FAF - First American Financial: Limited Housing Supply Leaves Shares Fully Valued

2023-12-30 03:56:58 ET

Summary

- First American Financial's title insurance business has faced a significant downturn due to a decline in real estate transactions.

- The company's revenue and pre-tax margins have been negatively impacted by the fall in real estate activity.

- Investment income has been aided by higher rates which may begin to reverse in 2024.

- While there may be some improvement in 2024, the magnitude of the recovery is limited by the lack of supply, and the company's shares are viewed as fully valued.

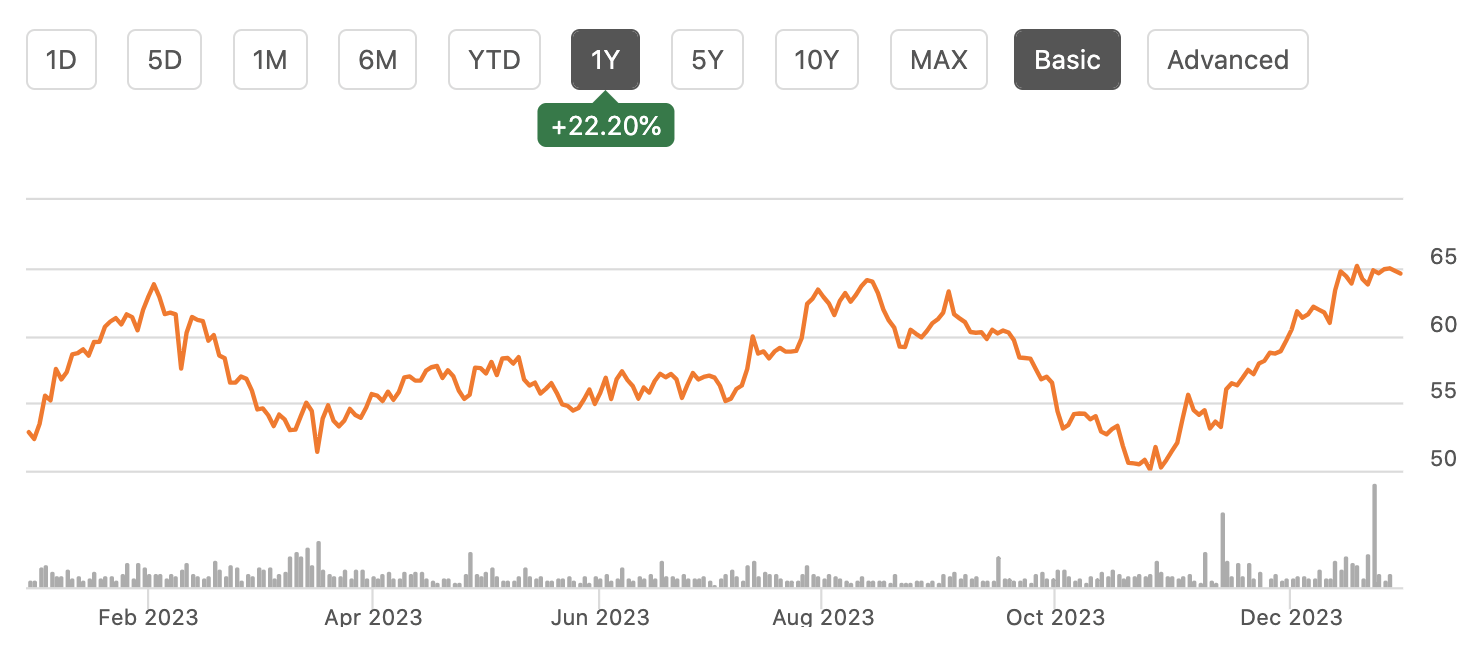

Shares of First American Financial ( FAF ) have returned over 25% this year including dividends, largely keeping pace with the broader market even as its title insurance business has faced a significant downturn. I expect recovery in this unit to be slow, while lower rates could begin to reduce investment income by mid-year. As such, I view shares as fully valued.

