OGI - Finding The Long-Term Winners In The Cannabis Sector

2023-03-27 01:16:04 ET

Summary

- This developing industry has ample opportunity and sustained tailwinds.

- Very few U.S. companies have positive operating margins; very few of their Canadian counterparts have positive gross margins.

- Since most of the ETFs are full of cash-burning companies, I believe picking a handful of individual companies is better.

Thesis

On October 6th 2022 , Biden asked the Attorney General and the Department of Health and Human Services to begin the process of rescheduling cannabis to something more appropriate based on available evidence. It is unclear which classification it will be rescheduled to, but once it is moved away from Schedule-1 to a scheduling more appropriate for its characteristics, both the 280e tax obligation and the federal restrictions to moving it across state lines will be removed. The news of rescheduling is almost certainly going to cause yet another sector wide rally.

With the next cannabis rally seemingly inevitable, it sounds like a no-brainer to make an investment now, with plans to sell into the top of the next rally, but that has its own perils. This is an emerging industry full of struggling companies, only a few of them are going to thrive in the post rescheduling ecosystem. Dilution is already a common problem and depending on how long the DHHS takes to announce news, some of them could experience another round of dilution before rescheduling.

Since the ETFs are all baskets of stocks representing the sector, this same problem also plagues the cannabis ETFs. Investing into ETFs is fantastic for well-established industries but for emerging industries, with competition fierce and failure rampant, I have always felt it was a poor decision. The conclusion I came to is to try and build myself a basket of stocks based on gross margins and revenue growth, knowing the better companies are both less likely to dilute me while I wait, and will be better able to thrive during the period of extreme competition I expect to follow rescheduling.

Long-Term Trends

The cannabis industry in the United States is projected to have a CAGR of 14.2% through 2030. The Canadian cannabis industry is expected to have a CAGR of 13.26% through 2027. Several of these companies have plans to expand into Germany, so it's prudent to bring up its projected CAGR of 14.01% until 2027. CBD is expected to have a global CAGR of 31.5% through 2031.

The United State Cannabis Market

Because cannabis is currently considered a Schedule-1 drug by the United States Federal Government, it is not allowed to be moved across state lines. This has produced a situation where each separate state is its own market, with both limited supply and a limited customer base. Companies are encouraged to vertically integrate to avoid supply problems and so have become sort of pseudo-monopolies, where they have significant but not total control over both supply and price. The end result of this is that prices in the United States vary dramatically based on location.

{kind=link}

I fully expect that as soon as it is allowed to be shipped across state lines, competition will drive the price of wholesale cannabis in the United States down toward Oregon's level. This means those companies that are used to operating in the more expensive markets are going to see the largest margin contractions.

A Look At Margins And Growth In The U.S.

