WPC - Fire Sale: 2 Cheap REITs To Buy 1 To Sell

2023-10-09 10:35:00 ET

Summary

- REITs have been underperforming in 2023 due to higher interest rates and alternative investment options.

- Long-term investors may find discounted valuations in high-quality REITs as the rate hike cycle nears its end.

- REITs are under pressure with many trading at cheap valuations, but some REITs are simply cheap for a reason.

When it comes to REITs, it is no secret that the sector as a whole has been one of the worst performers in 2023. The reason is largely due to higher interest rates which provide a lot of alternative options for investors looking for yield.

Although rates are expected to remain higher for longer according to Fed Chairman Jerome Powell, the REIT sector could remain a weak performer, at least in the near term.

However, for those of you who are long-term investors with a time horizon of more than five years, this could be a great opportunity to add high-quality REITs to your portfolio at extremely discounted valuations. After all, the rate hike cycle, although could remain at an elevated level, the hiking part is largely done, maybe one or two hikes remain at most.

Given that, we will discuss three high-quality REITs that are trading at extremely discounted valuations.

2 Cheap REITs I Am Buying

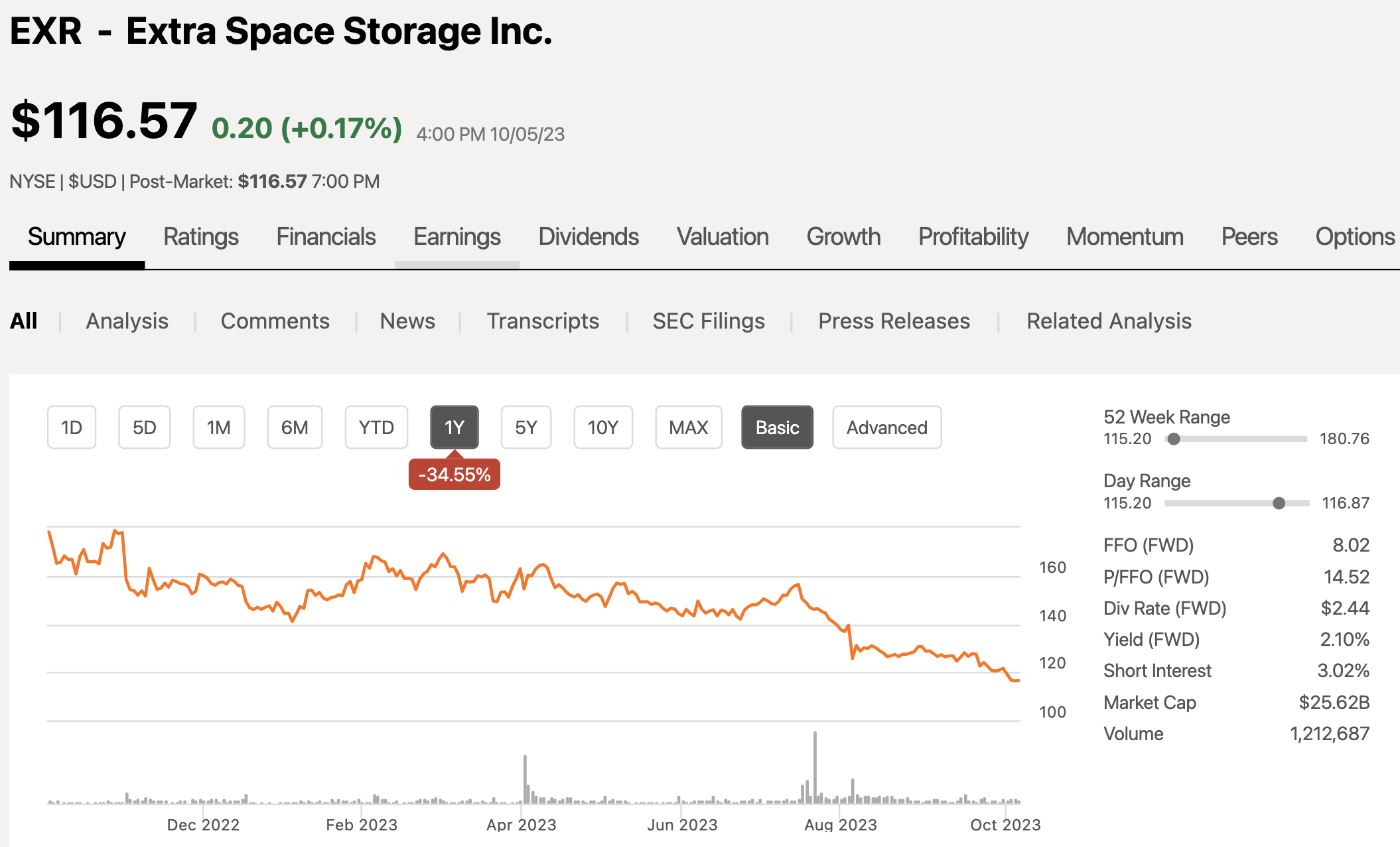

REIT #1 - Extra Space Storage ( EXR )

Extra Space Storage is the second largest self-storage REIT behind Public Storage ( PSA ) with a market cap of $26 billion and over the past 12 months, the stock is down 35%.

{kind=link}

If there is one thing that holds through regardless of the economic backdrop, it's the fact that Americans hate to get rid of things, which benefits the self-storage industry.

