FINV - FinVolution: Chinese Fintech With Huge AI Tailwinds

2023-03-20 17:52:47 ET

Summary

- FinVolution is a thriving fintech company which is poised to benefit from the growth in China's middle class population and strong economy.

- The company grew its total transaction volume by 25% year over year to $7 billion (RMB 48.6B).

- The business produced an outstanding loan recovery rate of approximately 90% in Q4,22 and it's increasingly focusing on higher quality borrowers.

- FinVolution has hiked its forward dividend yield to 5.75% which is incredible, especially for a technology company.

- CEO Feng Zhang has decided to step down after eight years, and President and Vice Chairman Tiezheng Li has been appointed the new CEO.

FinVolution ( FINV ) is a rapidly-growing fintech company based in China. The company operates a peer-to-peer lending platform that brings together ~75 financial institutions with ~24 million Chinese consumers. An economic forecast by Fitch has recently revised China's growth rate to 5% for 2023, up from 4.1% prior. Given many western economies are forecast to have a 99% chance of entering a recession in 2023, diversification internationally looks to make sense. In addition, Finvolution is founder led, with an experienced team of former Microsoft (MSFT) and Baidu (BIDU) executives. In this post, I'm going to break down the company's AI-powered business model, its fourth-quarter financials, and valuation.