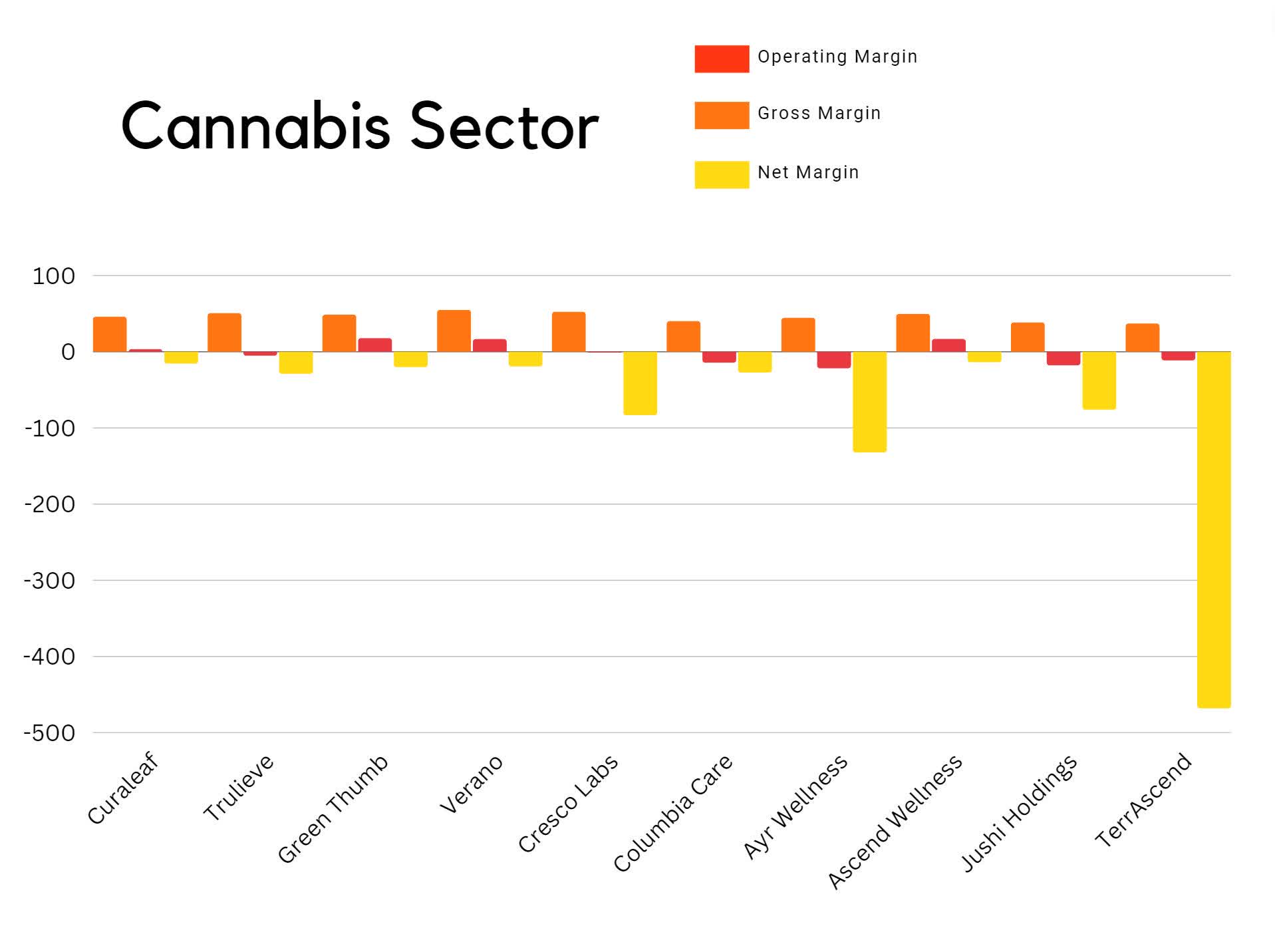

The companies that have the best gross margins and growth today, are the most likely to thrive in the coming price war. Before I start talking about these companies I should state that I intentionally excluded companies that were not pure play cannabis companies. So, Scotts Miracle-Gro ( SMG ) and Innovative Industrial Properties ( IIPR ) are not on here. All of the charts were produced using the most recent quarterly reports, so this is just a snapshot in time and all these numbers will all be different in another 3 months. Also, I am only comparing margins and growth here because when the next sector rally arrives, I expect most or all of these companies to raise money through at-the-market offerings. This means looking at present day cash on hand for any of these companies isn't going to be a very useful indication of what things will be like later. For context, the 280e tax obligation forces these companies to pay taxes before they are allowed to deduct operating expenses. It's incredibly difficult to produce a business model that is profitable through that.

U.S. Cannabis Margins (Blake Downer)

{kind=link}

So let's take a look at what removing the tax obligations does for net margins. As we can see without the taxes, a couple of the companies are close to or just above net income positive. We can also see that TerrAscend ( TRSSF ) is singlehandedly skewing the chart. Looking into their financials, that loss was the result of an unusual item, so let's move on to the next chart.

U.S. Cannabis Margins Without Taxes (Blake Downer)