When it comes to self-storage exposure, there are really three main REIT options:

- Public Storage

- Extra Space

- CubeSmart ( CUBE )

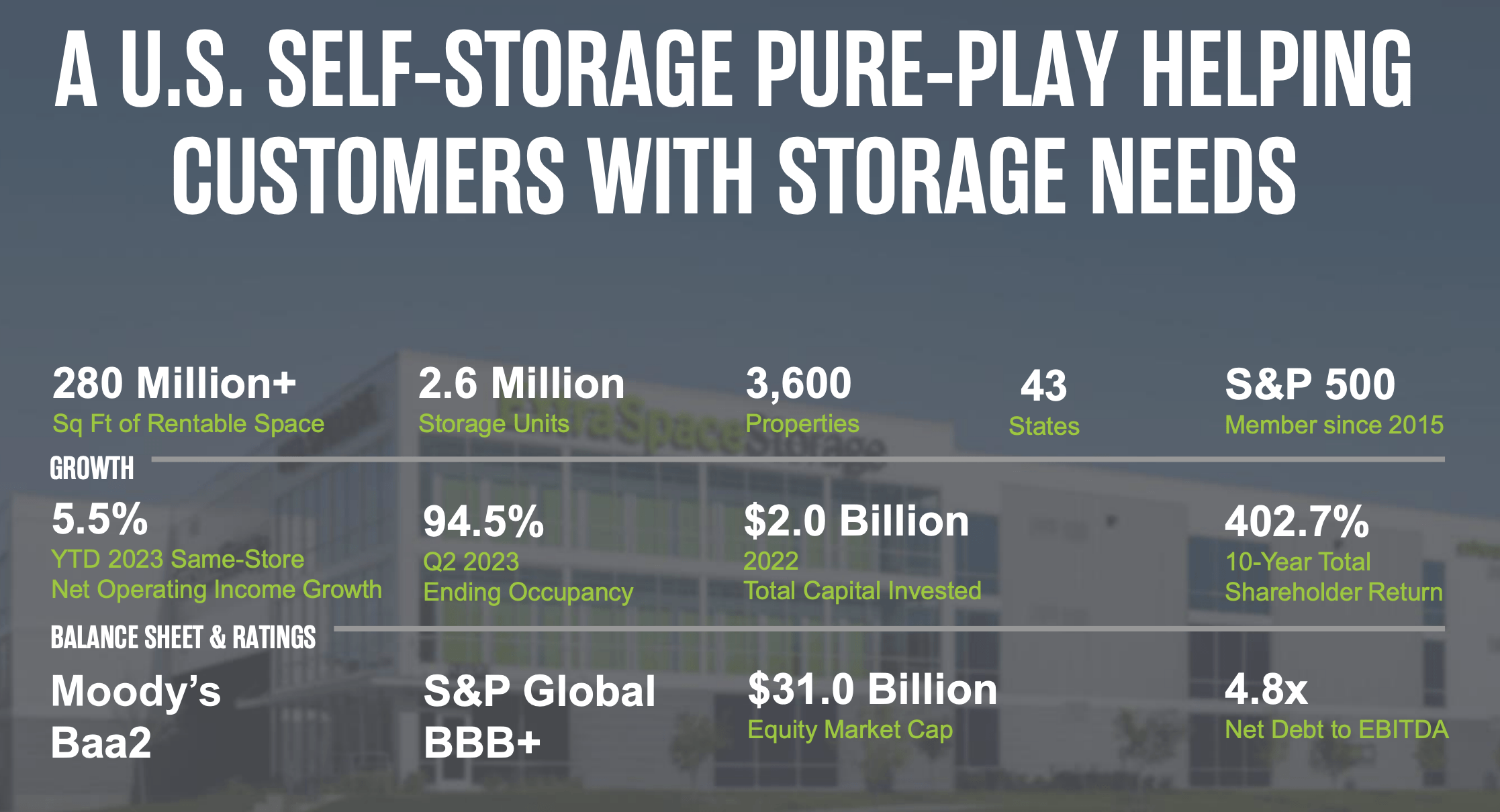

Here is a closer look at Extra Space Storage:

{kind=link}

The company has roughly 2.6 million storage units that are throughout 3,600 properties within 43 states in the US. As of the end of Q2, the company had an occupancy rate of 94.5%.

The REIT is well capitalized with a solid BBB+ credit rating and a net debt to EBITDA ratio of 4.8x.

