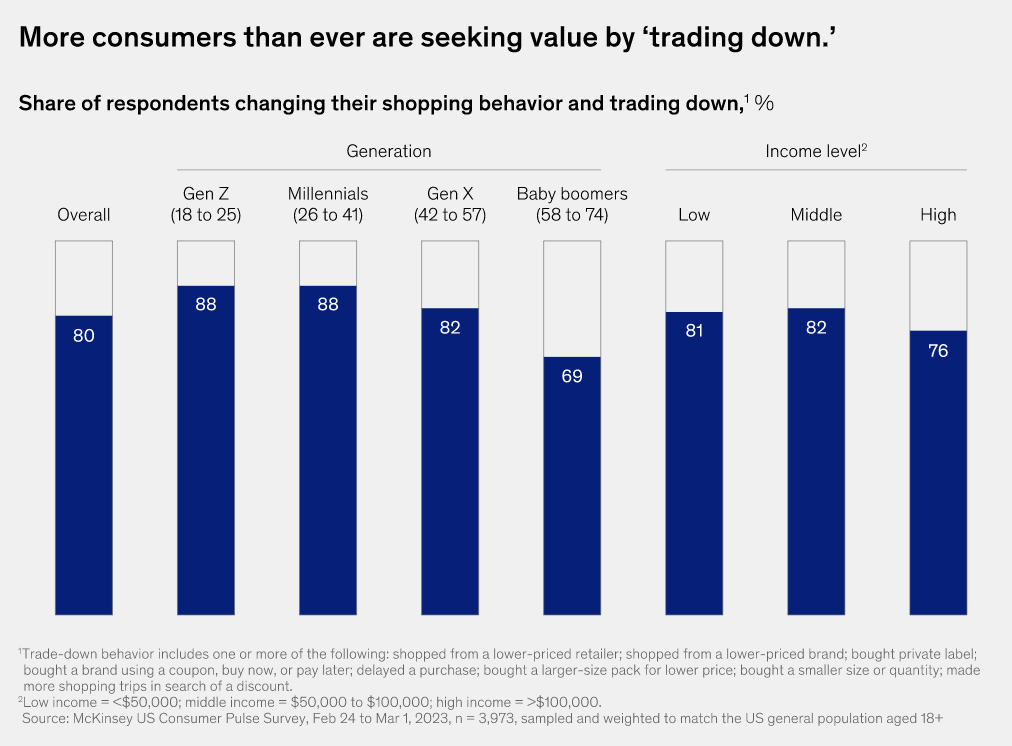

According to a study by McKinsey:

Consumers are trading down, seeking savings. Despite continuing to spend, they are prioritizing value. Eighty percent of our survey respondents stated that they are changing their shopping behavior by trading down.

Trade-down behavior includes one or more of the following: shopping from lower-priced retailers, purchasing lower-priced brands, ...

(Source: McKinsey )

{kind=link}

Trade-down in consumer spending (McKinsey)

Therefore, in the coming months, we may witness a trend where customers of premium brands, in an effort to reduce expenses, opt for lower-priced brands. Under Armour positions itself within this segment.

While it is highly unlikely that we will observe a +100% increase in sales next quarter, it is reasonable to expect that at least some consumers of premium brands may make the switch to lower-priced brands to save money.

Hence, in my opinion, we could potentially see a slight growth despite the flat growth forecasts provided in the 2024 guidance. This, in turn, could help mitigate the decline in the share price, acting as a sort of "parachute.”

Bottom Line

As you can probably tell, I'm not very bullish on the company. In my opinion, it is crucial for Under Armour to address significant issues such as the brand problem, as I highlighted in my previous article. While the company may be undervalued compared to market multiples and competitors, that alone doesn't automatically make it a value opportunity. Ultimately, the strength of the business is what matters.

Nevertheless, with the share price having declined by nearly -20% in the past three months, it is approaching a significant support level at $6.50 ($6 for UA, $6.50 for UAA). I personally have doubts that it will break below that level, as a substantial portion of the "bad news" and issues are already partially priced in. Therefore, while I still see a potential -10% downside from the current price of $7.45 for UAA, I am upgrading the rating from "Sell" to "Hold," as there is little room for opening a short position on the company.

For further details see:

Finding Hope Amidst Under Armour's Challenging Outlook