{kind=link}

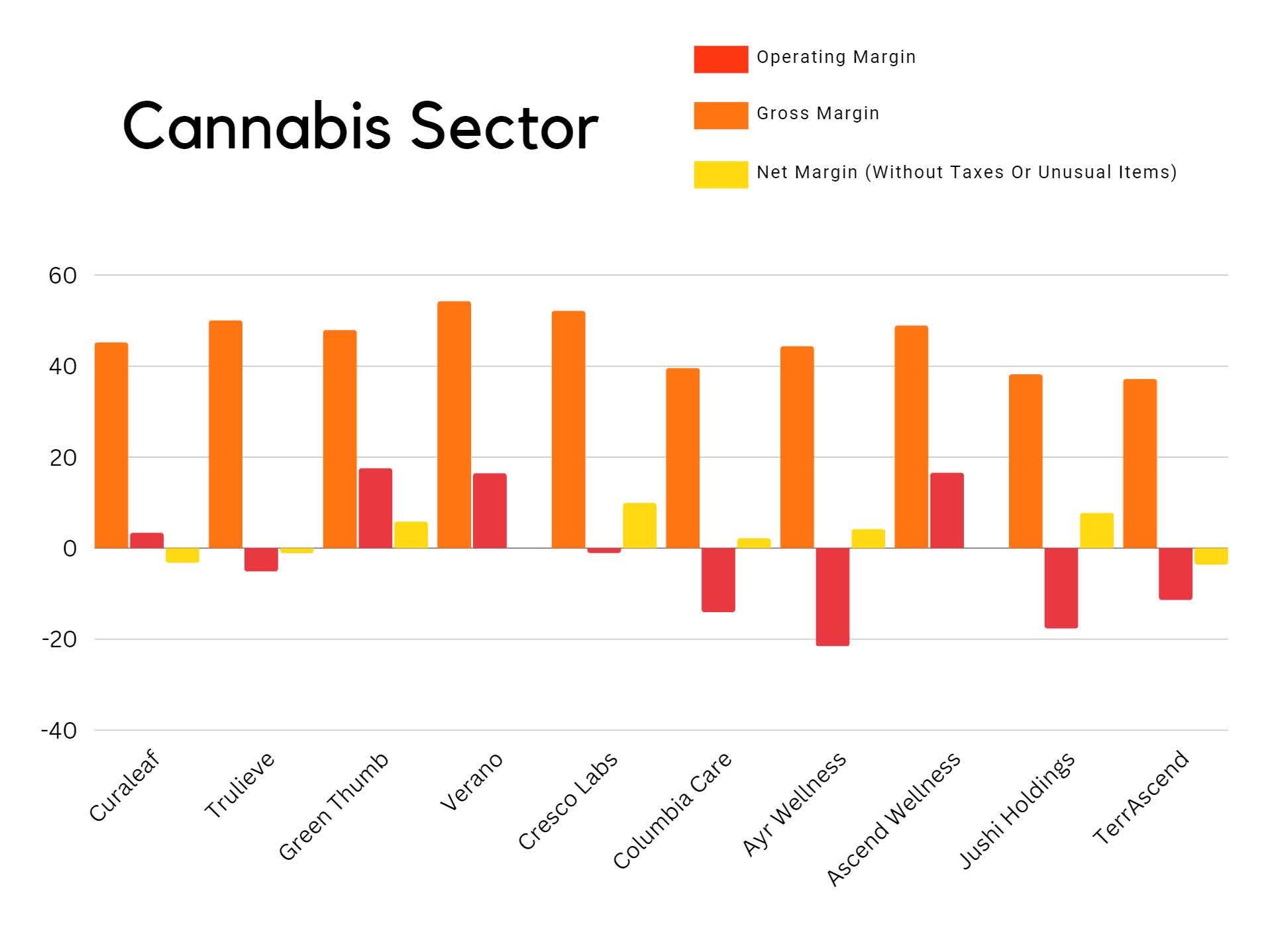

Here we have both taxes and write-downs removed. Taking a look at the 10 largest companies in the U.S. by revenue, it becomes clear that not all of them are created equal. While they all have gross margins in the 30 to 50% range, only four of them have positive operating margins. The narrative around this sector is that it is the tax obligation that's preventing them from becoming profitable but most of these companies wouldn't be operationally viable even if we remove their tax burden.

U.S. Cannabis Margins Without Taxes Or Unusual Items (Blake Downer)

