CCSI - First Eagle High Income Fund 2nd Quarter 2023 Commentary

2023-08-23 04:10:00 ET

Summary

- First Eagle Investments is an independent, privately owned asset management firm dedicated to serving the needs of individuals and institutions worldwide as well as the financial professionals that advise them.

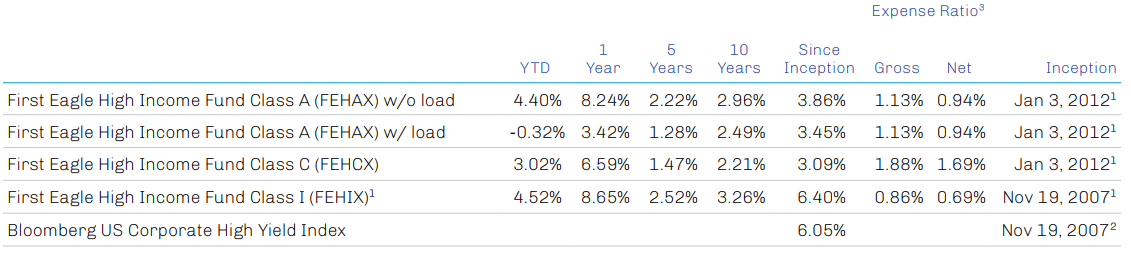

- High Income Fund A Shares (without sales charge) posted a return of 1.17% in the second quarter 2023.

- The High Income Fund underperformed the Bloomberg US Corporate High Yield Index in the period.

Market Overview

The second quarter was in many ways a photo negative of the first. With March’s bank failures seemingly contained, markets refocused their attention on the hawkish rhetoric coming from the Federal Reserve, sending interest rates sharply higher and supporting the performance of shorter-duration credit.

The Bloomberg US Corporate High Yield Index posted a return of 1.7% in the quarter, lagging the 3.1% advance of the Credit Suisse Leveraged Loan Index but besting the Bloomberg US Aggregate Bond Index’s 0.8% loss. Notably, lower-quality paper - which one would assume would be most fundamentally challenged by the higher cost of capital and/or a weakening economy - led the way during the quarter.1

Twisting in the Wind

Perhaps the most interesting thing about fixed income markets thus far in 2023 has been the lack of a unifying theme beyond the direction of interest rates. In searching for certainty around the terminal fed funds rate, the market has considered everything, it seems, other than the Fed’s explicit messaging, though that may have changed - somewhat. Fixed income markets generally had seemed to coalesce around the “higher for longer” narrative toward the end of the first quarter, but mid-March’s bank failures called into question the Fed’s willingness to follow through on this strategy amid such systemic fragility, pulling rates lower across the curve. The rate pendulum began to swing back in the other direction starting with the Fed’s May 3 policy meeting. Though the 25 basis point increase, which brought the federal funds rate target to 5–5.25%, was dubbed by some as a “dovish hike” given the messaging that accompanied it, rhetoric from Fed governors in the days and weeks that followed made it clear there was still work to be done in the fight against inflation. This was amplified at the central bank’s mid-June meeting; though the fed funds rate was left untouched, many considered this a “hawkish pause” in light of Powell’s comments and the release of a new dot plot showing rates peaking at 5.6% later this year.

Traders responded accordingly; by the end of June, market-based indicators of rate expectations forecast the fed funds rate to peak around 5.4%; in mid-May, the expected terminal rate was just shy of 5%.2 If the market seems to have bought in on the Fed’s insistence that rates will be higher, however, it has yet to be convinced that they will stay that way for longer; traders are expecting rate cuts in late 2023/early 2024. In contrast, Fed Chair Powell suggested in recent comments that he doesn’t expect core inflation to get back to 2% until 2025 and that “we’re a long way” from loosening policy. It’s easy to see why; while headline inflation has improved markedly on the back of falling energy and food costs, core inflation remains sticky, reflecting resilient economic activity and a still-strong labor market.

The volatility we have seen in rates and spreads has weighed on issuance across leveraged credit. Borrowers aggressively took advantage of the near-zero rates that resulted from pandemic-related stimulus, and significant bond and loan issuance was met by very strong demand from investors desperate for yield. This dynamic has flipped over the course of the tightening cycle, however. Issuers uncertain about the trajectory of rates are reluctant to commit to financing at current levels, while investors are content to clip Treasury coupons without credit or duration risk while they wait for markets to settle down. Notably, the maturity wall for this year is minimal, which should provide some needed breathing room for the market, which could be vital given investor demand trends and signs that lenders are less willing to extend credit.

