FCNCB - First Citizens BancShares Still Has Room To Run After 50% Gain

2023-03-28 15:19:10 ET

Summary

- First Citizens BancShares, Inc. trades at 70% of book after the recent run up.

- During normal times, First Citizens has traded for 1.5 times book value.

- Management has a track record of buying distressed banks for shareholders' benefit.

- Historically, First Citizens BancShares has been a well-run bank.

What happened?

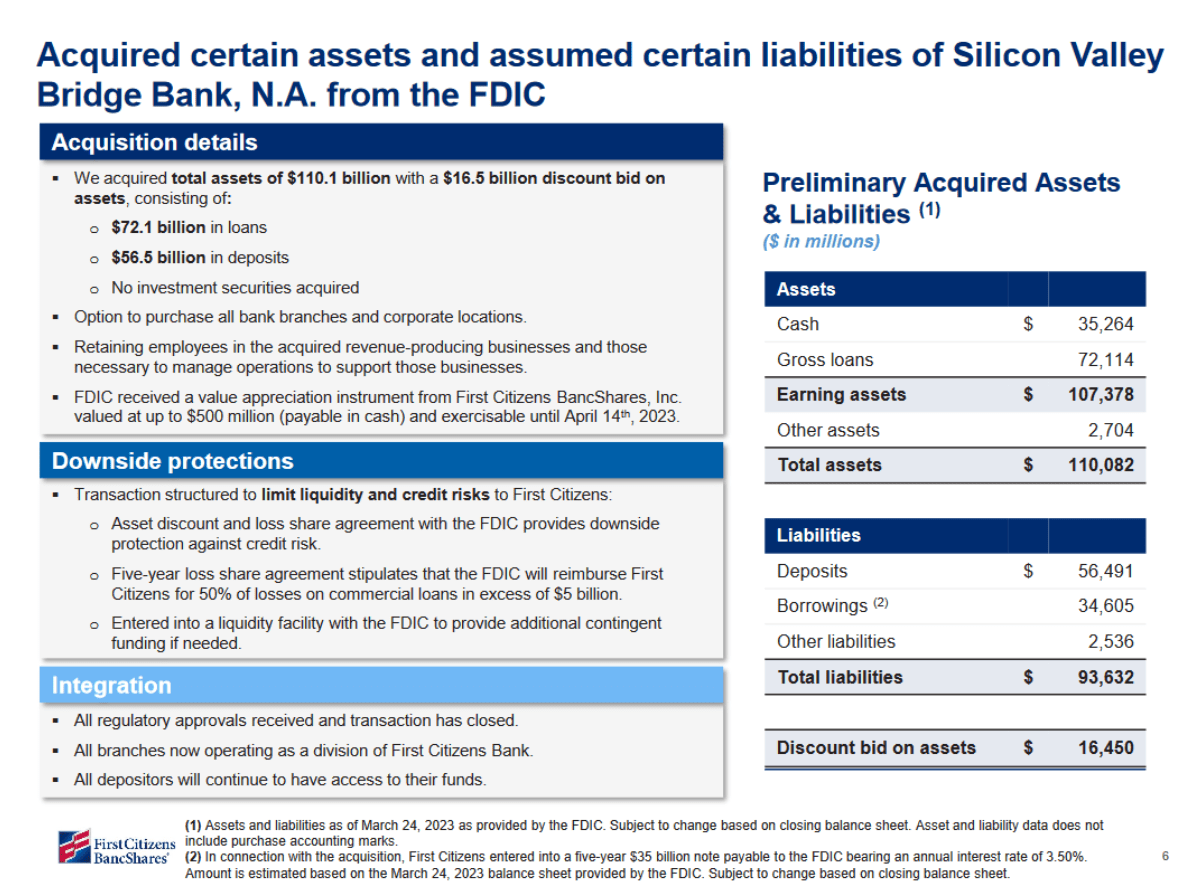

First Citizens BancShares, Inc. ( FCNCA , [[FCNCB]]) bought part of Silicon Valley Bank of SVB Financial Group ( SIVBQ ) from the FDIC. They got a $16.5B discount along with several other sweeteners from the FDIC. This $16.5B is free equity for FCNCA. An eye-popping amount, considering that FCNCA only had $8.8B in common equity before the deal.

In addition to this free equity, First Citizens BancShares, Inc. received several other benefits. A 5-year, $35B loan at a 3.5% coupon. 5-year treasuries currently yield ~3.5%, so borrowing at this rate is a coup. Downside protection in the form of a loss share with FDIC if loan losses exceed $5B. A liquidity facility that will allow FCNCA to borrow from the FDIC at a market rate. This facility is large enough to guarantee all non-insured deposits that FCNCA will have after the acquisition. $56.5B in low-cost deposits.