{kind=link}

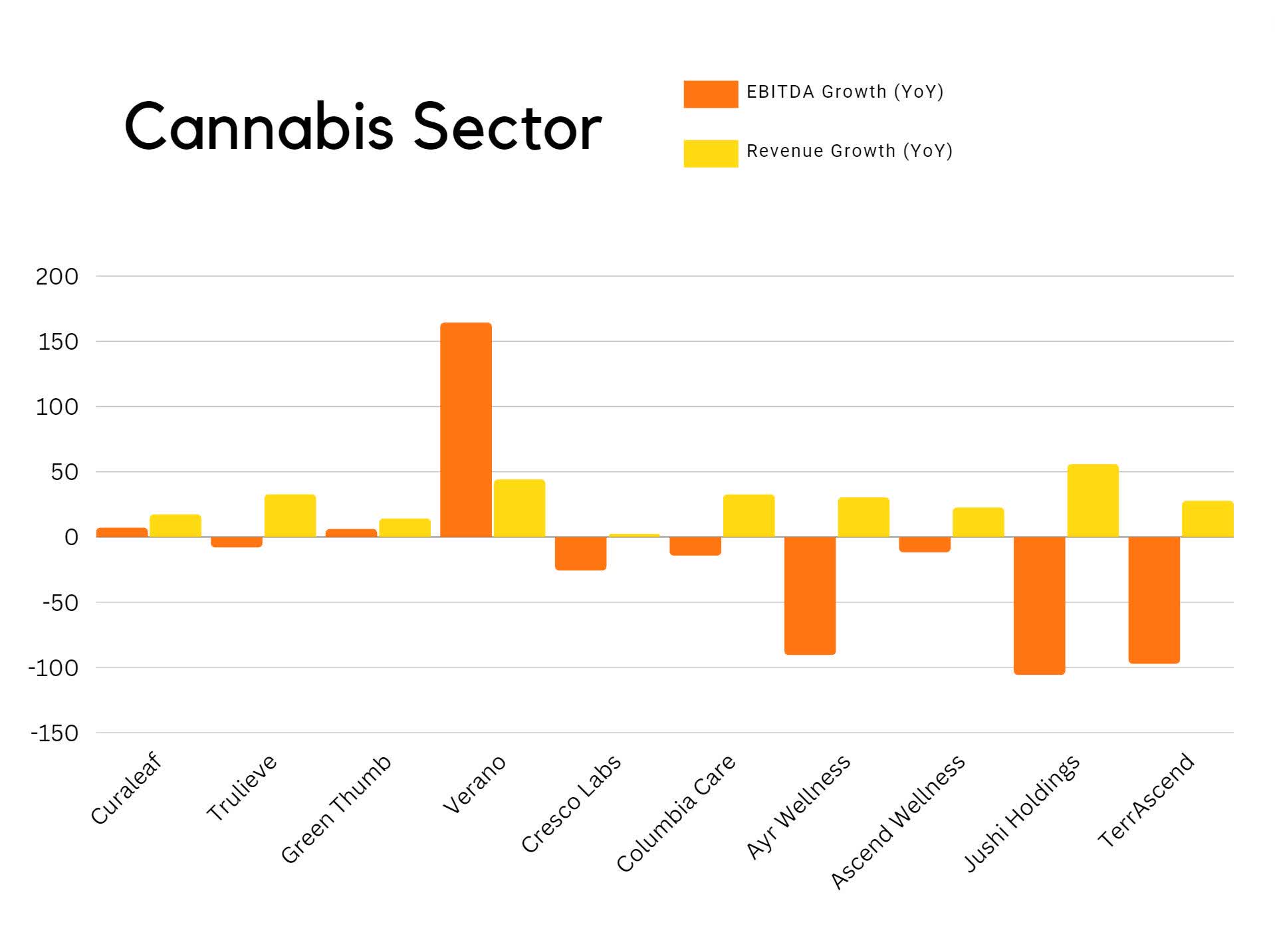

Taking a look at the growth these companies have been managing to achieve under this tax burden makes it clear that most of the sector has been experiencing noticeable revenue growth, but Verano Holdings ( VRNOF ) is a standout for EBITDA improvement.

U.S. Cannabis Growth (Blake Downer)

{kind=link}

A Look At Margins And Growth In Canada

While the United States market is characterized by its 50 separate ecosystems and brutal tax obligations, in Canada all the companies are suffering because of the price war. When Canada changed its laws in 2018, a wave of fresh money flowed into the sector and a new legal market emerged. Overproduction and competition drove the price of cannabis below the cost of production for most growers, and the market has been in a period of aggressive consolidation since then.