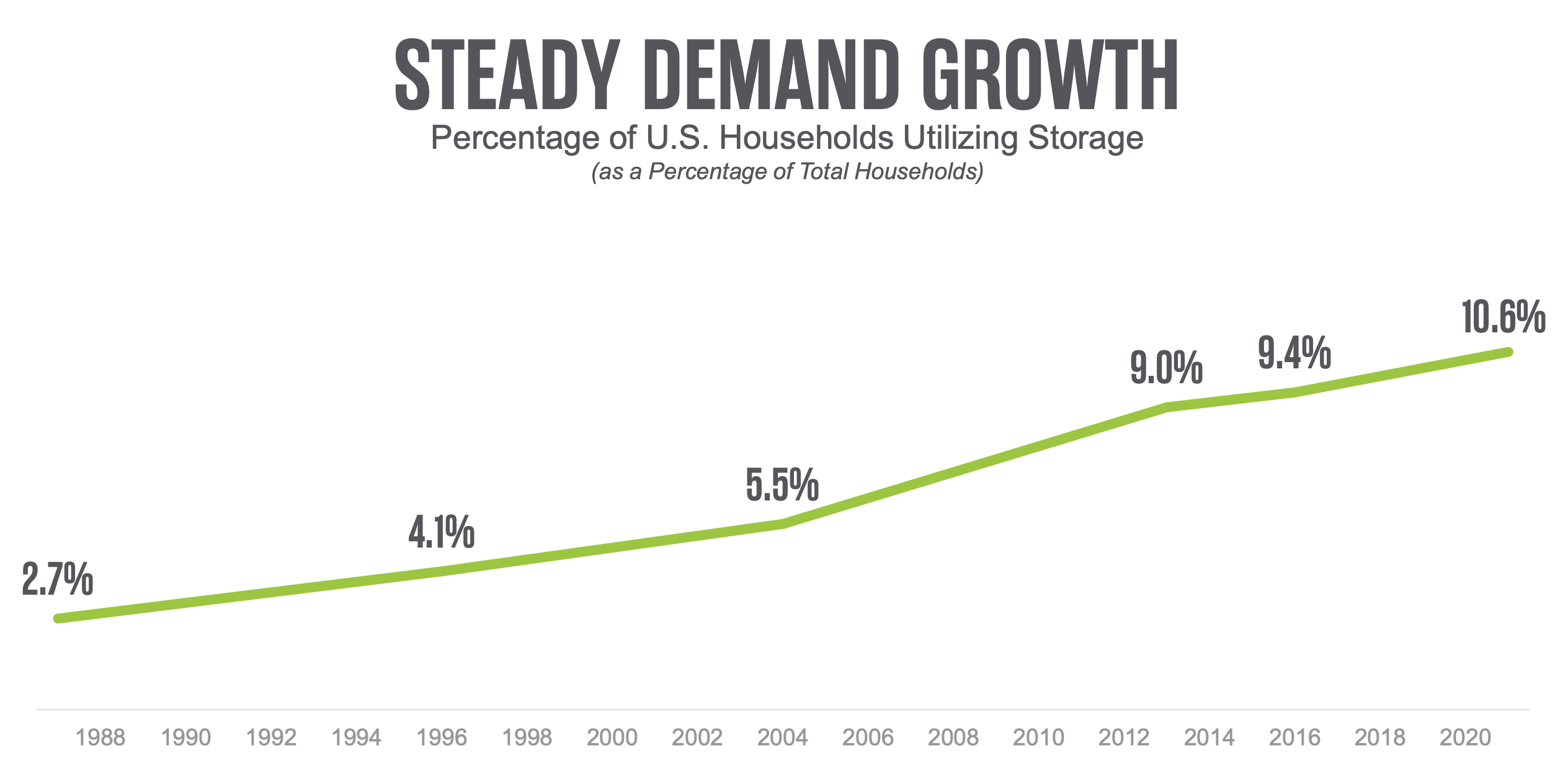

Since 1988, you can see the growth in the popularity of self-storage as the percentage of US households utilizing storage has grown from just 2.7% to nearly 11% today.

{kind=link}

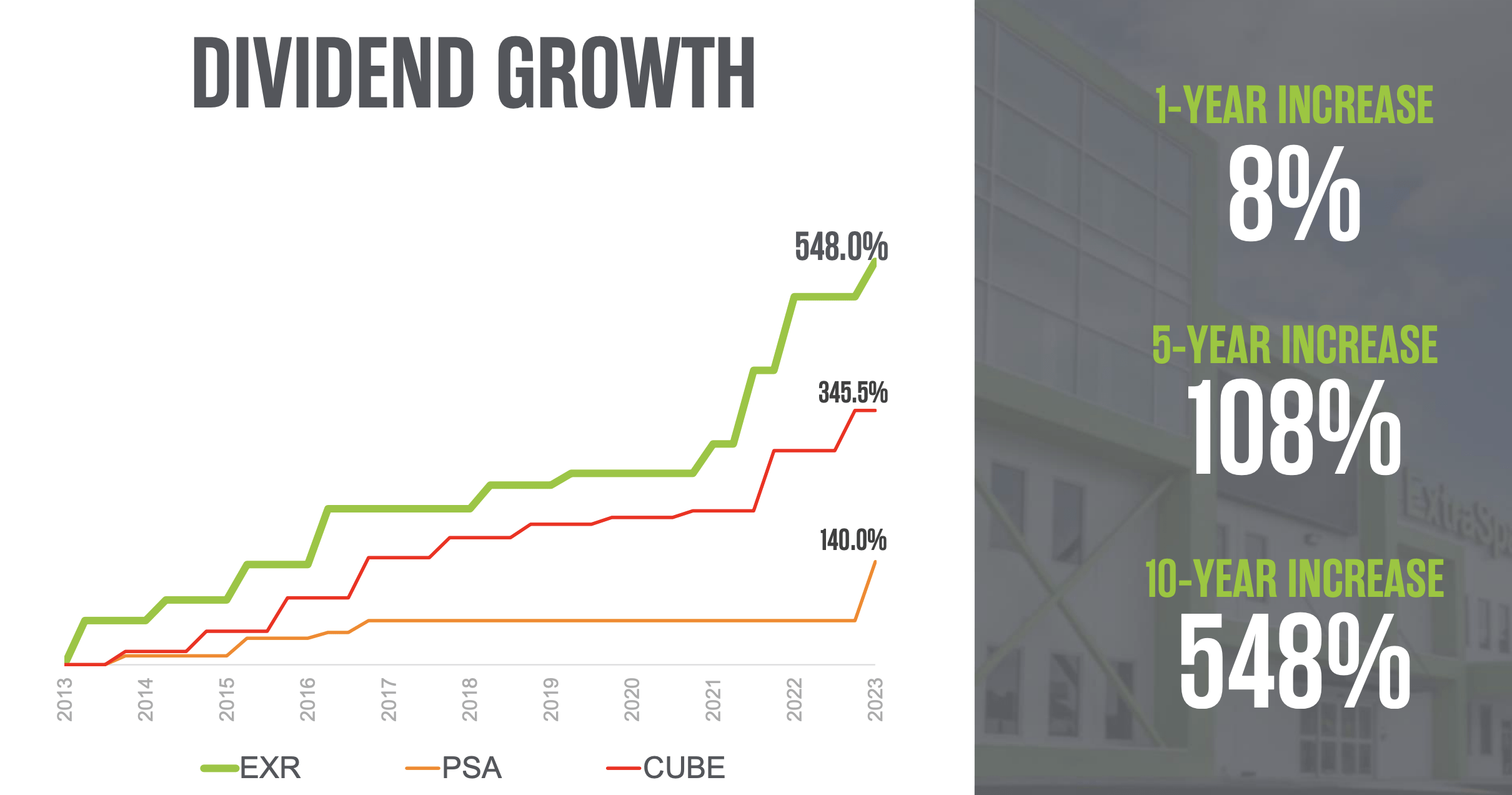

Not only has the demand for storage grown over the years, but so has the dividend. EXR has grown its dividend a total of 548% over the past 10 years, which is more than its two closest competitors combined. In the past year, the dividend for EXR grew 8%. The company has an average five-year dividend growth rate of 14%, making it a rare dividend growth REIT. Shares of EXR currently yield a dividend of 2.1%.