{kind=link}

Adding all of this up, FCNCA got a great deal. This transaction will double their shareholder equity without them needing to issue a share. In addition, the loan facilities and loss sharing provide downside protection.

While FCNCA rallied 50% on the news, it is still well below the expected book value. Historically, FCNCA has been recognized as a well-run bank that deserved a premium to book value.

Looking at the banker

The rest of this article is going to be a breakdown of the numbers behind the acquisition. I want to focus on the acquiring bank first. The bank itself and the banker are critical to the thesis. These bankers have the best idea of their existing assets and the assets being acquired. While we can break down the numbers, it's hard to trust them without trusting the banker themselves. FCNCA has been run by Frank Holding, Jr. since 2008 . Before that, Frank had been the president of the bank since 1999. FCNCA and its predecessor organizations have been in the Holding family since 1935. It is safe to say that Frank has banking in his blood.

FCNCA has been a well-run bank, having a positive return on equity every year since at least 1993. I find it reassuring that Frank has been on board for multiple economic cycles.

Frank and the holding family have a significant amount of net worth attached to First Citizens BancShares, Inc. They own over 20% of the economic interest in FCNCA. They have been net buyers of the stock in the past year. Continuing to put their money on the line.

FCNCA has grown by buying distressed banks. Buying 12 banks out of receivership since the GFC.

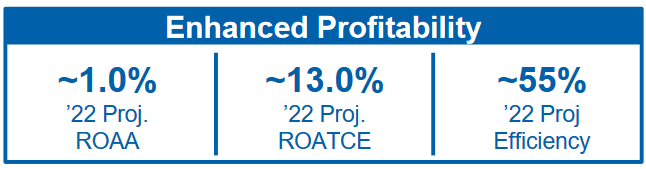

Most recently, they acquired CIT group in a highly accretive deal. They combined CIT’s specialized commercial lending portfolio with FCNCA’s strength as a deposit-gathering franchise. So far, management has delivered on the promised synergies and the deal has been highly accretive. Compare the pro-forma metrics from the merger announcement.

Management's efficiency projections from CIT merger announcement (FCNCA investor relations)

