FNLC - First Bancorp: A Quality Balance Sheet Justifies The 1.6x TBV Share Price

2024-01-05 10:30:00 ET

Summary

- The First Bancorp's net interest income remains strong despite the challenging interest rate climate.

- The bank reported a net profit of $22.8M for the first nine months of 2023, with a low default rate on its loan book.

- The bank's stock is trading at 1.6 times its tangible book value.

Introduction

As I still like regional banks, I am taking a look at some smaller names I previously covered to see if there's any value in some of them. The First Bancorp, Inc. ( FNLC ) is a Maine-based bank holding company , and I am mainly interested in seeing how the bank is able to protect its net interest income and how the equity and book value may be impacted by unrealized losses in the portfolio of securities held to maturity.

The earnings remain strong thanks to a robust NII performance

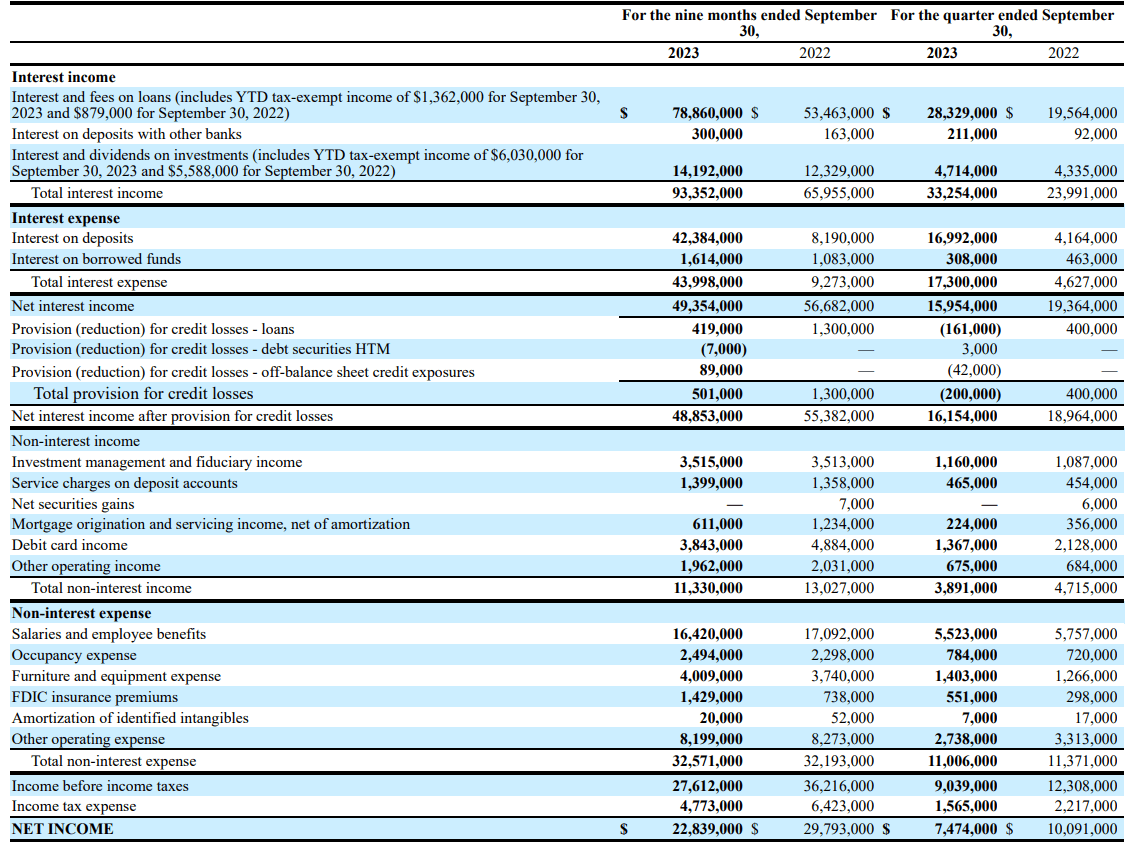

I am actually quite pleased with how The First Bancorp is navigating through this tricky interest rate climate. In fact, its net interest income decreased by just a low-double digit percentage compared to the first nine months of last year. As you can see below, the total interest income increased from $66M to just over $93M and this was almost sufficient to compensate for the interest expenses which almost quintupled. The net interest income was $49.4M, and while the Q3 net interest income was a bit weaker with just under $16M, the performance is still quite alright.

{kind=link}

Looking at the Q3 results, the bank also reported a net non-interest expense of approximately $7M resulting in a pre-tax income of $9.04M. This includes a $0.2M reversal of previously recorded loan loss provisions and this helped to boost the net income to $7.5M for an EPS of $0.68.

Looking at the 9M 2023 performance, the bank reported a net profit of $22.8M for an EPS of $2.08 despite recording a net amount of $0.5M for loan loss provisions (about $0.7M of loan loss provisions was recorded in the first semester before FNLC was able to take back some of those provisions in the third quarter).