{kind=link}

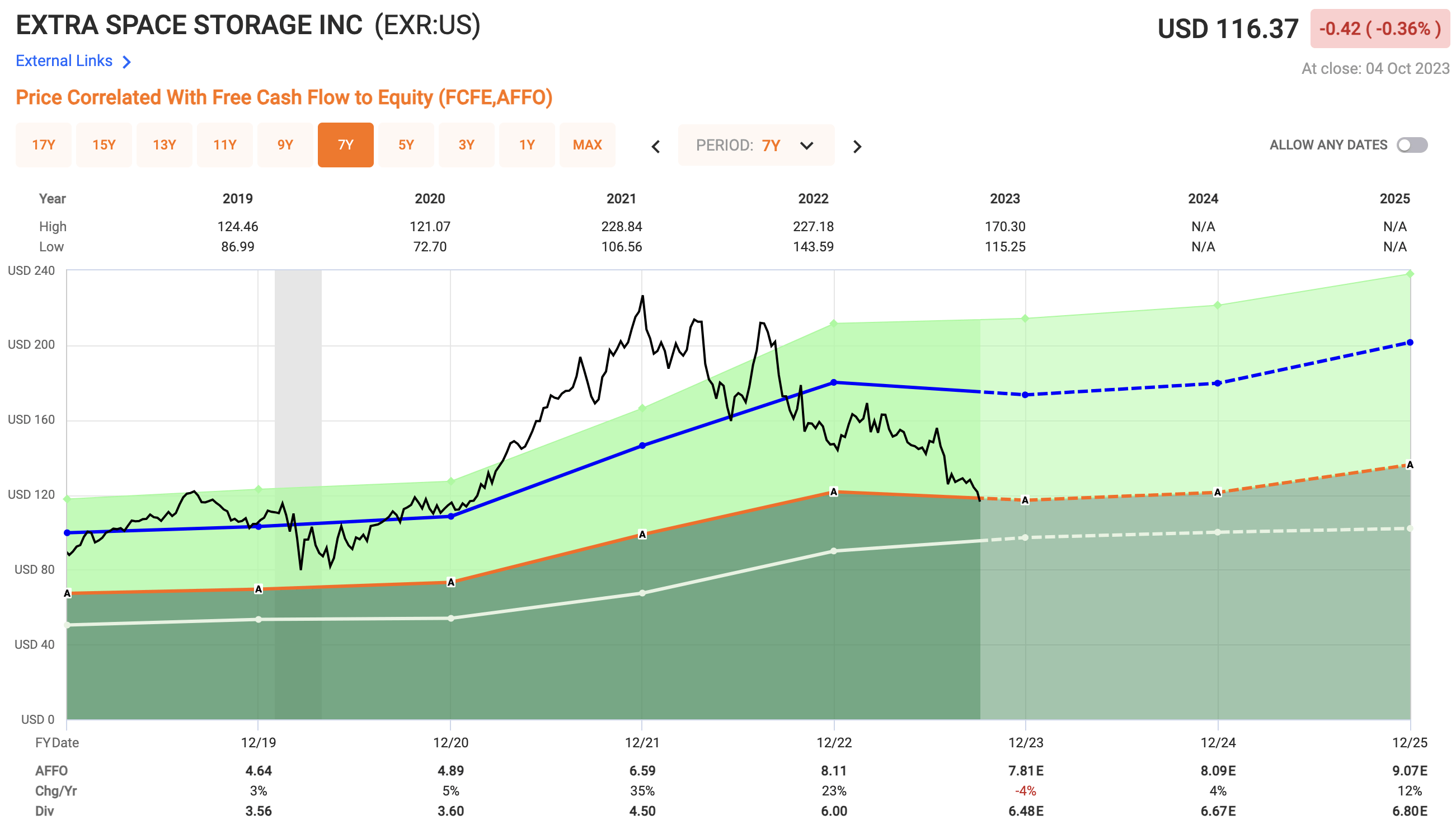

As I mentioned at the start, shares of EXR are down big time over the past 12 months giving long-term investors a HUGE opportunity in this high-quality REIT. Analysts are looking for AFFO growth of 4% in 2024 and 12% in 2025. Using next year's estimates, shares of EXR currently trade at an AFFO multiple of 14.3x, which is well below their five-year average of 22.2x.

{kind=link}

REIT #2 - Equinix, Inc. ( EQIX )

The second REIT operates in one of the best-performing sectors of 2023 which is data centers. With the continued growth in AI expected for many years, there is a huge demand for more data centers.

The hit against data center REITs for the past few years was concerns about the largest technology cloud companies, Microsoft ( MSFT ), Alphabet ( GOOGL ), and the likes of Amazon ( AMZN ), would build their own data centers. Well, the fact of the matter is that all companies are obviously not MSFT, GOOGL, or AMZN and do not have the liquidity to do that, hence the growth in data center REITs.