AI-Powered Business Model

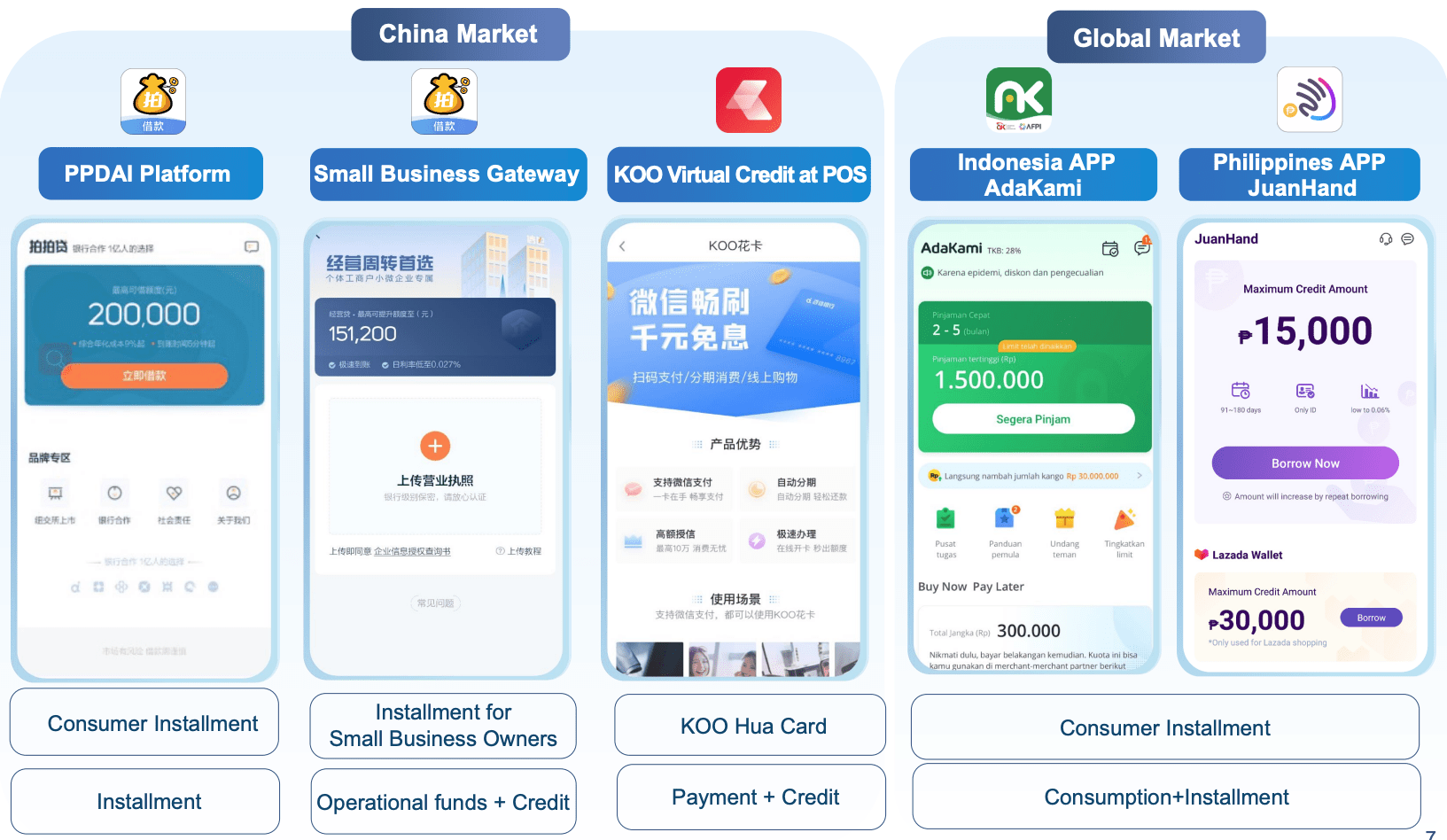

FinVolution's business model focuses on helping to financially empower underserved markets through its five main applications. The first is its PPDAI platform which is a popular peer-to-peer (P2P) lending platform. Its second product is a small business gateway that provides working capital and loans. The SMB market is known to be "underserved" by many traditional financial institutions and thus the gap for technology players is substantial. For example, over in the west Square Capital (owned by Block ) provides loans to SMBs and tracks the business transaction data in order to improve its underwriting.

{kind=link}

Finvolution (Investor presentation)

Its third product is KOO Virtual Credit, which enables consumers to access easy credit for purchases with flexible repayment options. I think of this as similar to a "buy now pay later" - BNPL - service which is a hot market with many large players such as Affirm( AFRM ) and Afterpay acquired by Block for a staggering $13.9 billion in early 2022. However, these operators do not run a service in China and thus this leaves a huge gap in the market for local players such as FinVolution. In fact, one forecast predicts the BNPL market in China to grow at a 37.2% compounded annual growth rate and be worth ~$354 billion by 2028. FinVolution also is rolling out similar solutions to its core China-based lending apps, internationally. This includes JuanHand which offers loans within 24 hours in the Philippines, in addition to its AdaKami app which operates in Indonesia. FinVolution has recently (Jan 2023) scored a strategic cooperation with Permata Bank, one of the top 10 largest banks in Indonesia by asset number.