So from an earnings perspective, FNLC looks pretty interesting. The quarterly dividend of $0.35 is well-covered with a payout ratio of just over 50% which means the bank is able to retain approximately $15M per year on its balance sheet.

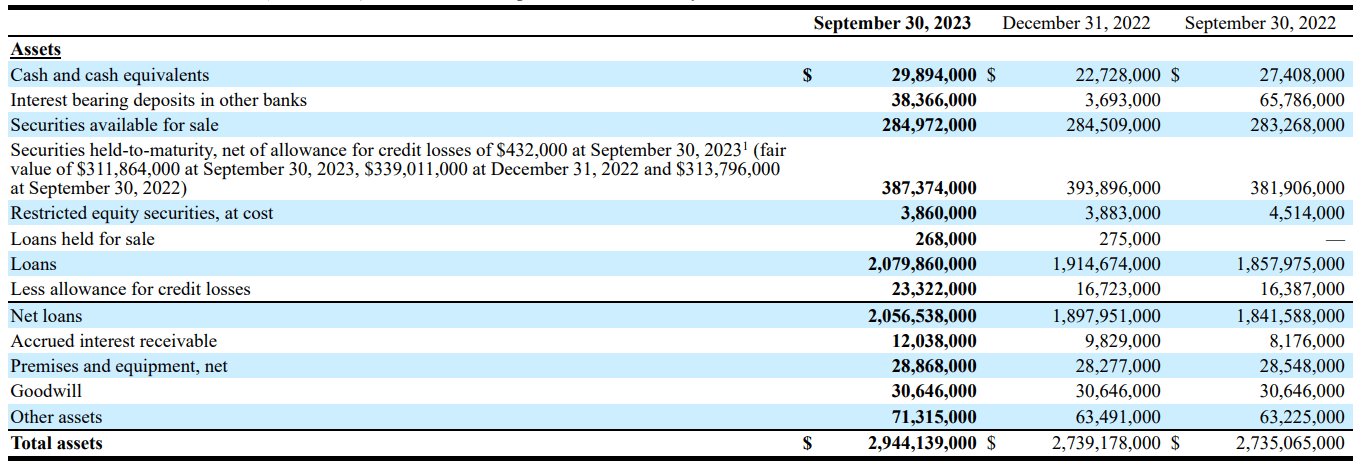

Looking at that balance sheet, the image below shows the bank has a total equity value of $226.7M which is in line with the FY 2022 equity position indicating the fluctuations in the portfolio of securities available for sale have been almost entirely neutralized by retained earnings.

{kind=link}

I also still like the bank's pretty liquid balance sheet. Of the $2.94B in assets, approximately $350M is held in cash and securities available for sale with an additional $387M in securities held to maturity.