{kind=link}

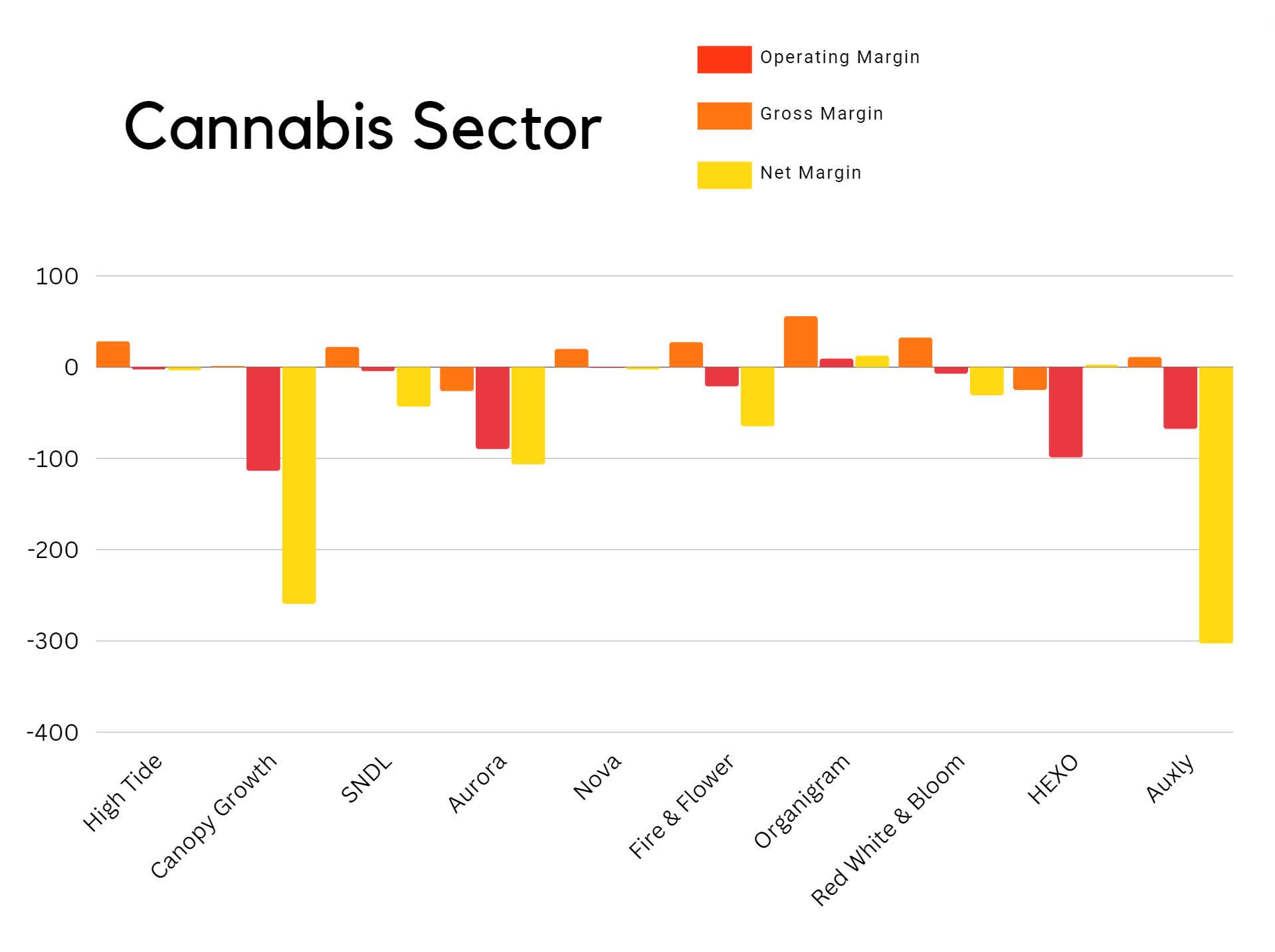

With end use consumers able to purchase cannabis for $100.12 CAD or about $75 USD per oz., negative operating margins are common. A majority of the cannabis companies in Canada regularly take large write downs. They skew the net margins on the below chart.

Canadian Cannabis Margins (Blake Downer)

{kind=link}

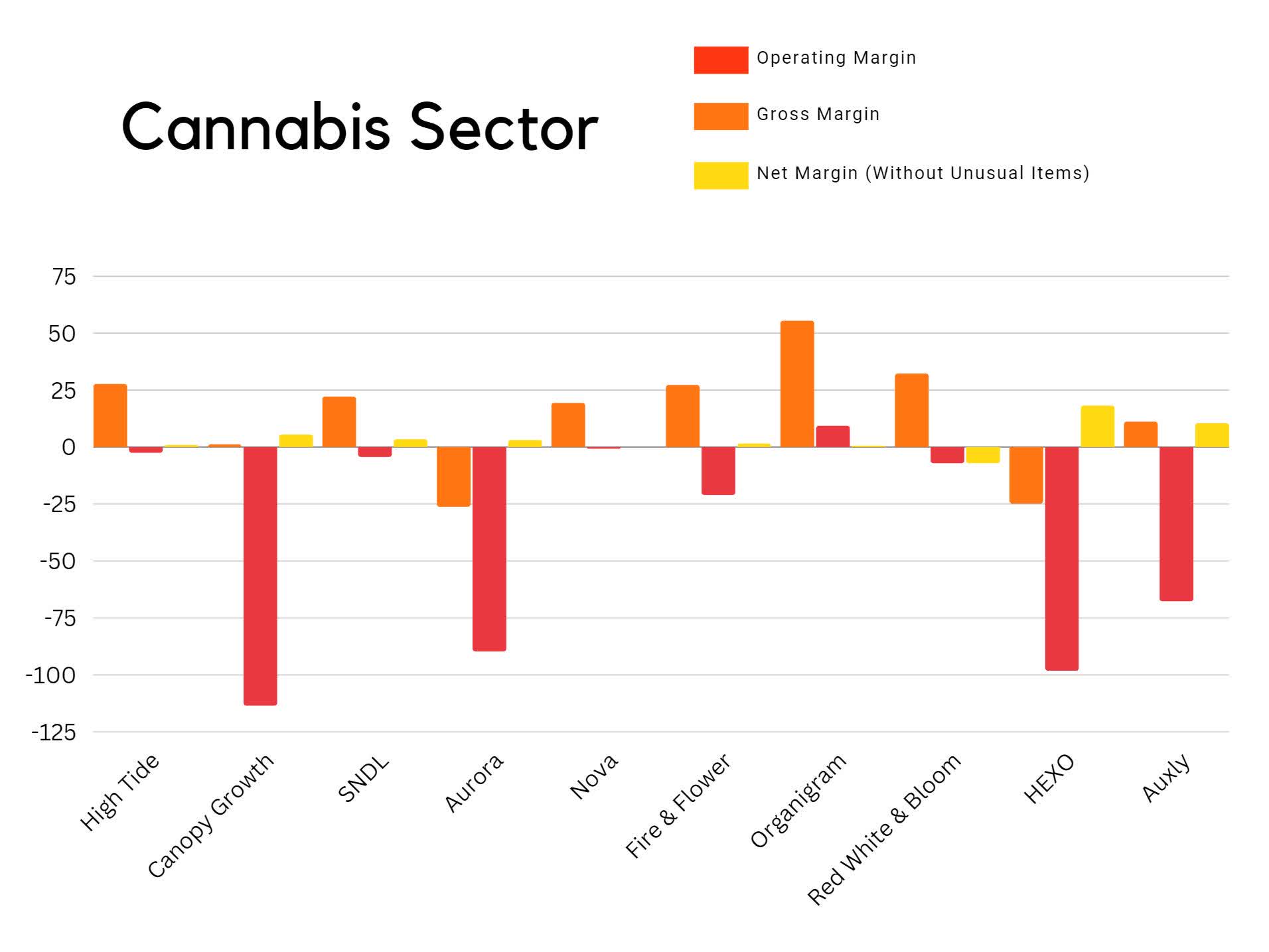

The following chart is if we were to remove the Unusual Items from their financial statements. It's not that I believe they don't belong, they do. It's just that removing them gives us a more clear picture of what these companies might look like if they weren't constantly writing down the value of their assets.