What Lies Beneath

While the high-yield market has performed well year to date thanks to decent coupons and a little bit of spread tightening, we need to be mindful of the problems that may be lurking below the surface. One example of this is the increase in distressed exchanges - out-of-court exercises in which troubled companies and creditors agree to a debt restructuring as an alternative to more-formal bankruptcy proceedings - since the start of the tightening cycle. These exchanges tend to be a forward indicator of trouble, as Moody’s estimates 47% of these businesses “re-default” after a restructuring.3 Year-to-date, more than $50 billion worth of bonds and loans have either defaulted or engaged in a distressed exchange, which already is more than all of last year. It would not be surprising to see this trend continue or perhaps accelerate in what we expect to be a fairly extended default cycle given the high levels of corporate debt and leverage.4

It seems like we’re in an interregnum between policy actions and their consequences, with the ultimate impact on markets and the economy likely to intensify the longer tighter conditions persist. Should the economic outlook deteriorate meaningfully, we are likely to see a widening of high-yield credit spreads and dispersion in performance among ratings cohorts, with lower-rated issues lagging significantly. In such an environment, we believe it is wise to focus on minimizing downside risk through shorter-duration, higher-quality, more-liquid issues from companies that have the pricing power to pass along rising input prices. Further, we maintain our defensive bias, with overweight in sectors like consumer non-cyclicals and underweights in consumer cyclicals and communications. We are comfortable being highly selective, allocating capital countercyclically as spread widening presents idiosyncratic opportunities.

Portfolio Review

High Income Fund A Shares (without sales charge*) posted a return of 1.17% in the second quarter 2023. Holdings across the high-yield rating spectrum contributed to performance, with B-rated issues seeing the greatest success and our exposure to CCC paper lagging. Consumer cyclicals and industrials were the leading contributors among market sectors, while financials and communications lagged. The High Income Fund underperformed the Bloomberg US Corporate High Yield Index in the period.

The leading contributors to performance during the quarter were Triton Water Holdings Inc. 6.25%, due 4/1/2029; Consensus Cloud Solutions Inc. ( CCSI ) 6.0%, due 10/15/2026; Carnival Corporation ([[CCL]], [[CUK]], [[CUKPF]]) 5.75%, due 3/1/2027; IHO Verwaltungs GmbH 4.75%, due 9/15/2026; and Petrofac Limited ([[POFCF]], [[POFCY]]), 9.75% due 11/15/2026.

Triton Water Holdings was formed by a private equity-backed leveraged buyout of Nestlé Waters North America in 2021, and in 2022, it was renamed BlueTriton Brands. It manufactures bottled water under brands, including Poland Spring, Deer Park, and Pure Life, and operates a customizable water and beverage delivery service. Following the leveraged buyout, the company’s new management team implemented a number of operational improvements, which provided support for these notes during the quarter.

Consensus Cloud Solutions provides secure information delivery and communications services with a software-as-a-service platform for the health care, financial services, law, and education industries. The company has been performing well, with most of its sales growth coming from the health care sector.

The corporate bonds of leisure travel company Carnival performed well as the company reported improvements in demand and expenses. The company’s post-Covid recovery had lagged its competitors because of its bigger exposure to Europe, which was slower to reopen compared to other geographies.

IHO Verwaltungs is a holding company whose main assets include German auto parts manufacturers Schaeffler AG ( SFFLY ) and Continental AG ( CTTAF ). The company has been executing well, and improving sentiment about the global economy also has been a tailwind.

Energy services company Petrofac provides engineering and construction for clients worldwide. The company continues to win new contracts following the disruption to its business from Covid and its leadership and governance overhaul last year.

The leading detractors in the quarter were United Natural Foods, Inc. ( UNFI ) 6.75%, due 10/15/2028; Staples, Inc. 10.75%, due 4/15/2027; Mercer International Inc. ( MERC ) 5.125%, due 2/1/2029; Centene Corporation ( CNC ) 4.25%, due 12/15/2027 and PRA Group, Inc. ( PRAA ) 7.375%, due 9/01/2025.

United Natural Foods is the largest grocery wholesaler in North America. The bonds underperformed on shrinking margins as a result of lower inflation benefits, fewer procurement gains, and higher inventory losses. Management has taken a number of steps to improve efficiency and better manage inventory.

The corporate bonds of office-supply retailer Staples, which also operates Office Depot stores, underperformed because of concerns about ongoing work-from-home trends. We believe the company has been executing well and its credit fundamentals are stable.

