FINS - FINS: Discounted Fund Providing Access To A Niche Market

Summary

- FINS invests in investment-grade bank debt with the majority of its portfolio.

- However, these are in community banks or small-cap non-bank financials, a niche area of the market.

- The fund carries a deep discount and could potentially be of interest to some investors.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on February 15th, 2023.

Angel Oak Financial Strategies Income Term Trust ( FINS ) provides investors with a unique portfolio of mostly investment-grade debt. The portfolio is heavily focused on community bank debt, a niche area of the market. However, they also contain small-cap non-bank financial exposure.

One such surprising position that I didn't expect to see is Trinity Capital Inc. ( TRIN ) listed. This is a venture-focused business development company or BDC. However, this isn't the equity position they are holding, but the Trinity Capital 7% 1/16/2025 ( TRINL ) notes position.

It has been quite some time since I've looked at FINS, but this seems to be consistent with some changes they implemented in late 2021. Simultaneously, they conducted a rights offering and broadened their investment mandate.

In addition, the Board has also approved the expansion of the Fund’s investment mandate to seek to allow for a more diversified portfolio across the U.S. financial sector, including non-bank financial institutions such as insurance companies, asset managers, real estate investment trusts and business development companies. The expanded investment strategy could minimize risk and volatility, increase diversification, offer noncorrelated income, and provide excess yield on a risk-adjusted basis.

Some other interesting exposure is the common equity of mREITs. However, they are in a fairly benign allocation; it helps drive home the point that they are more flexible in going into these types of investments.

Another change that happened to the fund was in 2022 . They merged Angel Oak Dynamic Financial Strategies Income Term Trust (DYFN) into FINS. This made FINS a larger fund, but both funds were fairly small, so now we are at a more reasonable level.

The fund's discount is currently quite attractive for this interesting fund. It could be presenting an interesting time for investors to consider this fund.

The Basics

- 1-Year Z-score: 0.04

- Discount: 10.80%

- Distribution Yield: 8.74%

- Expense Ratio: 2.15%

- Leverage: 32.72%

- Managed Assets: $522.5 million

- Structure: Term (anticipated liquidation date May 31st, 2031)

FINS's investment objective is "current income with a secondary objective of total return." To achieve this, they will invest in "a banking sector debt-centric strategy, which exhibits low historical correlations to other areas of the market."

Some investment highlights include "access to a niche market segment" and "focus on high-quality credit with at least 50% of the fund's portfolio is publicly rated investment grade or, if unrated, judged to be of investment grade quality by Angel Oak." Additional highlights include; "asset class duration historically uncorrelated to interest rates" and "benefits from Angel Oak's extensive resources and expertise in actively managing community bank debt investments."

The fund's expense ratio is one of the highest I've ever seen. While the portfolio is more niche and can take a fair bit of additional resources, this seems excessive. The advisory fee comes to 1.35%. This will make it difficult to perform well, but not impossible. When including leverage expenses, it comes up to 3.37%.

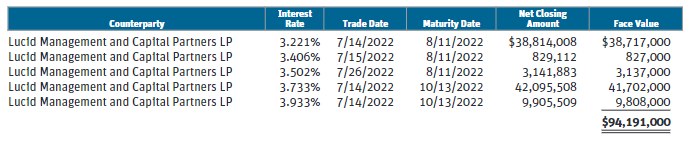

The leverage they employ is reverse repurchase agreements. These are short-term and are interest rate sensitive. As interest rates have been increasing, these costs have been rising rapidly. While these have matured already, it gives us an idea of the sorts of terms we saw through this period.

{kind=link}

FINS Reverse Repurchase Agreements (Angel Oak)

In addition to these, they have senior notes that they've issued. This was through a Series A and B. These offer fixed-rate financing, so some of the leverage for this fund is less susceptible to rising rates. These have fairly long maturity dates out to 2026 and 2028 as well.

{kind=link}

FINS Notes Leverage (Angel Oak)

The fund is a term fund anticipated to liquidate on May 31st, 2031. However, they've already attempted to extend this termination date to 2035, but it was shot down. I'd look at more attempts in the future if they are already trying to extend it so soon.

Lastly, shareholders were asked to approve the amendment of the Fund’s Declaration of Trust to extend the termination date of the Fund from May 31, 2031, to June 30, 2035, which subsequently did not receive affirmative vote based on the following results:

FINS Termination Date Extension Vote Summary (Angel Oak)

Performance - Attractive Discount

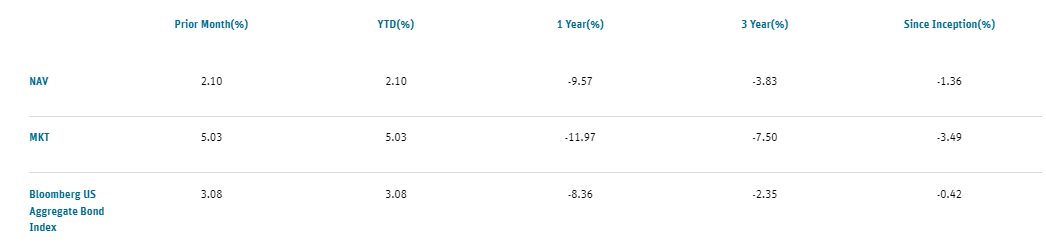

The fund's performance has been quite lackluster since the launch. That being said, it wasn't too far away from what the benchmark bond index is showing, either. Being a leveraged fund, we saw slightly worse results at a time when the benchmark was down isn't going to be anything shocking.