{kind=link}

First American generates 95% of its non-investment revenue from title insurance, and it has 25% market share. With higher interest rates, we have seen a meaningful decline in real estate transactions, which has naturally reduced premiums earned in title insurance (as this product is purchased when a home is bought with a mortgage or refinanced). This downturn began in 2022 as revenue fell from $9.2 billion to $7.6 billion. It has continued in 2023.

In the company’s third quarter , it earned $1.22 excluding unrealized investment losses as revenue fell by a further 19% to $1.5 billion. Title insurance revenue is down by 26% so far this year, and peak-to-trough, revenue may fall by about 40%. As with any business seeing revenue decline that much, margins have compressed. Pre-tax margins are down to 12% from 13.3% last year. This is despite the fact that personnel costs are down by 15% to $486 million. Management has moved aggressively to cut costs, but the fall-off in real estate activity has simply been too large to mitigate.

First American ended Q3 with open orders down by about one-quarter, pointing to ongoing weakness through Q4, though management expects title insurance margin to approach $2 billion in 2024, up about $300 million, aided by cost cuts and some rebound in activity. While I do expect to see improvement in 2024, I am cautious as to its magnitude.

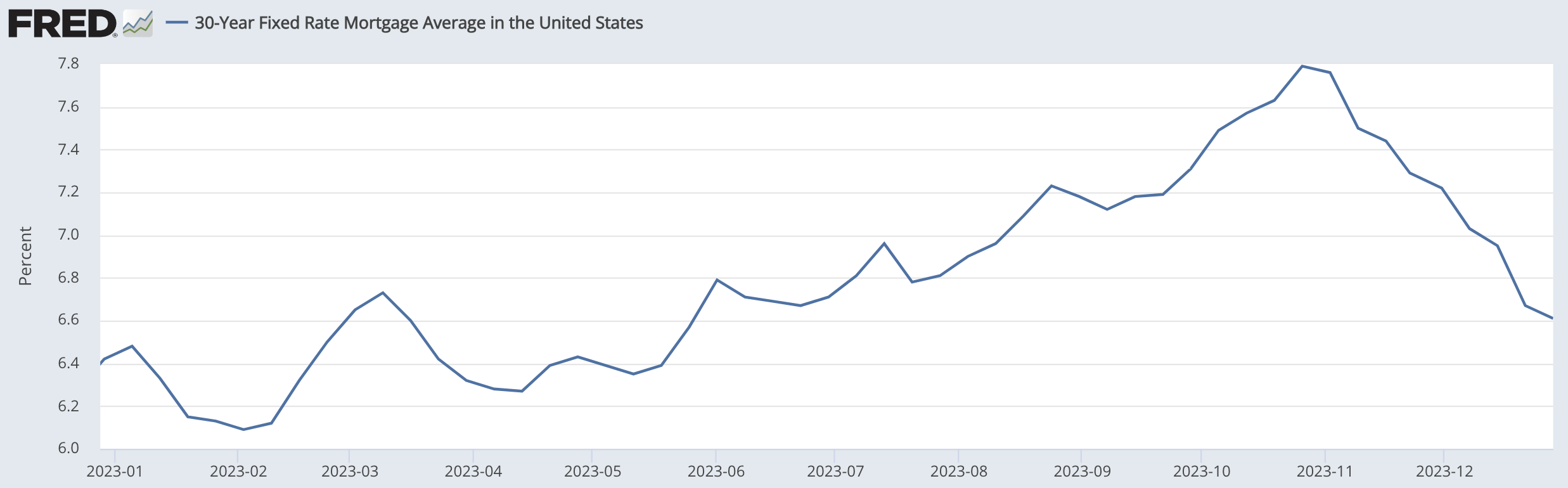

Now, higher mortgages have clearly slowed activity. They have meant refinancing transactions have all but stopped. Additionally, they have made monthly payments much less affordable for new homebuyers, reducing purchases. As you can see below, rates have fallen sharply from two months ago. This should help purchase activity, and some recent buyers may consider refinancing. However, mortgage rates are still higher than at the start of the year. In other words, this decline in interest rates is less likely to spark a surge of home transactions than arrest the decline we would otherwise have seen if mortgage rates stayed at 8%.