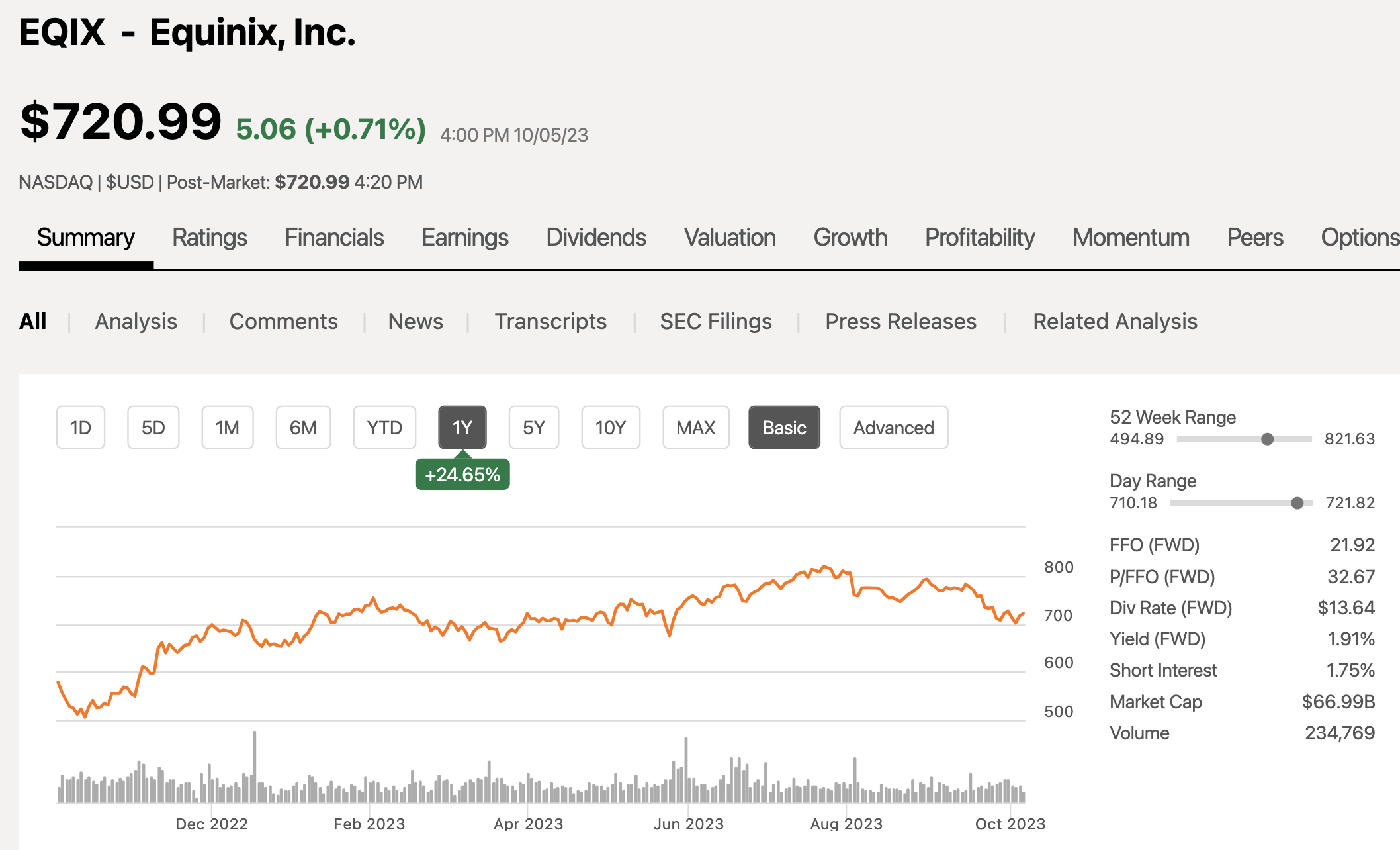

Equinix is the largest data center REIT with a market cap of $67 billion. Over the past 12 months, although the REIT sector is down heavily, shares of EQIX have climbed 25%, which doubles the return from the S&P 500.

{kind=link}

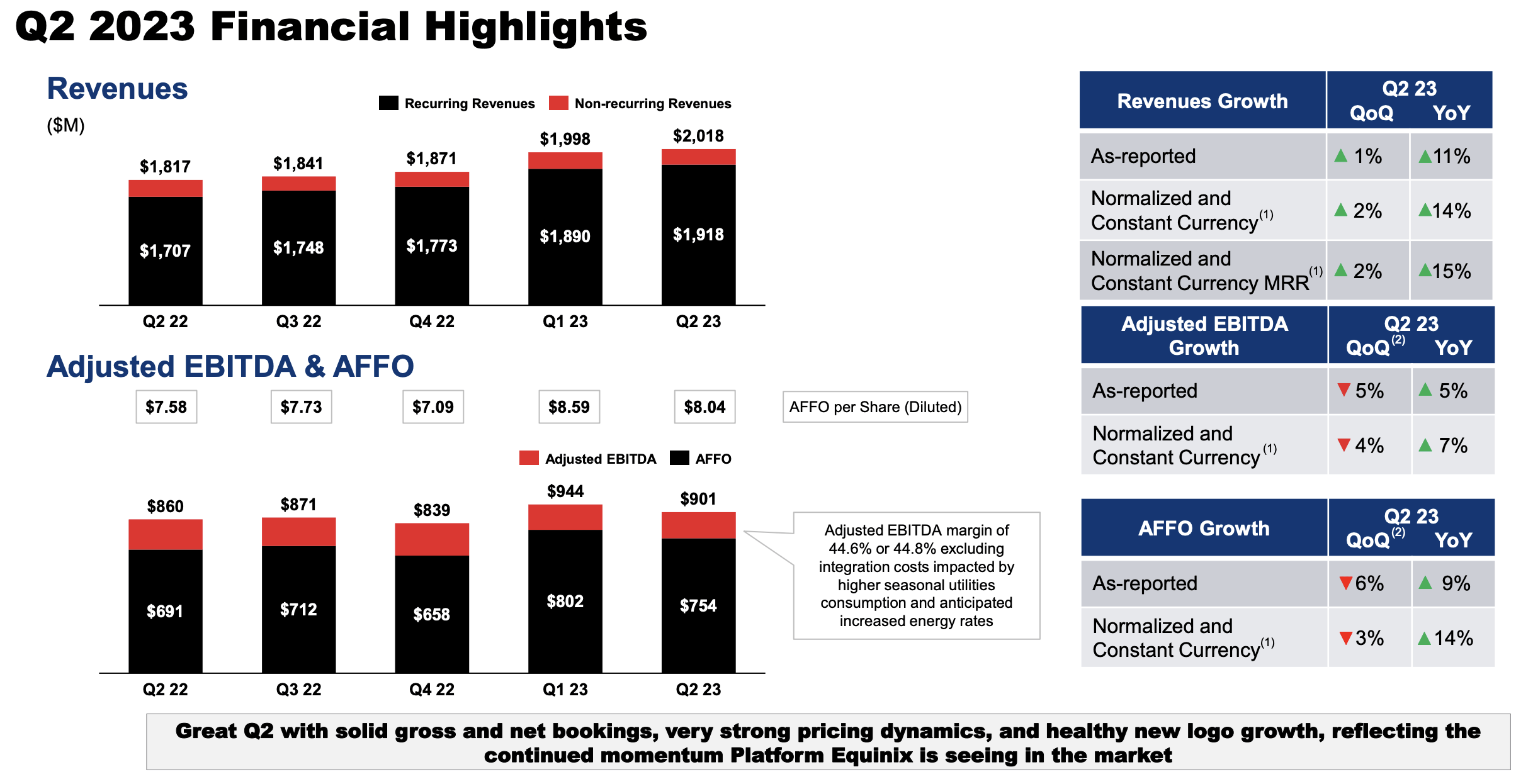

Looking at the chart below, you can see how revenues and AFFO have steadily been growing. On a year-over-year basis, revenues are up 11%, adjusted EBITDA is up 5%, and AFFO is up 9%. These are fantastic results at a time when many REITs are struggling and seeing slim results.