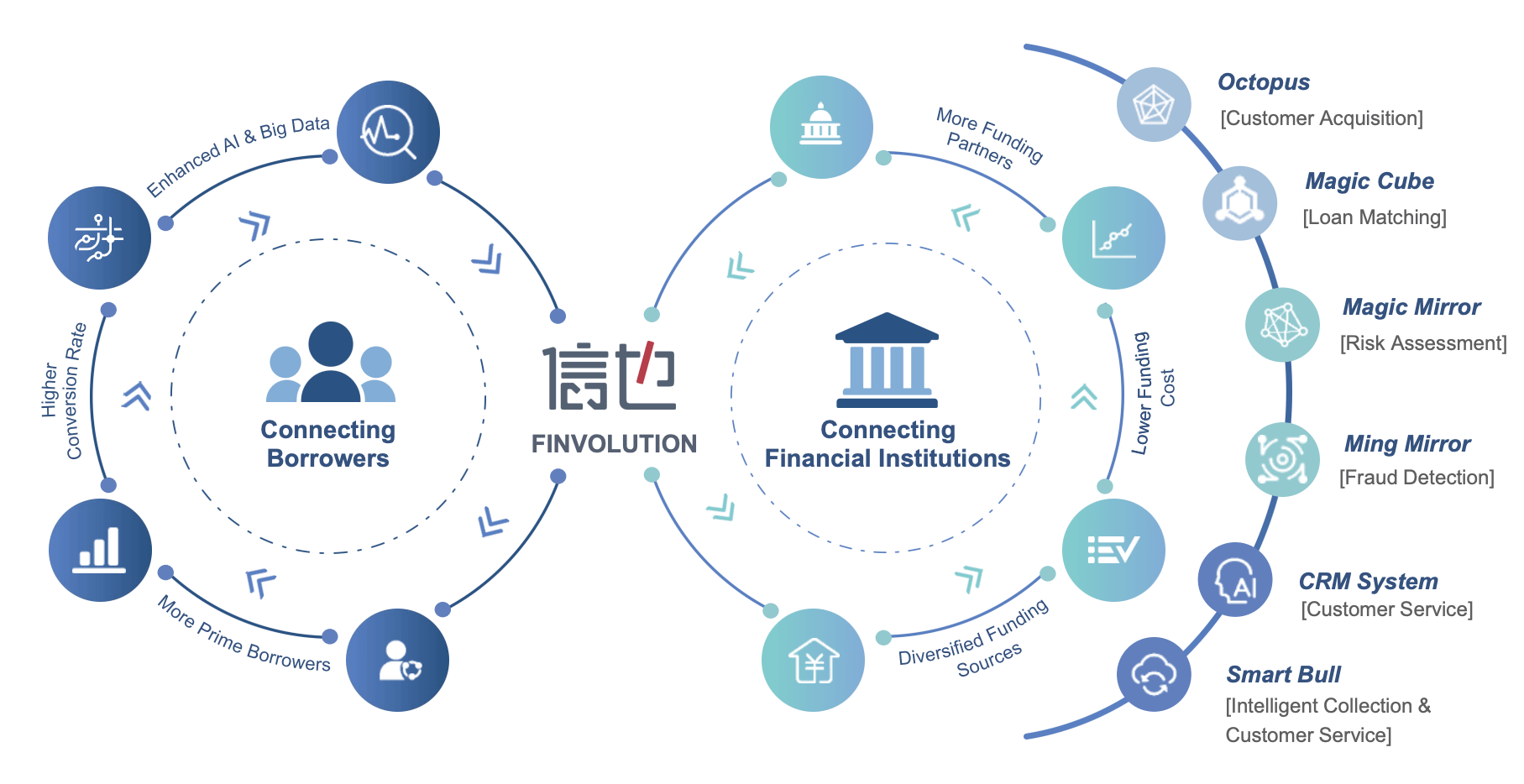

Overall FinVolution connects borrowers to financial institutions and uses a vast plethora of advanced AI-powered technology to achieve this. This includes a customer acquisition platform (Octopus), a loan matching service (Magic cube), a risk assessment tool (Magic Mirro), and many more. FinVolution even uses AI to improve the collection service (Smart Bull). All these services help to provide a more valuable service for financial institutions while also being much more efficient (and often accurate) than a pure human-based system.

{kind=link}

business model (Finvolution)