{kind=link}

Now, if mortgage rates continue to fall and the Federal Reserve delivers on its anticipated rate cuts in 2024, that could help to spark more demand for housing. While I am sympathetic to the thesis that housing demand increases in 2024, this could lift home prices more so than First American’s business, which is more closely tied to transaction volumes.

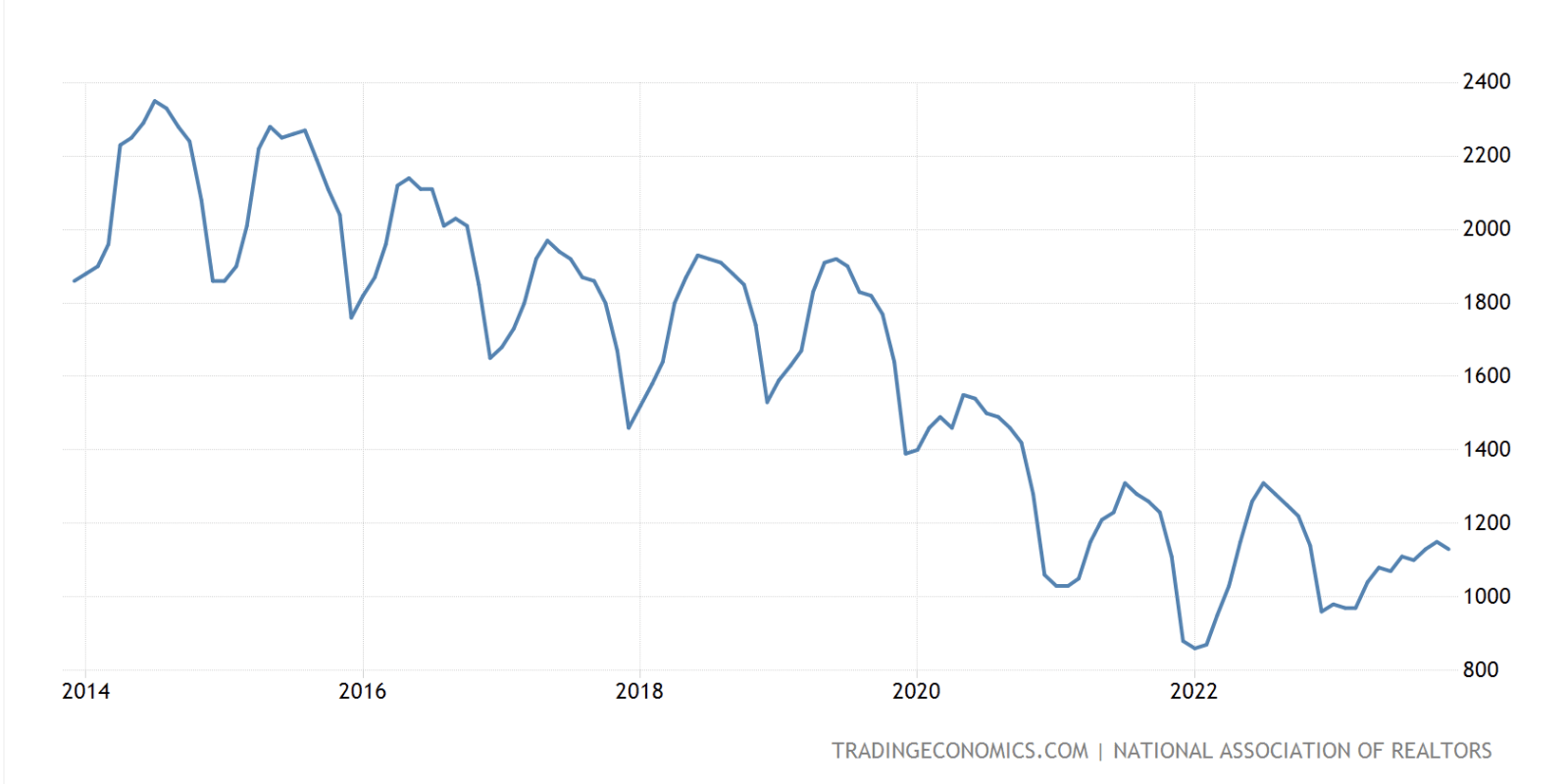

The challenge is that we still have a very supply-constrained market (which is why demand increases could push up prices). As you can see below, the number of existing homes for sale is still extremely low, even as it has risen from trough levels. Until more supply hits the market, it will be difficult to see a significant increase in transactions, even if rates fall further. With so many homeowners having mortgages below 4%, they remain highly incentivized to stay in their home than sell it. This factor is likely to suppress supply for a prolonged period.