{kind=link}

The more AI and cloud grow, the more the demand for data center space will grow, keeping the outlook very bright for the likes of EQIX and its closest competitor, Digital Realty Trust ( DLR ).

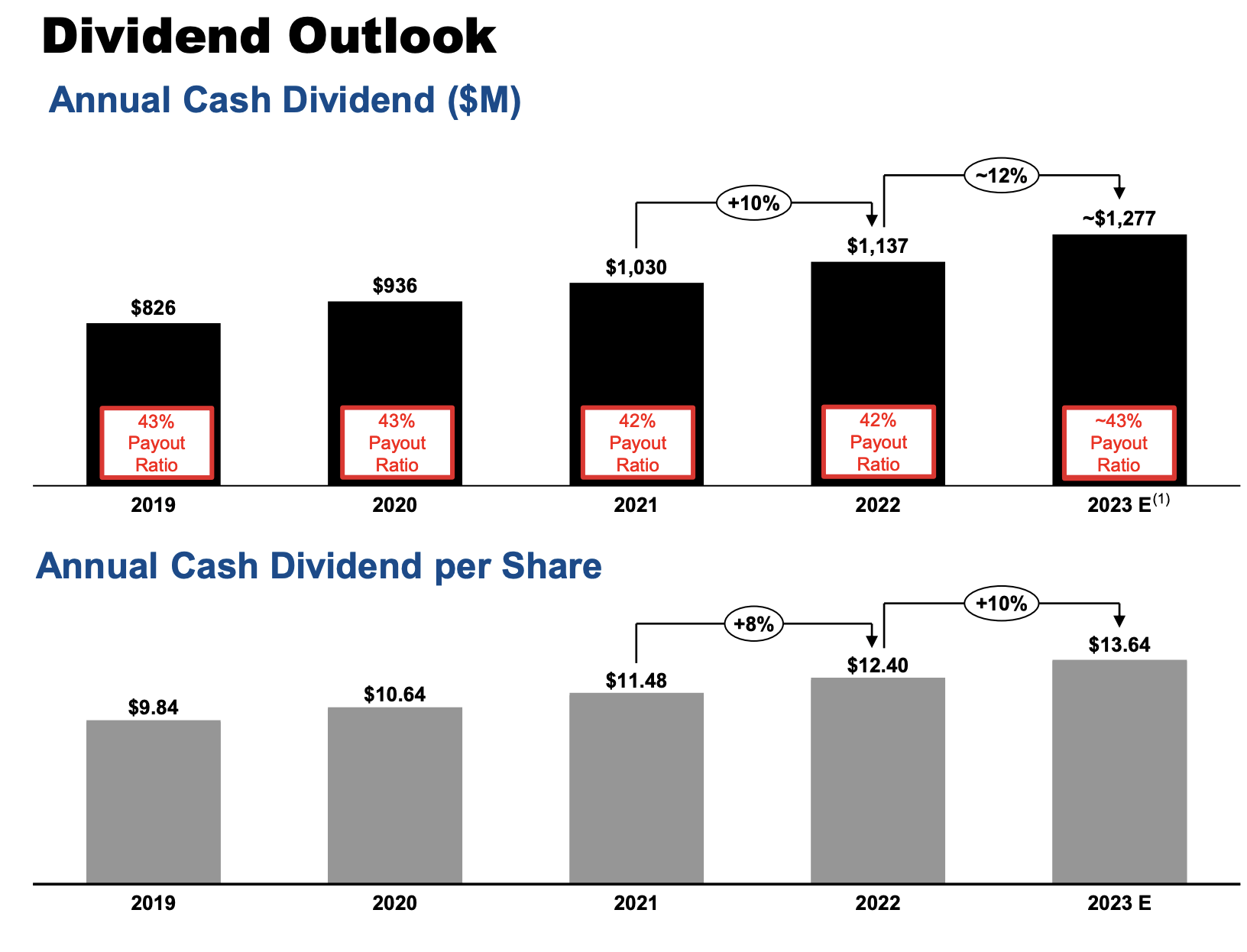

As the results have grown, so has the dividend. In the past year, the dividend grew 10% and over the past five years, dividend growth has averaged around 9% per year.