Fourth Quarter Financial Results

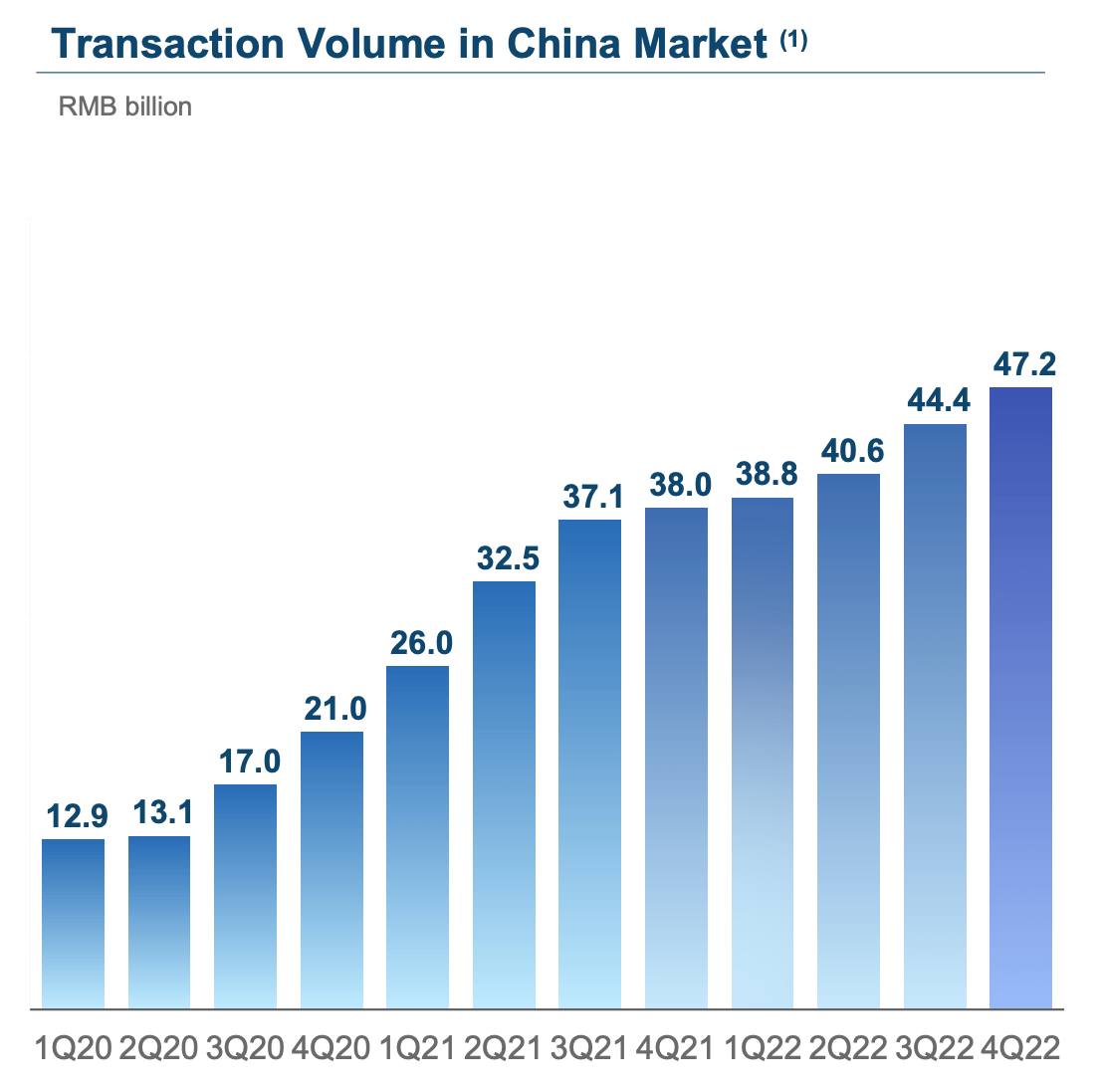

FinVolution reported strong financial results for the fourth quarter of 2022. Its total transaction volume was $7 billion (RMB 48.6B), which rose by a rapid 25% year over year and it was even up 7% sequentially. On a full-year basis, the results were even better, with total transaction volume of $25 billion (RMB 175B), which increased by a rapid 28% year over year. This was a fantastic result especially given the uncertain macroeconomic environment and even the hard lockdowns which have still been occurring across China. As you may have guessed the vast majority (97%) of its volume was in China with ~$6.8 billion (RMB 47.2B) in Q4,22. Its operating revenue rose by 24.6% year over year to $435 million (RMB 3B), which was strong.

{kind=link}

Transaction Volume in China (Q4,22 report)