{kind=link}

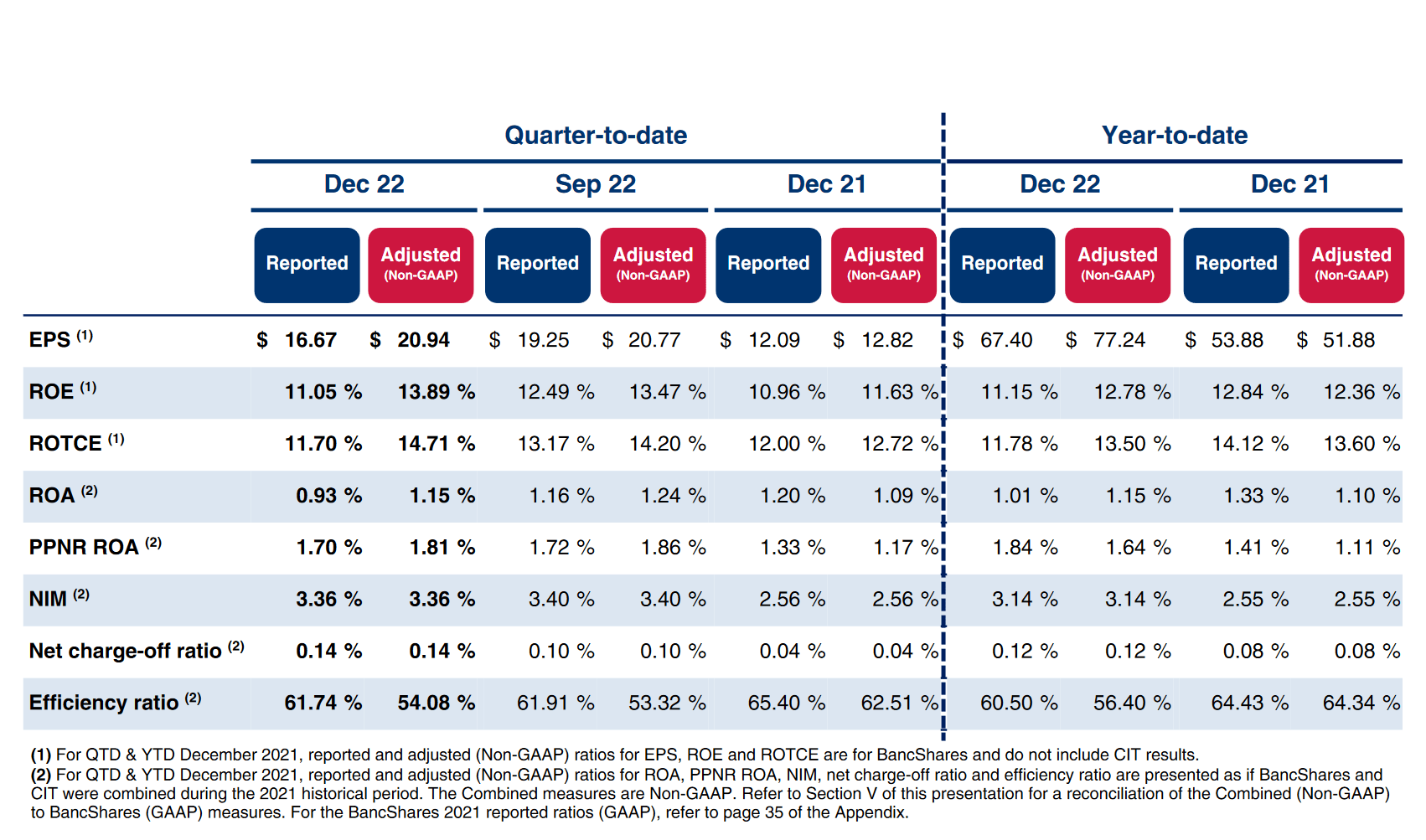

To the actual results from 2022 Q4.

{kind=link}

They are exceeding or close to all their projections. Resulting in EPS and tangible book value per share growing by ~40%.

Book value per share

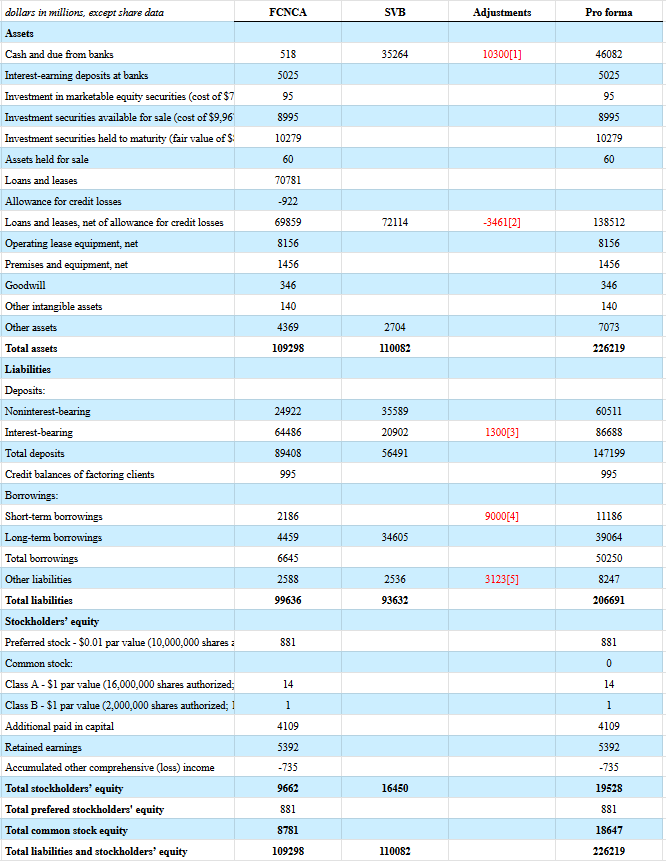

My work suggests that the common shareholder equity doubled from ~$9B to ~$18B when First Citizens BancShares, Inc. acquired SIVB. For reference, the current market cap is $12.9B, so FCNCA is still trading at a big discount to book.

There is some guesswork in my estimate. But I feel it is close to accurate and, given the large margin of safety, I don't feel a need to be more accurate. Here is my balance sheet breakdown, with adjustment explanations.

FCNCA pro forma balance sheet post transaction (Author's work)

{kind=link}

Adjustments:

[1] Per transaction presentation. First Citizens BancShares, Inc. has gained $1.3B deposits this quarter and borrowed $9B from the FHLB.

[2] The Loan portfolio already comes with ACLs built in. To be extra conservative, I'm writing off an additional 20% of SIVB's riskiest assets. This assumed write-down puts us close to the $5B limit where FCNCA would start splitting losses with the FDIC.

[3] FCNCA has gained $1.3B in deposits mostly in their direct banking business. Direct banking pays a high-interest rate.

[4] FCNCA borrowed $9B from the FHLB in order to provide additional liquidity before the transaction.

[5] $500M in the stock appreciation rights that FCNCA granted to the FDIC. Plus $2623M for a 21% tax on the bargain purchase gain.