{kind=link}

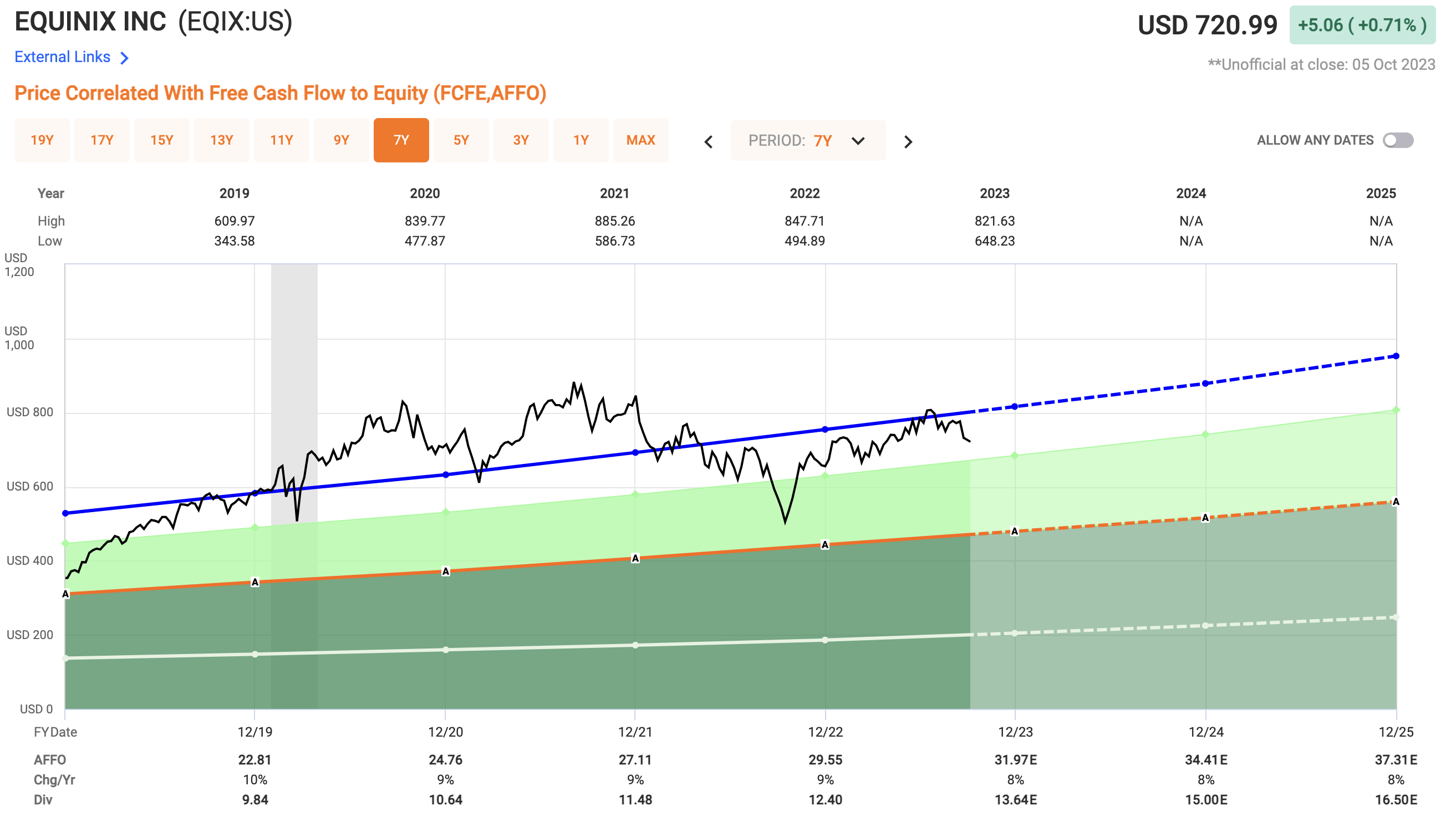

In terms of valuation, even with the growth we have seen in the past 12 months, shares are still very reasonable solely based on the growth ahead. Analysts are looking for AFFO growth of 8% each of the next two years which puts today's AFFO multiple at 20.8x which is below their five-year average of 25.5x.

{kind=link}

1 Cheap REIT I Am Selling

REIT #3 - W. P. Carey ( WPC )

W. P. Carey was a REIT I used to like and own until recent news dropped about the company selling off part of its office portfolio and spinning off the remainder of those office properties. The timing and the mismanagement were enough for me to sell out of my position in WPC.

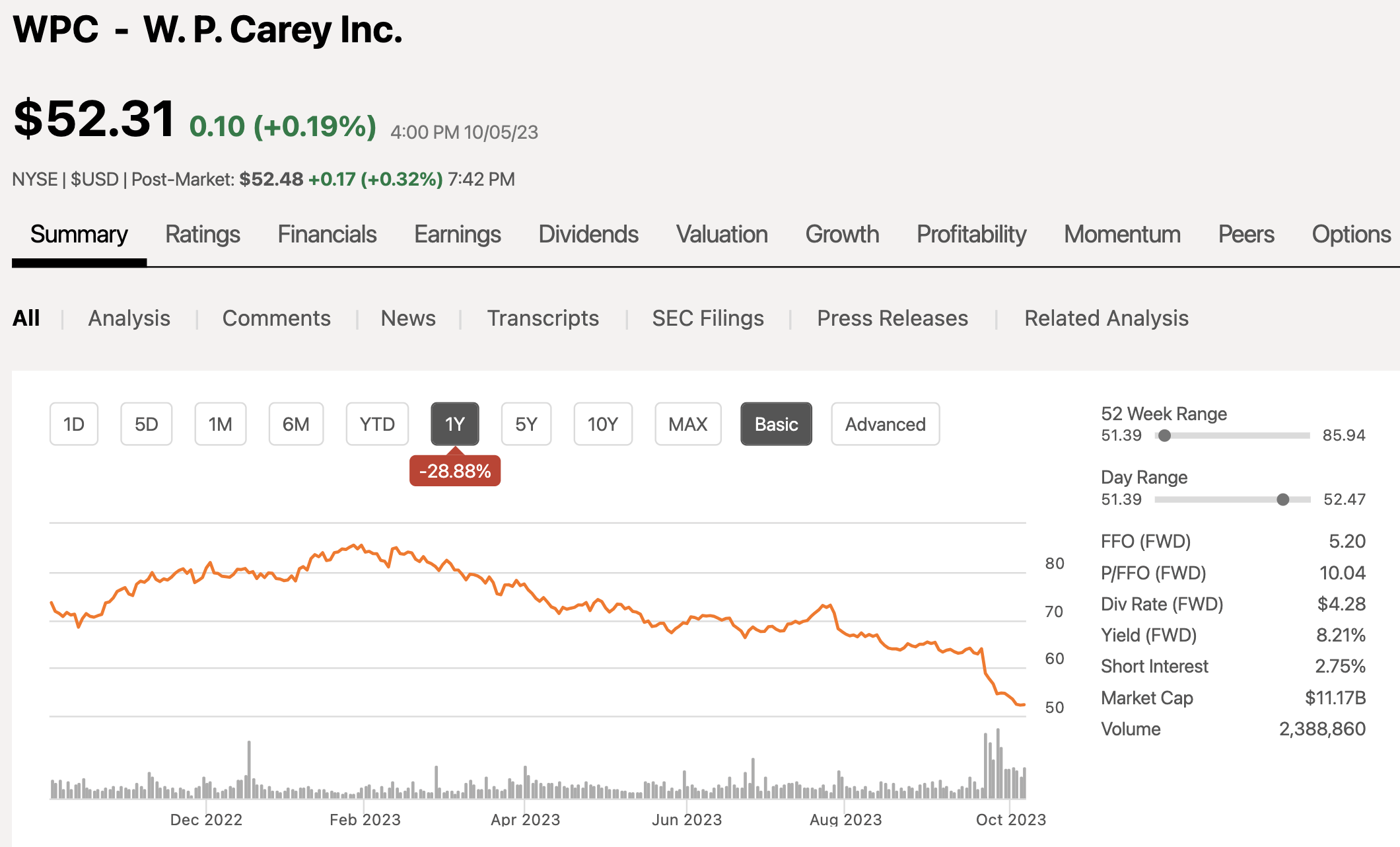

WPC shares have dropped nearly 30% in the past 12 months, including 20% in the past 4 weeks. The market cap currently sits at $11 billion now after the fall.