{kind=link}

FINS Annualized Returns (Angel Oak)

If they didn't have that wild expense ratio, results could have even been positive since inception. But I digress.

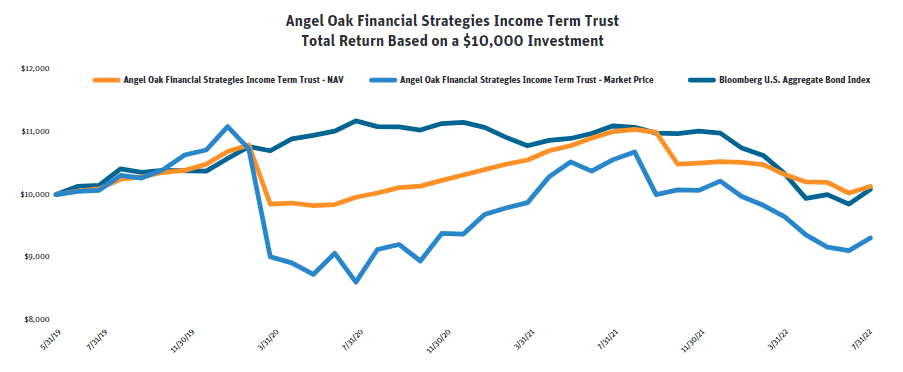

To visualize the fund's performance, the actual underlying portfolio would have resulted in a similar ending value as the Bloomberg U.S. Aggregate Bond Index. It would have ended in sizeable lagging results on the market price basis alone.

{kind=link}

FINS Growth of $10K (Angel Oak)

One thing that an index can't offer (besides being able to invest in it directly anyway) would be a discount. With FINS, the market results underperformed the NAV results over the more extended periods. That tells us that the fund has moved to a discount since launch. In fact, the fund's discount is now trading well below its average since the fund's inception.

Albeit, the fund isn't that old and trying to find a range in the last few years is fairly difficult. We've experienced some of the most extreme valuation changes between 2020 and 2021. 2022 wasn't any more 'normal' of a year being a bear market for equities and most asset classes showing deep losses.

Ycharts

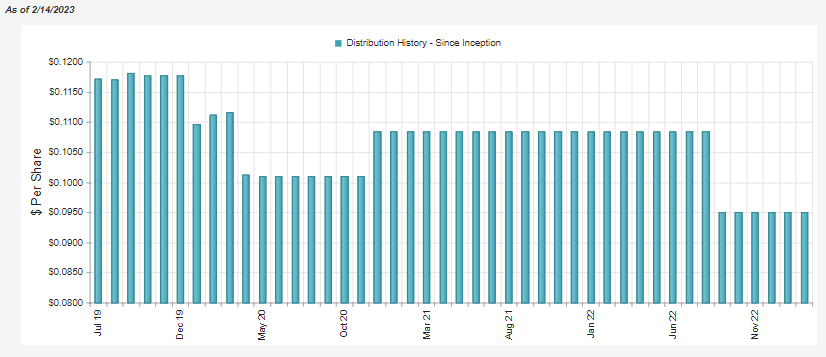

Distribution - 2022 Cut Due To Lack Of Coverage

With the fund absorbing DYFN, the fund's net investment income received a bump on an absolute basis. However, the fund still cut the distribution in 2022. It isn't uncommon for fixed-income funds to adjust their distributions over time as needed. With all the changes implemented for FINS and the merger, it's even harder to get a clear picture of a trend.

{kind=link}

FINS Distribution History (CEFConnect)

In the latest semi-annual report - admittedly a bit dated at this point - we can see that NII coverage came to only 59%. The next annual report isn't expected until early April. With that being said, on a per-share basis, it can help balance out what we are seeing. That cuts through the two mergers, investment policy mandate change and rights offerings we've seen.

{kind=link}

FINS Semi-Annual Report (Angel Oak)

Given that interest rates have been rising, we know their reverse repurchase agreements are costing them more. On the other hand, looking through the list of their holdings, we can see that a meaningful amount is floating rate debt obligations.

That means as interest rates rise, they should also receive higher income generation on these fixed-income positions. We started to see that be the case with the NII of $0.38 because if that were annualized, it would have exceeded last year's $0.73. Since then, rates have only been increasing further, so we could see NII per-share rise for the full year to a larger degree.