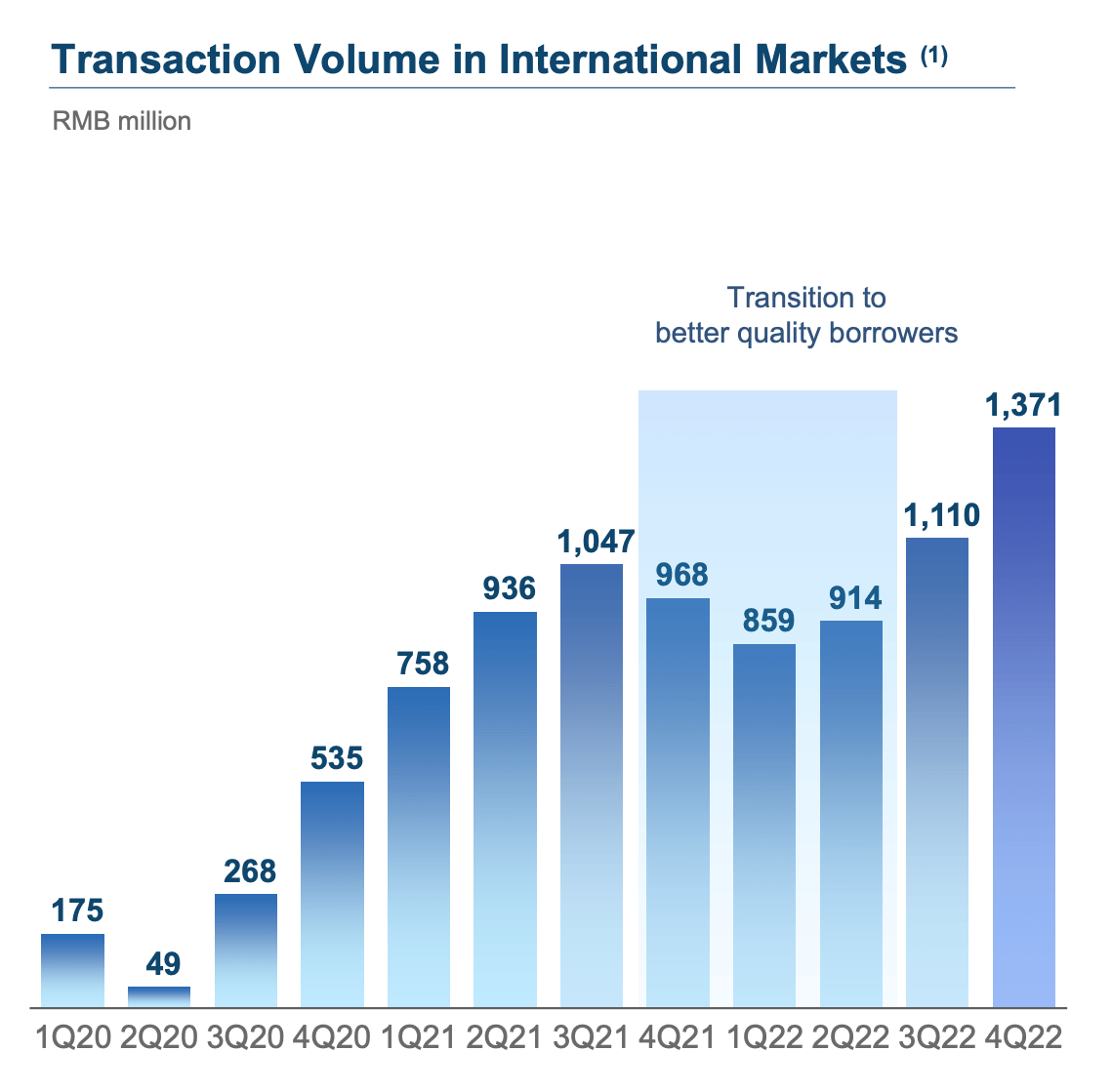

As mentioned prior, a core part of FinVolution's growth strategy is to expand internationally, especially in emerging and growing markets such as Indonesia and the Philippines. So far its growth strategy has been working well with ~36% increase in international transaction volume to $199 million (1.37B RMB). This was a positive result given the company was still honing its ideal cohort via a "transition" to higher-quality borrowers throughout 2022. FinVolution has gradually increased its partnerships with local banks, including Bank Jago, OCBC NISP, and the aforementioned Bank Permata. The result of this has been an increase of the proportion of loans funded by local banks to 63% in Q4,22, up from 48% in the prior quarter and just 10% in the equivalent quarter last year. This is a fantastic result as it effectively means a lower cost of capital and lower friction for its consumers.