Canadian Cannabis Margins Without Unusual Items (Blake Downer)

{kind=link}

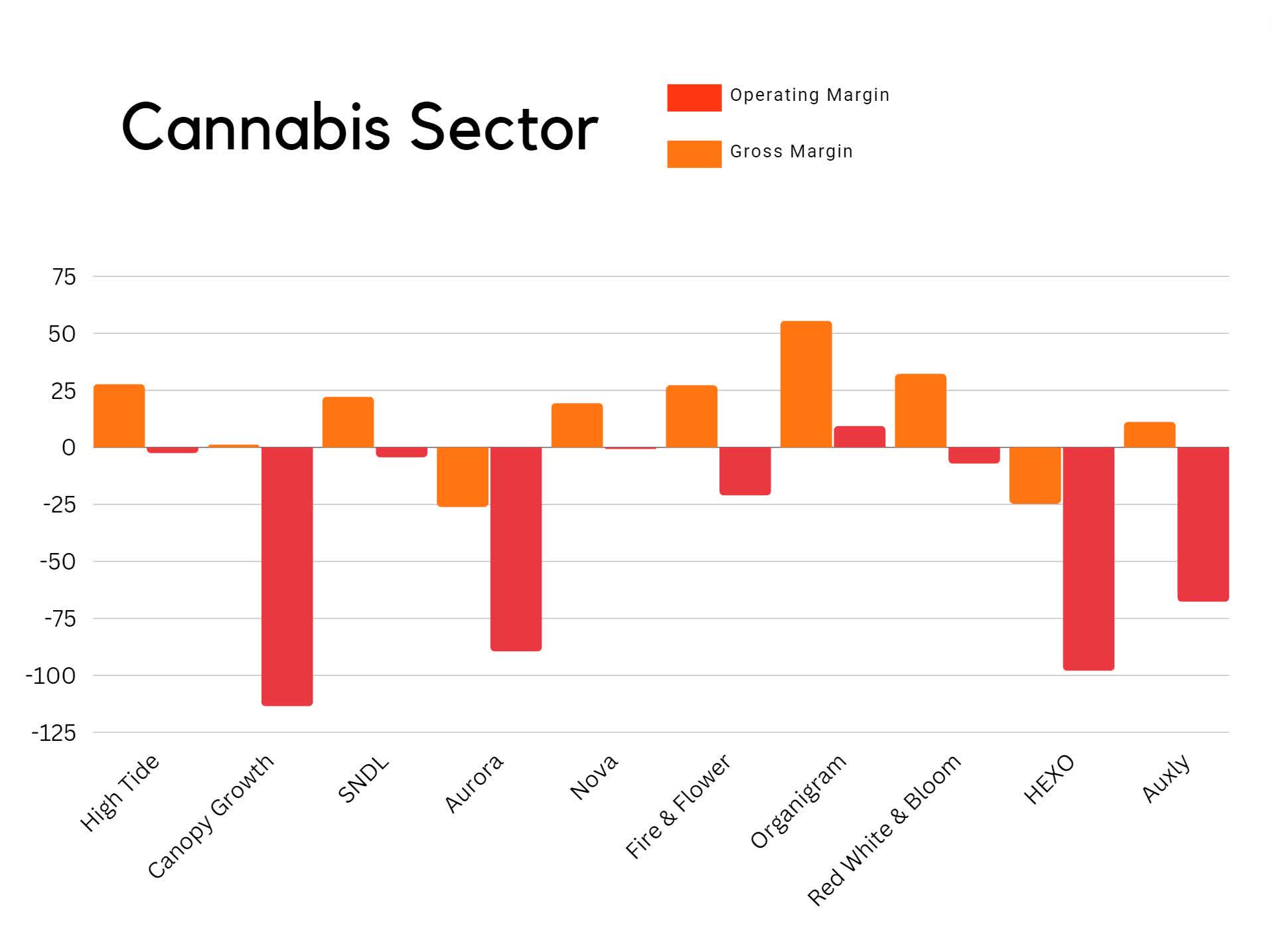

Removing net margins entirely gives us a more clear picture of what gross margins and operating margins look like. Similar to the U.S., but for different reasons, several of these companies have large negative operating margins.

Canadian Cannabis Gross and Operating Margins (Blake Downer)

{kind=link}

When trying to look at the growth for these ten companies, the growth rate on SNDL Inc. ( SNDL ) is skewing the chart. During the last rally, SNDL was able to raise over a billion dollars with offerings and has been using that money to buy up the assets of their competitors as most of the sector faces bankruptcy. Their revenue growth is not organic, they are purchasing it.