However, since coverage was so light, it seems quite clear why the distribution was cut. Even with rising rates, the distribution wouldn't appear to be covered. When they cut the distribution, they stated , "The Fund seeks to pay a distribution at a rate that reflects net investment income actually earned."

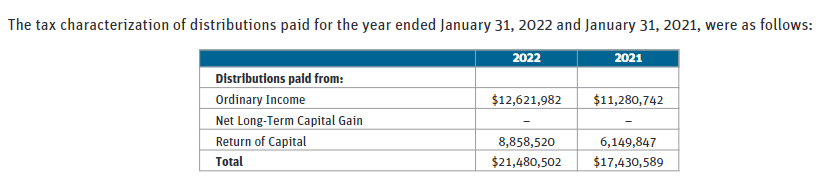

With return of capital classifications in the distribution and the coverage we are seeing, all signs pointed to not achieving that result. In fact, it could indicate further cuts would be needed if NII doesn't rise further.

{kind=link}

FINS Distribution Tax Classification (Angel Oak)

FINS's Portfolio

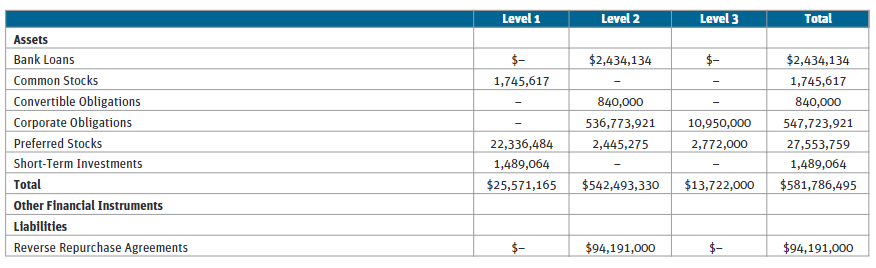

The portfolio regularly contains some exposure to level 3 securities. However, the bulk of the portfolio is listed as level 2. Generally speaking, if there were a large amount of level 3 securities - which are harder to value - a fund can trade at a large discount due to that. In this case, I don't think the amount here should be too much of a detriment. This was the portfolio breakdown at the end of July 31st, 2022, to give us an idea of how their portfolio can be positioned.

{kind=link}

FINS Security Level Breakdown (Angel Oak)

With quite a low turnover, the portfolio doesn't shift often. In the last report, they noted a turnover of 2.81%. In the prior full fiscal year, it was 13.82%. For fiscal 2021, they were a bit more active, but even then, it only came to 24.55%. Therefore, we shouldn't anticipate significant changes in the fund from update to update.

Bank debt is still the largest allocation to the fund. As mentioned at the open, they've shifted their portfolio a bit to include some other non-bank financial exposure. Some of the holdings include equity positions in mREITs and debt obligations of other investment companies. The breakdown listed here is as of December 31st, 2022 .

FINS Sector Breakdown (Angel Oak)

The credit quality of the portfolio is where the fund shines. Most CEFs invest in a lot of junk, not FINS. The majority of their portfolio is invested in investment-grade quality debt. They mentioned that unrated debt is only included if they feel that it would otherwise qualify as investment-grade. For the most part, that means no or very limited junk in this fund. I'd leave the door open with the word "limited" because it's at Angel Oak management's discretion to consider it investment-grade on the unrated portion. That can make it more interest rate sensitive, as it generally means longer maturities and lower yields.

FINS Credit Quality (Angel Oak)

When looking at the top holdings, they represent a fairly large weighting in the fund. Concentrating positions near the top means less diversity throughout the fund, but if you are investing in investment grade, that could be less of a concern.

FINS Top Ten Exposures (Angel Oak)

The latest list of their entire holdings only shows their October 31st, 2022 holdings. Within that, we can see greater details on their underlying holdings, such as the yields and whether they are floating. Keeping in mind that some of these are fixed-to-float and may be in the fixed portion of their life, which means we aren't seeing the benefits of rising rates yet. Additionally, it lists the maturity of each of their holdings as well.

Conclusion

FINS is trading at quite an attractive discount. The fund offers a niche investment portfolio for investors looking for community banking debt exposure. However, they've now been able to diversify their portfolio in non-bank financial positions further over the last year and a half. A meaningful portion of their portfolio is floating or fixed-to-float. That should bode well if rates continue to rise as a natural hedge.

Besides the reverse repurchase agreements, which are short-term financial instruments, the fund has employed leverage through fixed-rate notes. Those aren't going to be subject to the negatives of rising rates, putting them in a position that helps them benefit even more from increased interest rates. That being said, it wasn't enough to maintain their distribution. If they are looking for a sustainable distribution that's based on income only, they may have more cuts to go.

For further details see:

FINS: Discounted Fund Providing Access To A Niche Market