HRT - First Advantage: Uncertain Near-Term Macro Should Make The Stock Range Bound

2023-08-17 18:23:32 ET

Summary

- First Advantage is a leading provider of pre-employment screening services.

- Revenue for 2Q23 was down 8%, primarily due to weakness in international markets and slower growth in certain verticals.

- Despite potential upside and low market expectations, a hold rating is recommended due to concerns about the international segment and the uncertain macroeconomic environment.

Summary

First Advantage ( FA ) is a leading provider of pre-employment screening for companies to check the backgrounds of potential hires. This post is to provide an update on my thoughts on the 2Q23 business results and industry. I am recommending a hold rating for the stock despite my model indicating potential upside and the market having low expectations for the stock. My concern is that the near-term macroeconomic climate remains uncertain and that a deep recession could happen. In that case, FA stock is likely to see further pressure.

Investment thesis

Revenue for 2Q23 was $185 million, down 8% year over year but up 5% sequentially. Revenue fell due to weakness in international markets (down 27%) and slower growth in verticals such as technology, financial services, and business services. The positive drivers were success in up-selling and booking of new logos. The $56 million in EBITDA was roughly in line with projections. Management has reiterated their previous FY23 outlook, but they now anticipate results at the low end of their target ranges. This is good news, in my opinion, as it is still within expectations. Taking management at their word, this would imply a 4% decline in revenue and a 7% decline in adjusted EBITDA and adjusted net income for FY23, with total revenues of $770 million, adjusted EBITDA of $240 million, and adjusted net income of $145 million. Which means, management is expecting the business to see sequential improvements in growth from the weak 1H23 from here onwards.

Paying closer attention to the assumptions that management is making, I see possibilities for FA to beat this new guidance. There is room for FA to outperform if the economy improves, as management's previous expectations for modest improvement in 2H23 macro and hiring trends have been replaced by expectations of the status quo. My concern is with the international segment. While it is a small part of the business, the magnitude of the decline has certainly damaged the growth of the entire business. Within it, management noted India as area that was not performing well.

The decrease was due primarily to weakness in India, given the region's exposure to BPO and IT services-related businesses, and in APAC, given the tepid recovery in China, and other regional market dynamics. 2Q23 earnings results call

Due to its high dependence on BPO, I do not hold out much hope for a recovery so long as the economy remains stagnant. As a direct result of the delay in starting new projects, management has also noticed that their Indian clients have put off their annual hiring of new college grads.

Nonetheless, I think FA and the industry will continue to show healthy long-term growth. Background checks, in my opinion, are cyclical because the industry is driven by the total number of people hired. Nonetheless, the industry has secular tailwinds in the form of rising demand for background checks due to stricter regulations and greater enforcement of existing ones by businesses. Background screening is a highly competitive market, and FA is one of three major players, including Sterling Check ( STER ) and HireRight ( HRT ).

When we compare FA to these peers in various aspects, FA shines better. For one, FA has the best balance sheet strength amongst the three (FA 0.76x net debt to EBITDA vs 3x for the HRT and STER), which is critical in the current high rates environment (also allow FA to return capital to shareholders). Lastly, FA has the best EBITDA margin profile (28.7% vs STER at 18% and HRT at 21%). FA also wins from a stock momentum performance (best share price performance YTD), which makes it screen better than peers. Hence, FA appears to be the best candidate to take advantage of this secular trend among investors. From a stock perspective, FA should continue to see valuations being supported relative to other peers, making it a "safer haven" for capital allocators that are looking to invest in this industry.

As a result, I believe FA deserves higher multiple than that of competitors HRT and STER, and I rank FA as the top operator in its industry. Nonetheless, I wouldn't rush in to invest right now because I anticipate a further decline in hiring as employment trends normalize from historically high levels and stay wary that the FED might gear up rates, which will further hurt underlying business activities (i.e., hiring).

Valuation

{kind=link}

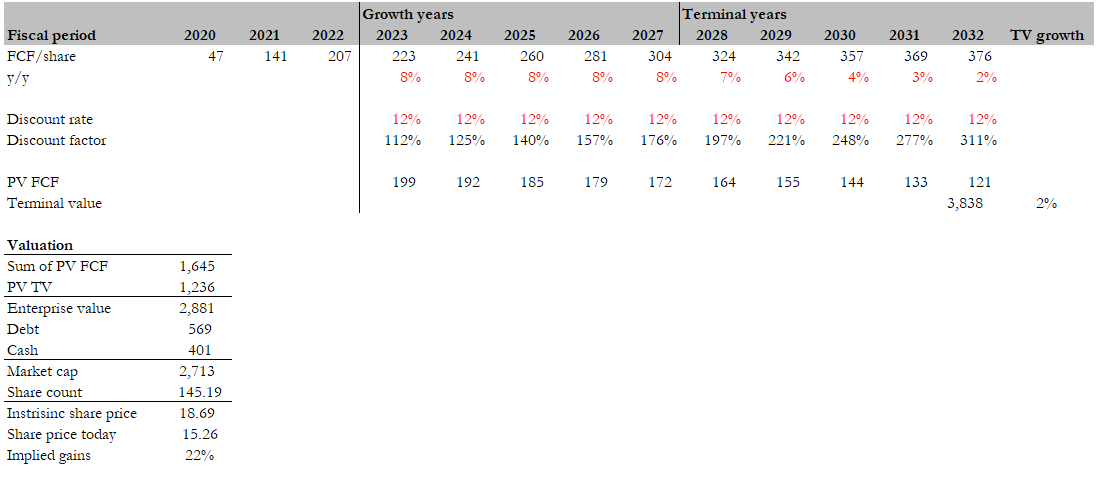

I believe the fair value for FA based on my DCF model is $18.69. My model assumptions are that FA will be able to grow FCF in line with the industry given that it is one of the three largest players in the field. As this is a business that is operating in a cyclical industry, I believe a high discount rate (12%) is warranted. A potential upside to my model is that I did not model share buybacks and dividends, as management has done in recent history. In any case, my model indicates a 22% upside using very conservative assumptions (FCF grows with industry, assuming no share capture from sub-scale players and no margin expansion as it scales). In other words, expectations are pretty low for the business and stock, but I believe the stock will be range-bound until the macroeconomic outlook becomes clearer.

Risk

The need for background screening services is influenced by the performance of customers' businesses and overall hiring patterns. If the current macroeconomic conditions were to transition into a significant economic downturn, it would exacerbate the adverse effects on FA's organic revenue growth.

Conclusion

My recommendation for FA is a hold, despite potential upside indicated by my model and low market expectations. The uncertainty of the near-term macroeconomic environment is likely to cause the stock to be rangebound. I also have concerns regarding the international segment, particularly in India due to its dependency on BPO. Nevertheless, the industry's long-term growth prospects remain strong due to increasing demand for background checks driven by stricter regulations. FA's competitive position, solid financials, and industry-leading margins position it as a strong candidate to benefit from this trend in the long-term.

For further details see:

First Advantage: Uncertain Near-Term Macro Should Make The Stock Range Bound