{kind=link}

Selling off its office portfolio was not the only news that came out in recent weeks, management also decided to slash its dividend, suggesting the company has liquidity issues which are never good. This puts an end to a 24 consecutive year period of hiking their dividend.

All of this news at once was a complete shock to investors and the market as a whole. A dividend, especially a rising dividend, can tell you a lot about the confidence management has in the future of a company. This management has lost the confidence of investors, clearly.

Dividend cutters tend to underperform the market for years, and I am not going to be sticking around to see the turnaround, even if the shares are cheap.

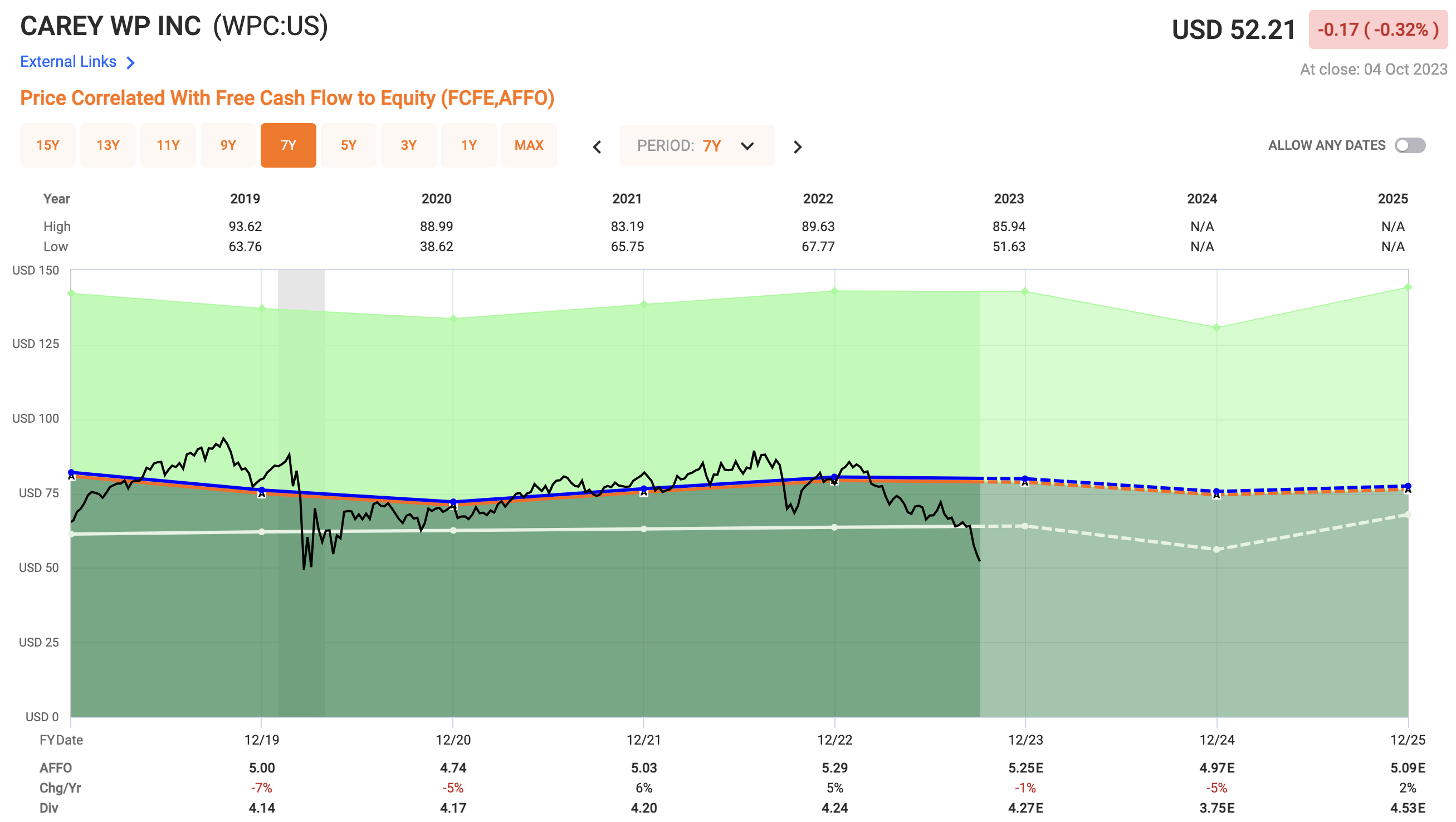

Analysts are calling for 1% AFFO decline this year and another 5% decline in 2024 which puts the average AFFO estimate at $4.97 per share. This estimate equates to an AFFO multiple of 10.5x, which is below their five-year average of 15x. These issues are going to take a few years to get right.

{kind=link}

Investor Takeaway

When it comes to stocks being cheap, some are an opportunity and some are cheap for a reason. WPC is cheap for a reason as the REIT has seen shares slide 20% in the past few weeks as the company ran into liquidity troubles, slashed its dividend, and announced it would be selling and spinning off its office properties. I had owned WPC for a while but quickly sold my position when news broke.

EXR and EQIX are two high-quality REITs that continue to grow. EXR operates in a sector that seems to do well regardless of the economic backdrop. EQIX is seeing robust growth in its sector based on the growth in both AI as well as cloud. The future is bright for both REITs and the valuations are great right now.

In the comment section below, let me know if you agree.

For further details see:

Fire Sale: 2 Cheap REITs To Buy, 1 To Sell