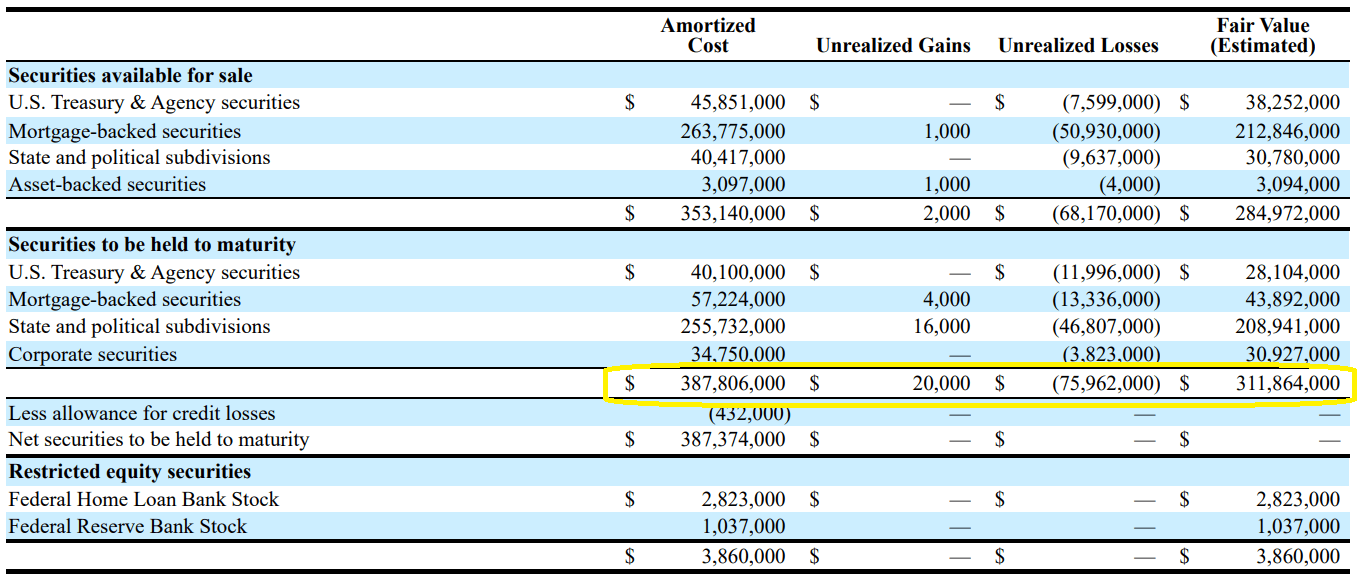

Looking at the footnotes to the financial statements, those securities held to maturity have a current fair value that's approximately $76M lower than the book value. While this would have a negative impact on the book value of approximately $6.8/share (the bank had a book value of $20.44 and a tangible book value of $17.66 per share as of the end of September so the pro forma TBV would be approximately $11/share if one would take the unrealized losses in the HTM portfolio into account), the risk is manageable as long as FNLC isn't facing a liquidity issue. The portfolio of securities HTM has a pretty long duration with in excess of 70% of the portfolio maturing after more than 10 years. Less than 5% of that position matures within the next five years.

{kind=link}

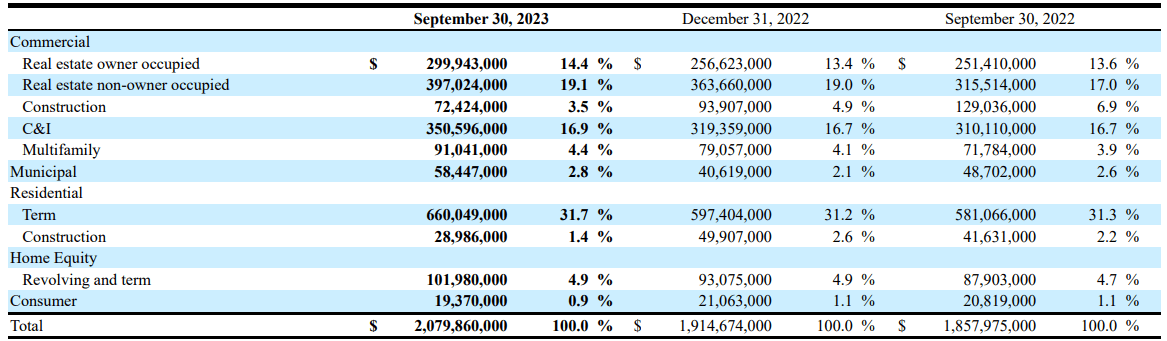

I was also pretty interested in the bank's loan portfolio which increased to $2.08B as of the end of September. The majority of the portfolio consists of commercial real estate, but I also like the 33% exposure to residential real estate.

{kind=link}

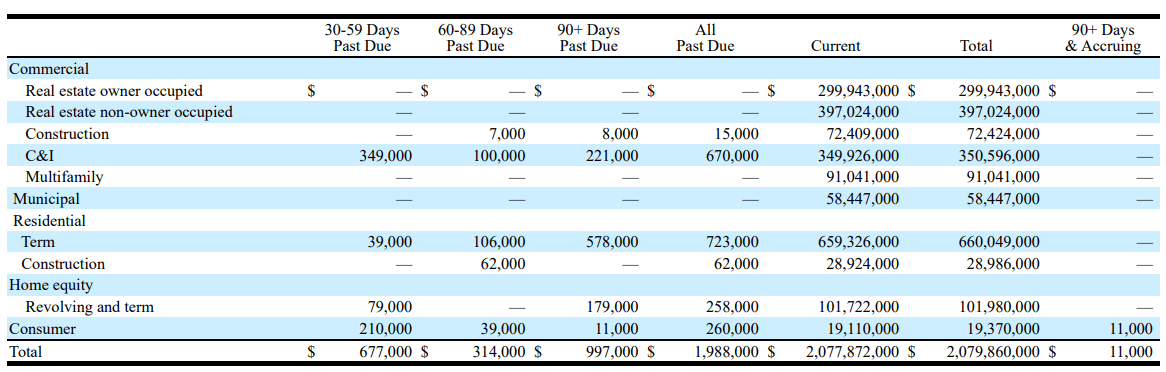

I'm fine with a bank having a relatively high exposure to commercial real estate, as long as the loans are paid off on time. And FNLC has an exemplary loan quality. As you can see below, less than $2M of the $2B loan book is currently past due.

{kind=link}

This means less than 0.1% of the loan book is currently past due and that is very remarkable.

Investment thesis

As explained in a recently published article on another small regional bank, Ames National Corporation ( ATLO ), I'm usually not keen on paying 1.5 times the tangible book value, but a very strong regional bank could be an exception to the rule. FNLC is trading at about 1.6 times its tangible book value (excluding the unrealized losses in the portfolio of securities held to maturity) but as the market interest rates start to decrease again, that unrealized value should decrease while the portfolio of securities available for sale should see a value increase.

I am especially impressed with the very low default rate of the loan book. This, in combination with an attractive dividend and the ability of the bank to retain in excess of $1/share in earnings on an annual basis, makes FNLC attractive.

I currently have no position in The First Bancorp, but I will follow this bank closely from now on.

For further details see:

First Bancorp: A Quality Balance Sheet Justifies The 1.6x TBV Share Price