{kind=link}

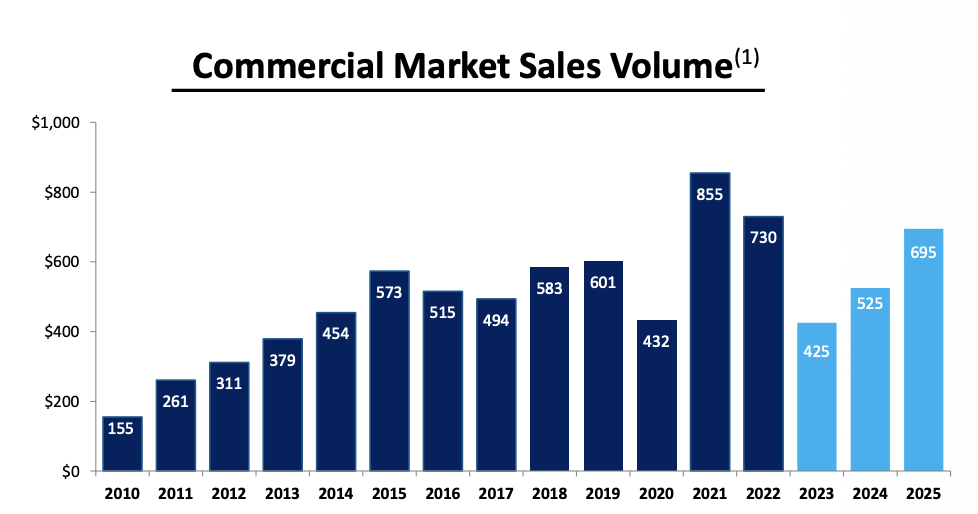

Aside from residential volumes, there has also been a significant decline in commercial transactions given higher rates. Commercial revenue is running down 39% this year. As you can see below, activity has fallen by half since 2021. Management is forecasting an over 20% recovery in 2024 to levels seen in the 2026-2017 period. Given rates are still substantially higher on an absolute basis, a recovery of this magnitude strikes me as aggressive.

{kind=link}

To be clear, I do expect commercial and residential volumes to improve in 2024 vs 2023, barring a recession or a surprise increase in interest rates. Given lower rates and some pent-up demand, activity should improve. However, given supply limitations, I expect improvement to be in the single-digits rather than a full recovery, unless mortgage rates fall much more aggressively, to about 5%, which could begin to unlock more supply.