I didn't deduct any value for duration exposure in the loan portfolio. 92% of SIVB's loan portfolio is floating-rate. While they do have some exposure to long-maturity fixed-rate mortgages, the impact of marking them down would be inconsequential.

{kind=link}

It is notable how much cash on hand First Citizens BancShares, Inc. has. They could have almost the entire SIVB deposit base runoff and cover it with cash. FCNCA is not going to fail in the short term because of liquidity.

Earnings power

Normalized earnings power is harder to project. The biggest question is the liability side of the balance sheet. A lot depends on if FCNCA can retain SIVB's remaining depositors and potentially win some old customers back. Having access to these low-cost deposits would juice earning power.

My guess is that most of the remaining deposits stay in FCNCA. If you already made it through a bank run and bank failure I don't know why you would move now. It's also possible SIVB regains some of the deposits they lost if former clients decide to put some, but not all, of their money back in the bank.

On the call, management gave some hints on what they expected to earn.

Frank my last question is on the assets acquired. Is there any way to estimate what ROA would be on those assets? I think legacy first citizen is well north of 1%? Is there any reason to believe the ROA on those assets couldn't be over 1%?

-Brady Gailey - analyst

Yes. No reason to believe that they could not be in that range

-Craig Nix - CFO

If we assume a 1% ROA, that would yield $2.3B in earnings power.

Over the last ten years, SIVB has averaged slightly over 1% ROA while FCNCA has averaged somewhat under. So this estimate feels reasonable to me. This estimate would be conservative in the current rate environment. Both SIVB and FCNCA are banks that would benefit from non-zero interest rates. Both have a large percentage of their assets in floating-rate loans and low-beta deposits.

Risk - Poor assets

Assets acquired either from CIT or SIVB could sink FCNCA. CIT assets have at least been digested for a year. Early results look good but things could still go wrong. CIT is focused mostly on CRE lending. Specifically specialized commercial lending. They have a wide range of what their loans are secured by.

SIVB portfolio is over half capital call lines . Capital call lines are used by private equity funds to smooth working capital needs between raising funds from their LPs. These loans are generally low-risk since they are secured by large private portfolios at a low LTV. They are also mostly floating-rate and have less than a year until maturity.

The other half of the portfolio is mostly centered around lending to high-net-worth individuals and lending to leveraged buyout firms/early-stage startups. The part of the portfolio centered around early-stage start-ups and leveraged buyouts is the riskiest, especially in the current environment. But it is small enough that even if FCNCA loses all its investment, it wouldn't sink them.

For the SIVB loans, some extra protection is offered from the FDIC loss share agreement. For any loss of over $5B, the FDIC will eat half of the loss. For both sets of loans, we have to put trust in management, which is why I emphasize their track record.

Risk - Too many acquisitions

A financial that is growing quickly is not usually a good sign. Banks that are serial acquirers often don't perform well. It can be hard to maintain customer relationships, risk management standards, and a consistent experience when merging.

In Q1 2022, FCNCA doubled its size when it merged with CIT. They had barely finished digesting that acquisition when they merged with FCNCA. Once again doubling their size. That is a lot of growth.

I think in both cases it helps that the other banks were bought at bottom basement prices. If you pay a low price you can still have a good outcome if things go wrong. CIT had a high cost of funds pre-acquisition. They also didn't have a long track record of success, they failed during the GFC. These factors lead to a depressed valuation. FCNCA was able to scoop CIT on the relatively cheap.

SIVB was obviously a significant discount. The FDIC was a forced seller. In their first auction process, they didn't even get a bid they could accept. Value recovery is also not the only thing the FDIC looks for when selling a bank.

FCNCA had another period during and after the GFC when they gobbled up a number of failed banks. Frank Holdings Jr. was also the CEO then, so he has a track record of being able to pull this off.

Valuation

The price to book is the best way to value First Citizens BancShares, Inc. currently. I normally like using earnings power, but there is too much uncertainty in future earnings. FCNCA has traded for 1.5 times its book value during normal times. Considering the specialized loan portfolios, low-cost deposit base, and track record of strong management, 1.5 times book feels fair.

Given my project book value, this would value First Citizens BancShares, Inc. at ~$1900 a share. Still a huge premium from the current price.

Final thoughts

First Citizens BancShares, Inc. is in the least popular areas of the market right now. Venture capital lending, commercial real estate, and regional banks are all seen as high-risk. However, the sweetheart deal they got from the FDIC makes the math compelling.

While the current story has some unknowns, I believe the large margin of safety makes First Citizens BancShares, Inc. compelling. I like the combination of an asset undervalued because of unknowns and a jockey with a track record of success.

For further details see:

First Citizens BancShares Still Has Room To Run After 50% Gain