{kind=link}

Transaction volume in International markets (Finvolution)

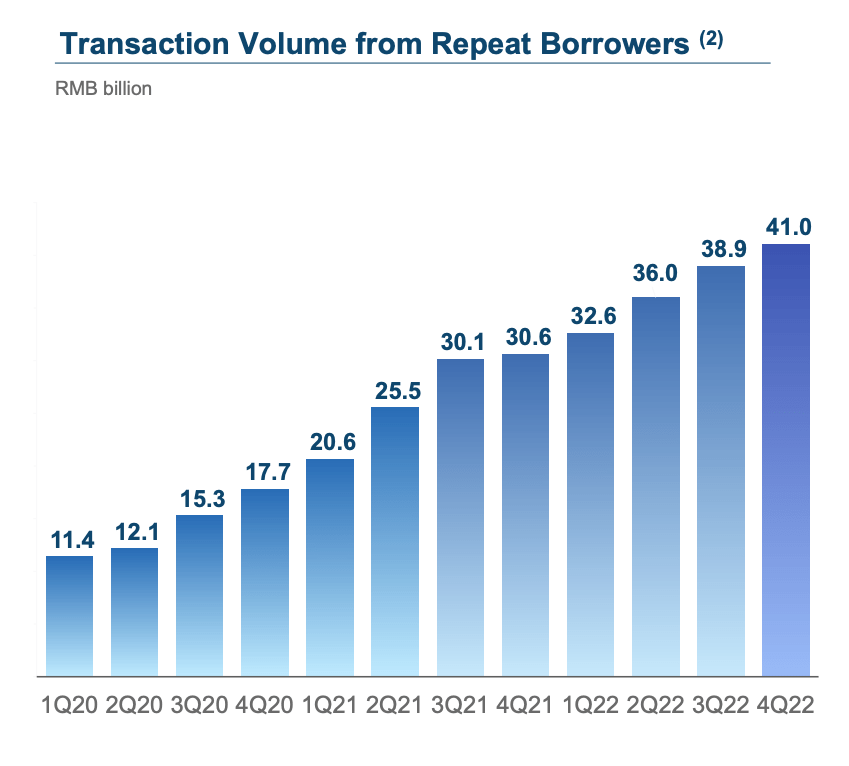

Another interesting metric to analyze is the transaction volume from repeat borrowers. In this case, 84% or (RMB 41B) of its transaction volume is from repeat borrowers. This is a fantastic sign as it means consumers are finding value in its products and returning. Therefore this should help to reduce the overall customer acquisition costs and increase the lifetime value of the customer. The end result should be an improvement in margins as operating leverage becomes apparent. In this case, non-GAAP operating income was $92.5 million (RMB 638m), which increased by 13.8% year over year.

{kind=link}

Transaction Volume from repeat borrowers (Q4,22 report)