Canadian Cannabis Growth (Blake Downer)

{kind=link}

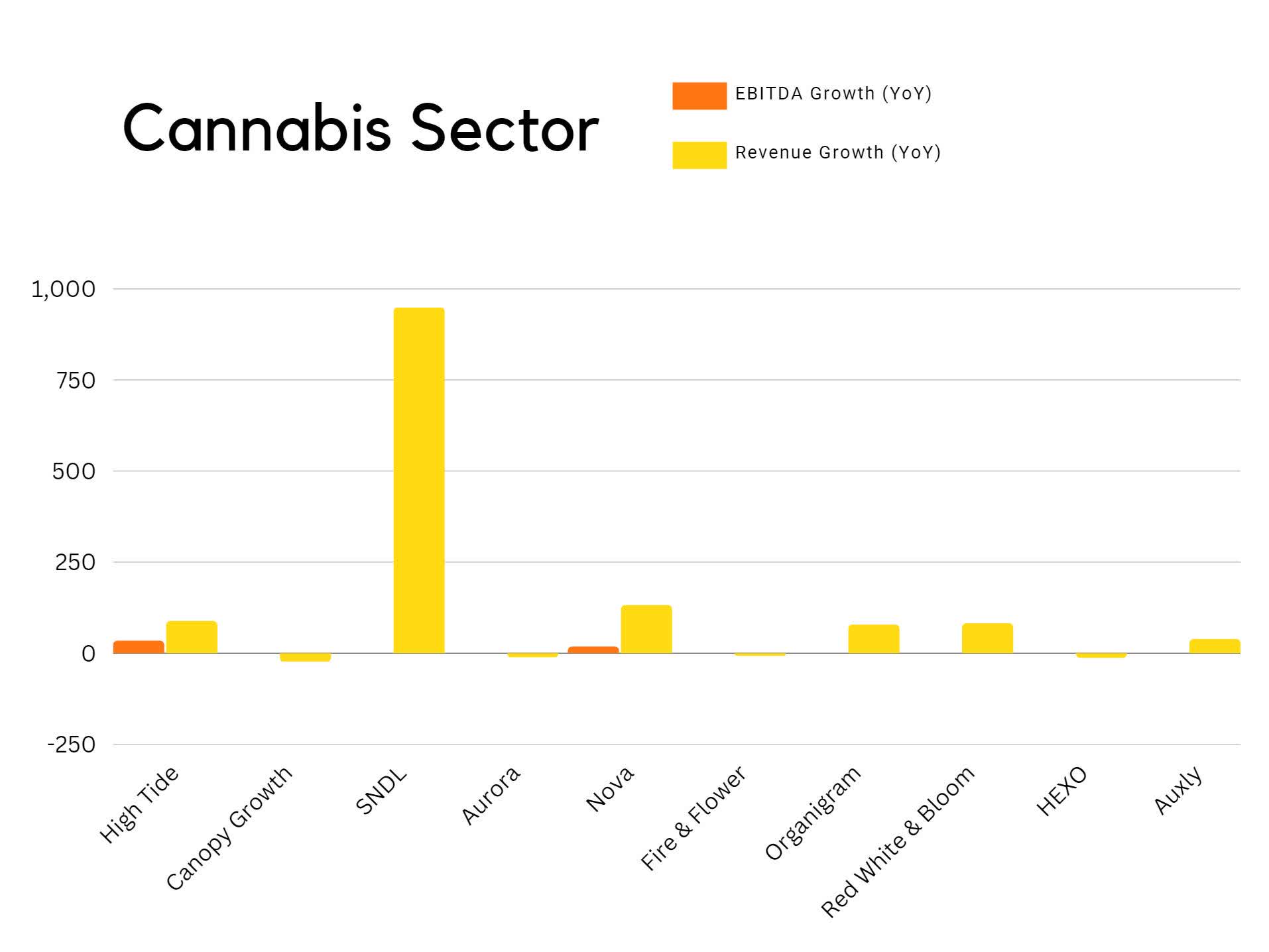

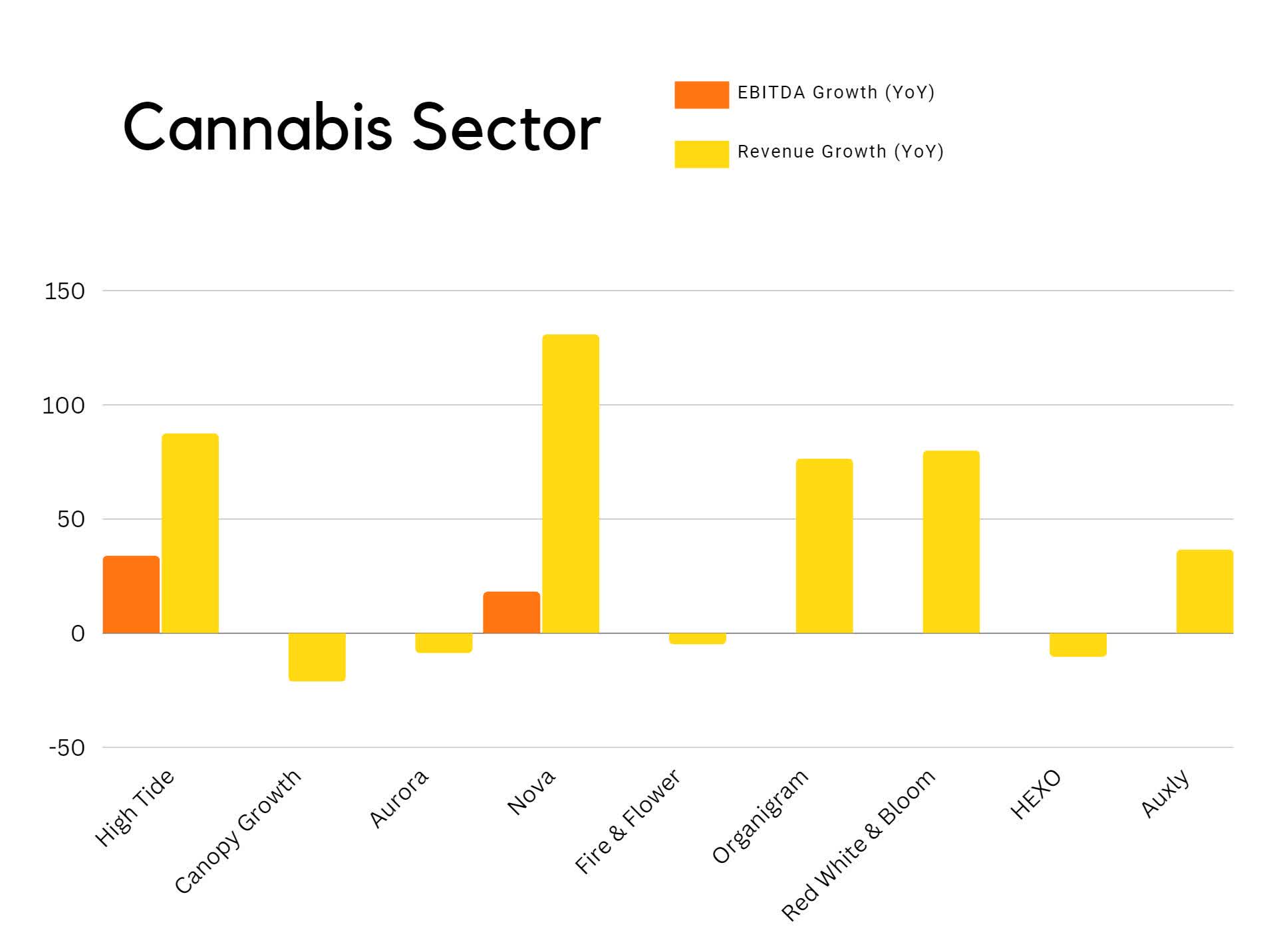

Removing SNDL allows us to look at the rest of the Canadian sector. Five other companies are also growing revenue, but only High Tide ( HITI ) and Nova Cannabis ( NVACF ) have been able to grow EBITDA.

Canadian Cannabis Growth Sans SNDL (Blake Downer)

{kind=link}

Conclusions

As we can see, not all of these companies are created equal. Of the U.S. companies, only three have strong operating margins. And of the Canadian companies, only six of them even have positive gross margins. This means that we have narrowed the list of companies worth watching from 20, down to 9. I should note that the two largest companies Curaleaf ( CURLF ) and Trulieve Cannabis ( TCNNF ) are both not on the list because I don't think their operating margins are strong enough to thrive during the coming price war. The Canadian companies that made the list are already surviving during Canadas price war and so are inherently quite competitive.

Green Thumb Industries ( GTBIF )

Verano Holdings ( VRNOF )

Ascend Wellness Holdings ( AAWH )

High Tide ( HITI )

SNDL Inc. ( SNDL )

Nova Cannabis ( NVACF )

Fire & Flower Holdings (FFLWF)

Organigram Holdings ( OGI )

Red White & Bloom Brands ( RWBYF )

Once rescheduling arrives, I believe a price war will break out in the United States. I expect the U.S. sector will experience sudden margin expansions from the removal of the 280e tax burden, followed by margin contractions once competition drives the price of cannabis down. The Canadian market is already more mature than any of the 50 separate markets that make up the United States. If cannabis is removed from the list of controlled substances entirely, then ultra cheap Canadian cannabis will flood the United States and most of its growers will face bankruptcy.

What am I missing?

When Henry Ford opened his first factory in 1908, Detroit had over 125 car companies; by the 1960's most of them had been driven out of business and we were left with the big three. This article only covers the ten largest companies in each country by revenue. There are companies that are worth watching that were just too small to show up in the top ten. I know from my previous research that MariMed ( MRMD ) and Vext Science ( VEXTF ) are both worth adding to the list. That makes 11; there have to be others. I am inviting you all to point them out in the comments. I don't have hard limits, but I am expecting the list to end up in the 12 to 15 range. I really don't care about market capitalization or cash on hand, we are looking for the companies with the best margins. Once we have a list of operationally viable companies, we can begin looking into their competitiveness by examining their individual edges and moats.

For further details see:

Finding The Long-Term Winners In The Cannabis Sector