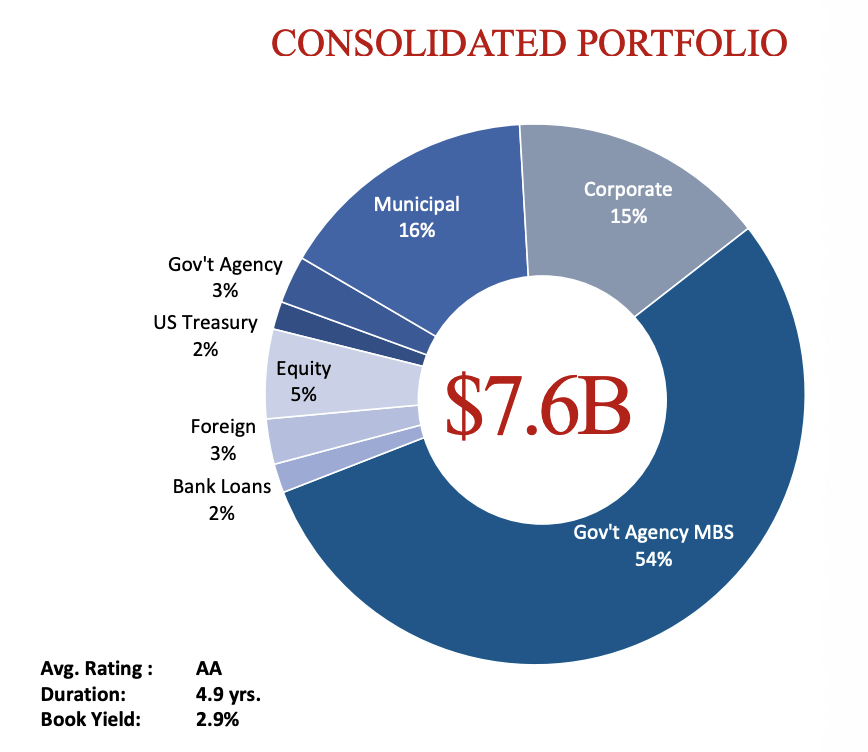

Now, while higher rates have hurt its core insurance business, FAF has seen a benefit on its investment portfolio. Net investment income rose to $142 million in Q3 from $105 million last year as it reinvests short-dated securities at higher interest rates. As you can see below, FAF maintains a high-quality investment portfolio with an AA average rating, leaving it with minimal credit risk. Management estimates that each 25bp Fed move has a $15-20 million annual impact.

{kind=link}

This becomes the challenge for determining how much earnings and cash flow can recover next year. If we assume the Fed delivers on 3 rate cuts, that will be a ~$60 million annualized headwind. Assuming a 15% incremental margin, FAF will need to increase title revenue by $400 million to offset this loss. That is about 7% growth from 2023 levels. If market pricing for 5 or 6 cuts materializes, the required transaction growth is even greater.

Now, high-single digit growth is a reasonable expectation in my view, but because of headwinds on its investment portfolio, this may not allow the company to actually increase earnings much from its ~$4.50 run-rate with about $550 million of annual operating cash flow.

Now, the company also raised its divided by 2% to $2.12 annually, and while it has slowed buybacks from $441 million in 2022, the share count is 1% lower than a year ago. However, with $1.9 billion of debt, FAF has a 23.5% debt to capitalization vs an 18-20% target. Beyond the dividend, which costs about $220 million, that means operating cash flow for the next 12–24 months should go to deleveraging its balance sheet rather than repurchases.

I would also note that the company did suffer a cybersecurity incident, but operations are back online as of 12/28 . Bank accounts were always secure, limiting the financial risk of this event, though Q4 results could be softer due to systems interruptions. Ultimately, I do not see material ongoing financial risk from this event that is material and would shift the investment thesis.

With mortgage rates declining, I can understand investors looking to play a housing recovery. Given limited supply, I tend to think increased demand is more likely to boost prices than transaction volumes, limiting FAF’s upside, which is why I have consistently liked the homebuilders, like Toll Brothers (TOL). Additionally, there may be some headwind to investment income that offsets transaction growth as the Fed cuts rates. With shares at 14x, earnings growth minimal, and debt above long-term targets, I view shares as fully valued and likely to be dead-money. While there may not be significant downside absent a recession, I would take advantage of the rally to rotate out of FAF.

For further details see:

First American Financial: Limited Housing Supply Leaves Shares Fully Valued