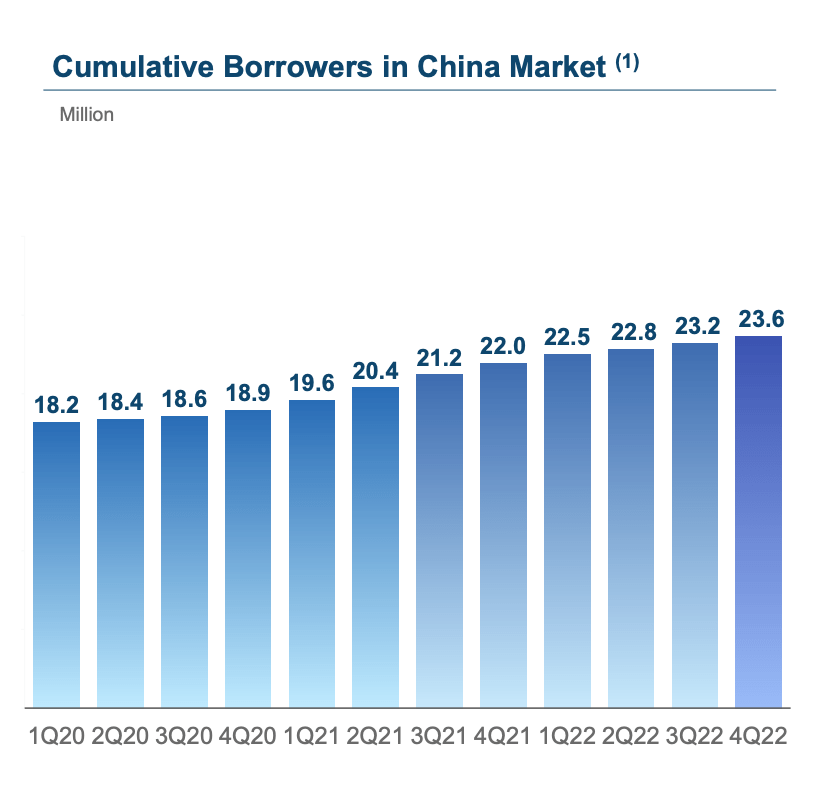

Back to the China market, FinVolution has continued to increase its overall borrowers to a staggering 23.6 million people. This is a positive achievement given the company also increased the "quality" of its borrowers from 63% in Q4,21 to 77% category A borrowers by Q4,22. This improvement in the quality of borrowers has helped to reduce its funding costs to just below 7% in Q4,22 down from 7.8% in Q4,21. In addition, FinVolution has maintained a healthy delinquency rate of between 2.3% and 2.4%, which is fairly standard (but good) for the industry from my experience in working with lenders, who are usually giving loans to standard borrowers. This is all while maintaining a solid borrowing rate of 23%, which fits with the company's "financial inclusion" philosophy. Its outstanding loan finance has also increased by 28% year over year to $9.4 billion (RMB 64.6 billion).

{kind=link}

Cumulative borrowers China Market (Q4,22 report)

The company has a solid balance sheet with $527 million in cash and cash equivalents and $497 million in short-term investments. Its debt levels looks to be minimal at ~$26 million, although the data is scarce on this metric.

Valuation and Forecasts

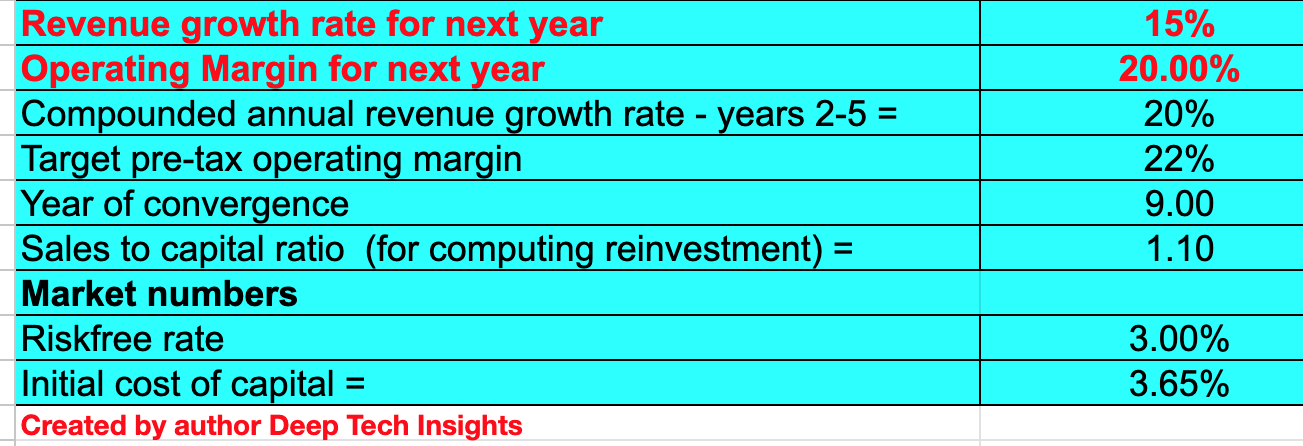

In order to value FinVolution I have plugged its latest financial data into my discounted cash flow valuation model. I have forecast 15% revenue growth for "next year" or the full year of 2023. This is based upon the midpoint of management's forecast of transaction volume between 10% and 20%, which I have extrapolated down to give a revenue estimate. In years 2 to 5, I have forecast a faster revenue growth rate of 20% per year, which is still less than the 24.6% growth rate achieved in Q4,21. I expect this growth to be driven by strong international revenue growth (as per the current trend). International transaction market revenue is expected to increase by 15% year over year. I also expect growth in its core China market, as many sources indicate the "zero CV19" policy has begun to ease.