Mercer International produces pulp for use in tissues, hygiene products, and printing and writing paper. This position underperformed because of weakness in pulp prices. We believe this is a cyclical slowdown that should not threaten the longer-term outlook on Mercer’s credit fundamentals.

Centene provides insurance and services to government-sponsored and commercial health care programs. Centene’s business has been performing well but rising interest rates weighed on these relative long-duration bonds.

PRA Group purchases, collects, and manages portfolios of nonperforming consumer loans and receivables. The company reported a large net operating loss in its most recent quarter, driven by a decline in expected recoveries for select vintages of its portfolio; though the shortfall in estimated cash collections will be realized over the next several years, accounting rules dictate that the write-down be accounted for in the current quarter. We don’t believe this one-time accounting charge accurately reflects the underlying health of PRA’s business.

We appreciate your confidence and thank you for your support.

Sincerely,

First Eagle Investments

| Footnotes 1. The Fund commenced operations in its present form on December 30, 2011, and is successor to another mutual fund pursuant to a reorganization December 30, 2011. Information prior to December 30, 2011, is for the predecessor fund. Immediately after the reorganization, changes in net asset value of the Class I shares were partially impacted by differences in how the Fund and the predecessor fund price portfolio securities. 2. Inception date shown for the Bloomberg US Corporate High Yield Bond Index matches the High Income Fund Class I shares, which have the oldest since inception date for the High Income Fund. 3. First Eagle Investment Management, LLC (the ‘‘Adviser’’) has contractually agreed to waive and/ or reimburse certain fees and expenses of Classes A, C, I, R3, R4, R5, and R6 so that the total annual operating expenses (excluding interest, taxes, brokerage commissions, acquired fund fees and expenses, dividend and interest expenses relating to short sales, and extraordinary expenses, if any) (‘‘annual operating expenses’’) of each class are limited to 0.94%, 1.69%, 0.69%, 1.04%, 0.79%, 0.69% and 0.69% of average net assets, respectively. Each of these undertakings lasts until February 29, 2024, and may not be terminated during its term without the consent of the Board of Trustees. The Fund has agreed that each of Classes A, C, I, R3, R4, R5, and R6 will repay the Adviser for fees and expenses waived or reimbursed for the class provided that repayment does not cause annual operating expenses (after the repayment is taken into account) to exceed either: (1) 0.94%, 1.69%, 0.69%, 1.04%, 0.79%, 0.69%, and 0.69% of the class’s average net assets, respectively; or (2) if applicable, the then-current expense limitations. Any such repayment must be made within three years after the year in which the Adviser incurred the expense. * Performance for Class A shares without the effect of sales charges and assumes all distributions have been reinvested, and if a sales charge was included values would be lower. Average Annual Returns as of Jun 30, 2023 The performance data quoted herein represent past performance and do not guarantee future results. Market volatility can dramatically impact the Fund’s short-term performance. Current performance may be lower or higher than figures shown. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Past performance data through the most recent month-end are available at www.firsteagle.com or by calling 800-334-2143. The average annual returns for Class A Shares “with sales charge” of the First Eagle High Income Fund gives effect to the deduction of the maximum sales charge of 4.50%. Class I Shares require $1MM minimum investment and are offered without sales charge. There is no minimum subsequent investment amount for Class I Shares. The annual expense ratio is based on expenses incurred by The Fund, as stated in the most recent prospectus. Fee waivers were in effect for some of the periods shown. Had fees not been waived and/or expenses reimbursed, returns would have been lower. Inception date shown for the Bloomberg US Corporate High Yield Bond Index matches the High Income Fund Class I shares, which have the oldest since inception date for the High Income Fund. The Fund commenced operations in its present form on 30-Dec-2011, and is successor to another mutual fund pursuant to a reorganization 30-Dec-2011. Information prior to 30-Dec-2011 is for this predecessor fund. Immediately after the reorganization, changes in net asset value of the Class I shares were partially impacted by differences in how the Fund and the predecessor fund price portfolio securities. A credit rating as represented here is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of credit worthiness of an issuer with respect to debt obligations, including specific securities, money market instruments, or other bonds. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest); ratings are subject to change without notice. Not Rated ((NR)) indicates that the debtor was not rated and should not be interpreted as indicating low quality. For more information on the Standard & Poor’s rating methodology, please visit standardandpoors.com and select Understanding Ratings” under Ratings Resources. The BB credit rating means that there is a higher probability for default of a debt issuer or a debt instrument. This is the grade by S&P and Fitch while the respective grade by Moody’s scale is Ba2. The BB is the second-best non-investment grade. An obligation rated ‘CCC’ is currently vulnerable to nonpayment, and is dependent upon favorable business, financial, and economic conditions for the obligor to meet its financial commitment on the obligation. Risk Disclosures All investments involve the risk of loss of principal. There are risks associated with investing in securities of foreign countries, such as erratic market conditions, economic and political instability, and fluctuations in currency exchange rates. These risks may be more pronounced with respect to investments in emerging markets. Strategies whose investments are concentrated in a specific industry or sector may be subject to a higher degree of risk than funds whose investments are diversified and may not be suitable for all investors. Investments in bonds are subject to interest-rate risk and can lose principal value when interest rates rise. Bonds are also subject to credit risk, in which the bond issuer may fail to pay interest and principal in a timely manner, or that negative perception of the issuer’s ability to make such payments may cause the price of that bond to decline. Recent market conditions and events, including a global public health crisis and actions taken by governments in response, may exacerbate these risks. The Fund invests in high-yield securities (commonly known as “junk bonds”), which are generally considered speculative because they may be subject to greater levels of interest rates, credit (including issuer default), and liquidity risk than investment-grade securities and may be subject to greater volatility. High-yield securities are rated lower than investment-grade securities because there is a greater possibility that the issuer may be unable to make interest and principal payments on those securities. One cannot invest directly in an index. Indices do not incur management fees or other operating expenses. Bloomberg Global Aggregate Bond Index measures the performance of global investment grade debt from 24 local currency markets, including treasury, government-related, corporate, and securitized fixed rate bonds from both developed and emerging markets. The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below and is composed of fixed-rate, publicly issued, non-investment grade debt, is unmanaged, with dividends reinvested, and is not available for purchase. The index includes both corporate and non-corporate sectors. The corporate sectors are Industrial, Utility, and Finance, which include both US and non-US corporations. The holdings mentioned herein represent the following total assets of the First Eagle High Income Fund as of 30-Jun-2023: Triton Water Holdings, Inc. 6.25%, due 4/1/2029 1.04%; Consensus Cloud Solutions, Inc. 6.0%, due 10/15/2026 1.54%; Carnival Corporation 5.75%, due 3/1/2027 1.18%; IHO Verwaltungs GmbH 4.75%, due 9/15/2026 1.58%; Petrofac Limited 9.75%, due 11/15/2026 0.72%; United Natural Foods, Inc. 6.75%, due 10/15/2028 0.72%; Staples, Inc. 10.75%, due 4/15/2027 0.17%; Mercer International Inc. 5.125%, due 2/1/2029 0.35%; Centene Corporation 4.25%, due 12/15/2027 1.38%; Pra Group, Inc. 7.375%, due 9/01/2025. This commentary represents the opinion of the First Eagle High Income Fund portfolio managers as of 30-Jun-2023 and is subject to change based on market and other conditions. The opinions expressed are not necessarily those of the entire firm. These materials are provided for informational purposes only. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed. The Fund’s portfolio is actively managed and holdings can change at any time. Current and future portfolio holdings are subject to risk. The opinions expressed are not necessarily those of the firm. These materials are provided for informational purposes only. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed. The views expressed herein may change at any time subsequent to the date of issue hereof. The information provided is not to be construed as a recommendation to buy, hold or sell or the solicitation or an offer to buy or sell any fund or security. Third-party marks are the property of their respective owners. FEF Distributors, LLC (“FEFD”) ((SIPC)), a limited purpose broker-dealer, distributes certain First Eagle products. FEFD does not provide services to any investor but rather provides services to its First Eagle affiliates. As such, when FEFD presents a fund, strategy, or other product to a prospective investor, FEFD and its representatives do not determine whether an investment in the fund, strategy, or other product is in the best interests of, or is otherwise beneficial or suitable for, the investor. No statement by FEFD should be construed as a recommendation. Investors should exercise their own judgment and/or consult with a financial professional to determine whether it is advisable for the investor to invest in any First Eagle fund, strategy, or product. Investors should consider investment objectives, risks, charges and expenses carefully before investing. The prospectus and summary prospectus contain this and other information about the Funds and may be viewed at www.firsteagle.com or by calling us at 800-747- 2008. Please read our prospectus carefully before investing. Investments are not FDIC insured or bank guaranteed and may lose value. First Eagle Funds are offered by FEF Distributors, LLC, a subsidiary of First Eagle Investment Management, LLC, which provides advisory services. © 2023 First Eagle Investment Management, LLC |

{kind=link}

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

First Eagle High Income Fund 2nd Quarter 2023 Commentary