{kind=link}

FinVolution stock valuation 1 (created by author Deep Tech Insights)

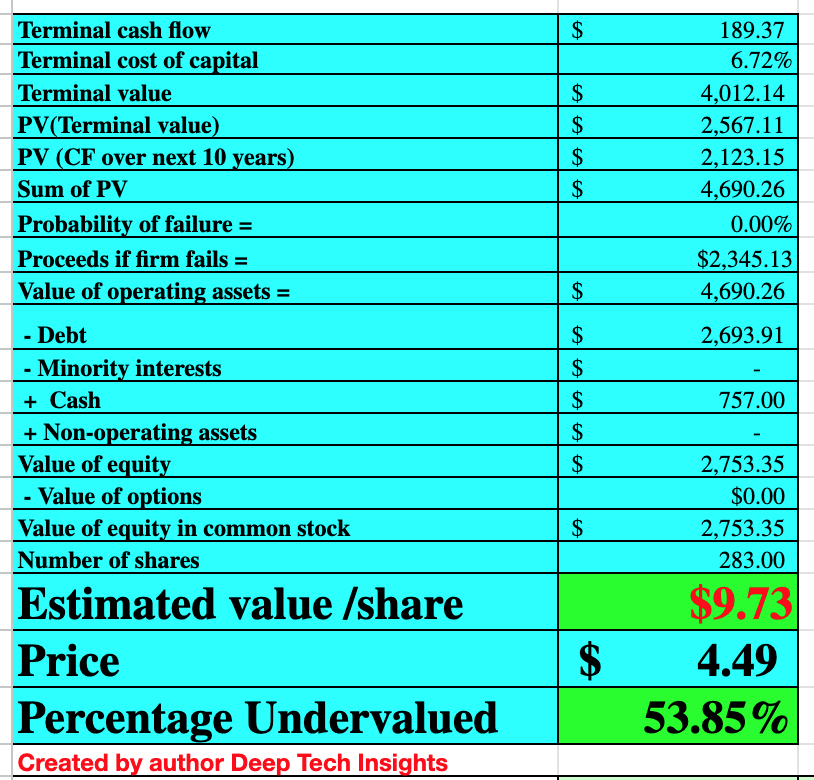

To increase the accuracy of my model, I have capitalized R&D expenses which has boosted net income.

{kind=link}

FinVolution stock valuation 2 (created by author Deep Tech Insights)

Given these factors I get a fair value of $9.73 per share, the stock is trading at $4.49 per share at the time of writing and thus is ~54% undervalued, according to my forecasts and model.

The stock also trades at a price-to-earnings ratio = 3.78, which is extremely cheap and over 56% cheaper than the financial services sector average. On the below chart, you can also see the stock trades at a cheaper valuation than most industry peers.

Risks

Recession/loan defaults/China Risk

Many western economies have had recessions forecast for 2023. This may have a knock-on effect on China, as the country gains a large portion of its GDP from exports. Lower consumer default or job losses could result in higher default rates for its loans. There's also the "country risk" which comes with investing into all Chinese stocks. Many of these stocks trade as an ADR or American Depository Receipt on U.S. exchanges. In addition, the SEC has previously threatened to delist Chinese stocks from U.S exchanges that don't comply with auditing.

Citi has also recently downgraded the company to Neutral from a Buy. It has also lowered the price target to $5.08 from $5.68 previously. A positive is this is still substantially higher than the 3.74 per share, at the time of writing.

Final Thoughts

FinVolution is an innovative fintech company that has embedded AI into every part of its platforms. But this is not an "AI hype" stock, the company uses its technology to generate solid metrics. Given the growing middle- class population in China and its strong economy, FinVolution looks to be the ideal company to benefit. Given my valuation model and forecasts indicates the stock is undervalued intrinsically at the time of writing it looks to be a great opportunity.

For further details see:

FinVolution: Chinese Fintech With Huge AI Tailwinds